The Union Budget 2019-20 for the FY 2019-2020 was presented on 05th July 2019. The Budget proposed new Sections for TDS such as 194M which is applicable from 01st September, 2019.

Article explains Reason for introduction of Section 194M, Meaning of Section 194M, Person liable to deduct TDS under Section 194M, Time limit for Tax Deduction at Source under Section 194M, Rate of TDS for Tax Deduction at Source under Section 194M, Time Limit for Depositing TDS under Section 194M, Specified payments covered under section 194M and Frequently Asked Questions (FAQs) on TDS under Section 194M.

Page Contents

- Reason for introduction of Section 194M

- Meaning of Section 194M

- Person liable to deduct TDS under Section 194M

- Time limit for Tax Deduction at Source under Section 194M

- Rate of TDS for Tax Deduction at Source under Section 194M-

- Time Limit for Depositing TDS under Section 194M

- Specified payments covered under section 194M

- Frequently Asked Questions (FAQs) on TDS under Section 194M

- Meaning of Work under Section 194M (same as 194C)

- Meaning of Professional services under Section 194M (same as 194J)

Reason for introduction of Section 194M

This section was introduced for the purpose to cover some specified high value transactions in personal nature under TDS which was previously excluded from TDS provisions.

As per existing provisions of 194J and 194C, individual & HUF are not required to deduct TDS if: –

- Payment made exclusively for personal purposes

- Payment made for other than personal purpose but individual & HUF are not required to get their accounts audited.

- A major amount of payment made for contractual works and professional fees was escaping the levy of TDS because of this exemption, creating a scope for tax evasion.

Meaning of Section 194M

√ An individual and/or Hindu undivided family (HUF) has to deduct tax at source under Section 194M. Such individuals and HUF must not be required to get their books of accounts audited.

√ It applies when the total amount paid to a resident individual, for carrying out any contractual work or providing any professional service, in a financial year exceeds Rs 50,00,000.

√ If they are required to get Books of Accounts audited, TDS deduction is applicable as per Section 194C and 194J. The individual and/or HUF who have to deduct TDS under Section 194C (TDS on payment to a contractor) and 194J (TDS on payment on professional fees) do not have to deduct tax at source under Section 194M.

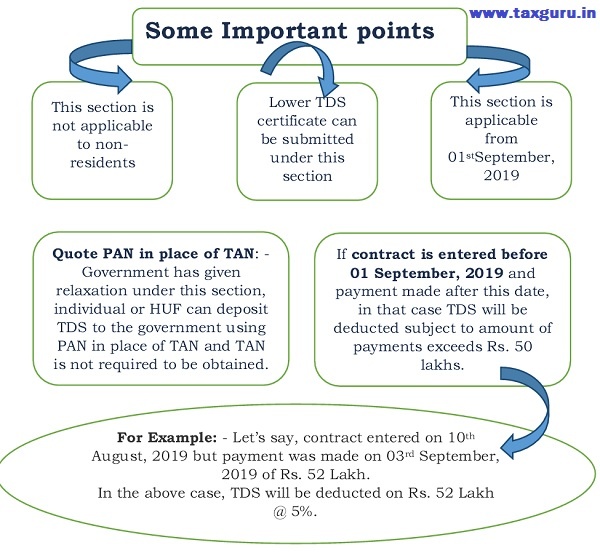

√ The individual or HUFs who has to deduct tax can pay the tax to the government by quoting his or her PAN only. Not required to get a tax deduction account number (TAN) for TDS deduction.

√ Payments to non-residents are not covered under this section.

Person liable to deduct TDS under Section 194M

- If any payment is made by any individual/HUF to a resident contractor or a resident professional for carrying out any work in nature of personal purpose (including the supply of labour) under any contract or by way of fees for professional services rendered during the financial year, exceeding Rs 50,00,000 in a year will have to deduct TDS at 5% under Section 194M.

- If any payment is made to a resident by way of commission or brokerage by an individual or HUF who are not required to get their books of accounts audited.

- Section 194M will be effective from 1 September 2019 onwards.

- TDS amount will be deducted on any payment made after this date even if the contract existed before, provided the payment exceeds Rs 50,00,000.

- Please note insurance commission does not gets covered under section 194M

Time limit for Tax Deduction at Source under Section 194M

TDS under section 194M will be deducted on the earlier of the following dates:

1. At the time of credit of the amount.

2. At the time of payment by cash or by the issue of a cheque or draft.

Rate of TDS for Tax Deduction at Source under Section 194M-

TDS at 5% will be deducted under 194M if the total amount paid to a resident exceeds Rs 50,00,000 in a particular financial year but In case the PAN of the deductee is not available, then TDS will be deducted at 20%.

Let’s take an example, Mr. Ram made a payment of Rs. 50 Lakh for professional services on 18thAugust, 2019, In this case TDS will not be deducted as amount of payment does not exceed Rs. 50 Lakh.

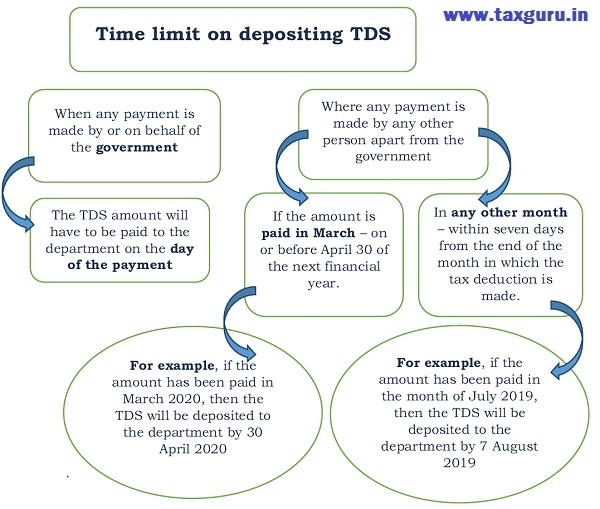

Time Limit for Depositing TDS under Section 194M

Specified payments covered under section 194M

- Payment (not covered u/s 194C) made to a resident contractor

- Payment (not covered u/s 194J) made to a resident professional

- Payment (not covered u/s 194H) made to a resident individual by way of commission.

On other words If Individual and HUF are required to get Books of Accounts audited, TDS deduction is applicable as per Section 194C /194J /194H. The individual and/or HUF who have to deduct TDS under Section 194C (TDS on payment to a contractor), Section 194H TDS on Brokerage and Commission and Section 194J (TDS on payment on professional fees) do not have to deduct tax at source under Section 194M.

Some Important points related to Section 194M

Frequently Asked Questions (FAQs) on TDS under Section 194M

Q1. A made a payment of Rs.55 Lakh for professional services on 05th September, 2019. Whether TDS will be deducted in this case and if yes, on what amount?

A1. In the above case, TDS will be deducted as amount of payment exceeds Rs. 50 Lakh and TDS will be deducted on Rs. 55 lakh @ 5% i.e. 2.75 Lakhs.

Q2. Ram entered into a contract of catering on 25th July, 2019 and payment made of Rs. 55 Lakh on 30 August, 2019. Whether TDS will be deducted in this case?

A2. In this case, contract was entered before 01st Sep, 2019 but payment was made before 01st September, 2019 hence TDS will not be deducted

Q3. Shyam made a payment of professional fees of Rs. 55Lakh, and Shyam is liable to get his accounts audited under section 44 AB. Whether TDS is required to be deducted under this section?

A3. As per this section, individuals who are required to get their accounts audited are not covered hence TDS will not be deducted under this section.

Q4. An individual receives a bill of catering of Rs. 42 Lakh and a bill of consultancy of Rs. 10 Lakh from one single person. Whether TDS will be deducted?

A4. The threshold limit of Rs. 50 Lakh is aggregate limit for both professional and contractual work hence TDS will be deducted. So. TDS will be deducted on 52 Lakh @ 5% i.e. 2.60 Lakh

Q5. How deductee will get the credit/refund of the tax deducted?

A5. When tax is deposited to government through challan, the tax will appear in 26AS of the deductee and deductee can claim credit of TDS.

Q6. How to pay TDS amount to government under this section?

A6. Every person responsible for deduction of tax under section 194M shall furnish the certificate of deduction of tax at source in Form No. 16D to the payee within fifteen days from the due date for furnishing the challan-cum-statement in Form No. 26QD under rule 31A after generating and downloading the same from the web portal specified by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or the person authorized by him

Meaning of Work under Section 194M (same as 194C)

√ Advertising

√ Broadcasting and telecasting including production of programs for such broadcasting or telecasting.

√ Carriage of goods and passengers by any mode of transportation, other than railways.

√ Catering.

√ Manufacturing or supplying a product according to the requirement or specification of a customer by using material purchased from such customer. But does not include manufacturing or supplying a product according to the requirements or specifications of a customer by using material purchased from a person, other than such a customer.

√ Contract: This expression includes sub-contract.

Meaning of Professional services under Section 194M (same as 194J)

√ Professional fees

√ Fees for technical services

√ Remuneration paid to directors excluding salary means which is not liable to TDS u/s 192 (For example, sitting fees to attend board meetings,)

√ Royalty

√ Payments in the nature of non-compete fees (i.e., fees paid to not carry on any business or profession for a specified time and within certain geographical boundaries) or fees paid to not share any technical knowledge or know-how.

Author Bio

I had paid rs 25 lakhs earlier and now will be paying rs 50 lakhs and in future also i will be paying some small small amounts to resident contractor.

Do i need to fill form 26QD every time for each remittance?

thank you so much

Sir,

If a joint family is in a contract with a Contractor to construct their house, where all family members are Jointly Owner in that house and cont. value is 75 Lakhs, and all four family member paid to contractor in ratio as per their ownership percentage and no any family member paid more than 50 Lakhs ,

Than TDS u/s 194M will be applicable or not

Please clarify.

Sir (Mr Piyush Agarwal, CA)

Could you please clarify whether this section applies to such cases of ‘collaborative contract’ arrangements, where the building material for construction of the house, as in this case, has been purchased by the Contractor from out side and not from the Customer/Owner of the residential plot. Definition of work in this Section 194M, ‘does not include manufacturing or supplying a product according to the requirements or specifications of a customer by using material purchased from a person, other than such a customer’.

Is the 50 lakh limit is for individual services, like 50l for contract, 50l for professor. services and 50l for commission Or 50lakhs is for aggregate.

Sir, section specifies the payment made by Individual and HUF to any resident but not specified only to individual which you are mentioning in the article

Section 194M is applicable to all payees and not just individual. Please clarify. Seems some confusion is there