BARE ACT:

Payment of certain amounts in cash.

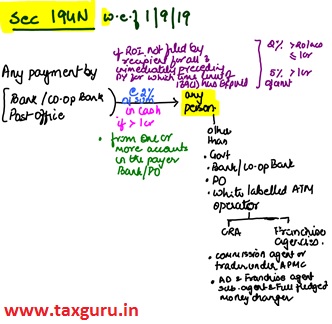

194N. Every person, being,—

i) a banking company to which the Banking Regulation Act, 1949 applies (including any bank or banking institution referred to in section 51 of that Act);

ii) a co-operative society engaged in carrying on the business of banking; or

iii) a post office,

who is responsible for paying any sum, being the amount or the aggregate of amounts, as the case may be, in cash exceeding 1 crore rupees during the previous year, to any person (herein referred to as the recipient) from one or more accounts maintained by the recipient with it shall, at the time of payment of such sum, deduct an amount equal to two per cent of such sum, as income-tax:

SUMMARY

Any payment made by

i) a banking company

ii) a co-operative society engaged in carrying on the business of banking;

iii) a post office,

- to any person (herein referred to as the recipient)

- in cash >1 crore rupees (per Bank)

- during the previous year,

- from one or more accounts(savings/current) maintained by the recipient with it.

- shall, at the time of payment of such sum, deduct an amount equal 2% of such sum, as income-tax on the amount in excess of 1 crore

- Where the relevant PY is 2021-22, the due date of the years that has expired before the start of the year i.e. 01/04/21 will be PY 2019-20, 2018-19, 2017-18.

- The provision is applicable where the assessee has NOT filed the return for any of the 3 years. However where the assessee has filed a belated return, this provision will not be applicable

1st Proviso: Provided that in case of a recipient who has not filed the returns of income for all of the three assessment years relevant to the three previous years, for which the time limit of file return of income under sub-section (1) of section 139 has expired, immediately preceding the previous year in which the payment of the sum is made to him, the provision of this section shall apply with the modification that

i) the sum shall be the amount or the aggregate of amounts, as the case may be, in cash > 20 lac rupees during the previous year; and

ii) the deduction shall be

a) an amount equal to 2% of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash > 20 lacs during the previous year but does not exceed one crore rupees; or

b) an amount equal to 5% of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash exceeds 1 crore rupees during the previous year:

2nd Proviso: Provided further that the Central Government may specify in consultation with the Reserve Bank of India, by notification in the Official Gazette, the recipient in whose case the first proviso shall not apply or apply at reduced rate, if such recipient satisfies the conditions specified in such notification:

3rd Proviso: Provided also that nothing contained in this section shall apply to any payment made to—

(i) the Government;

(ii) any banking company or co-operative society engaged in carrying on the business of banking or a post office;

(iii) any business correspondent of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the guidelines issued in this regard by the Reserve Bank of India under the Reserve Bank of India Act, 1934 (2 of 1934);

(iv) any white label automated teller machine operator of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 (51 of 2007):

Analysis: No tax is required to be deducted at source under section 194N on cash withdrawals by

(a) the Government;

(b) any banking company or co-operative society engaged in carrying on the business of banking or a post office

(c) any business correspondent of a banking company or co-operative society engaged in carrying on the business of banking,

(d) any white label automated teller machine operator of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Setllement Systems Act, 2007:

Note: White Label ATMs are owned and operated by Non-Banking Financial Company (NBFC) . RBI has granted license or permission to non-banking entities to open such ATMs. Any non-banking entity with a minimum net worth of ₹ 100 crore can apply for white label ATM

4th Proviso: Provided also that the Central Government may specify in consultation with the Reserve Bank of India, by notification in the Official Gazette, the recipient in whose case the provision of this section shall not apply or apply at reduced rate, if such recipient satisfies the conditions specified in such notification.

SECTION 194N OF THE INCOME-TAX ACT, 1961 : CIRCULAR NO. 14/2020 [F. NO. 370142/27/2020-TPL], DATED 20-7-2020 Accordingly, in exercise of the said power. Central Government has issued three notifications which are as under:

| (a) | Notification 68 of 2019 dated 18-9-2019: Cash Replenishment Agencies (CRAs) and franchise agents of White Label Automated Teller Machine Operators (WLATMOs) for the purpose of replenishing cash in ATMs operated by these entities subject to conditions mentioned in the said notification | ||

| (b) | Notification 70 of 2019 dated 20-9-2019: Commission agent or trader operating under Agriculture Produce market Committee (APMC) and registered under any law relating to Agriculture Produce Market of the concerned State have been exempted subject to conditions specified in the said notification | ||

| (c) | Notification 80 of 2019 dated 15-10-2019: the authorized dealer and its franchise agent and sub-agent and Full Fledged Money Changer (FFMC) licensed by the Reserve Bank of India and its franchise agent for the purposes of- | ||

| (i) | Purchase of foreign currency from foreign tourists or non-residents visiting India or from resident Indians on their return to India, in cash as per the directions or guidelines issued by Reserve bank of India; or | ||

| (ii) | Disbursement of inward remittances to the recipient beneficiaries in India in cash under Money Transfer Service Scheme (MTSS) of the Reserve Bank of India; | ||

and subject to the conditions specified in the said notification.

Other applicable Sections

a) Sec 206AA:If the deductee has not furnished the PAN to the deductor then the tax deducted will be @ 20%

b) Sc 197: Certificate for no deduction/lower deduction cannot be issued by the Assessing Officer

c) Sec 198: Tax deducted u/s 194N is not deemed to be income received of the assessee.

d) Sec 199 Where the Income on which tax has been deducted is clubbed in the hands of another person the the credit of the TDS will be given to the person in whise hands the income is clubbed and not to the deductee. However u/s 194N the credit will be given to the deductee only i.e the person from whose account the TDS was deducted.

ISSUES: Amendment as on 01/07/2020

1) Is TDS deductible on amount withdrawn in excess of 1 crore or on the entire amount if the withdrawals exceed 1 crore

Substituted provisions by the Act No. 12 of 2020, w.e.f. 1-7-2020.

Payment of certain amounts in cash.

194N. Every person, being,

(i) a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) a co-operative society engaged in carrying on the business of banking; or

(iii) a post office,

who is responsible for paying any sum, being the amount or the aggregate of amounts, as the case may be, in cash exceeding one crore rupees during the previous year, to any person (herein referred to as the recipient) from one or more accounts maintained by the recipient with it shall, at the time of payment of such sum, deduct an amount equal to two per cent of such sum, of sum exceeding one crore rupees, as income-tax:

Prior to its substitution, section 194N read as under :

“194N. Payment of certain amounts in cash.—Every person, being,—

(i) a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) a co-operative society engaged in carrying on the business of banking; or

(iii) a post office,

who is responsible for paying any sum, or, as the case may be, aggregate of sums, in cash, in excess of one crore rupees during the previous year, to any person (herein referred to as the recipient) from one or more accounts maintained by the recipient with it shall, at the time of payment of such sum, deduct an amount equal to two per cent of sum exceeding one crore rupees, as income-tax:

Opinion: from the reading of the aforesaid provisions we see that the words “ of the sum exceeding one crore rupees” is missing in the new substituted law, which may lead to the interpretation that the TDs will be deductible on the entire amount if it exceeds 1 crore. For example if amount withdrawn is 1.20 crore then it could imply that TDS is deductible on 1.20 crore. However after discussion with many leading Bankers I came to the understanding that practically even now the TDS is being deducted only on 20 lacs. It remains to be seen of the Income Tax department takes a different view.

2) Is Sec 194N applicable to cash withdrawal only through self cheque or under bearer cheque as well?

A simple reading of the Act may lead to a conclusion that Sec 194N The payment made by any payer from the accounts maintained by the taxpayer will only attract TDS under Section 194N. For instance, if a bank makes a cash payment of more than Rs 1 crore in an FY to its account holder (i.e any taxpayer) from the account maintained by him, then the bank will have to deduct TDS. But, if the taxpayer gives a bearer cheque (uncrossed) in the name of a person, say Mr A, and he withdraws cash from the individual’s account, then will the TDS will not be deducted. From practical understanding and reading the intention of legislature it seems that any withdrawal from the account by the holder or anyone else will be liable for TDS u/s 194N