Pratap Singh

Commissioner,

Income Tax (TDS)

Mumbai

mumbai.cit.tds2@incometax.gov.in

The Author is from 1991 batch of Indian Revenue Service (IRS) and is an Engineering graduate from IIT Kanpur and has done LLB and MBA. He has worked in various capacities at Delhi, Kanpur, Bangalore and Mumbai and is presently posted as CIT-TDS Mumbai. He has been part of various initiatives of the department and is part of the committee constituted by CBDT on E commerce transaction. He has authored two research papers on ‘Demonetisation 2016’ and ‘Taxation in India: Trends and Issues’. The present paper discusses ‘Emerging issues in TDS ‘which contains new areas of TDS mobilization like securitization Trusts, Interest Subvention, multi brand retail, banking correspondent businesses, year end provisions, Railway intermediaries, and TDS on e-commerce transactions. The paper gives some insight in these areas and will certainly help the TDS officers around the country to mobilize additional revenue.

Executive Summary

TDS contributes about 43% of direct taxes revenue as also significant proportion of indirect tax collections. Besides it is the most regular source of revenue unlike advance tax which is received in four installments. Therefore in recent years the Government has placed more and more reliance on such mode of tax collection which is very convenient and cost effective. With globalization and expansion of economic landscape, various new and emerging areas of TDS mobilization have come into play which have to be effectively tapped not only to mobilize the valuable revenue but also to expand the tax base.

This paper covers some of these new and emerging areas of TDS mobilization. The first section deals with interest subvention scheme being prevalent in real estate sector. In this scheme a builder undertakes to pay interest on housing loan for a few years on behalf of the customer, which is not being subjected to TDS and therefore has huge tax potential and significant work in this regard has been done in TDS- Mumbai. The next section deals with TDS on E-Commerce transactions, which have grown by leaps and bounds, in the form of online retailing like Amazon, Flipkart etc., food portals like Ube rets, Swiggy, Zomato etc., taxi aggregators, room aggregators (Oyo Rooms), ticket booking platforms( Book my show), online ticketing like makemytrip, yatra online etc. It is seen that TDS provisions are not being properly followed. Some action in this regard has been taken by Mumbai, Delhi, Jaipur and Pune region to bring such transaction under TDS net, which has got enormous potential. In the third section deals with TDS issues in Multi Brand Retail stores or Large Format stores like Pantaloons, Shoppers Stop, West Side etc., where Sale or on return basis model is followed. It is seen that in such stores, only space is provided to the Brands and therefore whatever such stores receive as share of profits on sale is nothing but an amount received in lieu of rent and therefore covered u/s 194I of the Act.

Next section deals with TDS on commission charged by Railway intermediaries on booking of tickets. It is seen that these intermediaries charge commission ranging from Rs. 25-40, on behalf of Railways and is shared with them, which is very clear from the agreement between Railways and intermediaries and therefore TDS provisions u/s 194H are applicable. Action in this regard has been taken in case of Central Railway by Mumbai TDS and action in case of Western Railways is being taken. The next section deals with the TDS on year end provisions, followed by TDS on Securitization trusts and Banking Correspondents which are latest and has huge TDS potential. In fact from securitization trusts TDS of over Rs. 1200 cr was moblised during 2018-19 and further amount of about Rs. 120 cr is being received on monthly basis in 2019-2020. Noncompliance of TDS provisions in respect of interest paid/ payable to group entities is discussed later. The last section deals with conclusions and recommendations.

Page Contents

- (A) Introduction to Emerging Issues in TDS

- (B) Interest Subvention Scheme in Real Estate Sector

- (C) TDS on E-Commerce Transaction

- (D) Multi Brand Retail –Sale on Return Basis Model

- (E) TDS on Service Charges Paid Paid to the Railway Intermediaries on Booking of Railway Tickets

- (F) TDS on Year End Provisions

- (G) TDS Surveys in Securitisation Trusts (Sansar Trust, Sriram Transport Company, Catalyst Trusteeship, IDBI Trusteeship)

- (H) Banking Correspondent Business and TDS non Compliance (Yes Bank, Paypoint, India Pvt Ltd and Nearby Technologies Pvt Ltd)

- (I) TDS Evaluation in Intra Group Interest Payments

- (J) Conclusions and Recommendations

(A) Introduction to Emerging Issues in TDS

TDS is one of the most important sources of revenue and being used world over in one form or the other to mobilize tax revenue. In India it contributes about 43% of direct taxes revenue as also significant proportion of indirect tax collections. As TDS is received by the Government on monthly basis, it is the most regular source of revenue unlike advance tax which is received in four installments. Therefore in recent years the Government has placed more and more reliance on such mode of tax collection which is very convenient and cost effective. TDS works on the concept of PAYE- pay as you earn. It requires that every person making specified type of payments to any person shall deduct tax at the rates prescribed in the Income Tax Act at source and deposit the same into the government’s account. The person who is making the payment is responsible for deducting the tax and depositing the same with government and is called a ‘deductor’ and who receives the payment is called ‘deductee’. The TDS mechanism is implemented by CPC-TDS, through TRACES. Form 26AS is a statement generated on processing of TDS satatement being filed quarterly by a deductor and shows the amount of tax deducted.

With expansion of economic landscape, globalization and integration of trade and commerce, specially with incidence of internet and digital economy, various new and emerging areas of TDS mobilization have come into play which have to be effectively tapped not only to mobilize taxes as also to increase the tax base. Some of these areas are discussed as under:

(B) Interest Subvention Scheme in Real Estate Sector

Interest subvention scheme is a new form of financing for home loans wherein an individual applies for a loan for a property under construction to a bank or a NBFC. As per the terms of scheme, the concerned person need not pay any interest or Pre- EMIs till a fixed period of time or till possession of apartment and such interest till the fixed period or up to possession is borne/paid by the developer/builder.

There are three parties in this arrangement namely; the buyer, the banker and the developer. The buyer books the property by paying 5-30% money upfront. The rest is paid by the bank or the NBFC in the form of loan to the buyer. The Bank/NBFC disburses the loan to the developer as construction progresses. All this is routine, but the most important aspect is that the developer bears the interest cost till possession or for a fixed period mentioned in the buyer- seller agreement. This arrangement is beneficial to both the customer as also the builder, as builder ends up getting funds/loan at a much lesser interest rate of about 8% to 9% while the customer need not pay interest for 3-4 years or till project gets completed. Many builders NBFCs are following this route in Mumbai as also at other places.

In this regard a TDS spot verification u/s 133B of the Income-tax Act, 1961 was conducted in the case of xxx Private Limited. It was noticed that this company is engaged in the interest subvention facilities/builder subvention facilities with certain NBFCs and banks. Subsequently information was sought from Indialbulls Housing Finance Limited (IHFL) and it was gathered that an amount of Rs. 12,37,926/- was paid by M/s xxx Private Limited to IHFL without making TDS. TDS liability on the same worked out to 1,23,792/- u/s 194A of the Act.

As this issue was of wider ramification, it was thought appropriate to call for information from prominent NBFCs regarding interest subvention with the concurrence of CCIT(TDS). Requisition letters u/s 133(6) were issued to following NBFCs on 04.07.2019

| Sr. No. | Name of the NBFCs |

| 1 | Indiabulls Housing Finance Limited |

| 2 | Sundaram Finance Limited |

| 3 | Reliance Commercial Finance Ltd. (Reliance Capital Company) |

| 4 | Piramal Capital & Housing Finance Ltd. |

| 5 | Tata Capital Ltd. |

| 6 | Diwan Housing Finance Ltd. |

As per information collected from these entities, 336 companies/entities all over the country which are covered under interest subvention scheme involving total interest amount of Rs. 250,14,70,739/-, the TDS liability on this amount worked out to Rs. 25,01,47,074/- and interest u/s 201(1A) of the Act would be extra.

As many of the entities are from outside Mumbai, information to the respective TDS offices may be forwarded to the respective TDS Offices so that action can be taken expeditiously so that benefit of proviso to section 201(1) can’t be claimed by the deductors. The remaining 110 companies are assessed in Mumbai. The information in respect of the 57 cases in respect of the CIT(TDS)-1, Mumbai is being passed on for immediate action. In entities in CIT(TDS)-2, Mumbai charge, notices u/s 201(1) of the Act have been issued and the order are being passed now. The process of centralization of cases with one officer is being initiated for coordinated action and collection of outstanding demand. The above action would result into TDS collection of Rs. 19 crores in Mumbai. Besides it’ll also result into penalty demand u/s 271C of equal amount.

In the next phase, some more information has been requisitioned from other entities like Edelvies & ILFS etc, thus increasing TDS impact. Infact total volume of real estate market is around 2,70,000 cr in India, out of which about 10%-15% is covered by interest subvention scheme. Thus total loan s under this scheme is estimated to somewhere around 30,000- 40000 cr. The possible quantum of interest may be about Rs. 2500-3000 cr on annual basis and for 3-4 years put together it may work out as handsome amount, TDS impact on which u/s 194A may work out to about Rs. 250- 300 cr.

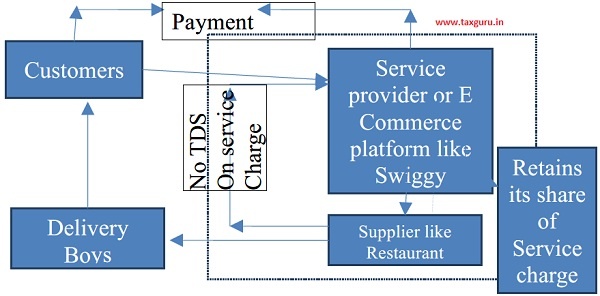

(C) TDS on E-Commerce Transaction

The e-commerce has transformed the way business is done in India and online market-platforms like Amazon, Flipkart, Zomato, Swiggy, Uber, Make- my-trip, Yatra Online,Paytm etc are on ascent. The Indian e-commerce market is expected to grow to US$ 200 billion by 2026 from US$ 38.5 billion as of 2017. Much growth of the industry has been triggered by increasing internet and smartphone penetration. India’s E-commerce revenue is expected to jump from US$ 39 billion in 2017 to US$ 120 billion in 2020, growing at an annual rate of 51 per cent, the highest in the world. It is seen that proper compliance of TDS provisions is not being made by these e-commerce platforms as it is not clear as to who should do TDS and on what amount.

TDS on payments made by E-commerce operators to actual suppliers.

The question is how to bring these E-Commerce transactions under the TDS? The existing provisions impose an obligation on the payer (subject to exclusions) to make TDS on the payments made to payee. In the E-commerce model, there may be difficulties to apply the existing TDS provisions on account of the fact that the E-Commerce operators are not the actual payers; it is the final customer who is the actual payer. These operators act as a facilitator between the actual buyers and the sellers.It is difficult for the payer (who is the end customer) to comply the TDS provisions on such transactions. Further the existing TDS provisions do not apply on the purchase of goods.

How to introduce TDS on above E-commerce model?

Considering the above difficulties, it may not be possible to introduce TDS on these transactions under the current set of TDS provisions. The possible way is by introducing a special provision to specify E-commerce operator as ‘deemed payer’ for the purpose of TDS compliances. Once, the E-commerce operator is considered as deemed payer, the provisions of TDS will come into play and the amounts being remitted by the E-Commerce operators to the actual suppliers can be subject to TDS.

Detailed discussions to that effect were held in 16th TDS Conference held at Jaipur recently wherein it was decided to constitute a study group to recommend guidelines on the subject. Since then this matter has been discussed in great length and discussions with some of the e-commerce platforms have also been held. These transactions essentially constitute payment of commission by prospective sellers to the e-commerce platforms, and delivery charges paid, to the delivery boys/entities etc which are hit by provisions of Section 194H and 194C respectively.

It is also seen that w.e.f. 2018, such transactions have been brought under GST provisions (sec. 52 of GST Act) and are subjected to 2% TDS on gross sales amount in respect to registered vendors having turnover of over Rs. 25 Lakhs.

Since this area has huge potential in terms of identifying new tax payers, as also mobilising the revenue from TDS, it is recommended that a new section 194P may be inserted in the Income-tax Act w.e.f. 1.4.2020 to bring such transactions under the ambit of TDS @ 1% which may be levied on gross sales amount, so that entire transaction amount is subjected to TDS. It is felt that the rate of 1% is very low and may not cause any grievance, either to the e-commerce platforms or to the vendors or the suppliers.

Responsibility to make TDS would be of the e-commerce platform. In fact by applying TDS @ 1% at the end of e-commerce platforms itself, the unnecessary hassles of making TDS by thousands of vendors/suppliers can be avoided and the department will have to deal with only very few entities. It is also proposed to keep a reasonable limit of turnover say Rs. 3 Lacs beyond which these provisions would be attracted so that very small people/vendors are excluded from such TDS.

It is therefore proposed that a new section 194P may be introduced as under:-

Section 194P:-

1. Notwithstanding anything contained in this Chapter, any e-commerce platform/ digital platform facilitating purchase/sale of any goods or services or booking of any rooms or shows or tickets or any such services will deduct TDS @ 1% of the gross amount of sales.

2. Provisions of sub-section (1) shall not be applicable if gross sales amount in respect of an entity during a year is less than Rs. 3 lacs.

3. Further, the seller of such goods or services through e-commerce platform or digital platform will not be required to make any further TDS on payment made/ retained by e-commerce platform in nature of commission or delivery charges etc.

4. Provision of sub-clause (3) will not be applicable to amount received by e-commerce platforms for hosting advertisements of anybody or providing any other services other than purchase/ sale of goods or services.

5. Explanation 1: An E-commerce platform/ digital platform includes;

i. Food delivery platforms like Ubereats, Swiggy, Zomato food panda or any such platform.

ii. Merchandising platform like Amazon, Flipkart etc.

iii. Ticketing platform like Make-my-trip, Yatra Online, go ibibo, Book my show or similar platform.

iv. Hotel booking platform like Trivago, Oyo rooms etc.

v. Transportation platforms like Uber, Ola, Meru etc.

vi. Any other similar platform, rendering such services in digital environment.

(D) Multi Brand Retail –Sale on Return Basis Model

It is seen that a lot of retail sales is made through Large Format Stores, more so in bigger towns like; Pantaloons, Shoppers Stop, Lifestyle, Westside, Central, Big Bazar etc. They essentially follow Sale or on Return Basis model where goods are purchased from the brand manufacturer only when sales happen in large format store (LFS). It saves lot of burden and risks at the end of such LFA, as they need not invest in inventory and whatever remains unsold it is returned to the brand owner. TDS survey was conducted on a multi Brand Retail Company ( xxx Stop Ltd) where in it was observed that in its showroom, various multi brands items were sold- clothes, shoes, watches, accessories, furniture etc. and agreements have been made by this Company with manufacturers of different brands/items to sell their items in its show room and profit margins are fixed. The retailer company is only providing space, security, and manpower to the manufacturer, whereas brands are providing their stalls, sales man, design of counter at its own cost. It was found that the items were sold at pre-fixed margin, which was shared between the large format store and the brand owner or manufacturer.

As the share of profit, the retailer is getting, is only for providing space and other services, therefore TDS provisions are attracted u/s 1941.

Alternatively the profit shred with the LFS is in nature of commission and is therefore attracts TDS u/s 194H.

Accordingly an order u/s 201 was passed in this case raising a demand of Rs.114 cr, out of which an amount of Rs. 10 cr was collected and balance in monthly installments. Thereafter action has been taken in other such cases by TDS Mumbai and other charges and in many cases such stores have accepted departmental stand.

This issue however has huge TDS potential, as the retail sales have volume of about Rs. 2,00,00,000/- in India and lot of such stores have come up all over the country. The possible TDS impact of this issue is estimated to be about Rs. 500 cr.

(E) TDS on Service Charges Paid Paid to the Railway Intermediaries on Booking of Railway Tickets

Railway ticketing revenue is about Rs. 50000 Crores annually, significant portion of which is done by the Railway Intermediaries who charge small sum ranging from Rs. 2 to Rs. 40/- per ticket as service charges. This revenue is shared between Railway and Intermediaries in the ratio of 25%: 75%. Even though the collections are made by such service providers but in effect the service charges are collected on behalf of Railway and shared between both, therefore, the amount retained by the Service providers (intermediaries) is deemed to be the commission paid by the Railways, thus, TDS provisions are applicable u/s 194H on such amount received/ retained by the intermediaries. Two of such intermediaries are Yatri Ticket Suvidha Kendra (YTSK) and Jan Sadharan Ticket Booking Seva (JTBS).

It is seen from the scheme floated by Railways for establishment and operation of Yatri Ticket Suvidha Kendra (YTSK) and agreement entered into between Railways and such service providers that:

i. YTSKs are working as agents of Railway.

ii. YTSKs are liable to follow terms & conditions prescribed by the Railway.

iii. YTSKs will collect service charges (commission) from passenger as decided by the Railways.

iv. 25% of the service charges collected by the licensee from the passengers shall be credited to Railway account at the time of booking/cancellation of reserved tickets

Similarly, it is seen from the copy of Jan Sadharan Ticket Booking Seva (JTBS) agreement provided by the Central Railway that:

i. The JTBS shall deemed to be the agent of the Railway Administration and shall be subject to all the legal liabilities of agents.

ii. The appointment is purely contractual in nature.

iii. JTBS will collect service charges (commission) from passenger as decided by the Railways. The commission will be retained by the JTBS.

From the above, it is quite evident that there is Principal-agent relationship between Railways and intermediaries. Thus, any commission earned by the agent on account of agency of YTSKs/JTBS is only because of such Principal-agent relationship. The passenger is paying the extra amount to YTSK/JTBS only on account of them being agent of Railway. The commission receipt is also issued by the Railway by mentioning the commission amount on the ticket. Even if such commission is not remitted by the YTSK/JTBS but retained with them does not affect the TDS liability, which would squarely fall on Railways.

Deduction of tax is also applicable in a situation where commission or brokerage is retained by the agent and not remitted to the principal, as the retention of the said personnel amounts to constructive payment of the same to him by the consignee or principal. In such a case, deduction of tax at source is required to be made from the amount of commission. Therefore, the consignor/ principal must deposit the tax deductible on the amount of commission income to the credit of Central Government within the prescribed time.

As per information gathered from Central Railways in respect of service charges collected by intermediaries, an amount of Rs. 21,43,54,138/- was charged as service charges in FY 2015-16 to FY 2017-18,out of which Rs. 20,19,91,580/- was retained by the service providers and balance Rs. 1,23,62,558/- was Railway’s share. Since TDS was not deducted on the amount retained by the service providers, action u/s 201(1)/201(1A) of the Income-tax Act, 1961 is under progress. It is also to mention that in FY 2017-18, the commission charged by the JTBS was Rs. 1 per ticket (total amount Rs. 6,33,80,834/-) whereas from 01.09.2018, the Railways has revised the commission charges to Rs. 2/-. The proceedings u/s 201(1) has been completed in the case of Central railway where TDS liability of Rs. 1.8 crores is raised on this account for three years.

The information in respect of Western Railway is still awaited and is being collected. The liability in their respect will be much more. After we conclude the proceedings in respect of Western Railway, the information in respect of other Zones of Railway will be forwarded to jurisdictional charges.

This issue has huge Revenue potential and action u/s 201(1)/201(1A) of the Income-tax Act, 1961 has to be taken against all Zonal Offices of the Railways. In fact such action is warranted in respect of intermediaries for railway freight services as well, which is much larger than ticketing.

(F) TDS on Year End Provisions

Year end provisions as on 31st March and disallowance u/s 40 a (ia) and TDS compliance thereon is one of the important issues detected on account of surveys carried out in several cases at Mumbai.It has been found that some companies make provision of expenses as on 31st March. 30% of this expenditure is disallowed and added back u/s 40 a (ia), thus 70% of the expenses is claimed without making TDS.

It has been found that the parties in respect of which these provisions are made are identifiable and even amounts are certain. Therefore there appears to be a very big racket and results into deferment of TDS as the expenditure is booked in next year and legitimate TDS is delayed by several months. To plug this practice, actions u/s 201 have been taken in several cases raising demand in several hundred crores, a portion of which has been collected also.

In the month of March, 2019 a request was therefore made to DGIT (Systems) to generate a list of such cases at all India level and disseminate information among CIT-TDS charges, which has since been done and huge demand is likely to arise on this account all over the country. In the current year again a request is being made to DGIT (Systems) to generate similar information.

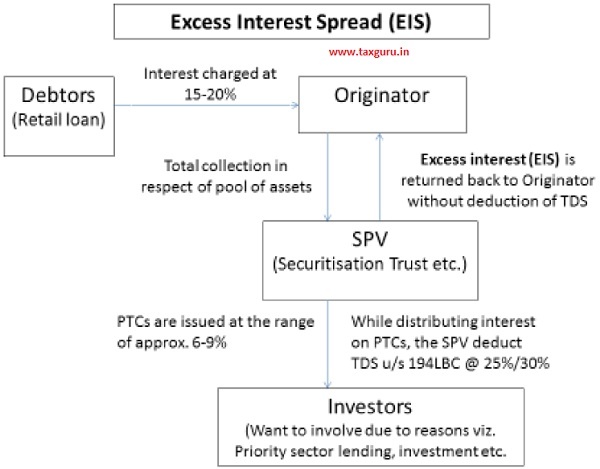

(G) TDS Surveys in Securitisation Trusts (Sansar Trust, Sriram Transport Company, Catalyst Trusteeship, IDBI Trusteeship)

A TDS survey was carried out in case of a NBFC (Sriram Transport Finance co ), which lends out Vehicle loan to various customers at the agreed terms and conditions of rate of interest and EMI’s. Once loan portfolio reached around 700.00 crores, it approached one Investor normally a bank. This bank creates a ‘Securitisation Trust” to provide funds to the NBFC. Then Trust entered an assignment agreement with NBFC and took over the pool of lent out money to various borrowers of NBFC. In lieu of assignment of assets of the NBFC, Trust made upfront payment of Principal amount of loan disbursed by NBFC to it. It was found that this NBFC created Sansar Trust for such purposes which was backed by IDBI bank and management was handed over to IDBI Trusteeship company.

As per the details gathered, there were 2455 such trusts mostly located in Mumbai, out of which 1784 were in nature of ARCs (asset reconstruction companies) and remaining 671 were securitization trusts. All these trusts have been covered under this exercise. These trusts had made payments EIS of Rs. 5505 cr without making TDS for fin. yrs 2016- 17 to 2018-19( till December 2018). Total TDS liability for the current year was Rs. 784 cr which has been collected fully. Further liability till March 2019 worked out to Rs 185 cr, which has also been paid. Besides orders u/s 201 were framed in respect of previous years namely F.Y 2016-17 and 2017-18 in cases of these trusts, where TDS liability of Rs. 310 cr was raised. Thus the details are tabulated as under:

(Rs. In Crores)

| Total no of trusts | 2455 |

| No of securitization Trus | 671 |

| Asset Reconstruction Trusts* | 1784 |

| Surveys conducted | 18 |

| No of entities covered | 671 |

| Amount of EIS paid on which TDS was not done | |

| From F Y 2016-17 onwards | 5505 |

| TDS liability thereon @30% | 1651 |

| Amount of EIS paid for the current year (2018- 19 till December 18) | 2614 |

| TDS liability u/s 194LBC @30% for current year | 784 |

| TDS liability for the month of Jan 19 to March 19 | 246 |

| TDS collected so far in 2018-19 | 1030 |

| Tentative TDS liability for earlier years (2016-17, 2017-18) | 621 |

| Demand raised u/s 201 so far for earlier years | 310 |

The total revenue collected through this is Rs. 1030 cr so far. Besides demand of Rs. 310 cr has been raised u/s 201 cr in respect of earlier years (2016-17 and 2017-18 ) and some more is expected to be raised, against which further payments are expected in due course. So the total impact of this exercise is over Rs. 1651 cr.

Ramification of this finding is huge and may have impact on the other cases of Securitisation Trusts and Asset Management Companies. Private Equity firms, all over the country, for which further action is in pipe line. This finding was shared in the 15th TDS conference held in Chennai and was widely appreciated.

(H) Banking Correspondent Business and TDS non Compliance (Yes Bank, Paypoint, India Pvt Ltd and Nearby Technologies Pvt Ltd)

For the purpose of achieving financial inclusion, Reserve Bank of India permitted banking institutions to appoint business correspondents (BCs) who can act as on behalf of the bank in rural areas for providing banking services. BCs who has technical platform and industry expertise in turn appoints distributors and agents for actually providing banking services for end customers. In this arrangement, RBI has permitted only banks to charge service fee on the customers. BCs are expressly prohibited from charging service fee on customers as per the clause 9 of circular dated 28-09-2010. This prohibition is to protect the customers from over charging by BCs. Bank is considered as principal always in this type of business arrangements.

In this process, a survey was carried out in case of Yes Bank and Paypoint India Pvt Ltd and Nearby Technologies Pvt Ltd. Subsequently orders u/s 201 waere passed raising a demand of Rs. 20.54 cr was raised, out of which an amount of Rs. 6 cr has ben collected. Further, volume of the transactions involved is very high as some BCs even manage around Rs. 150000 crores annually and service fee involved for one BC alone was Rs.225 crores. Relevant information about this is being shared with other charges.

In addition to TDS violations, some more issues are noticed in these cases. Service fee retained by agents especially in cash is not reported as income in their hands. BCs and banks also under- report their revenues by not including gross service fee as their income.

It is to be noted that banks and BCs stopped following changed model after TDS survey operations in October 2018 and shifted to the old system and started deducting TDS. This itself show that banks and BCs accepted their mistake of following the illegal arrangement.

The TDS potential of this issue is very large as almost all banks are following this model of business and may be followed by respective TDS charges.

(I) TDS Evaluation in Intra Group Interest Payments

It has been noticed that TDS compliance is not properly made on interest payment in intra group companies in big groups. In the case of xxx Realty Pvt. Ltd., it was found that TDS on interest expense for F.Y. 2018-19, was neither made nor paid. The total of interest payment was Rs. 2360 cr, TDS on which worked out to Rs. 236 cr and along with interest it worked out to Rs. 250 cr. Similar situation was found in another group in which TDS was not made on interest payment of over Rs. 400 cr to the group concerns. Both the groups were trying to take advantage of proviso to section 201 which exempts the payer from liability in case recipient has discharged the tax liability. However such game plan was disturbed by TDS officer by passing order u/s 201 before the due date for filing return and therefore the assesse now cannot take the advantage of this proviso. It is suspected that this methodology may be followed by very many other group entities with a view to dodge legitimate TDS payments.

(J) Conclusions and Recommendations

The government uses TDS as a tool to collect tax in order to minimize tax evasion by taxing the income at the time it is generated rather than at a later date. However TDS is not applicable to all incomes and persons for all transactions. Different rates of TDS have been prescribed by the Income Tax Act for different types of payments and different categories of receipts, which has to be followed meticulously by the payer, lest he may be in trouble. The law mandates not only for deduction of tax but also its payment within prescribed time limit, failing which there are penal and prosecution provisions, besides levy of late payment interest which is quite huge. So many persons have been recently convicted by the courts all over the country for non payment of TDS in government account. It is therefore advisable that TDS provisions are followed in letter and spirit to avoid unnecessary hassles at a later stage.

The areas discussed in foregoing paras are new and emerging and therefore requires a lot of application at the end of TDS officers. The issues like E Commerce has taken everything by storm and considering the dynamic situation, it is very difficult to tax such transactions. TDS however could be a very effective tool not only to tax such transactions but to establish a trail which may result into new tax payers. To simplify the entire process it is suggested that TDS may be done at the end of e-portal itself which is easy to understand and implement and easy to comply and the department has to deal with only a very few deductors as against thousands of end suppliers. This would require concerted efforts at the end of tax department to educate tax payers. Therefore conducting outreach programmes and tax awareness about them is not only desirable but necessary. As some government department like Railways and Banks are involved therefore it is desirable that they are sensitized towards their role and compliance issues.

Securitiation Trust and TDS implication on Excess Interest Spread is a very new area and has resulted into a lot of TDS in Mumbai region. Such other transactions like Mutual Fund distribution fees and interest/dividend in venture capital funds and alternate funds may be tapped for TDS. Interest Subvention, banking correspondent business, multi brand retail throws a host of issues relating to TDS which have to be effectively implemented and administered.

It is also suggested that there should be better coordination among various tax administrations specially Income Tax and GST, as similar kind of issues are addressed by both the departments specially in respect of services rendered and TDS issues there on. Data of lease and rental incomes etc. may also be shared between both the departments for better tax coverage.

An excellent write up on TDS.

Good article but I am really worried that people in Revenue try to split hairs and tax the taxed; for example after having paid GST why should the poor agent be taxed under 194H. No. of people who come to him are also not many; instead it is better to concentrate on Corporate who have a team of auditors to manipulate or save tax. I feel that the Revenue needs to concentrate on HIG and leave the poor alone

Dear Sri Pratap Singh ji

Congratulations for a detailed research paper on TDS. We do hope, public at large and readers are well benefited.

Best

Pani