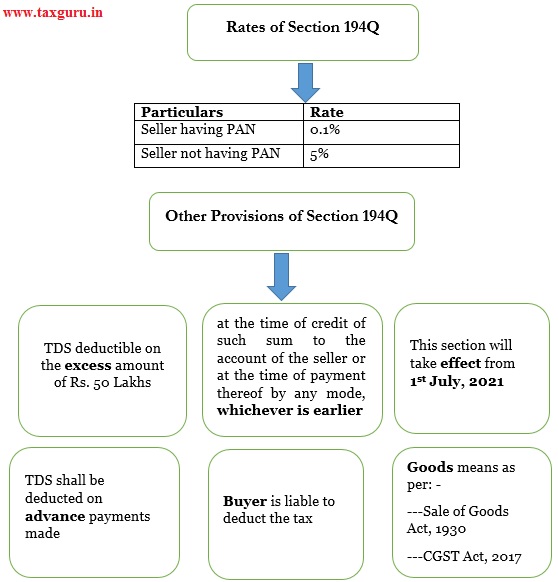

TDS on payment of certain sum for purchase of Goods-New Section 194Q inserted by The Finance Bill Budget 2021-22

Applicability of Section 194Q

This Section Applies to an Assessee (Buyer) whose Gross Receipts/Sales/Turnover in the Preceding financial year Exceed Rs. 10 Crore & when Aggregate amount of purchase from a particular buyer in the financial year Exceeds Rs. 50 Lakh.

Non-Applicability of Section 194Q

- A transaction on which tax is deductible under any provision of the Act

- A transaction, on which tax is collectible under the provisions of section 206C other than transaction to which sub-section (1H) of section 206C applies

Some Scenarios of Section 194Q

| Particulars | Scenario-1 | Scenario-2 | Scenario-3 |

| Turnover of Seller (In Cr.) | 12 | 6 | 12 |

| Turnover of Buyer (In Cr.) | 6 | 12 | 12 |

| Sale of Goods (In Cr.) | 2 | 2 | 2 |

| Sales Consideration paid during the year (In Cr.) | 1 | 1 | 1 |

| Who is liable to deduct or collect tax? | Seller | Buyer | Buyer |

| Rate of Tax | 0.1% | 0.1% | 0.1% |

| Amount on which tax to be deducted or collected (In Cr.) | 0.5 | 1.5 | 1.5 |

| Tax to be deducted or collected | 5,000/- | 15,000/- | 15,000/- |

Compiled by: – CA Ayush Agarwal, CA Piyush Agarwal

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.

Author Bio