These are financial advice that even the common man understands. I request everyone to follow. 4 things that are very, very necessary for any person, whether they know i or not in share market or insurance or mutual find. These are really basic advices.

These four things will give so much Financial protection to your family. so I am talking about cultivating 4 financial habits to safeguard your family from any uncertainty and also for your secured retirement planning.

1. Health Insurance (Mediclaim) + Personal Accident Policy

Mediclaim is very helpful in case of any health related emergency that comes to you Nowadays the cost of each operation has gone up from Rs 5 lakh to Rs 20 lakh. It is not possible to withdraw such a large amount. or you have to reduce your savings. HEalth Insurance is really important. Health Insurance provides coverage on the medical claims within the tenure. Make sure Every Family member is covered. Even children. You can also add critical illness and accident add on for more coverage & security

2. TERM LIFE INSURANCE ( including disability rider)

Here I am not talking about normal life insurance policy. TERM LIFE INSURANCE is not like any other policy. It can give a a large amount to Family members at the time of death of the person holding the policy… for example.a young man can get a cover of 1 CRORE against 15000 annual PREMIUM. Meaning if one dies prematurely before 75 years, 1 crore members of the household get.. Term Insurance provides coverage for the premature death of the policyholder within the fixed term wheras Life Insurance provides coverage on the maturity of the policy. Term insurance means that after the untimely death of the earner, his family gets financial support. No insurance agent is required for this. By contacting any private bank branch directly, you can.. This basic product There is no rocket science in it. You can add as add on ” Disability” rider also. Term insurance is for a set period of time, for example, 30 years, 40 years, or as you may choose. You pay a certain premium for a fixed sum insured for the entire tenure of the plan. a term plan has one of the lowest premiums in the market. All your premium payments are eligible for a tax deduction while the sum insured is non-taxable.

3. PPF – public provident fund

Open PPF account of every person at your home.It can be opened in Post and It can be opened in any bank also . 7.1% interest which is TAX FREE. In addition investment will also be deducted from income. In 80c. 1.5 lakh per annum for 15 years. It is 100% SECURE too. Also 5 years can be extended too. You can earn 37 lakh with only 22.5 lakhs in 15 years and 57 lakhs with 30 lakhs investment in 20 years (Almost double). This is still the best investment option. TAX FREE even at maturity.

| Age | Opening Balance | Yearly Contribution | Interest rate 7.1% | Interest Rate @7.1% | Closing Balance |

| 26 | 0 | 1,50,000 | 7.10 | 10,650 | 1,60,650 |

| 27 | 1,60,650 | 1,50,000 | 7.00 | 21,746 | 3,32,396 |

| 28 | 3,32,396 | 1,50,000 | 6.90 | 33,285 | 5,15,681 |

| 29 | 5,15,681 | 1,50,000 | 6.80 | 45,266 | 7,10,947 |

| 30 | 7,10,947 | 1,50,000 | 6.70 | 57,683 | 9,18,631 |

| 31 | 9,18,631 | 1,50,000 | 6.60 | 70,530 | 11,39,160 |

| 32 | 11,39,160 | 1,50,000 | 6.50 | 83,795 | 13,72,956 |

| 33 | 13,72,956 | 1,50,000 | 6.40 | 97,469 | 16,20,425 |

| 34 | 16,20,425 | 1,50,000 | 6.30 | 1,11,537 | 18,81,961 |

| 35 | 18,81,961 | 1,50,000 | 6.20 | 1,25,982 | 21,57,943 |

| 36 | 21,57,943 | 1,50,000 | 6.10 | 1,40,785 | 24,48,728 |

| 37 | 24,48,728 | 1,50,000 | 6.00 | 1,55,924 | 27,54,651 |

| 38 | 27,54,651 | 1,50,000 | 5.90 | 1,71,374 | 30,76,026 |

| 39 | 30,76,026 | 1,50,000 | 5.80 | 1,87,109 | 34,13,135 |

| 40 | 34,13,135 | 1,50,000 | 5.70 | 2,03,099 | 37,66,234 |

| 41 | 37,66,234 | 1,50,000 | 5.60 | 2,19,309 | 41,35,543 |

| 42 | 41,35,543 | 1,50,000 | 5.50 | 2,35,705 | 45,21,248 |

| 43 | 45,21,248 | 1,50,000 | 5.40 | 2,52,247 | 49,23,495 |

| 44 | 49,23,495 | 1,50,000 | 5.30 | 2,68,895 | 53,42,390 |

| 45 | 53,42,390 | 1,50,000 | 5.20 | 2,85,604 | 57,77,995 |

| amount invested | Interest earned | Maturity Amount | |||

| 30,00,000 | 27,77,995 | 57,77,995 |

Assuming Interest rate will decrease 10 points yearly

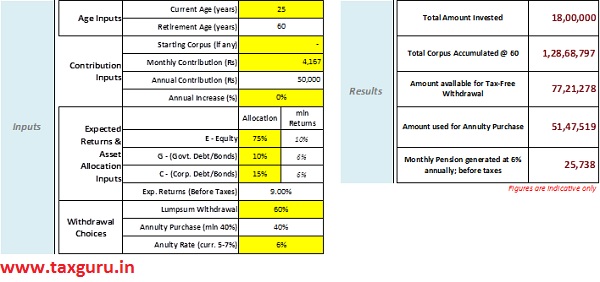

4. NPS – NATIONAL PENSION SCHEME

NPS is a government-sponsored pension scheme. The scheme allows subscribers to contribute regularly in a pension account during their working life. On retirement, subscribers can withdraw a part of the corpus in a lumpsum (60%) and use the remaining corpus (40%) to buy an annuity to secure a regular pension income after retirement. even , 0% amount will give higher maturity than PPF amount you would have got on same investment. Most banks, both private and public sector, are enrolled as NPS scheme provider. individuals can claim an additional deduction of up to Rs 50,000 under Section 80CCD (1B), which is in addition to Rs 1.5 lakh permitted under Section 80C. If the subscriber dies before 60 years, the entire accumulated wealth would be paid to the nominee/legal heir of the subscriber. maximum age is 65 to enter the scheme. Scheme invests in 75% equity and 25% in Govt bonds. At the maturity of 60th age , 60% amount will be returned and You will receive pension till death. from Annuity of 40% amount

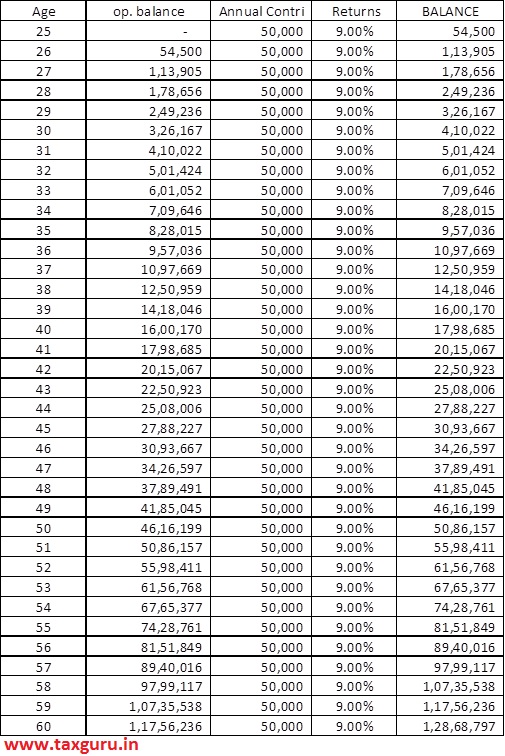

NPS YEARLY RS. 50000 contribution . JUST CHECK BELOW CHART to understand how amazing returns are. Just by Investing Rs. 50000 from age 25 to 60. Total investment would be Rs. 18 lacs and Total accumulated funds at end of 60th year is Rs. 1.28 crore

NPS CHART ( ASSUMING AGE OF ENTRY FROM 25)

A minimal Guide to Financial Planning for each Age Strata

| For Age from 25 to 45

A. Invest each year Invest Each year 1.5 lac in PPF. For next 20 years from age 25 (15 years + 5 year extension). Maturity amount save it for your future + NPS every year for Rs. 50000

B. Insure each year Get a TERM insurance of atleast 50 lac cover AND Get a Family floater health insurance of Atleast 10 lac cover. |

For Age Having 45 to 60

A. Invest each year Invest each year 1.5 lac in PPF. For next 20 years from age 45 (for 15 years) maturity amount save it for your future + NPS every year for Rs. 50000

B. Insure each year Continue with term insurance of atleast 50 lac cover. and Continue family floater health insurance of atleast 20 lac cover. |

For Age ABOVE 60

A. Invest each year POST MIS OF SENIOR CITIZEN will be good option as It will give you 7.4%. If you have balance fund at your disposal.

B. Insure each year Continue with term insurance of atleast 50 lac cover. and Continue family floater health insurance of atleast 20 lac cover. |

Nice and informative article.