Tax Deduction at Source (TDS) & Tax Collection at Source (TCS) are the prime mode of collection of Income Tax by the Government. It is imperative that Government takes all such action to widen the net of TDS & TCS and we have seen a hike in this in last couple of years. Now, one of such measures is leading to confusion among the members of the industry.

For years, trading in goods has been outside the scope of TDS/TCS (except some specified products) until we saw the first such change in October 2020, when selling of any goods was brought under the web of TCS from 1st October, 2020.

Now, the same activity has been also brought under TDS from 1st July, 2021. One may wonder how there can be both TCS & TDS on same activity. Though provisions are made in such a way that these compliances are mutually exclusive, there are a number of aspects which needs a discussion. Our intention in this article is to discuss some common hardships in compliance of these & how those can be mitigated.

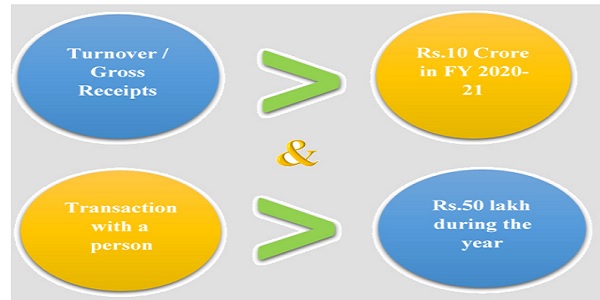

TDS u/s 194Q & TCS u/s 206C(1H) is triggered when both of the below conditions are satisfied. If you are person buying any goods TDS provisions are applicable & if you are a seller, TCS provisions are applicable.

Here comes a dilemma. What if a buyer & seller both have turnover exceeding the limit and transaction value between them is more than 50 lakh? Do both of them need to comply with their respective part of TDS & TCS? The answer is NO. In such a case, TDS is given priority and TCS provisions are not applicable on such transactions.

Let us address some common issues while complying with these sections:

Q1. I am a seller of goods. Do I need to collect tax from my customer in cases, if my turnover was more than Rs.10 crore in last year?

A1. No. Tax Collection is required only when value of goods sold to any single buyer exceeds Rs.50 lakh during the current year (from single or multiple transactions) & tax collection is required only after the limit is exceeded.

Q2. I am a retailer of goods; do I need to deduct TDS on all purchases I make (my turnover was more than Rs.10 crore in last year)?

A2. No. Tax deduction is triggered only when total purchase from a single supplier exceeds Rs.50 lakh during the current year.

Q3. My customer says I should not collect TCS from him & instead he will deduct TDS from payments being made to me on purchase of goods. Is he correct?

A3. Yes. If his turnover was more than Rs.10 crore in last year, he needs to deduct TDS & collection of TCS is not required by you.

Q4. How do I know whether my customer is liable to deduct TDS & whether I need to collect TCS?

A4. This can only be decided after checking the turnover of the buyer. In order to be compliant with the law, it is advisable to obtain a declaration from all regular customers stating whether he is / is not required to deduct TDS from payments being made to you.

Q5. My regular supplier says he has been collecting TCS from me from October 2020 and he will continue to do so this year also. However, I understand that I am also required to deduct TDS from July, 2021. What I need to do?

A5. If your turnover was more than Rs.10 crore in the last year, you are required to deduct TDS from July, 2021. Explicit provisions are made to avoid TDS & TCS on same transaction. In cases where TDS is deducted, collection of tax is not required.

Q6. I am importing goods; do I need to deduct TDS?

A6. TDS is applicable when payments are being made to resident in India. Since you are importing & payments will be made to a non-resident, TDS deduction is not required.

Q7. I am a service provider and my turnover was more than Rs.10 crore in last year. I am purchasing an equipment (capital asset) whose value is more than Rs.50 lakh. Do I need to deduct TDS?

A7. Yes. There are no specific exemptions to service providers. TDS is applicable on all goods purchased irrespective if you deal in those goods or use as a capital asset.

Q8. Do I need to deduct TDS on Software purchases?

A8. Software has always been a matter of litigation. There are various judicial pronouncements which state the transactions in software are to be considered as ‘Goods’. However, this depends on facts of each case. If such purchase of software is treated as a service (royalty), TDS needs to be deducted u/s 194J or 195 and this section is not applicable.

However, if such software acquisition is treated as ‘goods’, this section applies, as no exemptions are given so far.

Q9. What is the meaning of ‘Goods’ in this context?

A9. The term ‘Goods’ is not defined in Income Tax Act, 1961. However, definition of goods in Sale of Goods Act, 1930 can be used in this context. Accordingly, any movable property other than actionable claims & money are goods.

Q10. What is the value to be considered for TDS purpose – inclusive or exclusive of GST?

A10. Unlike other TDS sections, value to be considered here is inclusive of GST.

Q11. Are there any adjustments required for purchase returns etc?

A11. No. TDS needs to be deducted before considering adjustment of purchase returns.

(The above article is only for educational purpose & does not constitute any professional opinion. The author can be reached at ca.ganesh@outlook.com)

Author Bio

Can I file my income tax for 2019-2020?

Insight site for compliance is very slow…how to check 50000 vendors.

informative article..

This is really great content useful for every one who wants to practice on taxation.