Case Law Details

T Srikanth Vs DCIT (ITAT Chennai)

Summary: The ITAT Chennai allowed the assessee’s appeal, holding that the deeming fiction under Section 50C is confined to computation of capital gains under Section 48 and cannot be extended to determine the “net consideration” for exemption under Section 54F. The assessee had disclosed actual sale consideration of Rs. 2.03 crore from the sale of one shop and four immovable properties and invested Rs. 2.16 crore in purchase of land and construction of a residential house, claiming full exemption under Section 54F. The Assessing Officer substituted the stamp duty value under Section 50C, proportionately restricted the exemption, and taxed the balance capital gains, while the CIT(A) directed recomputation after the DVO’s report but did not accept the principal contention on Section 54F. The Tribunal held that “net consideration” under Section 54F refers to the actual consideration received and not the deemed value under Section 50C, observing that the statutory fiction cannot be extended beyond its purpose and that, absent proof of higher actual consideration, the assessee cannot be required to invest more than what was received. Since the entire actual sale consideration had been invested in the new residential house, the full exemption under Section 54F was allowed, and the alternate issue regarding agricultural land was left open.

Core Issue. Whether the deeming fiction under section 50C, which substitutes the stamp duty value as the full value of consideration for computing capital gains under section 48, can also be applied while determining the “net consideration” for the purpose of exemption under section 54F.

Facts. The assessee earned long-term capital gains from the sale of one shop and four immovable properties and disclosed actual sale consideration of Rs.2.03 crore. The entire sale consideration was invested in purchase of land and construction of a residential house aggregating to Rs.2.16 crore, and full exemption under section 54F was claimed.

During scrutiny, the Assessing Officer invoked section 50C and substituted the stamp duty value of Rs.4.64 crore as the deemed full value of consideration. Though the valuation was referred to the DVO, the assessment was completed before receipt of the valuation report. By treating the deemed value under section 50C as the “net consideration” for section 54F, the Assessing Officer proportionately restricted the exemption and brought the balance capital gains to tax. The CIT(A), after receipt of the DVO’s report, directed recomputation of capital gains but did not accept the assessee’s principal contention regarding section 54F.

Tribunal’s Analysis: The Tribunal held that the legal fiction created by section 50C is confined exclusively to the computation of capital gains under section 48 and cannot be extended to any other provision unless the statute expressly so provides.

It observed that section 54F employs the expression “net consideration”, which is specifically defined as the actual consideration received or accruing on transfer, reduced by expenditure incurred wholly and exclusively in connection with such transfer. The Legislature has consciously used the expression “net consideration” in section 54F and not the deemed “full value of consideration” referred to in section 50C.

The Tribunal reiterated the settled principle that a statutory fiction must be strictly confined to the purpose for which it is enacted. Importing the deeming fiction of section 50C into section 54F would compel an assessee to invest an amount which he never actually received, leading to an impossible and unintended consequence. Unless the Revenue establishes that the assessee actually received consideration over and above the amount stated in the registered sale deed, exemption under section 54F cannot be denied merely because the stamp valuation authority adopted a higher value.

Since the assessee had invested more than the entire actual sale consideration received from the transfer in acquiring a new residential house, the statutory requirement of section 54F stood fully satisfied. Consequently, the entire capital gain was exempt notwithstanding the higher deemed consideration adopted under section 50C for computing capital gains.

Having allowed the appeal on this legal issue, the Tribunal left open the alternate contention that the lands sold were agricultural lands, holding the issue to be academic.

Cases Relied Upon

Mancheri Puthusseri Ahmed & Ors. v. Kuthiravattam Estate Receiver (1996) 6 SCC 185 (Supreme Court) – Statutory deeming fiction cannot be extended beyond the purpose for which it is created.

CIT v. Smt. Nilofer I. Singh (2009) 309 ITR 233 (Delhi High Court) – Meaning of “full value of consideration” outside section 48 cannot automatically be governed by section 50C.

CIT v. Ace Builders (P.) Ltd. (2006) 281 ITR 210 (Bombay High Court) – Legal fiction must remain confined to the provision creating it.

CIT v. Assam Petroleum Industries (P.) Ltd. (2003) 262 ITR 587 (Gauhati High Court) – Deeming provisions are to be strictly construed.

Mrs. Baskarababu Usha v. ITO (2022) 135 taxmann.com 307 (ITAT Chennai) – Section 50C cannot be imported into section 54F while computing exemption.

DCIT v. Dr. Chalasani Mallikarjuna Rao (2016) 161 ITD 721 (ITAT Visakhapatnam) – Actual consideration, and not deemed consideration under section 50C, is relevant for section 54F.

Mr. R. Srinivasan (HUF) Versus The Income Tax Officer, Ward I (1), Trichy – 2016 (8) TMI 1092 – ITAT CHENNAI

Shri Shivkumar Lakshman v. The Income Tax Officer, International Taxation – I in ITA No. 402/Mds/2015

Gyan Chand Batra v. ITO (2010) 8 taxmann.com 22 (ITAT Jaipur) – Section 50C is restricted to section 48 and cannot be applied for determining “net consideration” under section 54F.

Decision. The appeal was allowed. The Tribunal held that the deeming fiction under section 50C is confined to computation of capital gains under section 48 and cannot be imported into section 54F. Since the assessee had invested the entire actual sale consideration in the new residential house, the whole of the capital gain was exempt under section 54F. The alternate issue regarding the agricultural nature of the land was left open.

FULL TEXT OF THE ORDER OF ITAT CHENNAI

This is an appeal preferred by the assessee against the order of the Learned Commissioner of Income Tax (Appeal)/NFAC, (hereinafter referred to as ‘Ld.CIT(A)’), Delhi, dated 07.10.2025 for the Assessment Year (hereinafter referred to as ‘AY’) 2017-18.

2. Brief facts of the case are that the appellant is the legal heir/son of deceased Shri Skandhakumar Tellakulla who was the assessee in this case. The appellant’s father-assessee had filed his return of income (RoI/ITR) for AY 2017-18 wherein he admitted long term capital gain (LTCG) of Rs.1,97,94,679/- arising from sale of five properties (one shop and four land). And since he had invested an amount of Rs. 2,15,67,970/-in purchase of land and constructed a new residential house, he claimed the entire capital gains as exempt under section 54F, on the plea that the investment made in residential house was more than the net consideration received by him from transfer of shop & land. Later, the ITR of assessee was selected for scrutiny and the AO examined the claim of assessee regarding LTCG & deduction claimed under Section 54F; and thereafter, the AO in respect of sale value of the transferred lands in question, invoked section 50C and adopted deemed guideline value of the four (4) lands as the full value of consideration i.e. Rs 4,63,87,220/-. And the AO finding that since the assessee had invested for the new residential house only Rs. 2,15,67,970/-, which is less than the deemed guideline value of the four (4) lands, gave show cause to proportionately disallow the exemption under section 54F of the Act.

3. The assessee objected to the aforesaid proposal firstly on the ground that the lands sold were agricultural property, and hence they were not ‘capital asset’ and hence capital-gain is not attracted on its transfer. Secondly, the proposal to adopt guideline value was erroneous, since fair market value of the lands were less than the guideline value and pleaded for referring the same to the DVO; and thirdly, assessee objected to the adoption of the value as per section 50C as net consideration for the purpose of calculating exemption under section 54F of the Act. The AO in light of the objections raised by assessee, first of all rejected the claim of assessee that the land-sold were agricultural property, but referred the valuation of the four land in question to the DVO, but since DVO couldn’t give the report within the time barring period, the AO invoked section 50C and adopted deemed guideline value of the four (4) lands as the full value of consideration i.e. Rs 4,63,87,220/- and computed the LTCG at Rs 4,58,81,899/-. And the AO finding that since the assessee had invested for the new residential house only Rs. 2,15,67,970/-, [which is less than the guideline value of the four (4) lands, i.e. Rs 4,63,87,220/-] computed the deduction eligible u/s 54F at Rs 2,13,33,018/- and hence according to him, capital gains to be brought to tax is Rs 2,45,48,881/- (Rs 4,58,81,899/- minus Rs 2,13,33,018/-).

4. Aggrieved, the assessee filed an appeal against the assessment order. And during the pendency of appeal before the Ld.CIT(A), the assessee passed away and the Appellant herein, being the legal heir stepped-in and has pursued the appeal. During the pendency of the appeal, the valuation report of the DVO was received determining the Appellant’s share of the fair market value of the lands in question. And the Ld.CIT(A) reproduced the valuation report given by the DVO at page 33 of his order and directed the AO to recompute the amount of longterm capital gain after allowing all deductions as per the Act, but the Ld.CIT(A) dismissed the appeal. In this regard, the Ld.AR of the assessee/appellant brought to our notice that till date, the AO hasn’t passed any order giving effect to the order of the CIT(A) by considering the value determined by the DVO for the purpose of section 50C of the Act. Table below will give the values adopted by the AO and determined by the DVO for the purpose of section 50C of the Act in respect of the lands transferred by the assessee:

| Particulars | Value adopted by the AO | Value determined by the DVO |

| Sale of Nanjai Land at Thirukovilur, Survey No. 133/2 (Document No. 3133 of 2016) | 42,50,000 | 58,26,500 |

| Sale of Nanjai Land at Thirukovilur, Survey No. 134/1 (Document No. (Document No. 3134 of 2016) | 20,60,100 | 14,17,000 |

| Sale of Nanjai Land at Thirukovilur, Survey No. 168/1 and 168/2 (Document No. 3135 of 2016) | 1,47,54,240 | 74,01,000 |

| Sale of Nanjai Land at Thirukovilur, Survey No. 345/1B, 345/2B and 348/1B (Document No. 3136 of 2016) | 2,53,22,880 | 1,27,02,500 |

| Total | 4,63,87,220 | 2,73,47,000 |

5. The Appellant is noted to have raised various ground before this Tribunal including the ground that the lands sold by the Appellant’s father/assessee were agricultural lands and thus, they are not capital assets and hence doesn’t attract capital gain from transfer of such property; (ii) and that the deeming fiction under section 50C has to be applied only for the purpose of computing capital gains under section 48 and not for the purpose of computing deduction under section 54F and hence, claimed that since the entire consideration as shown in sale-deed of Rs. 2,03,00,000/- has been fully invested in the new residential house, the Appellant is entitled to full deduction under section 54F. Further, according to the Ld.AR, anyway, the AO was bound to adopt the value determined by the DVO for the purpose of section 50C, and pointed out that if the value determined by DVO exceeds the guideline value of the property, by applying section 50C(3), only the guideline value should be considered for the purpose of section 50C of the Act. And in this regard, brought to our notice that in respect of Survey No. 133/2 (Document No. 3133 of 2016), since the value determined by DVO exceeds the guideline value of the property, only the guideline value is required to be considered for the purpose of section 50C of the Act.

6. Having noted the grounds supra, before us however, the Ld.AR submitted that for argument sake even if it is assumed that the lands sold by assessee were not agricultural lands, still, in the facts of the present case, no capital gains shall be chargeable on the ibid transfer of properties because assessee has fully utilized the sale-consideration leave alone the net-consideration from transfer of original-assets for purchase of new asset (i.e. land and construction of new residential house); and hence, assessee is entitled for exemption u/s.54F of the Act, and no capital gain is taxable in the facts of the case. Explaining on this issue, the Ld AR submitted, it can’t be disputed that assessee is entitled for exemption u/s.54F, and because the consideration from transfer of original-assets has been utilized for residential house, hence no addition is warranted in the facts of the case. In this regard, the Ld AR submitted, Section 54F(1) provides that (a) if the cost of the new asset is not less than the net consideration in respect of the original asset, the whole of such capital gain shall not be charged under section 45; (b) if the cost of the new asset is less than the net consideration in respect of the original asset, so much of the capital gain as bears to the whole of the capital gain, the same proportion as the cost of the new asset bears to the net consideration, shall not be charged under section 45. Thus, according to him, for calculating the quantum of exemption under section 54F, a comparison of “cost of the new asset” is made with the “net consideration” and where the cost of new asset is less than the net consideration, proportionate capital gains is exempt as per the following formula: – ‘Capital gains * Cost of new asset / Net consideration’

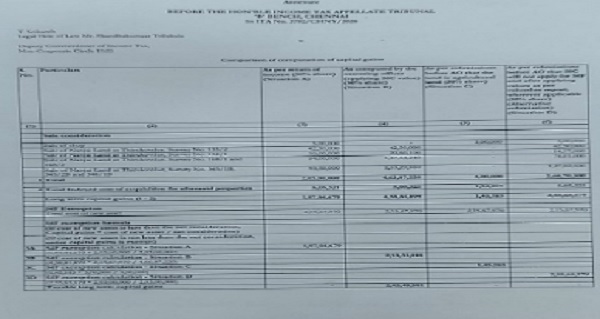

7. Referring to the above formula, the Ld AR pointed out that the AO has sought to adopt the deemed full value of consideration as determined under section 50C in the denominator instead of the actual sale consideration received by the assessee/appellant’s father. A comparison chart showing the computation of capital gains as admitted in the return of income, as computed by the AO and as computed based on the values provided by the DVO is enclosed as Annexure.

8. A perusal of the chart, according to Ld AR, show that the Appellant’s father has received only Rs. 2,03,00,000/- as net consideration in respect of the sale of one shop and four (4) lands, whereas the AO has adopted the value as per section 50C not only for the purpose of computing capital gains, but also for the purpose of calculating exemption under section 54F. Drawing our attention to row 3B of the chart, he showed us that the AO has adopted the guideline value as the denominator while calculating the exemption under section 54F, which is erroneous.

9. The thrust of the assessee’s assertion is that deeming provision of section 50C is only for adopting the guideline value as fair market value (FMV) if sale consideration shown in sale-deed is less than the guideline value, for the purpose of computing capital gain under section 48 and not for the purpose of calculating “net consideration” under section 54F. In section 50C the deeming fiction is for adopting “full value of consideration” for the purpose of computing capital gain under section 48 of the Act, whereas the term used in under section 54F is “net consideration” from transfer of original asset and not “full value of consideration” as stated in section 50C of the Act. The Appellant submits that, since the actual sale consideration on transfer of assets is of Rs. 2,03,00,000/-, which has been fully invested by the assessee in a residential house in accordance with section 54F, the whole of the capital gains is eligible for exemption. In other words, section 54F only requires the investment of the actual sale consideration received by or accruing to the assessee as a result of transfer and not the deemed full value of consideration as per section 50C of the Act. The said deemed full value of consideration is a fiction created by the statute, in order to discourage persons from lowering the price of the property for avoiding payment of stamp-duty while registering the transfer of property and then pay the balance amount of consideration in cash (on-money). However, unless it is proved by the Revenue, that assessee received consideration more than what parties has shown in the registered sale-deed, the assessee cannot be expected to invest more than what he received from the purchaser. In other words, what could have been invested by the assessee to avail deduction under section 54F can only be the actual sale consideration received by him and not the deemed consideration u/s 50C. Thus, according to him, reading section 50C into section 54F for determining the net consideration in the denominator would tantamount to requiring the Appellant to do an impossible act. Hence according to Ld AR, irrespective of whether the capital gains is calculated on the basis of actual consideration or the value as per section 50C, since the amount invested by the assessee being more than the actual net consideration received by him, entire capital gain is eligible for exemption under section 54F. Therefore, according to the Ld.AR, for the purpose of determining exemption under section 54F, it is only net consideration received which has to be taken into account in the denominator and the same does not get altered by substituting the value as per section 50C (irrespective of whether the guideline value or the value determined by DVO is adopted under section 50C). Thus, the calculation of exemption under section 50C ought to be as per row 3D of the chart supra.

10. For the aforesaid proposition, the Ld.AR relies on the following orders of this Tribunal: –

A. Shri Baskarababu Usha v. Income-tax Officer [2022] 135 taxmann.com 307 (Chennai – Trib.)

B. Mr. R. Srinivasan (HUF) Versus The Income Tax Officer, Ward I (1), Trichy – 2016 (8) TMI 1092 – ITAT CHENNAI

C. Shri Shivkumar Lakshman v. The Income Tax Officer, International Taxation – I in ITA No. 402/Mds/2015

D. Gyan Chand Batra v. Income-tax Officer [2010] 8 com 22 (Jaipur)

11. He drew our attention to para 11 of the order of this Tribunal in the case of Mrs. Baskarababu Usha v. Income-tax Officer [2022] 135 taxmann.com 307 (Chennai – Trib.) wherein it has been held that deeming fiction under section 50C cannot be applied while calculating exemption under section 54F. It would be gainful to read the observation, which is noted as under: –

“11. As regards adoption of deemed consideration for the purpose of exemption u/s 54F of the Income-tax Act 1961, the Assessing Officer has adopted deemed consideration and computed eligibility for exemption u/s.54F of the Act. The deeming fiction provided for computing full value of consideration as a result of transfer of property as per provisions of section 50C of the Act is only applicable for determining full value of consideration as defined u/s.48 of the Act and thus, for the purpose of computing exemption u/s.54F of the Act, deeming fiction provided u/s.50C cannot be enlarged because, one cannot expect a person to perform impossible things, as when the assessee receives a particular amount from transfer of property, he cannot be expected to reinvest amount over and above consideration received for transfer of property. In fact, that may not be intention of the legislature. If you apply deeming fiction provided u/s.50C to provisions of section 54F of the Act, for computation of exemption, then it is impossible for assessee to fulfil said conditions because no assessee will have consideration over and above what was received from transfer of property. This principle is supported by the decision of ITAT., Visakhapatnam Bench in the case of Dy: CIT v. Dr. Chalasani Mallikarjuna Rao [2016] 75 taxmann.com 270/161 ITD 721. Therefore, we are of the considered view that the Assessing Officer has erred in adopting deemed consideration for the purpose of computation of exemption u/s. 54F of the Income-tax Act, 1961

12. In view of the above submissions, the Appellant-assessee prays that the exemption under section 54F be allowed in full and prays that the other issues including that the lands are agricultural properties be left open.

13. Per contra, the Ld.DR fully supported the impugned action of the Ld.CIT(A) and doesn’t want us to interfere.

14. Heard both the parties. The assessee in this case had filed his return of income returning a total income of Rs.19,10,850/- wherein, he has computed long-term capital gain (LTCG) by adopting his share of 50% consideration received from sale of shop and four (4) immovable properties/lands (hereinafter referred to as ‘the Original Asset’), wherein he has shown the LTCG at Rs.1,97,94,679/- [after deducting index cost of acquisition of the immovable properties of Rs.5,05,321/-]. The assessee also claimed the entire long-term capital gain of Rs.1,97,94,679/- as exempt u/s.54F of the Act for investing the entire sale consideration of Rs. 2,03,00,000/- for purchase of land & construction of new residential house/asset (hereinafter referred to as ‘New Asset’). During the course of assessment proceedings, the AO called for details of the sale of original assets and noted from perusal of the registered sale deed that the sale consideration recorded therein was Rs. 2,03,00,000/- (i.e.50% of the share) and noticing that guideline value as determined by stamp-duty authority for the properties sold were more, proposed to adopt the value of the property as per provisions of Section 50C of the Act, i.e. market value as determined by stamp-duty authority/guideline value of the properties for computing the capital gain from the transactions. Pursuant to the same, assessee filed his objections by raising two (2) issues i) that the four (4) immovable properties sold by him were agricultural lands and thus they are not ‘capital-assets’ and therefore, question of capital gain doesn’t arise from such transfer. And ii) assessee contested the adoption of market value as determined by stamp valuation authority, since the market value of the immovable properties were less than what was determined by stamp-duty authorities. Accordingly, the AO referred the valuation of property to the departmental valuer (DVO), after rejecting the assessee’s claim that lands sold were agricultural properties; and when the reference to DVO was pending, the AO called upon the assessee to justify the exemption claimed u/s.54F of the Act. In response, the assessee submitted that details incurred for purchase of land and construction of residential house/new asset as Rs.2,15,67,970/- and therefore, claimed that the entire capital gain derived from sale of properties was eligible for exemption u/s.54F of the Act. The AO, however, was not convinced with the explanation given by the assessee and in the absence of DVO report, the AO is noted to have adopted the deemed full value of consideration as determined u/s.50C of the Act i.e. Rs 4,63,87,220/- for the purpose of computing the LTCG at Rs 4,58,81,899/-and finding that since the assessee had invested for the new residential house only Rs. 2,15,67,970/-, [which is less than the guideline value of the four (4) lands, i.e. Rs 4,63,87,220/-] computed the deduction eligible u/s 54F at Rs 2,13,33,018/- and hence according to him, capital gains to be brought to tax Rs 2,45,48,881/- (Rs 4,58,81,899 minus Rs 2,13,33,018). On appeal, the Ld.CIT(A) after considering the DVO report is noted to have given direction to the AO to recompute the amount of long-term capital gain accordingly, after allowing all deductions as per the Act.

15. Still note satisfied, the assessee is before us and has reiterated that the four (4) immovable properties sold by the assessee were agricultural lands; and secondly, has raised an alternate ground that the deeming fiction under section 50C has to be applied only for the purpose of computing capital gains under section 48 and not for the purpose of computing deduction under section 54F and hence, claimed that since the entire consideration as shown in sale-deed of Rs. 2,03,00,000/- has been fully invested in the new residential house/new-asset, the Appellant is entitled to full deduction under section 54F.

16. We will first of all take up the alternate ground. Considering the facts and circumstance of the case, we are of the view that on transfer of the original assets, capital-gain is not chargeable u/s 54F since assessee has invested the entire consideration from transfer of the original assets in construction of new-asset. Reason for such a conclusion is that in this case, the sale-consideration disclosed in the sale-deeds is Rs. 2,03,00,000/- (i.e.50% of the share), and assessee in this case has invested in constructing new asset Rs.2,15,67,970/-, which fact is not disputed. Hence assessee is noted to have fulfilled the condition for being entitled for exemption u/s 54F of the Act and consequently, no capital-gain is chargeable to tax, even if the capital gain is computed by adopting the value as per section 50C of the Act.

17. The Authorities in this case, for restricting/disallowing the claim of exemption u/s 54F is noted to have adopted the ‘full value of consideration’ as defined under the provisions of section 50C of the Act. The question for consideration is for the purpose of exemption u/s. 54 of the Act, the ‘full value of consideration’ as defined under the provisions of section 50C of the Act is applicable or actual consideration received as a result of transfer of original asset. It should be borne in mind that the provisions of section 50C of the Act, comes into play when the sale consideration is less than value adopted by any authority of the State Government for the purpose of payment of stamp duty in respect of transfer of assets, whereas, section 54 of the Act provides for exemption where the assessee invests ‘net sale consideration’ for the purpose of acquiring new house, then the cost of new house shall be allowed as deduction in computing the capital gains. The term ‘net sale consideration’ has been defined to mean the full value of the consideration received or accrued as a result of the transfer of the capital asset after deduction of any expenditure incurred, wholly and exclusively in connection with transfer. Thus it can be seen that the term ‘net consideration’ used in section 54F is contra distinct to the term deemed ‘full value of consideration’ as referred to in section 50C, which is only for purpose of computing capital gains u/s 48 of the Act and such deeming provision cannot be extended for the purpose of determining the exemption given u/s 54F of the Act because legislature in its wisdom has used the term ‘net consideration’ and not ‘full value of consideration’ as defined under the provisions of section 50C of the Act. It is settled that in construing the fiction, it is not to be extended beyond the purpose for which it is created, or beyond the language of the section by which it is created. In the case of Mancheri P Ahmed v. Kuthiravattam Estate Receiver (1996) 6 SCC 185, the Hon’ble Supreme Court observed that deeming provision cannot be extended by importing another fiction. Hence, deeming provision created for section 50C will not be applicable to section 54F so far as the meaning of full value of consideration is concerned as deeming provision mentioned in section 50C is for specific asset and for the purpose of section 48 of the Act. Hence the assessee is entitled for deduction under s. 54F of the Act.

18. Moreover, the net sale consideration as a result of transfer of capital asset is a consideration received or accrued as a result of transfer. And as noted, there is difference between ‘net sale consideration’ and ‘full value consideration’. In our considered view, if the assessee invests net sale consideration for the purpose of purchase/construction of new residential house property, then assessee is eligible for exemption u/s. 54 of the Act, even though the ‘full value of consideration’ is more than the net sale consideration as a result of transfer. As discussed, the deeming fiction as provided u/s. 50C of the Act in respect of the words ‘full value of consideration’ is to be applied only to section 48 of the Act and therefore meaning of full value of consideration as referred to in explanation to section 54F(1) of the Act is not governed by the meaning of the words full value of consideration as mentioned in section 50C of the Act as held by the coordinate bench of ITAT Jaipur in the case of Gyan Chand Batra v. ITO [2010] 8 taxmann.com 22. It would be gainful to refer to the relevant portion of the order, which is extracted below:

From sub-s. (1) of s. 50C, it is clear that in case the consideration received is less than the value adopted by stamp valuation authority then the value so adopted is to be taken as full value of the consideration for the purposes of 5. 48. Sec. 50C provides a deeming provision for considering the full value of consideration as the value adopted for stamp duty. In modern statutes, the expression ‘deem’ is used a great deal and for many purposes. It is at times used to introduce artificial conceptions which are intended to go beyond legal principles or to give an artificial construction of a word for phrase, Thus the artificial meaning of full value of the consideration has been given in s. 50C for the purpose of s, 48. One is entitled to ascertain the purpose for creating a statutory fiction. After ascertaining the purpose, full effect must be to the statutory fiction and it should be carried to its logical conclusion and to that end, it be proper and even necessary to assume all those facts on which alone fiction can operate legislature in its wisdom has referred to s. 48 in s. 50C for adopting the same value market value. Hence, the deeming fiction as provided in s. 50C in respect of the word value of consideration’ is to be applied only for s. 48. The words ‘full value of consideration mentioned in other provisions of the Act are not governed by the meaning of full value consideration as contained in s. 50C. The natural meaning of full value of consideration refers to consideration specified in the sale deed. Hence, for the meaning of full value of consideration mentioned in different provisions of the Act except in s. 48, one will have to consider it value of consideration as specified in sale deed. -CIT v. Smt. Nilofer 1. Singh (2009) 22 (Del) 277: (2008) 14 DTR (Del) 108: (2009) 309 ITR 233 (Del)relied on. (Para 7.1)

In Explanation to s. 54F(1), it is mentioned that net consideration means the full value a consideration received or accruing as a result of the transfer of the capital asset as reduced by any expenditure incurred wholly and exclusively in connection with such transfer. The meaning of full value of consideration in Explanation to s. 54F(1) will not be governed by meaning o words ‘full value of consideration’ as mentioned in s. 50C. The value adopted for stamp duty is to be considered as full value of consideration for the purpose of computing the capital gains under s. 48. Sec. 54F(1) says that capital gains is to be dealt with in accordance with the provisions of sub-cls. (a) and (b) of s. 54F(1). In the instant case, the cost of new asset is not less than the net consideration thus the whole of the capital gains will not be charged even if the capital gains has been computed by adopting the value adopted by stamp registration authority. It is clearly mentioned in s. 54F(4) also that net consideration which is not appropriated towards the purchase of new asset the same is to be taxed in case such net consideration not appropriated is not deposited in the capital gain account It is not necessary that the new asset should be got registered before filing of the return. The requirement of law is that net consideration is required to be appropriated towards the purchase of the new asset. Thus, deduction under s. 54F is clearly applicable. Deeming provisions as mentioned in s. 50C will not be applicable to s. 54F so far as the meaning of full value of consideration is concerned as deeming provision mentioned in s. 50C is for specific asset and for the purpose of s. 48. Hence the assessee is entitled for deduction under s. 54F.-CIT v. Ace Builders (P.) Ltd. (2005) 195 CTR (Bom) 1. (2006) 281 ITR 210 (Bom) and CIT v. Assam Petroleum Industries (P.) Ltd. (2003) 185 CTR (Gau) 71: (2003) 262 ITR 587 (Gau)applied. (Paras 7.3 to 7.5)”

19. Considering the facts and circumstances of the case and also applying the ratio of the case laws discussed above, we are of the view that the assessee is eligible for exemption u/s. 54 of the Act, if the net sale consideration is invested in construction or purchase of new residential house. In the present case, the assessee has invested the entire sale consideration for construction of new residential house property. Hence, though, the full value of consideration as defined u/s. 50C of the Act is more than the net sale consideration as referred in section 54F(1) of the Act, once the sale consideration has been fully applied under the provisions of section 54 of the Act, then the deeming consideration as defined u/s. 50C of the Act cannot be imported or read into the provisions of section 54F of the Act. Therefore, we are of the view that the assessee is eligible for exemption u/s. 54 of the Act, therefore, the whole of the capital gain is not chargeable to tax even if the capital gain is computed by taking the value as per the provision of section 50C of the Act. Therefore, we direct the A.O. to allow the exemption u/s. 54 of the Act.

20. In the light of the aforesaid action of ours, the ground raised by the assessee that the original asset (land) sold were agricultural property is not being adjudicated, being academic, is left open.

21. In the result appeal of the assessee is allowed.

Order pronounced on the 07th day of July, 2026, in Chennai.

Author Bio