Case Law Details

Vasamsetty Veera Venkata Satyanarayana Vs ITO (ITAT Hyderabad)

Conclusion: Assessees could not claim cost of improvement and indexation cost as assessee had to furnish some evidence and in the absence of any evidence or information, the information contained in the registered sale deed was required to be accepted.

Held: Assessee was an individual and derived income from business, long term capital gain and from other sources. Assessee had filed his return of income for the AY 2016-17 on 24.03.2018 declaring income of Rs. 8,26,153/-. A search and seizure operation u/s.132 was conducted on the assessee as part of the searches conducted on M/s. Skill Promoters Pvt. Ltd. Group and others on 22.10.2019. Accordingly, notice u/s. 153C was issued to the assessee. In response to the notice, assessee had not filed any return of income. However, assessee filed return of income on 24.03.2018 for the A.Y. 2016-17. Subsequently, notices u/s. 142(1) was issued to assessee by AO. Thereafter, AO had completed the assessment u/s. 153C inter alia by making addition of Rs.1,30,01,435/- on account of Long Term Capital Gains. Revenue, submitted that on the basis of the registered sale deed, assessee had claimed long term capital gain and indexation cost whereas in the agreement of sale dated 21.11.2015 the property had been shown as vacant plot of land. Hence considering the above assessee had wrongly claimed long term capital gain as well as indexation cost. Assessee filed appeal before CIT(A), who granted partial relief to assessee. It was held that to claim the cost of improvement and indexation cost, assessee had to furnish some evidence and in the absence of any evidence or information, then the information contained in the registered sale deed was required to be accepted. Therefore, the information contained in the registered sale deed related to the assessee and AO had rightly invoked the jurisdiction under section 153C.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

The captioned appeals are filed by the assessee, feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals) – 12, Hyderabad dt.28.09.2022 for A.Y. 2016-17.

2. The grounds raised by the assessee in ITA No.706/Hyd/2022 for A.Y. 2016-17 read as under :

“1. For that the Order of the Learned Commissioner of Income Tax (Appeals) is contrary to law, facts and circumstances of the case.

2. For that the Learned Commissioner of Income Tax (Appeals) has erred in upholding the Order u/s 153C r.w.s 144 of the Act in the absence of any incriminating material pertaining to the Appellant found from the persons searched.

3. For that the Learned Commissioner of Income Tax (Appeals) erred in denying the benefit of indexation on cost of improvement incurred during FY 2004-05 amounting to Rs.37,77,148/- having directed the Assessing Officer to allow the claim of cost of improvement on account of compound wall, parking area, drying platforms, roads, leveling and soil dumping workings amounting to Rs.16,17,779/-.

3. Similar grounds were raised by the assessee in other appeal also i.e., ITA 707/Hyd/2022 for A.Y. 2017-18 except the amounts involved in.

4. Before us, at the outset, both the parties submitted that the issues raised in both the appeals were identical. In view of the aforesaid submissions, we, for the sake of convenience proceed to dispose of both the captioned appeals by a consolidated order but however refer to the facts in ITA No.706/Hyd/2022 for A.Y. 2016-17.

5. The brief facts of the case are that assessee is an individual and derives income from business, long term capital gain and from other sources. The assessee had filed his return of income for the AY 2016-17 on 24.03.2018 declaring income of Rs. 8,26,153/-. A search and seizure operation u/s.132 was conducted on the assessee as part of the searches conducted on M/s. Skill Promoters Pvt. Ltd. Group and others on 22.10.2019. Accordingly, notice u/s. 153C was issued to the assessee. In response to the notice, the assessee had not filed any return of income. However, the assessee filed return of income on 24.03.2018 for the A.Y. 2016-17. Subsequently, notices u/s. 142(1) was issued to the assessee by the AO. Thereafter, Assessing Officer had completed the assessment u/s. 153C of the I.T. Act, interalia by making addition of Rs.1,30,01,435/- on account of Long Term Capital Gains.

6. Feeling aggrieved by the order passed by the assessing officer, assessee filed appeal before the Ld. CIT(A), who granted partial relief to the assessee.

7. Feeling aggrieved with the order of ld.CIT(A), assessee is now in appeal before us.

8. Ground No.1 is general in nature and requires no adjudication. Ground No.2 is with respect to upholding the order of Assessing Officer u/s 153C r.w.s. 144 of the Act by the ld.CIT(A) and Ground No.3 is with respect to the addition of Rs.33,65,988/- confirmed by the ld.CIT(A).

Ground No.2

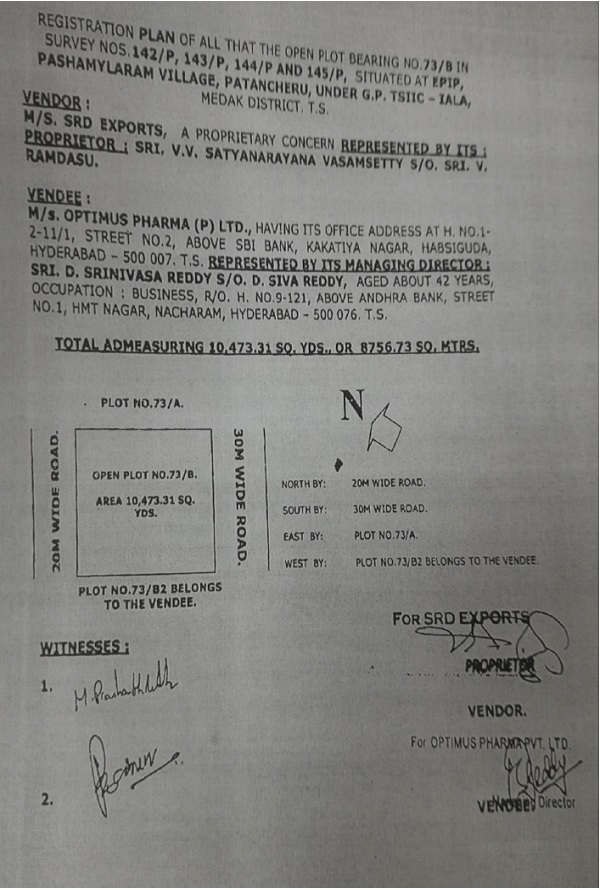

9. Before us, ld. AR has submitted that the registered sale deed executed between M/s. SRD Exports, a proprietary concern represented by its Proprietor Sri VV. Satyanarayana Vasamsetty and M/s. Optimus Pharma Pvt. Ltd. represented by its Managing Director Sri D. Srinivasa Reddy for the shed on open plot admeasuring 142/P, 143/P and 145/P admeasuring 10,008 sq.yards situated at EPIP Pashamylaram Village, Patancheru dt.21.11.2015 for an amount of Rs.1,58,22,000/-was not an incriminating document pertaining to the assessee and therefore, cannot form basis of the addition u/s 153C of the Act. It was submitted that the registered sale deed though recovered from the residential premises of searched person cannot be said to be an incriminating document, per se as the said registered sale deed was available in public domain and therefore, cannot be said to be an incriminating document. Further, it was submitted that the said document does not pertain to the assessee as it pertains to the searched person namely, M/s. Optimus Pharma Pvt. Ltd and therefore, cannot be relied upon by the Assessing Officer to make an addition. In reply to the above said submission, the ld.AR relied upon the following decisions :

|

Sl.No. |

Case Law |

| 1 | PCIT Vs. Meeta Gutgutia – (2017) 82 taxmann.com 287 (Delhi) dt.25.05.2017 |

| 2 | PCIT Vs. Meeta Gutgutia – (2018) 96 taxmann.com 468 (SC) dt.02.07.2018 |

| 3 | CIT Vs. Arpit Land P. Ltd. – (2017) 78 taxmann.com 300 (Bombay High Court) |

| 4 | CIT Vs. IBC Knowledge Park Pvt. Ltd. – (2016) 69 taxmann.com 108 (Karnataka High Court) |

| 5 | Yellaiah Setty Vs. ACIT, Hyderabad – ITA No.494/Hyd/2017 dt.15.11.2018 |

10. On the other hand, the ld.DR submitted that the search and seizure operation was conducted on 22.10.2019 in the residential premises of Sri D.Srinivasa Reddy, wherein material during the course of search from the residential premises of said D. Srinivasa Reddy relates to M/s. SRD Exports, for which, the assessee is the Proprietor were seized. It was submitted that in the registered sale deed, the name of the assessee was duly mentioned, and it was submitted that on the basis of the registered sale deed, the assessee had claimed long term capital gain and indexation cost whereas in the agreement of sale dt 21.11.2015 the property has been shown as vacant plot of land. It was further submitted that as in the registered sale deed, no construction was shown rather the property was shown as a vacant piece of land and therefore, the said sale deed though registered was rightly held. Ld. DR further submitted that the assessee had wrongly claimed long term capital gain as well as indexation cost. It was further submitted that the document relates to the assessee and therefore, the lower authorities had relied upon this document for the purpose of deciding the issue against the assessee.

11. We have heard the rival submissions and perused the material on record, including the registered sale deed and section 153C of the Act. Bare reading of section 153C of the Act provides as under :

153C. 72[(1)] 73[Notwithstanding anything contained in section 139, section 147, section 148, section 149, section 151 and section 153, where the Assessing Officer is satisfied that,—

(a) any money, bullion, jewellery or other valuable article or thing, seized or requisitioned, 74belongs to; or

(b) any books of account or documents, seized or requisitioned, pertains or pertain to, or any information contained therein, relates to, a person other than the person referred to in section 153A, then, the books of account or documents or assets, seized or requisitioned shall be handed over to the Assessing Officer having jurisdiction over such other person] 75[and that Assessing Officer shall proceed against each such other person and issue notice and assess or reassess the income of the other person in accordance with the provisions of section 153A, if, that Assessing Officer is satisfied that the books of account or documents or assets seized or requisitioned have a bearing on the determination of the total income of such other person

76[for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made and] for the relevant assessment year or years referred to in sub-section (1) of section 153A] :]

77[Provided that in case of such other person, the reference to th e date of initiation of the search under section 132 or making of requisition under section 132A in the second proviso to 78[sub-section (1) of] section 153A shall be construed as reference to the date of receiving the books of account or documents or assets seized or requisitioned by the Assessing Officer having jurisdiction over such other person :]

79[Provided further that the Central Government may by rules80 made by it and published in the Official Gazette, specify the class or classes of cases in respect of such other person, in which the Assessing Officer shall not be required to issue notice for assessing or reassessing the total income for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made 81[and for the relevant assessment year or years as referred to in sub-section (1) of section 153A] except in cases where any assessment or reassessment has abated.] 82[(2) Where books of account or documents or assets seized or requisitioned as referred to in sub-section (1) has or have been received by the Assessing Officer having jurisdiction over such other person after the due date for furnishing the return of income for the assessment year relevant to the previous year in which search is conducted under section 132 or requisition is made under section 132A and in respect of such assessment year—

(a) no return of income has been furnished by such other person and no notice under sub-section (1) of section 142 has been issued to him, or

(b) a return of income has been furnished by such other person but no notice under sub-section (2) of section 143 has been served and limitation of serving the notice under sub-section (2) of section 143 has expired, or

(c) assessment or reassessment, if any, has been made, before the date of receiving the books of account or documents or assets seized or requisitioned by the Assessing Officer having jurisdiction over such other person, such Assessing Officer shall issue the notice and assess or reassess total income of such other person of such assessment year in the manner provided in section 153A.]

83[(3) Nothing contained in this section shall apply in relation to a search initiated under section 132 or books of account, other documents or any assets requisitioned under section 132A on or after the 1st day of April, 2021.]

12. From the reading of the above said provision, it is abundantly clear that section 153C(b), clearly mentioning that any book of account or documents seized or requisition pertain to any information contained therein relates to the assessee. Now the question which is required to be considered is whether the information contained in the registered sale deed relates to the assessee or not ? In the present case, admittedly, in the agreement of sale as per the schedule annexed to that sale deed, the property has been shown as vacant piece of land and the same is clear from pages 22 and 27 of the paper book which is to the following effect :

13. From the cursory look of both the maps annexed with the two sale deeds, which are the subject matter of the proceedings, it is clear that what has been sold by the assessee were merely piece of an open lands and not any constructed property. The assessee in the return of income had claimed the long term capital gain and in the said capital gain, the assessee had claimed the cost of acquisition and cost of improvement with indexation. In our view, the cost of improvement, is required to prove with contemporaneous evidence showing that some construction or improvements were carried out on the plot of land after its original purchase in the year 2004, and before it was sold by the assessee on 21.11.2015. The information contained in the sale deed (including the site plan) clearly shows that what has been sold by the assessee was a vacant piece of plot and not a built up property. To claim the cost of improvement and indexation cost, assessee has to furnish some evidence and in the absence of any evidence or information, then the information contained in the registered sale deed is required to be accepted. Further, the information contained in the registered sale deed relates to the assessee and therefore, we are of the opinion that the Assessing Officer was right in invoking the jurisdiction u/s 153C of the Act and therefore, there is no ground for interference by us with the order of ld.CIT(A) and accordingly, the ground no.2 is dismissed.

Ground No.3

14. With respect to ground No.3, ld. AR had submitted that the ld.CIT(A) was erred in denying the claim of assessee. Ld. AR further submitted that evidence in the form of photographs were provided to the Assessing Officer as well as ld.CIT(A) which show that the improvement was carried out at the residential premises of the assessee. Further, the assessee drew our attention to the certificate issued by the Architect in the year 2015 during the proceedings before the ld.CIT(A) substantiating that the construction was carried out in the premises.

15. Per contra, ld. DR had submitted that the ld.CIT(A) had granted more relief than the assessee deserves. It was submitted that the site plans annexed to sale deed clearly show that there was no construction in the property at the time of transferring property to M/s. Optimus Pharma Pvt. Ltd and once the open plot has been transferred by the assessee then there is no scope of improvement and further, there is no scope of granting the indexation cost on such improvements. It was further submitted that during the course of assessment proceedings, the assessee has not filed any documents for claiming the indexation cost and our attention was drawn to paras 10 to 12 of the assessment order which is the following effect :

“10. The assessee has not filed the return in response to this office notice issued under section 153C of the I.T. Act. However, the assessee filed a return of income on 24.03.2018 for the assessment year 2016-17 wherein capital gains of Rs.6,18,202 are disclosed in the schedule CG of the return as under :

|

Full value of consideration |

Rs.1,58,22,000 |

| Less: Cost of acquisition with indexation | Rs.20,66,447 |

| Less : Cost of Improvement with indexation | Rs.1,31,37,351 |

| Long term capital gains on the property | Rs.6,18,202 |

11. As seen from the above, the assessee declared long term capital gains after reducing the indexed cost of acquisition and indexed cost of improvement. On a perusal of the working of capital gains furnished by the assessee, it is observed that no basis is given for arriving at the cost of improvement with requisite details like year of commencement / completion of construction if any on land which was transferred during the year under consideration and expenditure stated to be incurred thereon, extent of construction along with necessary documentary evidences, so as to verify the claim of long term capital gains shown in the return of income. Therefore, as there was no concrete evidence is submitted by the assessee with respect to the claim of expenditure towards improvements on land, the same is not considered.

12.Further, as per the assessee’s calculation the taxable capital gains submitted at Rs.4,19,503 as against Rs.6,18,202 declared in the return. Thus, there is inconsistency in the claim of capital gains as per the return of income vis a vis the information furnished during the course of assessment proceedings. The assessee was also specifically requested to furnish a detailed working for the computation of long term capital gains with all necessary evidences and explain the discrepancy as stated above in this office show cause notice dt.17.12.2019. As the assessee has not furnished correct computation, not reconciled the discrepancy, and in the absence of requisite particulars for computation of capital gains, there is no option except to compute the capital gain as per the information gathered from TSIIC, Hyderabad, and as available form the records.

16. Further, the ld. DR had drawn our attention to para 6.7.1 of the order passed by the ld.CIT(A) wherein the above issue has been examined by the ld.CIT(A).

Discussion & Decision

6.7.1 I have considered the submissions of the AR and the order of the AO. It is seen that the appellant has sold land admeasuring 8368.60 sq. meters along with Shed to M/s. Optimus Pharma (P) Ltd. vide sale deed No. 20907/115 dated 21.11.2015 for a consideration of Rs.1,58,22,000/-. The appellant claimed cost of improvement of Rs.139.66 lakhs and submitted a certificate dated 19.02.2015 from an approved Civil Engineer & valuer to substantiate its claim. Photographic evidence of the construction was also provided. It is also a fact that the existence of construction and shed was mentioned in the sale deed itself. Under these circumstances, not giving any benefit towards cost of construction is the assessment order is not proper. In the remand report, AO has not given any adverse findings. In order to calculate the cost of improvement, the certificated by the AR from the valuer and the sale deed No.20907/115 were perused. On perusal of the valuer’s certificate, it is seen that the appellant is said to have incurred expenditure of Rs.90,59,538/- on construction of sheds, Rs.14,58,000/- on compound wall and gate, Rs.1,26,500/- on parking area, Rs.3,11,750/- on drying platforms, Rs.7,64,400/- on roads and Rs.6,50,000/- on leveling and soil dumping works, Rs.58,800/- on security room, Rs.5,28,528/- on building, Rs.9,85,950/- on platforms and Rs.23,328/- on sump towards cost of improvement. Out of the above, the appellant claimed expenditure of Rs.81,53,584/- (90% of Rs.90,59,538/-) on construction of sheds during the year and the balance Rs.9,05,954/-in the next year i.e., AY 2017-18 when he had sold the remaining portion. On account of compound wall, parking area, drying platforms, roads, leveling and soil dumping works appellant incurred total cost of Rs.33,10,650/- but claimed Rs.16,17,779/- in the current year based an the share of land sold during the year. On this amount of Rs.16,17,779/-, appellant claimed indexation benefit and the indexed cost as per the AR worked out to Rs.37,77,148/-. However, there is no proof produced by the AR to support his contention that appellant has incurred these development expenses in the FY 2004-05 and is therefore eligible for indexation. In the absence of supporting evidence, the indexation benefit claimed by the appellant is denied. Further, the appellant fairly submitted that land cost of Rs.13,10,594/- was inadvertently included in the cost of construction. Hence this amount is reduced from the claim of cost of construction. To sum up, appellant is allowed cost of improvement of Rs.16,77,779/- and Rs.81,53,584/- towards share of shed in land sold totaling to Rs.97,71,363/- as against the claim of Rs.1,31,37,351/-. Accordingly, AO is directed to allow cost of construction / improvement of Rs.97,71,363/- and appellant gets relief to that extent. The remaining disallowance of Rs.33,65,988/- (Rs.1,31,37,351/- – Rs.97,71,363/-) is confirmed. The appeal of the appellant on this issue is PARTLY ALLOWED.”

17. We have heard the rival submissions and perused the material on record. Admittedly, the assessee had sold the land admeasuring 10,008.58 sq.yards vide sale deed bearing no.20907/2015 on 21.11.2015 for consideration of Rs.1,58,22,000/- Against the said sale consideration, the assessee had claimed cost of improvement for a sum of Rs. 16,77,779/- and also submitted a Certificate from the approved Civil Engineer along with photographs. Admittedly, the assessee has not produced any evidence towards the development expenses in the previous year and ld.CIT(A) had disallowed an amount of Rs.33,65,988/-.

18. In our view, it is essential for the assessee to prove that there were improvements made in the plots by the assessee prior to the execution of the sale deed. If we compare the site plans annexed to agreement for sale 03.11.2004 and the sale deed dt.21.11.2015, then it is clear that both the site plans are similar to each other except in the plan annexed to the sale deed dt.21.11.2015 wherein the total built up area was mentioned as 1155.90 Sq.Fts. Admittedly, the ld.CIT(A) had granted the improvement cost to the assessee at the appellate stage at Rs.41,70,153/- However, the remaining amount of Rs.87,00,973/- was confirmed by the ld.CIT(A). In our view, whenever a question arise as to the amount of construction / its extent arises in respect of a property, which is transferred by way of registered document, then for that purposes, the extent of construction mentioned in the sale document and plan annexed thereto as per Transfer Property Act would be determinative in nature. In the first sale deed dt.21.11.2015, the Schedule of the Property and description of the property at pages 19 and 20, it was mentioned as under :

SCHEDULE OF THE PROPERTY

All that the Shed constructed on open plot bearing No.73/B/Part in Survey Nos.142/P, 143/P, 144/P and 145/P, total admeasuring 10,008.58 Sq.Yds., with built-up area of 1155.90 Sq.Ft., roof covered with RCC, as shown in the plan annexed herewith situated at EPIP, PASHAMYLARAM VILLAGE, PATANCHERU, UNDER G.P. TSIIC – IALA, MEDAK DISTRICT T.S., MP PATANCHERU, Z.P. Medak at Sangareddy, Registration Sub-District Sangareddy, Registration District Medak at Sangareddy and bounded by :

NORTH BY : 25’ WIDE ROAD

SOUTH BY : 30’ WIDE ROAD

EAST BY : REMAINING OPEN PLOT

NO.73/B/PART.

WEST BY : 100’ WIDE ROAD.

ANNEXURE 1A

|

01. Description of the Building |

All that Shed constructed on open plot bearing No.73/B/Part in survey Nos. 142/P, 143/P, 144/P and 145/P, situated at EPIP, PASHAMYLARAM VILLAGE, PATANCHERU, UNDER G.P. TSIIC – IALA, MEDAK DISTRICT T.S., |

20. Similarly, in respect of second sale deed dt.13.04.2016, the extent of construction mentioned in the Schedule of the Property placed at page 25 reads as under :

SCHEDULE OF THE PROPERTY

All that the open plot bearing No.73/B/ in Survey Nos.142/P, 143/P, 144/P and 145/P, total admeasuring 10,473.31 Sq.Yds., or 8756.73 Sq.Ft., as shown in the plan annexed herewith situated at EPIP, PASHAMYLARAM VILLAGE, PATANCHERU, UNDER G.P. TSIIC – IALA, MEDAK DISTRICT T.S., MP PATANCHERU, Z.P. Medak at Sangareddy, Registration Sub-District Sangareddy, Registration District Medak at Sangareddy and bounded as follows :

NORTH BY : 25’ WIDE ROAD

SOUTH BY : 30’ WIDE ROAD

EAST BY : PLOT No.73/A

WEST BY : PLOT NO.73/B2

BELONGS TO THE VENDEE

21. From the reading of the description of built up area referred in above noted sale deed, it is crystal clear that no construction activity has been mentioned in the first sale deed executed on 21.11.2015 except a small shed of 1155.90 sq.yards covered with RCC as against total area of plot admeasuring 10,008.58 sq. yards.

21.1. In our view, whatever relief can be granted to the assessee was with respect to the small shed of 1155.90 sq.yards and on which the assessee was eligible for improvement cost and indexation cost. However, the assessee is not entitled either the cost of improvement or indexation for the remaining area, as when there was no construction, then there was no occasion for grant of any improvement cost or indexation thereto. In our view, the ld.CIT(A) has granted more relief than what the assessee deserves. Similarly, in the other sale deed dt.13.04.2016, there was no construction whatsoever mentioned in the sale document. The registered document namely, sale deed once suggests and mentions no construction in the plot, there is no occasion to consider the construction in the plot and granting costs of improvement and indexation thereto does not arise.

22. Ld.AR had relied upon the certificate issued by the Civil Engineer to prove the improvement made in the property, the said certificate is in contradiction to contents of the registered sale deed, hence same cannot be accepted , as a cogent evidence to prove the improvement in the property. As per the Indian Evidence Act, the contents mentioned in the registered sale deed will have precedence over the certificate issued by the Civil Engineer certifying the extent of construction in the property. There was no reason for the assessee to mention the incorrect extent of construction in the sale document, by virtue of which the assessee had transferred the land and the building if any existing thereon. In view of the above, we do not find any discrepancy in the decision of ld.CIT(A). We may point out that the law of evidence clearly provides that when there is any infirmity between the documents filed by the parties, the contents of the registered document will prevail over the other document. The assessee had failed to demonstrate by any evidence the cost of improvement like bills / vouchers, approval of the local authorities and claim of expenditure claimed in the earlier return of incomes. In view of the above, the assessee is not entitled to the relief claimed in these appeals. Even the case laws relied upon by the assessee are of no help as the facts of those cases are clearly distinguishable. Admittedly, none of the decisions cited supra dealt with the issue of appreciation of evidence of registered sale deed and claim of the cost of improvement and indexation based on the certificate issued by the Civil Engineer. Thus, ground No.3 of the assessee is also dismissed. Accordingly, the appeal of the assessee is dismissed.

23. In the result, the appeal of assessee in ITA No.706/Hyd/2022 is dismissed.

24. As far as the other appeal is concerned, in view of the submission of both the parties that the issues raised in A.Y. 2016-17 are identical to the other assessment year, we for the reasons stated hereinabove while deciding the appeal in ITA 706/Hyd/2022 and for similar reasons, dismissing the other appeal also. Accordingly, the appeal of assessee in ITA No.707/Hyd/2022 is dismissed.

SA Nos.47 and 48/Hyd/2023

25. In view of the dismissal of both the appeals of assessee, the stay applications filed by the assessee got vacated.

26. To sum up, both the appeals and the stay applications filed by the assessee are dismissed. A copy of the same may be placed in respective case files.

Order pronounced in the Open Court on 23rd March, 2023.