In this age of globalization many organizations including individuals have got their wings spread all over the world.

In any country the tax is levied based on 1) Source Rule and 2) the Residence Rule. The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides. If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international scale would become prohibitive and would deter the process of globalisation. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) becomes very significant.

In India the residential status is the key point for determination of income tax. In case of Residents their global income (i.e Indian Income as well as Foreign Income) is taxable in India whereas in case of non-residents only Indian Income is taxable. So we can say that in India residence rule is applied for residents whereas source rule is applied for Non-residents. The residential status of a person is determined based on the provisions of Section 6 of Income Tax Act 1961.

Image courtesy of David Castillo Dominici at FreeDigitalPhotos.net

Many a times, it is seen that in case of residents, the income tax has been paid in other countries on their income abroad (i.e Foreign Income) and on the same income they are also required to pay tax in India. In such cases, there are provisions of providing relief from double tax. Basically there are two sections (i.e section 90 and section 91) in Income Tax Act 1961, which provides relief from Double tax.

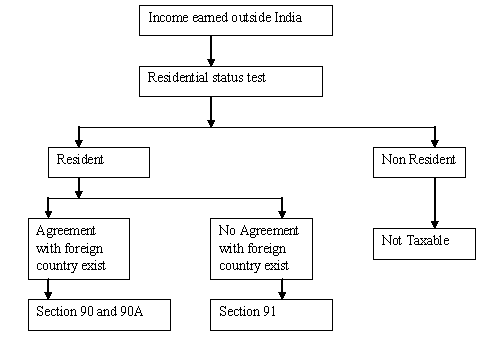

The application of section 90 and 91 can be explained with the help of the following diagram.

As can be seen from the above diagram that section 90 is applicable in cases where India has entered into a Bilateral agreement with other country and section 91 is applicable in case where there is no such bilateral agreement (i.e there is unilateral agreement)

As of now India has entered into DTAA with 93 countries and Limited Agreements with 8 Countries.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee. However the provisions of Chapter X-A(GENERAL ANTI-AVOIDANCE RULE) of the Act inserted wef 01.04.2016 shall apply to the assessee even if such provisions are not beneficial to him.

Where there is an DTAA agreement (Section 90)

U/s 90 there are two methods of granting relief under Double Taxation Avoidance Agreement.

1) Exemption method – A particular income is taxed in one of the both countries and exempted in the other country. (For example- For the Income from Dividend, Interest, royalty and fees for technical services source rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for a citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and if for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not be at all taxable in India).

2) Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of source. For example- Mr A (an Indian resident) has received salary from a US company for job in US. Since Mr A is a resident so his global Income will be taxable. In this case source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr A the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

In case where Bilateral agreement has been entered u/s 90 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more favourable to assessee. [CIT Vs ITC Ltd (2002)]

For example: As per DTAA between Indian and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence one can follow DTAA and pay tax @ 10% only.

Where there is an NO DTAA agreement (Section 91)

(1) If any person who is resident in India in any previous year proves that, in respect of his income which accrued or arose during that previous year outside India (and which is not deemed to accrue or arise in India), he has paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, income-tax, by deduction or otherwise, under the law in force in that country, he shall be entitled to the deduction from the Indian income-tax payable by him of a sum calculated on such doubly taxed income at the Indian rate of tax or the rate of tax of the said country, whichever is the lower, or at the Indian rate of tax if both the rates are equal.

(2) If any person who is resident in India in any previous year proves that in respect of his income which accrued or arose to him during that previous year in Pakistan he has paid in that country, by deduction or otherwise, tax payable to the Government under any law for the time being in force in that country relating to taxation of agricultural income, he shall be entitled to a deduction from the Indian income-tax payable by him—

(a) of the amount of the tax paid in Pakistan under any law aforesaid on such income which is liable to tax under this Act also; or

(b) of a sum calculated on that income at the Indian rate of tax;

whichever is less.

(3) If any non-resident person is assessed on his share in the income of a registered firm assessed as resident in India in any previous year and such share includes any income accruing or arising outside India during that previous year (and which is not deemed to accrue or arise in India) in a country with which there is no agreement under section 90 for the relief or avoidance of double taxation and he proves that he has paid income-tax by deduction or otherwise under the law in force in that country in respect of the income so included he shall be entitled to a deduction from the Indian income-tax payable by him of a sum calculated on such doubly taxed income so included at the Indian rate of tax or the rate of tax of the said country, whichever is the lower, or at the Indian rate of tax if both the rates are equal.

Misuse of DTAA, Treaty shopping and amendment made by Finance Act 2012

Treaty Shopping occurs when the resident of a third country takes advantage of the provisions of DTAA between two countries.

As per the DTAA with Mauritius, Capital Gain accruing in India to a resident of Mauritius is not taxable in India subject to certain exception. Again there is no capital gain tax applicable in Mauritius. Hence it leads to tax exemption in both the countries.

FIIs (Foreign Institutional Investors) in order to take advantage of such treaty get themselves incorporated in Mauritius and becomes the resident of Mauritius. As held by the Supreme Court in the case of UOI Vs Azadi Bachao Andolan (2003) and via CBDT Circular No 789 dated 13.04.2000 it has been clarified that wherever a certificate of residence is issued by Mauritius Authority, such certificate will constitute sufficient evidence for accepting the status of residence as well as beneficial ownership for applying DTAA accordingly. Hence a number of cases of treaty shopping has been observed which is very legal.

In order to curb this treaty shopping section 90 has been amended by Finance Act 2012, by which now submission of Tax Residency Certificate (TRC) will be a necessary but not sufficient condition for availing the benefit of the agreements referred to in this section. The format of TRC will be notified by board. It appears that after notification of the format of TRC it will be difficult for an intermediate country like Mauritius to issue TRC to certify that a global company has significant operation in Mauritius.

The details of DTAA can be extracted from the site www.incometaxindia.gov.in

Contributed by: CA Srikant Agarwal

srikantagarwal@bharatpetroleum.in, srikant.agarwal@gmail.com

Click here to read Other Articles of CA Srikant Agarwal

(Republished With Amendments)

Author Bio