1. The Income Tax Department has enabled the online income tax return form ITR-4, for FY 2023-24 (AY 2024-25) on the e-filing portal. The taxpayers, eligible to file ITR 4 can now file their Return for FY 2023-24.

3. In this article, an attempt has been made to explain the intricacies of filing ITR-4 with the help of Illustration.

3. Illustration Mr. Anupam is a salaried employee and also engaged in derivative trading. His CA suggested to file ITR 4 as it is a simple form compared to ITR 3 and, Books of Accounts are not required to be maintained. Let us help him filing ITR 4.

The details of Mr. Anupam’s total income for the year 2023-24 are as indicated below:

| Sl. | Particulars | Amt (Rs.) | Amt (Rs.) |

| (a) | Income from Salary | 20,00,000 | |

| (b) | Absolute turnover from F&O | 2,50,00,000 | |

| (b1) | Through account payee cheque | 2,40,00,000 | |

| (b2) | Through Cash/ any other mode | 10,00,000 | |

| (c) | Loss from F&O Business | (4,50,000) | |

| (d) | Income from Interest | 1,20,000 | |

| (e) | Income From dividend | 25,000 |

4. Eligibility: First of all, we need to check whether Mr. Anupam is eligible to file ITR 4 or not. ITR 4 can be filed by (a) Resident Individual / HUF/Firm (other than LLP) (b) having Income from Business & Profession computed on a presumptive basis u/s 44AD/44ADA/44AE. (c) having Income from Salary/Pension, one House Property, Agricultural Income (up to ₹ 5000/-) (d) Income from other Sources excluding winning from Lottery and Income from Racehorses):

4.1 An individual who is either a director in a company or has invested in unlisted equity shares or if income-tax is deferred on ESOP or has agricultural income more than Rs.5000 is not eligible for filing ITR 4.

4.2 ITR 4 can be filed by an individual resident whose income from Business & Profession can be computed on a presumptive basis.

5. Presumptive Taxation Presumptive taxation scheme is designed to give relief to small businesses and professionals from maintaining books of accounts. Section 44AD, 44ADA & 44AE governs the rule for Presumptive Scheme.

5.1 Any business which has a turnover of less than Rs 2 crore can opt to be taxed presumptively. They must declare profits of 8% for non-digital transactions and 6% for digital transactions.

5.3. The Finance Act 2023 was amended to raise the threshold limit of gross turnover from Rs. 2 crores to Rs. 3 crores, given that receipts in cash do not exceed 5% of the total gross turnover for the previous year

6. Mr. Anupam is engaged in F&O business and his turnover from such business is Rs. 2.50 crores. The cash receipts of Rs. 10 Lakhs do not exceed 5% of total gross turnover. He is eligible to file ITR 4.

7. Step-by-Step Procedure to File ITR 4

(a) Login to https://eportal.incometax.gov.in/

(b) Select Assessment Year: 2024-25 > mode of filing: online> status: individual> ITR to be filed: ITR 4 > Proceed with ITR 4.

(c) Let’s Get Started > reason to file ITR: taxable income is more than the basic exemption limit> validate pre-filled return.

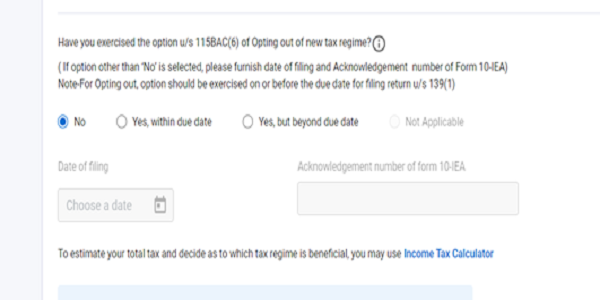

(d) Option for Tax Regime The new tax regime is the default tax regime from April 1, 2023. If a taxpayer having income from Business or Profession wishes to opt-out from new regime & file tax under old regime, he needs to file Form 10IEA on or before due date for filing return. The acknowledgement number and date of filing Form 10IEA is to be provided at the time of filing ITR 4

Mr. Anupam does not wish to opt out of the default new regime and clicked on No

(e) Enter the details of Salary.

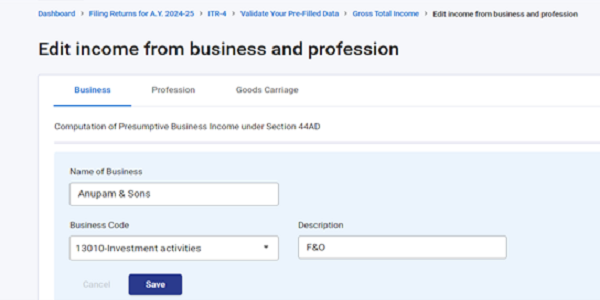

(f) Nature of Business Select Code from the drop-down list. A trade name can be taxpayer’s name. Enter the description as F&O / Intraday business in the given box. This will give a fair idea about the nature of the business of the assessee.

There is no specific business code mentioned for F&O. The code 13010 – Investment activities, can be selected for F&O transactions.

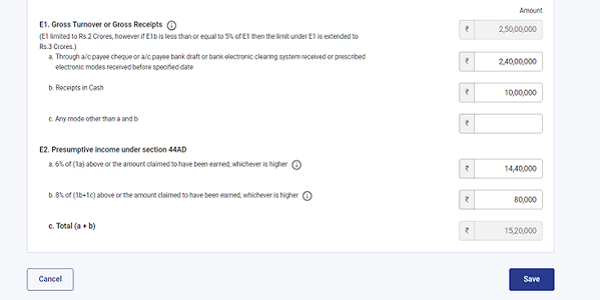

(g) Enter Gross Turnover & Presumptive Income

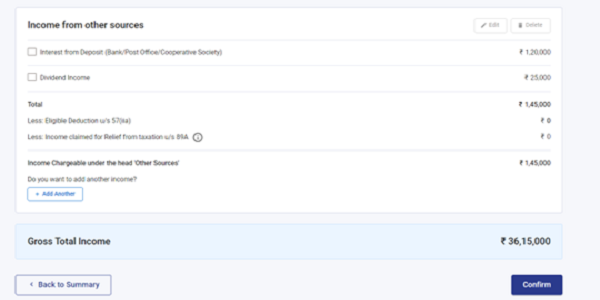

(h) Enter the details of Income from Other Sources.

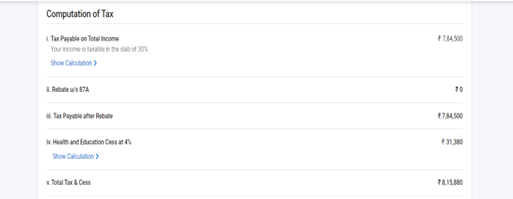

(i) Computation of Tax

(j) Pay the tax, validate, and submit the return.

8. Constraints As can be seen, if Mr. Anupam opts for a presumptive taxation scheme and files ITR 4, his tax liability will be Rs. 8,15,880/-. Despite having loss from F&O business, he has to pay tax on presumptive income of Rs. 15,20,000/-. Not only this, once he opts for presumptive taxation in FY 2023-24, he must follow it for the next 5 years. Otherwise, he is required to get his accounts audited and maintain the books of Accounts Audited.

8.1 Opting out of it for any 1 year during these 5 years will make him ineligible to again opt for it the 5 years immediately following the year when he opted out of it.

9. Computation of Tax Liability in regular scheme of taxation:

| Sl. | Particulars | Amt (Rs.) | Amt (Rs.) |

| (a) | Income from Salary | 19,50,000 | |

| (b) | Income from other sources | 1,45,000 | |

| (c ) | F&O Losses | (1,45,000) | |

| (d) | Taxable Income | 19,50,000 | |

| (e) | Tax Liability including cess | 2,96,400 |

9.1 Notes

(a) Losses from F&O can be set off from any other income except Salary Income.

(b) Mr. Anupam can carry forward losses for the next 8 years

(c) Assuming that Mr. Anupam had never opted for Presumptive taxation before, he is not required to get audit done even if he opts for normal taxation

10. Mr. Anupam is recommended to maintain books and file ITR 3 under the regular scheme of taxation.

*****

The author can be approached at caanitabhadra@gmail.com

Disclaimer: The article is for education purposes only.

Author Bio

Interest income will be added – taxable under the head “ Income from other source”

iam filling presumptive tax . can interest income will be added or reduce as case may be