Q. 1 The newly enacted section 194O of Income tax Act, 1961 TDS on which entities and what goods and services ?

Every E-commerce operator (like Amazon, Facebook, Flipkart, Snapdeal etc.) is required to make TDS on payments due to ‘e-commerce participants’ i.e., suppliers ( who are resident in India) on sale of goods or provision of services (including digital services) facilitated by it through its digital or electronic facility or platform. ‘Services’ include ‘fees for technical services’ and fees for ‘professional services’.

Q. 2 From which date has the new Section 194O comes into force?

The new Section 194-0 has been introduced in the Union Budget, 2020 and has come into force from 1st October, 2020.

Q. 3 What is the rate at which TDS is required to be deducted?

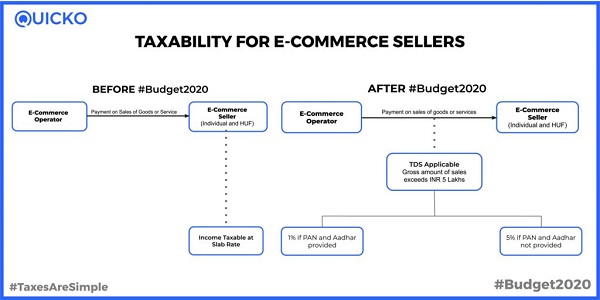

The e-Commerce operator has to deduct TDS @ 1% at the time of credit of the amount to an e-Commerce participants or at the time of actual payment thereof to such e-Commerce participants by any mode, whichever is earlier. The payment should be towards the sale of goods, services or both. The TDS is to be made @ 1% of the gross amount of sales.

Q 4. Obligations of supplier ?

The supplier ( i.e.,) should furnish its PAN or Aadhar to the E-commerce operator. Otherwise, the e-commerce operator will deduct TDS @ 5%.

Q. 5 Are there any exceptions to section 194-0?

(i) No TDS will be made if the supplier is an individual or Hindu Undivided Family (HUF) and where the gross amount of sale of goods, services or both during the (financial) year does not exceed Rs. 5,00,000/- (Rs. Five Lakhs) and such individual/HUF e-Commerce participant furnishes his PAN or Aadhar to the e-Commerce operator).

(ii) No TDS is required if the”e-commerce participant” is a non-resident

(iii) No TDS shall be made for amounts received or receivable by an e-commerce operator for hosting advertisements or providing any other services which are not in connection with the sale or services as mentioned above.

Q. 6 An illustrative example.

e-Commerce operator -XYZ Ltd.

e-Commerce participant-ABC Ltd

ABC Ltd. sells its goods through XYZ Ltd to one Mr. Rohan on online platform for Rs. 59,000/- (which includes GST of Rs. 9,000/) on 1st November,2020.

XYZ Ltd. credits the amount to ABC Ltd. on 1st November, 2020 and Mr. Rohan makes the payment to ABC Ltd. on 15th November 2020.

In this case, XYZ Ltd. is required to deduct TDS @ 1% on Rs. 50,000/- (i.e. Rs. 500/-) on 1st November 2020.

Q. 7 Is there any notification issued by CBDT with respect to section 1940?

The CBDT has issued circular no 17 of 2020 with respect to section 194-0 containing the following guidelines-

(i) Provisions of section 194-0 shall not be applicable in relation to

a. Transactions in securities and commodities.

b. Transactions in electricity.

c. Transactions in renewable energy certificates and energy saving certificates.

(ii) The payments for the e-Commerce is usually facilitated by some third party payment gateways e.g. Billdesk; such payment gateways will not be required to deduct TDS u/s 194-0, if the tax has been deducted by the e-Commerce operator u/s 194-0 of the Act, on the same transaction.

(iii) An insurance agent or insurance aggregator who has no involvement in transactions between insurance company and the buyer of insurance policy, he would not be liable to deduct tax u/s 194-0 of the act for those subsequent years except first year.

(iii) For the calculation of the threshold of Rs. 5,00,000/- for an individual/HUF (being e-Commerce participant furnishing PAN/Aadhar in respect of such previous year) of sale of goods, services or both for which the deduction u/s 194 is applicable, shall be counted from 1st April, 2020.

Q9. What should be the resident status of e-Commerce operator?

Section 194-0 is applicable to both resident and non-resident e-Commerce operators which are fulfilling the other conditions under this section.

Image Source- Quicko