ITBA Processing Instruction No. 17

DIRECTORATE OF INCOME TAX (SYSTEMS)

ARA Center, G. Floor, E-2, Jhandewalan Extension, New Delhi-110055

F. No. System/ITBA/Instruction/ITR Processing/2023-24/

Dated: 25.03.2024

To,

All Pr. CCsIT CCOT

All Pr. DGsIT DGsIT

All Pr. CsIT / CsIT / CsIT (Admin & TPS) All Pr. DsIT / DsIT

Madam/Sir,

Sub.: Functionality for processing of electronically filed valid returns (upto AY 2021-22) having refund claims which were not processed within the time allowed u/s 143(1) due to some technical or other reasons.

Ref. : 1. CBDT’s Order u/s 119 of Income Tax Act, 1961 dated 01.03.2024

2. CBDT’s Order u/s 119 of Income Tax Act, 1961 dated 31.01.2024

3. CBDT’s Order u/s 119 of income Tax Act, .1961 dated 01.12.2023

4. CBDT’s Order u/s 119 of income Tax Act, 1961 dated 16.10.2023

(issued in partial modification of earlier order u/s 119 dated 05.01.2021 and 30.09 2021)

Kindly refer to the above.

2. References from the field formations and taxpayers have been received in Board informing that due to certain technical or other reasons, not attributable to the assessee, several returns for various years, which were otherwise filed validly under section 139, 142 and 119 of the Income-tax Act, 1961, could not be processed within the time prescribed under section 143(1) of the Act due to which refund due to the assessee could not be Issued.

3. The CBDT in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961 vide its Order dated 05.07.2021 and 30.09.2021 issued through File No. 225/98/2020/ITA-II had relaxed the time frame prescribed in Second proviso to sub section (1) of section 143 till 30,11.2021. Further, the CBDT vide its Order under section 119 of the Act dated 16.10.2023 issued through File No. 225/132/2023/114-II, relaxed the time frame prescribed in second proviso to sub section (1) of section 143 (for the eligible cases upto AY 2017-18) till 31.01.2024. For the above purpose, the ITBA Processing Instruction No. 15 has already been issued on 17.11.2023. Furthermore, the CBDT vide its Order under section 119 of the Act dated 12.2023 issued through File No 225/132/2023/ITA-II, relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for the eligible cases upto AYs 2018-19, 2019-2020 & 2020-21 also) till 31.01.2024. For the above purpose, the MIA Processing Instruction No. 16 has already been issued on 11.12.2023. The CBDT vide its order dated 31.01.2024 issued through File No. 225/132/2023/ITA-II has extended the aforesaid time-limit from 31.01.2024 to 30.04.2074.

4. To mitigate the genuine hardship being faced by the taxpayers on this issue, the CBDT, in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961, has further relaxed the time frame prescribed in second proviso to sub section (1) of section 143 (for the eligible cases for AY 2021-22 also) till 30.04,2024. In this regard, CBDT has issued an order u/s 119 dated 01.03.7024 through File No.225/132/2023/ITA-II. The CBDT’s earlier order dated 16.10.2023 (for AYs upto 2013-18), order dated 01.12.2023 (for AYs 2018-19, 2019-2020 & 2020-21) and order dated 01.03.2024 (for AY 2021-22) does not cover paper return and is applicable for only electronically filed valid II Rs.

5. As per the above referred order(s) of CBDT (dated 16.10.2023, 01.12.2023 and 01.03.2024), all such unprocessed time-barred electronically filed valid ITRs upto AY 2021-22 (subject to other exceptions mentioned in CBDT’s Order u/s 119 dated 05.07.2021, 16.10.2023, 01.12.2023 & 01.03.2024) can now be processed with prior administrative approval of concerned Pr. CCIT/CCIT. Once administrative approval is accorded by Pr. LCII/CCII, the concerned Pr.CIT/CIT shall make a reference to DGIT(Systems) to provide necessary enablement to Assessing Officer for processing of return.

6. For the ease of making reference to XII (Systems) by Pr, CIT/CIT, a screen has been made available in the RBA’s ITR Processing Module named “Enablement u/s 119” It is requested that all Pr. CsIT/CsIT should use this screen for making a reference to DOT (Systems) for making necessary enablement r.t. CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07.2071), order dated 01.12.2023 & order dated 01.03.2024. Further, all concerned are requested to process such references/proposals at the earliest, for the enablement of processing of such unprocessed time barred returns filed electronically It is to clarify that in each such case, the processing rights will be enabled by the ITBA team and subsequently, the processing action has to be performed by the respective Assessing Officer. The proposals for the enablement of time barred processing may kindly be submitted by PCsIT/CsIT before 10.04.2024 so that these references can be enabled/processed well within the time period ending on 30.04.2024.

7. Following scheme and validation are prescribed in the CBDT’s above order dated 05.07.2021,16.10.2023 01.12.2023 & 01.03.2024:

Pre-Conditions :

(i) The ITR should be –

-

- for AY upto AY 2021-22.

- a valid ITR.

- electronically filed

- filed within permitted time limit u/s 139, 142(1) or 119 of the Act.

(ii) Assessee has claimed refund in return of income.

(iii) On computation, the resultant outcome is refund.

(iv) The returns of income should not have remained unprocessed due to any reason attributable to the concerned assessee.

(v) The returns of income should not be under Scrutiny assessment.

8. Processes to be followed by the PCIT / CIT :

8.1 Prior administrative approval of concerned Pr. CCIT/CCIT must be obtained for processing of such time-barred eligible electronically filed valid returns of income as mentioned in CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07.2021), order dated 01.12.2023 and order dated 01.03.2024.

8.2 Once administrative approval is accorded by the concerned Pr. CCIT/CCII, the concerned Pr. CIT/CIT would enter the details in the screen available in ITR Processing Module-> “Enablement u/s 119″ to refer the case to the DGIT(Systems) for the purpose of providing necessary enablement to the assessing officer for processing such return.

Steps of entering/submitting details by Pr.CIT/CIT for making reference to DGIT (Systems):

a) In ITBA, Open ITR Processing > Enablement u/s 119 > Condonation – Enter New details.

b) Enter PAN and AY of the case. Thereafter, basic details like Name of Assessee, AO Detail, Date of Filing of ITR and Acknowledgement No. of electronically filed valid ITR will be automatically populated if such unprocessed return is available in the system.

c) Thereafter, enter Pr. CCIT/CCIT administrative approval Order No. and Order Date. Once this is done, the details have to be saved by clicking ‘Save‘ Button.

d) After saving the details, lick on Attachment button and ‘Attachment’ screen will be opened. Choose category “Approval Order of CCIT/CCIT” to attach the order of approval (uploading, of Administrative Approval of Pr.CCIT/CCIT is compulsory and mandatory). Further, if needed, any other documents may also be attached, by adding row and choosing category as ‘Others‘ and Clicking on ‘Upload’ Button.

e) After Attachment, submit the details by mandatorily clicking on ‘Submit’ Button.

f) Please note that merely saving the details by pressing “Save” button is not sufficient, the reference/details would be electronically moved to the System’s database only once the “Submit” button is pressed.

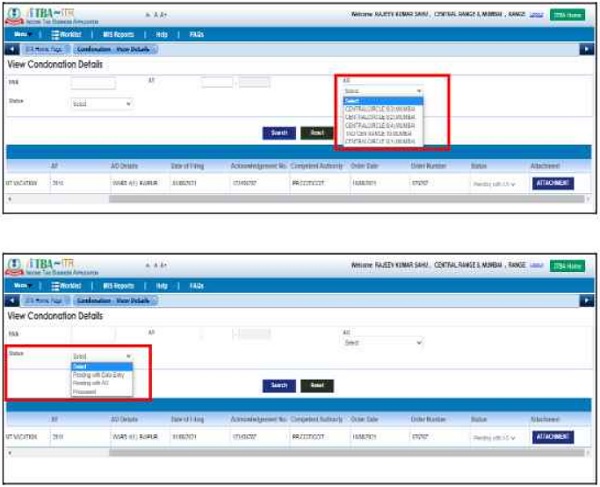

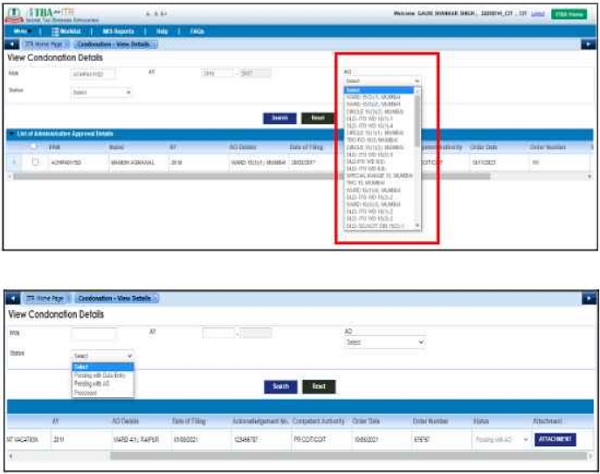

8.3 Submitted details will be visible for record/monitoring purpose In the read only mode at ITBA portal via navigation path “ITBA > ITR Processing > Enablement u/s 119 > Condonation – View Details” screen (This screen will be accessible to Pr.CIT/C1 f, Range-Head and AO). User may Search the record by entering PAN and AY. Status will get updated as per the actions taken by AO

9. Processes to be followed by the AOs :

9.1 For the cases up to A.Y. 2015-16: Cases for these years will be processed through MOU, The AO can process such time-barred eligible returns manually and upload the same through Manual Order Upload (MOU) functionality as explained in II BA Assessment/Processing Instructions issued so far to submit the return to CPC.

Such ITRs are required to be processed manually by the AO /after getting approval of the Pr.CCIT/CC11 and making reference by the POT/CIT in the screen “Enablement u/s 119″1 and upload in ITBA portal via Manual Order Upload (MOU) functionality through the navigation-path “Go to iron Assessment home page > Menu > Manual Order Upload”.

9.2 Cases of A. Y. 2016-17 to 2021-22: For the A.Y. 2016-17 to 2071-22, all the e-filed returns pushed to AOs by CPC-ITR are required to be processed in ITBA portal (via ITR Processing > Return Receipt Register (RRR) Screen) as per the process described in ITBA Processing Instructions issued so far. The checkbox of 119(2)(a) would be enabled in “Inter Condonation details” Screen under ‘Part-A General’ segment of `Enter Return Details’ Screen by ITBA Team. Then AO will be able to Compute/Submit the return to CPC.

Such IT Rs will be submitted by the AO for processing in ITBA RRR Module through navigation-path: “Go to ITBA > ITR Processing > Return Receipt Register > View RRR > Search and Select Return and Click View/Proceed to Data Entry > (The checkbox of 11)(2)(a) would he available enabled in ‘Enter Condonation details” Screen under `Part-A General’ segment of ‘tater Return Details’ Screer0 Enter Return Details> Click on Save > Submit to CPC for computation”.

10. It is further emphasized that all such cases should be examined on priority and reference as per the prescribed procedure may be sent to this Directorate (through the screen “Enablement u/s 119”), as soon as possible_ It is expected that all the officers may henceforth use the aforesaid process, wherever required, while redressing the grievance of the taxpayers seeking refund where the relevant electronically filed valid lilts (upto AY 2021-22) could not be processed due to reasons not attributable to the assessee (as per the order u/s 119 of CBDT dated 16.10.2023 issued in partial modification of earlier order dated 05.07.2021, order dated 01.12.2023 and order dated 01.03.2024).

11. In case of any technical difficulty being observed, users may immediately contact the ITBA Helpdesk via:

A. Raising ticket at ITBA Helpdesk Portal.

B. Helpdesk telephone numbers: 011-69134300, 0120-2811201) and 0120-4836850

C. Email id: itba.Helpdesk@incometax.gov.in

12. This issues with t he prior approval of DGIT (Systems).

Yours sincerely,

(Ashim Kumar Modi)

Commissioner of Income Tax (ITBA),

Directorate of Income Tax (Systems), New Delhi

Copy to:

1. The P.P.S to Chairman, Member (Legislation), Member (Audit and Judicial), Member (Income Tax & Revenue), Member ( Fax Payers Services), Member (Systems & Faceless Scheme), Member (Administration), CBDT for kind information.

2. The P.S. to DGIT (S), Bangalore for kind information

3. The P.S. to DGIT (S), Delhi for kind information

4. The Web Manager of irsofficersonline.gov.in website with the request to upload the Instruction.

5. ITBA Publisher (ITBA.Publisher@incometax.gov.in) for https://itba.incometax.gov.in with a request to upload the Instruction on the ITBA Portal.

Yours sincerely,

(Ashim Kumar Modi)

Commissioner of Income Tax (ITBA),

Directorate of Income Tax (Systems), New Delhi

Income Tax Department

Department of Revenue, Ministry of Finance, Government of India

Functionality for processing of electronically filed valid returns having refund claims which were not processed within the time allowed u/s. 143(1) due to some technical or other reasons – ITR Module.

Please refer to CBDTs order u/s 119 dated 16.10.2023 [File No. 225/132/2023/ITA-II issued in partial modification of CBDT order u/s 119 dated 05.07 2021 (File No. 225/96/2020/ITA-II)] (for upto AY 2017-18), CBDTs order u/s 119 dated 01.12.2023 (File No. 225/132/2023/ITA-II) (for AY 2018-19 to 2020-21) and CBDTs another order u/s 119 dated 01.03.2024 (File No. 225/132/2023/ITA-II) (for AY 2021-22).

CBDT, in exercise of powers conferred on ft. under section 119 of the Act has issued an order u/s 119 dated 16.10.2023 (File No. 225/132/2023/ITA-II in partial modification of CBDT order U/s 119 dated 05.07 2021 (File No. 225/98/2020/ITA-II) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (upto AY 2017-18) till 31.01.2024 A detailed instruction in this regard has been issued vide ITBA Processing Instruction No. 15 dated 17.11.2023.

Further CBDT in exercise of powers conferred on it. under section 119 of the Act. has issued another order u/s 119 dated 01 12.2023 (File No 225/132/2023/ITA-II) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (for AY 2018-19 to 2020-21) till 31.01 2024 A detailed instruction in this regard has been issued vide ITBA Processing Instruction No.16 dated 11.12.2023.

Further, CBDT in exercise of powers conferred on it, under section 119 of the Act. has issued another order U/s 119 dated 31.01.2024 (File No 225/132/2023/ITA-II) and has extended the above mentioned time-limit of 31 01 2024 (mentioned in The aforesaid order(s) dated 16.10 2023 and 01.12 2023 to 30.04.2024.

Furthermore, CBDT in exercise of powers conferred on it, under section 119 of the Act has issued another order u/s 119 dated 01 03.2024 (File No. 225/132/2023/ITA-II) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (for AY 2021‑22) till 30 04 2024 A detailed instruction in this regard has been issued vide ITBA Processing Instruction No. 17 dated 26.03.2024.

In all such eligible cases. PCCIT/CCIT have to accord administrative approval for processing and concerned PCIT/CIT has to send reference to DGIT (Systems) so that Directorate of Systems can do necessary enablement for processing of such ITRs.

Once the reference has been made to DGIT (Systems) by PCIT/CIT (by using screen named “Enablement u/s 119″ in the ITBA’s ITR Processing Module), necessary enablement would be made in ITBA systems for processing of such ITRs Subsequently the processing action has to be performed by the respective assessing officer This document lists out the step by step procedure to be followed by Assessing Officer for processing of such eligible ITRs

The steps to be followed by AO users for processing of eligible ITRs as per CBDT Order u/s 119 dated 16.10.2023, 01.12.2023 and 01.03.2024 are as under:-

Once the details of administrative approval of PCCIT/CCIT have been submitted by PCIT/CIT through “Enablement u/s 119” in the ITBA’s ITR Processing Module and necessary enablement has been made in system SMS alert and Email will be sent to concerned Assessing Officer for necessary action in ITBA Portal.

USER : AO

1. For the cases up to AY 2015-16: Cases of these years will be required to be processed in ITBA through MOU (Manual Order Upload) functionality. The administrative approval of Pr.CCIT/CCIT will be entered by the PCIT/CIT in the system as per process mentioned in ITBA Processing instruction No 15 dated 17.11.2023 and thereafter necessary enablement would be made in ITBA to upload manual order through MOU.

Steps to process through Manual Order Upload is as follows‑

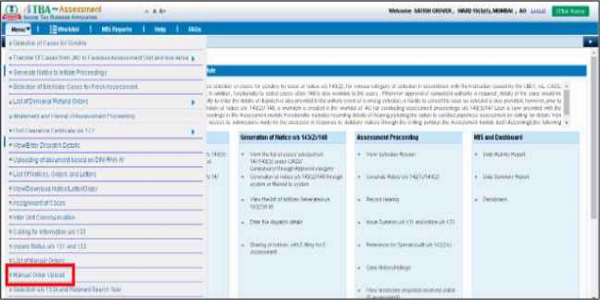

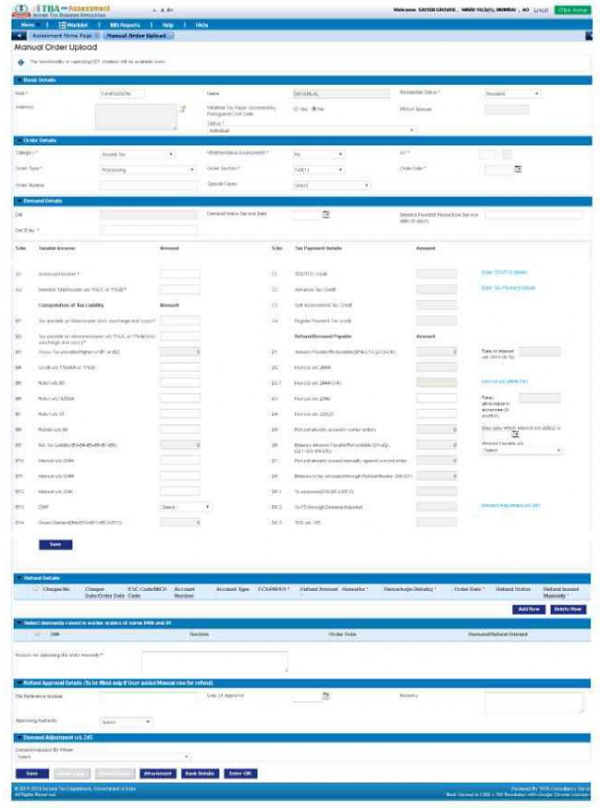

a) Navigate to Assessment module.

b) Go to Menu 4 Manual Order Upload link.

c) Enter PAN Based on PAN Name Residential Status will get auto-populated. Select Status.

d) Enter Order Details such as AY, Order Type (as Processing), Order Section (as 143(1)) Order date, Order Number

e) Enter the Income and Tax Payment Details on screen and Save.

f) Enter Reason for uploading the order manually and click on Save.

g) Order Copy button will be enabled after details are saved successfully Click on Order Copy.

h) Enter Date of Issue. File No. and click on Save & Generate DIN.

i) Enter Description, upload the order copy in File column and enter Date of Dispatch and Save.

j) Click on Generate Success message will be displayed on screen Navigate back to Manual order Upload screen.

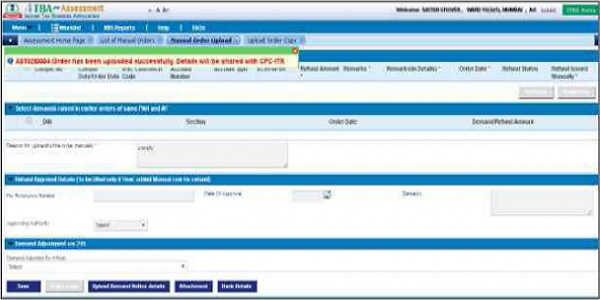

k) Upload Order button will be enabled on screen. Click on Upload Order Success message will be displayed

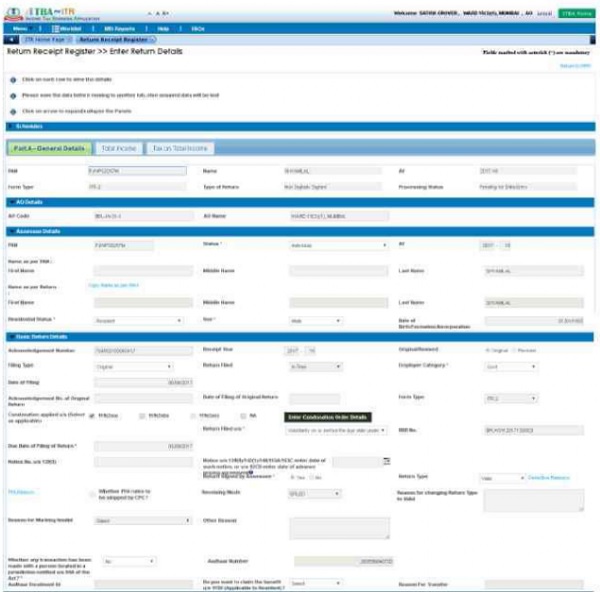

2. Cases of A.Ys. 2016-17 to 2021-22 : For the A.Ys. 2016-17 to 2021-22 the eligible ITRs are required to be processed at ITBA as per process described in ITBA Processing Instructions issued so far (including ITBA Instruction No.15, dated 17.11.2023, ITBA Processing Instruction No.16, dated 11.12.2023 and ITBA Processing Instruction No.17, dated 26.03.2024). The AOs are required to enter or modify the data and send the return to CPC-ITR for final computation and issuance of refund. Steps are mentioned below :

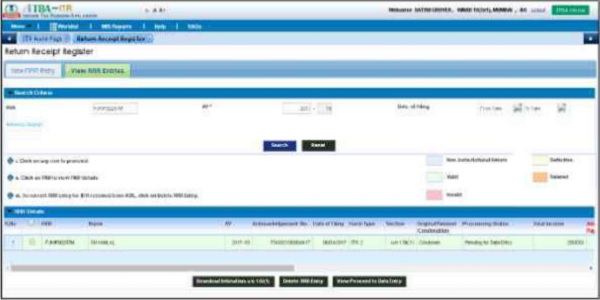

a). Navigate to ITR Processing module

b). Click on Return Receipt Register link under Quick Links.

c). Click on View RRR Entries tab. Enter PAN and AY and click on Search.

d). Select the record and click on View/Proceed to Data Entry button

e) Click on Enter Condonation Order Details button

Note The Condonation Order details entered by PCIT while enabling processing of return will be visible to AO in read-only mode.

f). Navigate back to Return Receipt Register screen and dick on Submit for Computation. The case will be submitted for computation to CPC.

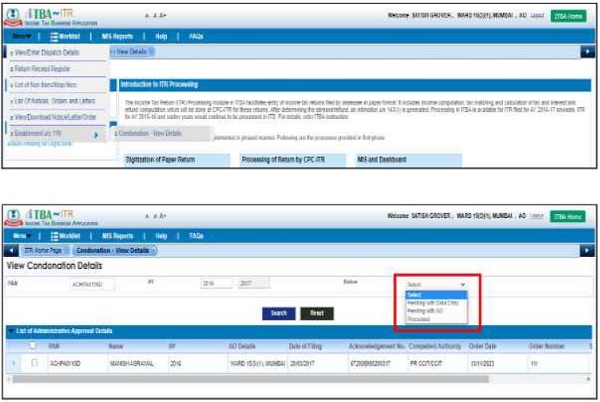

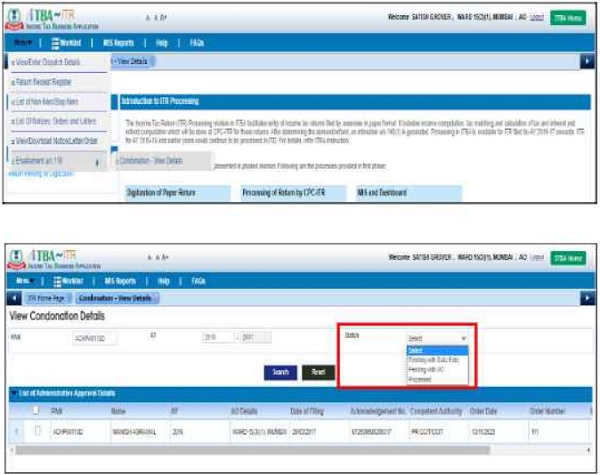

3. Details of cases referred by PCITICIT to DGIT (Systems) will be visible in the read-only mode to AO in ‘ITBA4ITR Processing4 Enablement u/s 119 > Condonation – View Details” screen. This screen will be accessible to AO and Range also. User may Search the record by entering PAN, AY and Status. Status will get updated as per actions of AC).

User: AO

Navigation: ITBA ->ITR Processing -> Enablement u/s 119 > Condonation — View Details

Functionality for sending reference to DGIT (Systems) by PCITICIT in the light of CBDT’s order u/s 119 dated 16.10.2023 [File No. 225/132/2023/ITA-11 issued in partial modification of CBDT order u/s 119 dated 05.07.2021 (File No. 225/98/2020/ITA-11)] (for upto AY 2017-18), CBDT’s order u/s 119 dated 01.12.2023 (File No. 225/132/2023/ITA-11) (for AY 2018-19 to 2020-21) and CBDT’s another order u/s 119 dated 01.03.2024 (File No. 225/132/2023/ITA-11) (for AY 2021-22).

CBDT, in exercise of powers conferred on it, under section 119 of the Act. has issued an order u/s 119 dated 16.10.2023 (File No. 225/132.12023111A-11) in partial modification of CBDT order u/s 119 dated 05.07,2021 (File No. 225/98/2020/ITA-11) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (upto AY 2017-18) till 31 01.2024 A detailed instruction in this regard has been issued vide ITBA Processing Instruction No. 15 dated 17.11.2023.

Further. CBDT in exercise of powers conferred on it, under section 119 of the Act, has issued another order u/s 119 dated 01.12.2023 (File No. 225/132/2023/ITA-II) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (for AY 2018-19 to 2020-21) till 31 01 2024. A detailed instruction in this regard has been issued vide ITBA Processing Instruction No. 16 dated 11.12.2023.

Further. CBDT in exercise of powers conferred on it, under section 119 of the Act. has issued another order u/s 119 dated 31.01.2024 (File No. 225/132/2023/ITA-11) and has extended the above mentioned time-limit of 31.01.2024 (mentioned in the aforesaid order(s) dated 16.10.2023 and 01.12.2023) to 30.04.2024.

Furthermore, CBDT in exercise of powers conferred on it, under section 119 of the Act, has issued another order u/s 119 dated 01 03.2024 (File No. 225/132/2023/ITA-11) and has relaxed the time frame prescribed in second proviso to sub section (1) of section 143 for processing of electronically filed valid ITRs (for AY 2021-22) till 30.04.2024. A detailed instruction in this regard has been issued vide ITBA Processing Instruction No. 17 dated 26.03.2024.

In all such eligible cases, PCCIT/CCIT have to accord administrative approval for processing and concerned PCIT/CIT has to send reference to DGIT (Systems) so that Directorate of Systems can do necessary enablement for processing of such ITRs

For the ease of making reference to DGIT (Systems) by Pr. CIT/CIT. a screen has been made available in the ITBA’s ITR Processing Module named “Enablement u/s 119”. It is requested that once administrative approval has been accorded by PCCIT/CCIT. the concerned PCIT/CIT should send reference to DGIT (Systems) in eligible cases only though this screen. This document lists out the step by step procedure to be followed by PCIT/CIT for sending such references,

The steps to be followed for sending reference to DGIT(Systems) as per “Enablement u/s 119” screen provided to CIT users (ITR Module) are as under: –

User: PCIT/CIT

1. Prior administrative approval of concerned CCIT/CCIT must be obtained for processing of such eligible time-barred returns.

2. Once administrative approval is accorded by the concerned PCCIT/CCIT, the concemed CIT/CIT would enter the details in the Condonation- Enter New Details screen in ITR Processing Module of ITBA. Once the details are entered and successfully submitted, necessary enablement will be made in system to enable the assessing officer to process the ITRs on case to case basis.

Steps of entering details are as follows :

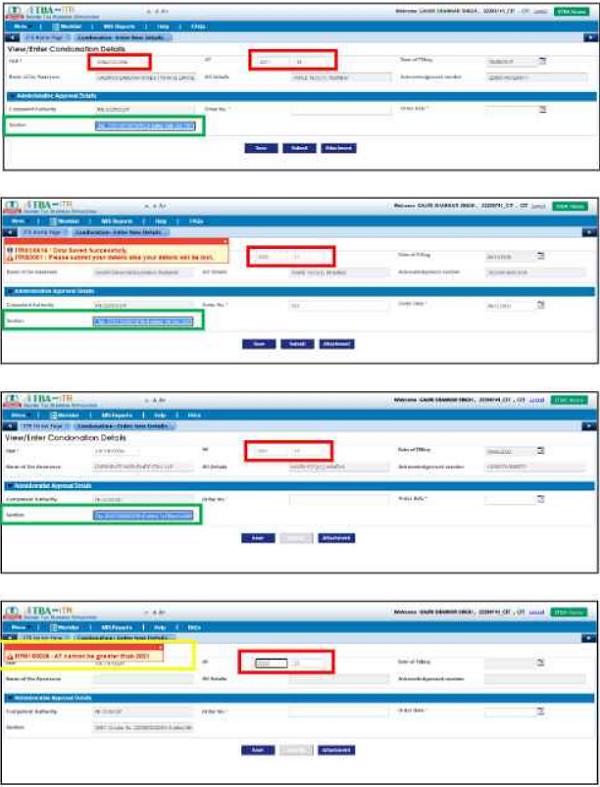

a. Login in ITBA, Open ITR Processing > Enablement Ws 119 > Condonation — Enter New details screen

b. PCIT/CIT has to enter PAN and AY. Basic Details like Name of Assessee, Date of Filing, AO Detail and Acknowledgement Number of return will be automatically populated if unprocessed return exists in the system. The concerned CBDT Order reference details will also be auto-populated based on the entered AY.

Notes:

i. The entry of AY can only be till AY 2021-22 as per CBDT order u/s 119 dated 16.10.2023, 01.12.2023 and 01.03.2024

ii. The order of CBDT u/s 119 dated 1610.2023, 01.12.2023 and 01.03.2024 is applicable only for electronically filed valid 1TRs. Therefore. paper returns are not covered under CBDTs aforesaid office orders. In case an 1TR has been filed electronically and is valid. the data of unprocessed ITR would be available in system. In case the ITR is paper return or is not a valid ITR, the data would not be available in system. If unprocessed return doesn’t exist in the system user will not be able to proceed.

iii. In case an ITR has been marked as defective by CPC then also the system would not allow the user to proceed ahead. In case there is any eligible defective ITR covered under the CBDT’s aforesaid orders, the AO may make communication with CPC regarding the same.

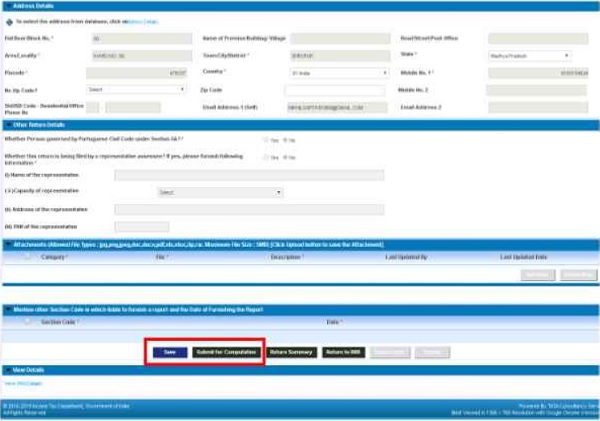

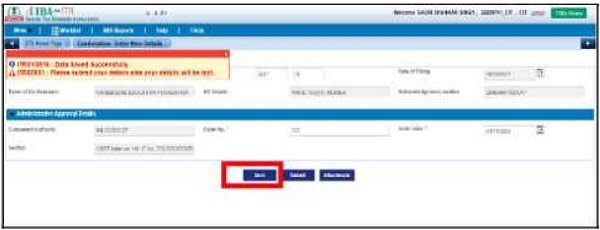

c. Thereafter, the PCIT/CIT has to enter details of the administrative approval accorded by the PCCIT/CCIT under “Administrative Approval Details”. PCIT/CIT should enter Order No. and Order Date of the administrative approval accorded by the PCCIT/CCIT. The PCIT/CIT user has to save the details by clicking ‘Save’ Button

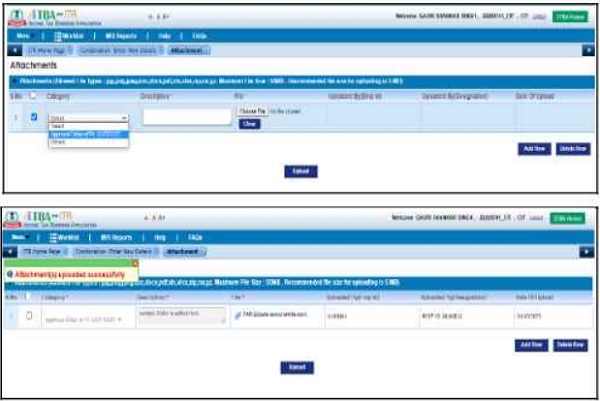

d. After saving the details, click on Attachment button and ‘Attachment screen will be opened. Choose category as “Approval Order of Pr. CCIT/CCIT’ (mandatory) to attach the order of administrative approval. Please note that it is mandatory to attach the administrative approval order of PCCIT/CCIT to proceed ahead. User may attach any other documents also, by adding row and choosing category as Others’ and clicking on ‘Upload’ Button.

e. After uploading Attachment, User may submit the record by clicking on ‘Submit’ Button.

Please note that merely saving the details by pressing “Save’ button is not sufficient the process would be complete and reference/details would be electronically moved to the System’s database only once the ‘Submit’ button is pressed.

Note: Once the details have been submitted and necessary enablement has been made in system, SMS alert and Email will be sent to concerned Assessing Officer for necessary action in ITBA Portal.

3. For the purpose of monitoring, the cases that have been submitted by PCITICIT, details of submitted cases will be Visible in the read-only mode to PCIT/CIT in ‘ITBA4ITR Processing4 Enablement u/s 119 > Condonation — View Details” screen. This screen will be accessible to AO and Range also User may Search the record by entering PAN, AY, AO and STATUS. Status will get updated as per actions of AO.

User: AO

Navigation. ITBA -> ITR Processing4 Enablement u/s 119 > Condonation — View Details

User: Range

Navigation: ITBA -> ITR Processing → Enablement u/s 119 > Condonation — View Details

Range user is able to search based on Status and AO as well.

User: PCIT/ CIT

PCIT/CIT user can search based on Status

PCIT/CIT user can search based on AO as well.

F. No. 225/132/2023/ITA-11

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

North Minch. the 01st March, 2024

Order under section 119 of the Income-tax Act. 1961

Subject: Processing of returns of income validly filed electronically with refund claims under section 143(1) of the Income-tux Act. 1961 beyond the prescribed time limits in nun-scrutiny cases-regd.

It has been brought to the notice of the Central Board of Direct faxes (‘Board’) that due to certain technical issues or for other reasons not attributable to the assessees contented, several returns for assessment year (AY) 2021-22. which were otherwise filed validly under section 139 or 142 or 119 of the Income tax Act. 1961 (‘Act’) could not be processed under sub-section (I) of section 143 of the Act. Consequently, intimation regarding processing of such returns could not be sent within the time farina prescribed under sub-section (1) of Section 143 of the Act. This has led to a situation where the taxpayers arc unable to get their legitimate refund in accordance with provisions of the Act, although the delay is not attributable to them.

2. The matter has been considered by Board. To mitigate genuine hardship being faced by the taxpayers on this issue. Board, by virtue of its powers under section 119 of the Act, hereby relaxes the time-frame prescribed in second proviso to sub-section (11 of section 143 and directs that all returns of income validly filed electronically for AY 2021-22 with refund claims. for which date of sending intimation under sub-section ( I) of section 143 of the Act has lapsed. subject to the exceptions mentioned in pant 4 below, can be processed now with prior administrative approval of Pr.CCIT/CCIT concerned. The intimation of such processing under sub-section (1) of section 143 of the Act can be sent to the assessee concerned by 30.04.2024.

3. All subsequent effects under the Act including issue of refund shall also follow as per the prescribed procedures. To ensure adequate safeguards, it has been decided that once administrative approval is accorded by the Pr.CCIT/CCIT. the Pr.CIT/CIT concerned would make a reference to the DGIT (Systems) to provide necessary enablement to the Assessing Officer on a case to case basis. The progress of disposal of such cases shall he monitored by the Pr.CIT/CIT concerned.

4. The relaxation accorded above shall not be applicable to the following returns:

a) returns selected in scrutiny;

b) returns remaining unprocessed, where either demand is shown as payable in the return or is likely to arise after processing it:

c) returns remaining unprocessed for any reason attributable to the assessee.

5. This may be brought to the notice of all for necessary compliance.

6. Hindi version to follow.

(Dr. Castro Jayaprakash. T)

Under Secretary to Govt. of India

Copy for information to:

i. Chairman (CBOT) and all Members of CBOT

ii. All Pr. CCsIT/DsGIT

iii. DGIT(Systems),Delhi it. DGIT (Systems),Bengaluru with request for further necessary action in the mutter

iv. ADG (TPS)-I and ADG(TPS)-2

v. ADG(Systems)-4 with request for uploading on department’s official website

vi. JCIT, Database Cell for uploading on IRS Officers website

vii. Guard file.

(Dr. Castro Jayaprakash. T)

Under Secretary to Govt. of India

F. No.225/132/2023/ITA-11

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

*****

North Block, the 31st January, 2024

Order under section 119 of the Income-tax Act, 1961

Subject: Processing of returns of income validly filed electronically with refund claims under section 143(1) of the Income-tax Act, 1961 beyond the prescribed time limits in non-scrutiny eases -regd.

Central Board of Direct Taxes (Board) vide its orders under section 119 of the Income-tax Act, 1961 (Act) dated 16.10.2023 and 01.12.2023 on the captioned subject relaxed the time prescribed in second proviso to sub-section (I) of Section 143 of the Act. It was directed that all returns of income validly filed electronically up to Assessment Year 2020-21 with refund claims which could not be processed under sub-section (I) of the Section 143 of the Act and which had become time-barred, should be processed by 31.01.2024, subject to the conditions/ exceptions specified therein.

2. The matter has been re-considered by Board in view of pending taxpayer grievances related to issue of refund. To mitigate the genuine hardship being faced by the taxpayers on this issue, Board, by virtue of its power under section 119 of the Act and in partial modification of its earlier orders under section 119 of the Act dated 16.102023 and 01.12.2023, supra, hereby further extends the time mentioned in the Para no. 2 of these orders till 30.04.2024 in respect of returns of income validly filed electronically up to AY 2020-21. All other contents of the said orders u/s 119 of the Act will remain unchanged.

3. This may be brought to the notice of all for necessary compliance.

(Dr. Castro Jayaprakash. T)

Under Secretary, (ITA-II), CBDT

Copy for information to:

i. Chairman (CBDT) and all Members of CBDT

ii. All Pr. CCsIT/DsGIT

iii. DGII(Systems), Delhi

iv. DG1T(Systems). Bengaluru with request for further necessary action in the matter Pr. DGIT (Admin & PS)

v. ADG (TPS-1) & ADO (TPS-2)

vi. ADG (Systems)-4 with request for uploading on department’s official website

vii. Database Cell for uploading on IRS Officers website

viii. Guard file

(Dr. Castro Jayaprakash. T)

Under Secretary, (ITA-II), CBDT

DIRECTORATE OF INCOME TAX (SYSTEMS)

ARA Center, G. Floor, E-2, Jhandewalan Extension, New Delhi-110055

F. No. System/ITBA/Instruction/ITR Processing/2023-24/

Dated: 11.12-2023

To,

All Pr. CCsIT / CCsIT

All Pr. DGsIT / DGsIT

All Pr. CsIT / CsIT / CsIT (Admin & TPS) All Pr. DsIT / DsIT

Madam/Sir,

Sub.: Functionality for processing of electronically filed valid returns (upto AY 2020-21) having refund claims which were not processed within the time allowed u/s 143(1) due to some technical or other reasons.

Ref: 1. CBOT Order u/s /19 of Income Tax Act, 1961 dated 01.12.2023

2. MT Order u/s 119 of Income Tax Act, 1961 dated 16.10.2023

(issued in partial modification of earlier order u/s 119 doted 05.07.2021 and 30.092021)

Kindly refer to the above.

2. References from the field formations and taxpayers have been received in Board informing that due to certain technical or other reasons, not attributable to the assessee, several returns for various years, which were otherwise filed validly under section 139, 142 and 119 of the Income-tax Act, 1961, could not be processed within the time prescribed under section 143(1) of the Act due to which refund due to the assessee could not be issued.

3. The CBDT in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961 vide its Order dated 05.07.2021 and 30.09.2021 issued through File No. 225/98/2020/ITA-11 had relaxed the time frame prescribed in Second proviso to sub section (1) of section 143 till 30.11.2021. Further, the CBDT vide its Order under section 119 of the Act dated 16.10.2023 issued through File No. 225/132/2023/ITA-II, relaxed the time frame prescribed in second proviso to sub section (1) of section 143 (for the eligible cases upto AY 2017-18) till 31.01.2024. For the above purpose, the ITBA Processing Instruction No. 15 has already been issued on 17.11.2023,

4. To mitigate the genuine hardship being faced by the taxpayers on this issue, the CBDT, in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961, has further relaxed the time frame prescribed in second proviso to sub section (1) of section 143 (for the eligible cases for AYs 2018.19, 2019-2020 & 2020-21 also) till 31.01.2024. In this regard, CBDT has issued an order u/s 119 dated 01.12.2023 through File No.225/132/2023/ITA-11. The CBDT’s earlier order dated 16.10.2023 (for AYs upto 2017-18) and order dated 01.12.2023 (for AYs 2018-19, 2019-2020 & 2020-21) does not cover paper return and Is applicable for only electronically filed valid ITRs.

5. As per the above referred order(s) of CBOT (dated 16.10.2023 and 01.12.2023), all such unprocessed time-barred electronically filed valid ITRs upto AY 2020-21 (subject to other exceptions mentioned in CBDT’s Order u/s 119 dated 05.07.2021, 16.10.2023 & 01.12.2023) can now be processed with prior administrative approval of concerned Pr.CCIT/CCIT. Once administrative approval is accorded by Pr.CCIT/CCIT, the concerned Pr.CIT/CIT shall make a reference to DGIT(Systems) to provide necessary enablement to Assessing Officer for processing of return.

6. For the ease of making reference to DGIT (Systems) by Pr. CIT/CIT, a screen has been made available in the ITBA’s ITR Processing Module named “Enablement u/s 119”. It is requested that all Pr. CsIT/CsIT should use this screen for making a reference to DGIT (Systems) for making necessary enablement w.r.t. CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07,2021) and order dated 01.12.2023. Further, all concerned are requested to process such references/proposals at the earliest, for the enablement of processing of such unprocessed time barred returns filed electronically. It is to clarify that in each such case, the processing rights will be enabled by the ITBA team and subsequently, the processing action has to be performed by the respective Assessing Officer. The proposals for the enablement of time barred processing may kindly be submitted by PCsIT/CsIT before 05.01.2024 so that these references can be enabled/processed well within the time period ending on 31.01.2024.

7. Following scheme and validation are prescribed in the CBDT’s above order dated 05.07.2021, 16.10.2023 and 01.12.2023 :

Pre-Conditions :

(i) The ITR should be —

- for AY upto AY 2020-21.

- a valid ITR.

- electronically filed.

- filed within permitted time limit u/s 139, 142(1) or 119 of the Act. (II) Assessee has claimed refund in return of income.

(ii) On computation, the resultant outcome is refund.

(iii) The returns of income should not have remained unprocessed due to any reason attributable to the concerned

(iv) The returns of Income should not be under Scrutiny assessment.

8. Processes to be followed In the POT/ CIT :

8.1 Prior administrative approval of concerned Pr. CCIT/CCIT must be obtained for processing of such time-barred eligible electronically filed valid returns of income as mentioned in CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07.2021) and order dated 01.12.2023.

8.2 Once administrative approval is accorded by the concerned Pr, CCIT/CCIT, the concerned Pr. CIT/CIT would enter the details in the screen available in ITR Processing Module-> “Enablement u/s 119″ to refer the case to the DGIT(Systems) for the purpose of providing necessary enablement to the assessing officer for processing such return.

Steps of entering/submitting details by Pr.CIT/CIT for making reference to KIT (Systems):

a) In ITBA, Open ITR Processing > Enablement u/s 119 > Condonation — Enter New details.

b) Enter PAN and AY of the case. Thereafter, basic details like Name of Assessee, AO Detail, Date of Filing of ITR and Acknowledgement No. of electronically filed valid ITR will be automatically populated if such. unprocessed return is available in the system.

c) Thereafter, enter Pr. CCIT/CCIT administrative approval Order No. and Order Date. Once this is done, the details have to be saved by clicking ‘Save’ Button.

d) After saving the details, click on Attachment button and ‘Attachment’ screen will be opened. Choose category “Approval Order of Pr. CCIT/CCIT” to attach the order of approval (uploading of Administrative Approval of Pr.CCIT/CCIT is compulsory and mandatory). Further, if needed, any other documents may also be attached, by adding row and choosing category as ‘Others’ and Clicking on ‘Upload’ Button.

e) After Attachment, submit the details by mandatorily clicking on ‘Submit’ Button.

f) Please note that merely saving the details by pressing “Save” button is not sufficient, the reference/details would be electronically moved to the System’s database only once the “Submit” button Is pressed.

8.3 Submitted details will be visible for record/monitoring purpose In the read only mode at ITBA portal via navigation path “ITBA > ITR Processing > Enablement u/s 119 > Condonation — View Details” screen (This screen will be accessible to Pr.CIT/CIT, Range-Head and AO). User may Search the record by entering PAN and AY. Status will get updated as per the actions taken by AO.

9. Processes to be followed by the AOs

9.1 For the cases up to A.Y. 2015-16: Cases for these years will be processed through MOU. The AO can process such time-barred eligible returns manually and upload the same through Manual Order Upload (MOU) functionality as explained in ITBA Assessment/Processing Instructions issued so far to submit the return to CPC.

Such rifts are required to be processed manually by the AO (after getting approval of the Pr.CCIT/CCIT and making reference by the PC1T/CIT in the screen “Enablement u/s 119’7 and upload in ITBA portal via Manual Order Upload (MOU) functionality through the navigation-path “Go to ITBA > Assessment home page > Menu > Manual Order Upload”.

9.2 Cases of A. Y. 2016-17 to 2020-21: For the A.Y. 2016-17 to 2020-21, all the e-filed returns pushed to AOs by CPC ITR are required to be processed in ITBA portal (via ITR Processing > Return Receipt Register (RRR) Screen) as per the process described in ITBA Processing Instructions issued so far. The checkbox of 119(2)(a) would be enabled in ‘Enter Condonation details” Screen under ‘Part-A General’ segment of ‘Enter Return Details’ Screen by ITBA Team. Then AO will be able to Compute/Submit the return to CPC.

Such ITRs will be submitted by the AO for processing in ITBA RRR Module through navigation-path: “Go to ITBA> ITR Processing > Return Receipt Register > View RRR > Search and Select Return and Click View/Proceed to Data Entry > (The checkbox of 119(2)(a) would be available enabled in ‘Enter Condonation details’ Screen under Part-A General’ segment of ‘Enter Return Details’ Screen)> Enter Return Details> Click on Save > Submit to CPC for computation”.

10. it is further emphasized that all such cases should be examined on priority and reference as per the prescribed procedure may be sent to this Directorate (through the screen “Enablement u/s 119“), as soon as possible. It is expected that all the officers may henceforth use the aforesaid process, wherever required, while redressing the grievance of the taxpayers seeking refund where the relevant electronically filed valid ITRs (upto AY 2020-21) could not be processed due to reasons not attributable to the assessee (as per the order u/s 119 of CBDT dated 16.10.2023 issued in partial modification of earlier order dated 05.07.2021 and order dated 01.12.2023).

11. In case of any technical difficulty being observed, users may immediately contact the ITBA Helpdesk via:

A. Raising ticket at ITBA Helpdesk Portal.

B. Helpdesk telephone numbers: 011-69134300, 01.20 2811200 and 0120 4836,850

C. Email id : itba.helpdesk@incometax.gov.in

2. This issues with the prior approval of DGIT (Systems).

Yours sincerely,

(Ashim Kumar Modi)

Commissioner of Income Tax (ITBA)

Directorate of Income Tax (Systems),

New Delhi

Copy to:

1. The P.P.S to Chairman, Member (Legislation), Member (Audit and Judicial), Member (Income Tax & Revenue), Member (Tax Payers Services), Member (Systems & 1-aceless Scheme), Member (Administration), CBDT for kind information.

2. The P. S. to DGIT (S), Bangalore for kind information

3. The P.S. to DGIT (5), Delhi for kind information

4. The Web Manager of www.irsoffcersonline.gov.in website with the request to upload the Instruction.

5. ITBA Publisher (ITBA Publisher@incometax.govin) for https://itbanincometax.gov.in with a request to upload the Instruction on the ITBA Portal.

Yours sincerely,

(Ashim Kumar Moth)

Commissioner of Income Tax (ITBA),

Directorate of Income Tax (Systems),

New Delhi

F. No. 225/132/2023/ITA-II

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

****

North Block, the 1st December, 2023

Order under section 119 of the Income-tax Act, 1961

Subject: Processing of returns of income validly filed electronically with refund claims under section 143(1) of the Income-tax Act, 1961 beyond the prescribed time limits in non-scrutiny cases-regd.

It has been brought to the notice of the Central Board of Direct Taxes (‘Board’) that due to certain technical issues or for other reasons not attributable to the assessees concerned, several returns for assessment years (AYs) 2018-19, 2019-20 and 2020-21, which were otherwise filed validly under section 139 or 142(1) or 119 of the income tax Act, 1961 (‘Act’) could not be processed under sub-section (I) of section 143 of the Act. Consequently, intimation regarding processing of such returns could not be sent within the time frame prescribed under sub-section (I) of section 143 of the Act. This has led to a situation where the taxpayers are unable to get their legitimate refund in accordance with provisions of the Act, although the delay may not be attributable to them.

2. To resolve the grievances of such taxpayers, the Board had earlier issued instructions/orders u/s 119 of the Act from time to time relaxing the prescribed statutory time limit for processing of such validly tiled returns with refund claims in non-scrutiny cases. As per the latest order dated 16th October, 2023, time frame was given till 31.01.2024 to process returns of income validly filed electronically with refund claims upto AY 2017-18.

3. The matter has been considered by the Board in view of pending grievances of taxpayers related to issue of refund for AYs 2018-19, 2019-20 and 2020-21. To mitigate genuine hardship being faced by the taxpayers on this issue, the Board, by virtue of powers vested with it under section 119 of the Act, hereby relaxes the time-frame prescribed in second proviso to sub-section (1) of section 143 and directs that all returns of income validly filed electronically with refund claims for AYs 2018-19, 2019-20 and 2020-21, for which date of sending intimation under sub-section (1) of section 143 of the Act has lapsed, subject to the exceptions mentioned in pare 5 below, can be processed now with prior administrative approval of Pr.CCIT/CCIT concerned. The intimation of such processing under sub-section (1) of section 143 of the Act can be sent to the assessee concerned by 31.01.2024.

4. All subsequent effects under the Act including issue of refund shall also follow as per the prescribed procedures. To ensure adequate safeguards, it has been decided that once administrative approval is accorded by the Pr.CCIT/CCIT, the Pr.CCIT/CIT concerned would make a reference to the DGIT (Systems) to provide necessary enablement to the Assessing Officer on a case to case basis. The progress of disposal of such cases shall he monitored by the Pr.CIT/CIT concerned.

5. The relaxation accorded above shall not be applicable to the following returns:

a) returns selected in scrutiny;

b) returns remain unprocessed, where either demand is shown as payable in the return or is likely to arise after processing it;

c) returns remain unprocessed for any reason attributable to the assessee.

6. This may be brought to the notice of all for necessary compliance.

7. Hindi version to follow.

(Dr. Castro Jayaprakash.T)

Under Secretary to Government of India

Copy for information to:

i. Chairman (CBDT) and all Members of CBDT

ii. All Pr CCsIT/DsGIT

iii. DGIT(Systems),Delhi & DGIT (Systems),Bengaluru with request for further necessary action in the matter

iv. ADG (TPS)-1 and ADG(TPS)-2 with request for further necessary action in the matter

v. ADG(Systems)-4 with request for uploading on department’s official website

vi. JICIT, Database Cell for uploading on IRS Officers website

vii. Guard file

(Dr. Castro Jayaprakash.T)

Under Secretary to Government of India

ITBA Processing Instruction No. 15

DIRECTORATE OF INCOME TAX (SYSTEMS)

ARA Center, G. Floor, E-2, jhandewalan Extension, New Delhi-110055

No. System/ITBA/Instruction/ITR Processing/2023-24/

Dated: 17-11-2023

To,

All Pr. CCsIT / CCsIT

All Pr. DGsIT / DGsIT

All Pr. CsIT / CsIT / CsIT (Admin & TPS) All Pr. DsIT / DsIT

Madam/Sir,

Sub. : Functionality for processing of electronically filed valid returns (upto AY 2017-18) having refund claims which were not processed within the time allowed u/s 143(1) due to some technical or other reasons.

Ref : CBDT Order u/s 119 of Income Tax Act, 1961 dated 16.10.2023

(issued in partial modification of earlier order u/s 119 dated 05.07.2021 and 30.09.2021)

Kindly refer to the above.

2. References from the field formations and taxpayers have been received in Board informing that due to certain technical or other reasons, not attributable to the assessee, several returns for various years, which were otherwise filed validly under section 139, 142 and 119 of the Income-tax Act, 1961, could not be processed within the time prescribed under section 143(1) of the Act due to which refund due to the assessee could not be issued.

3. The CBDT in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961 vide its earlier Order dated 05.07.2021 and 30.09.2021 issued through File No. 225/98/2020/1TA-11 had relaxed the time frame prescribed in Second proviso to sub section (1) of section 143 till 30.11.2021.

4. To mitigate the genuine hardship being faced by the taxpayers on this issue, the CBDT, in exercise of powers conferred on it, u/s 119 of the Income-tax Act, 1961, has further relaxed the time frame prescribed in second proviso to sub section (1) of section 143 (for the eligible cases upto AY 2017-18) till 31.01.2024 vide its Order under section 119 of the Act dated 16.10.2023 issued through File No. 225/132/2023/ITA-11. The order dated 16.10.2023 has been issued in partial modification of earlier order u/s 119 dates 05.07.2021. All other contents of the aforesaid order dated 05.07.2021 continue to apply except the fact that the order dated 16.10.2023 does not cover paper return and is applicable for only electronically filed valid ITRs.

5. As per the above referred order of CBDT, all such unprocessed time-barred electronically filed valid ITRs upto AY 2017-18 (subject to other exceptions mentioned in CBDT’s Order u/s 119 dated 05.07.2021 & 16.10.2023) can now be processed with prior administrative approval of concerned Pr.CCIT/CCIT. Once administrative approval is accorded by Pr. CCIT/CCIT, the concerned Pr.CIT/CIT shall make a reference to DGIT(Systems) to provide necessary enablement to Assessing Officer for processing of return.

6. For the ease of making reference to DGIT (Systems) by Pr. CIT/CIT, a screen has been made available in the ITBA’s ITR Processing Module named “Enablement u/s 119″. It is requested that all Pr. CsIT/CsIT should use this screen for making a reference to DGIT (Systems) for making necessary enablement w.r.t. CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07.2023). Further, all concerned are requested to process such references/proposals at the earliest, for the enablement of processing of such unprocessed time barred returns filed electronically. It is to clarify that in each such case, the processing rights will be enabled by the ITBA team and subsequently, the processing action has to be performed by the respective Assessing Officer. The proposals for the enablement of time barred processing may kindly be submitted by PCsIT/CsIT before 05.01.2024 so that these references can be enabled/processed well within the time period ending on 31.01.2024.

7. Following scheme and validation are prescribed in the CBDT’s above order dated 05.07.2021 and 16.10.2023 :

Pre-Conditions :

(i) The ITR should be —

- for AY upto AY 2017-18.

- a valid ITR.

- electronically filed.

- filed within permitted time limit u/s 139, 142(1) or 119 of the Act.

(ii) Assessee has claimed refund in return of income.

(iii) On computation, the resultant outcome is refund.

(iv) The returns of income should not have remained unprocessed due to any reason attributable to the concerned assessee.

(v) The returns of income should not be under Scrutiny assessment.

8. Processes to be followed by the PCIT / CIT :

8.1 Prior administrative approval of concerned Pr. CCIT/CCIT must be obtained for processing of such time-barred eligible electronically filed valid returns of income as mentioned in CBDT’s aforesaid order dated 16.10.2023 (issued in partial modification of earlier order dated 05.07.2021).

8.2 Once administrative approval is accorded by the concerned Pr. CCIT/CCIT, the concerned Pr. CIT/CIT would enter the details in the screen available in ITR Processing Module-> “Enablement u/s 119” to refer the case to the DGIT(Systems) for the purpose of providing necessary enablement to the assessing officer for processing such return.

Steps of entering/submitting details by Pr.CIT/CIT for making reference to DGIT (Systems):

a) In ITBA, Open ITR Processing > Enablement u/s 119 > Condonation — Enter New details.

b) Enter PAN and AY of the case. Thereafter, basic details like Name of Assessee, AO Detail, Date of Filing of ITR and Acknowledgement No. of electronically filed valid ITR will be automatically populated if such unprocessed return is available in the system.

c) Thereafter, enter Pr. CCIT/CCIT administrative approval Order No. and Order Date. Once this is done, the details have to be saved by clicking ‘Save’ Button.

d) After saving the details, click on Attachment button and ‘Attachment’ screen will be opened. Choose category “Approval Order of Pr. CCIT/CCIT” to attach the order of approval (uploading of Administrative Approval of Pr.CCIT/CCIT is compulsory and mandatory). Further, if needed, any other documents may also be attached, by adding row and choosing category as ‘Others’ and Clicking on ‘Upload’ Button.

e) After Attachment, submit the details by mandatorily clicking on ‘Submit’ Button.

f) Please note that merely saving the details by pressing “Save” button is not sufficient, the reference/details would be electronically moved to the System’s database only once the “Submit” button is pressed.

8.3 Submitted details will be visible for record/monitoring purpose in the read only mode at ITBA portal via navigation path “ITBA > ITR Processing > Enablement u/s 119 > Condonation — View Details” screen (This screen will be accessible to Pr.CIT/CIT, Range-Head and AO). User may Search the record by entering PAN and At Status will get updated as per the actions taken by AO.

9. Processes to be followed by the AOs :

9.1 For the cases up to A.Y. 2015-16: Cases for these years will be processed through MOU. The AO can process such time-barred eligible returns manually and upload the same through Manual Order Upload (MOU) functionality as explained in ITBA Assessment/Processing Instructions issued so far to submit the return to CPC.

Such ITRs are required to be processed manually by the AO (after getting approval of the Pr.CCIT/CCIT and making reference by the PCIT/CIT in the screen “Enablement u/s 1191 and upload in ITBA portal via Manual Order Upload (MOU) functionality through the navigation-path “Go to ITBA > Assessment home page > Menu > Manual Order Upload”.

9.2 Cases of A. Y. 2016-17 & 2017-18: For the A.Y. 2016-17 & 2017-18, all the e-filed returns pushed to AOs by CPC-ITR are required to be processed in ITBA portal (via ITR Processing > Return Receipt Register (RRR) Screen) as per the process described in ITBA Processing Instructions issued so far. The checkbox of 119(2)(a) would be enabled in ‘Enter Condonation details” Screen under ‘Part-A General’ segment of ‘Enter Return Details’ Screen by ITBA Team. Then AO will be able to Compute/Submit the return to CPC.

Such ITRs will be submitted by the AO for processing in ITBA RRR Module through navigation-path: “Go to ITBA > ITR Processing > Return Receipt Register > View RRR > Search and Select Return and Click View/Proceed to Data Entry > (The checkbox of 119(2)(a) would be available enabled in ‘Enter Condonation details” Screen under ‘Part-A General’ segment of ‘Enter Return Details’ Screen)> Enter Return Details> Click on Save > Submit to CPC for computation”.

10. It is further emphasized that all such cases should be examined on priority and reference as per the prescribed procedure may be sent to this Directorate (through the screen “Enablement u/s 119″), as soon as possible. It is expected that all the officers may henceforth use the aforesaid process, wherever required, while redressing the grievance of the taxpayers seeking refund where the relevant electronically filed valid ITRs (upto AY 2017-18) could not be processed due to reasons not attributable to the assessee (as per the order u/s 119 of CBDT dated 16.10.2023 issued in partial modification of earlier order dated 05.07.2023).

11. In case of any technical difficulty being observed, users may immediately contact the ITBA Helpdesk via:

A. Raising ticket at ITBA Helpdesk portal.

B. Helpdesk telephone numbers : 0120-2811200 and 0120-4836850

C. Email id : helpdesk®incometax.gov.in

12. This issues with the prior approval of DGIT (Systems).

Yours sincerely,

(Ashim Kumar Modi)

Commissioner of Income Tax (ITBA),

Directorate of Income Tax (Systems),

New Delhi

Copy to:

1. The P.P.S to Chairman, Member (Legislation), Member (Audit and Judicial), Member (Income Tax & Revenue), Member (Tax Payers Services), Member (Systems & Faceless Scheme), Member (Administration), CBDT for kind information.

2. The P.S. to DGIT (S), Bangalore for kind information

3. The P.S. to DGIT (S), Delhi for kind information

4. The Web Manager of www. irsofficersonline.govin website with the request to upload the Instruction.

5. ITBA Publisher (ITBA.Publisher@incometax.gov.in) for https://itbaincometax.aovin with a request to upload the Instruction on the ITBA Portal.

Yours sincerely,

(Ashim Kumar Modi)

Commissioner of Income Tax (ITBA),

Directorate of Income Tax (Systems),

New Delhi

F.No.225/132/2023/ITA-II

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

****

North Block, the 16th October, 2023

Order under section 119 of the Income-tax Act, 1961

Subject: Processing of returns with refund claims under section 143(1) of the Income-tax Act, 1961 beyond the prescribed time limits In non-scrutiny casts-regd.

Central Board of Direct Taxes (Board) vide its order under section 119 of the Income-tax Act, 1961 (Act) dated 05.07.2021 and 30.09.2021 on the captioned subject relaxed the timeframe prescribed in second proviso to sub-section (1) of Section 143 of the Act. It was directed that all validly filed returns up to Assessment Year 2017-18 with refund claims, which could not be processed under sub-section ( I) of the Section 143 of the Act and which had become time-barred, should be processed by 30.11.2021, subject to the conditions/ exceptions specified therein.

2. The matter has been re-considered by Board in view of pending taxpayer grievances related to issue of To mitigate the genuine hardship being faced by the taxpayers on this issue, Board, by virtue of its power under section 119 of the Act and in partial modification of its earlier order under section 119 of the Act dated 05.07.2021 and 30.09.2021, supra, hereby further extends the time frame mentioned in the para no. 2 of the order dated 30.09.2021 till 31.01.2024 in respect of returns of income validly filed electronically. All other contents of the said order u/s 119 of the Act dated 05.07.2021 will remain unchanged.

3. This may be brought to the notice of all for necessary compliance.

(Dr. Castro Jayaprakash.T)

Under Secretary to Government of India

Copy for information to:

i. Chairman (CBDT) and all Members of CBDT

ii. All Pr. CCsITiDsGIT

iii. DGIT(Systems), Delhi

iv. DGIT(Systems). Bengaluru with request for further necessary action in the matter

v. ADG(Systems)-4 with request for uploading on department’s official website

vi. JCIT, Database Cell for uploading on IRS Officers website

vii. Guard file

(Dr. Castro Jayaprakash.T)

Under Secretary to Government of India

No. 225/98/2020 – ITA-11

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

**************************

Room No. 245A, ITA-II division

New Delhi, the 30th September 2021.

Order under Section 119 of the income-tax Act,1961

Subject: Processing of returns with refund claims under section 143(1) of the Income-tax Act 1961 beyond the prescribed time limits in non-scrutiny cases – reg

Central Board of Direct Taxes (Board) vide its order under section 119 of the Income-tax Act, 1961 (Act) dated 05.07.2021 on the captioned subject relaxed the time-frame prescribed in second proviso to sub-section (1) of Section 141 of the Act. It was directed that all validln,, filed returns up to Assessment Year 2017-18 with refund claims, which could not be processed under sub-section (1) of the Section 143 of the Act and which had become time-barred, should be processed by 30.09.2021 subject to the conditions/exceptions specified therein.

2. The matter has been re-considered by Board in view of pending taxpaver’s grievances related to issue of refund. To mitigate the genuine hardship being faced by the taxpayers on this issue, Board, by virtue of its power under section 119 of the Act and in partial modification of its earlier order under section 119 of the Act dated 07.2021, supra. hereby further extends the time frame mentioned in the para no 1 of the said order from 30.09.2021 to 30.11.2021. All other contents of the said order ups 119 of the Act dated 05.07.2021 will remain unchanged.

3. This may be brought to the notice of all for necessary compliance.

(Sourabh Jain)

Under Secretary to the Government of India

Copy to:-

1. Chairman, CBDT and all the Members of CBDT.

2. All Pr. CCsIT/ Pr. DGsIT.

3. DGIT (Systems) with request for further necessary action in the matter.

4. Web Manager, with request for uploading on department’s official website www.incornetaxindia.gov.in

5. JCIT, Database Cell for uploading on IRS Officers website www.irsofficersonline. gov.in

6. Guard File

(Sourabh Jain)

Under Secretary to the Government of India

No.225/98/2020/1TA-II

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

*****

North Block, the 5th July, 2021

Order under section 119 of the Income-tax Act, 1961

Subject: Processing of returns with refund claims under section 143(1) of the Income-tax Act, 1961 beyond the prescribed time limits in non-scrutiny cases-regd.

It has been brought to the notice of the Central Board of Direct Taxes (*Board’) that due to certain technical issues or for other reasons not attributable to the assessees concerned, several returns for various assessment years up to the assessment year 2017-18 which were otherwise filed validly under section 139 or 142 or 119 of the Income-tax Act, 1961 (‘Act’) could not be processed under sub-section (1) of section 143 of the Act. Consequently. intimation regarding processing of such returns could not be sent within the period of one year from the end of the financial year in which such returns were filed as prescribed in the second proviso to sub-section (1) of section 143 of the Act. This has led to a situation where the taxpayer is unable to get his legitimate refund in accordance with provisions of the Act. although the delay is not attributable to him.

2. To resolve the grievances of such taxpayers. Board had earlier issued instructions/orders u/s 119 of the Act from time to time relaxing the prescribed statutory time limit for processing of such validly filed returns with refund claims in non-scrutiny cases. As per the earlier order dated 10th July time frame was given till 31.10.2020 to process such returns with refund claims.

3. The matter has been re-considered by Board in view of pending taxpayers’ grievances related to issue of refund. To mitigate genuine hardship being faced by the taxpayers on this issue, Board. by virtue of its powers under section 119 of the Act. hereby relaxes the time-frame prescribed in second proviso to sub-section (1) of section 143 and directs that all validly tiled returns up to assessment year 2017-18 with refund claims. which could not be processed under sub-section (I) of section 143 of the Act and which have become time-barred, subject to the exceptions mentioned in para below. can be processed now with prior administrative approval of CC1T/CCIT concerned. The intimation of such processing under sub-section (1) of section 143 of the Act can be sent to the assessee concerned by 30.09.2021. All subsequent effects under the Act including issue of refund shall also follow as per the prescribed procedures. To ensure adequate safeguards. it has been decided that once administrative approval is accorded by the Pr.CCIT/CCIT, the Pr CIT/CTT concerned would make a reference to the DG1T(Systems) to provide necessary enablement to the Assessing officer on a case to case basis.

4. The relaxation accorded above shall not he applicable to the following returns:

(a) returns selected in scrutiny;

(b) returns remain where either demand is shown as payable in the return or is likely to arise after processing it-,

(c) returns remain unprocessed for any reason attributable to the assessee.

5. This may be brought to the notice of all for necessary compliance.

(Prajna Paramita)

Director to the Government of India

Copy for Information to:

1) Chairman (CRDT) and all Members of CBDT

2) All Pr. CCsIT/DsGIT with request for further necessary action in the matter.

3) DGIT(Systems) with request for further necessary action in the matter.

4) ADG(Systems)-4/Web Manager with request for uploading on departmental website.

5) JCIT, Database Cell for uploading on the website irsofficersonline.

6) Guard file.

(Prajna Paramits)

Director to the Government of India