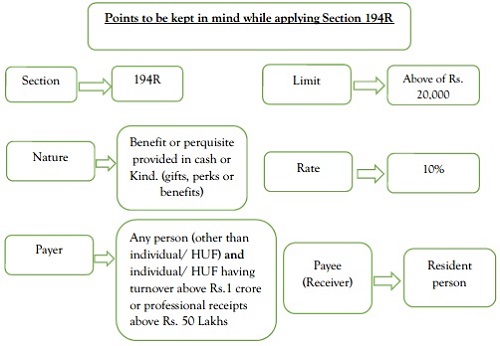

Union Budget 2022, a new TDS section 194R, has been proposed in the Finance Bill 2022, w.e.f. 01st July 2022.

Purpose for Introducing of Sec 194R:

It was observed by department that many companies claimed expenses for business promotions by offering various gifts/ perks/ benefits to its dealers (on fulfillments of conditions of under agreement or as per prevalent norms/ tradition practice followed by over the years by business entity) under section 37 of Income Tax Act 1961, however majority of dealer did not declare the said gifts/ perks/ benefits under business income as required by sec 28 (iv) of Income Tax Act 1961. So to bring such gifts/ perks/ benefits received due to business connections by resident dealers TDS U/s 194R is introduced to track the undeclared income.

–

| Particulars | Scenario-4 | Scenario-5 | Scenario-6 |

| Payer | Ganguly Limited | Ganguly Limited | Ganguly Limited |

| Receiver | Resident person | Resident Employee | Resident person |

| Benefits/perks amount | Rs. 17,000 on 20.06.2022 & Rs. 12,000 on 02.07.2022 | Rs. 85,000 on 20.07.2022 | Rs. 85,000 on 20.07.2022 |

| Applicability of section 194R | Yes | No | Yes |

| Reason | Exceeds aggregate limit of Rs. 20,000 ( whole FY amount considered for calculation of limit) | Benefits provided to employees, TDS deduction u/s 192 not u/s 194R | Exceeds aggregate limit of Rs. 20,000 |

| TDS on Amount | 29,000.00 | NA | 85,000.00 |

| TDS Amount | 2,900.00 | NA | 8,500.00 |

–

| Particulars | Scenario-7 | Scenario-8 | Scenario-9 |

| Payer | Ganguly Limited | Ganguly Limited | Ganguly Limited |

| Receiver | Resident person | Resident person | Resident person |

| Benefits/perks amount | Rs. 94,000 on 28.06.2022 | Rs. 94,000 on 28.07.2022 of Trade discount | Rs. 14,000 on 22.06.2022 & 22,000 on 10.10.2022 on the occasion of Diwali |

| Applicability of section 194R | No | No | No |

| Reason | Benefits given before 01.07.2022 | Trade discount is not a benefits, (if agreement specially mentioned for incentive than only TDS deductible) | Limit doesn’t exceed of Rs. 20,000 (Rs. 22,000 given on the occasion of Diwali which is not in the relation to business) |

| TDS on Amount | NA | NA | NA |

| TDS Amount | NA | NA | NA |

–

| Particulars | Scenario-10 | Scenario-11 | Scenario-12 |

| Payer | Dravid sports club | Ganguly Limited | Mr. Proprietor (Turnover below Rs. 1 crore) |

| Receiver | Resident person | Resident person | Resident person |

| Benefits/perks amount | Rs. 1,50,000 on 15.08.2022 of winning games | Rs. 34,000 on 22.07.2022 & 22,000 on 10.10.2022 on the occasion of Diwali | Rs. 80,000 on 15.07.2022 |

| Applicability of section 194R | No | Yes | No |

| Reason | Amount given for winning lottery /games TDS will be deducted u/s 194B not u/s 194R | Limit exceeds of Rs. 20,000 (TDS non deduction on Rs. 22,000 due to given on the occasion of Diwali which is not in the relation to business) | Payer is individual having turnover below Rs. 1 crore |

| TDS on Amount | NA | 34,000.00 | NA |

| TDS Amount | NA | 3,400.00 | NA |

Compiled by: – CA Ayush Agarwal | CA Piyush Agarwal

Author Bio