Alternative Investment Funds: Indian Experiments and Way Forward with Tax Efficiency

Executive Summary

To enable ease of doing business, the taxation framework for Alternative Investment Funds (AIF) provide pass-through status to profits of the AIF (Category I and Category II) to the investors under which any income, barring business income, earned by AIFs would be exempt in the hands of such AIFs, and taxable directly in the hands of its investor(s). A huge taxation relief is accorded to non-resident investors of AIFs in India due to which overseas investment by AIFs of non-resident investors is not taxable in India and thereby leveraging ease of doing business in India. Tax incentives are not only provided to the investors of AIFs, but entities who receive investments from AIFs are also accorded a beneficial taxation position which includes exemption of venture capital undertakings availing funding from Category I and Category II AIFs from Angel Tax, start-ups are allowed to deduct their investments from VCFs while calculating the share capital to deduce whether they are eligible for exemption from taxation of any excess premium received by a closely held company upon the issue of shares. Despite there being an adequate framework for regulation of AIFs by SEBI, certain loopholes which need attention includes tax-pass through status to Category III AIFs and pass through of losses of AIFs which are incurred after March 31, 2019. There was an absence of appropriate provision to cover transactions made between non-residents involving a holding company based outside India of an Indian company. A cross-border uniform AIF taxation structure is required in order to supress the effect of loopholes existing in taxation structure of different jurisdictions and further motivate investors to park funds in India without bearing the burden of tax related ambiguities. It is also recommended that the Indian regime can introduce a provision which encourages exiting start-ups to infuse or redeploy their investment in new start-up ventures.

ALTERNATIVE INVESTMENT FUNDS

Capital infusion is a major necessity for any economy to shift towards progressive activities. The effect of increased capital infusion can be witnessed across the growth of various sectors. In any economy, one of the major barriers to growth is the inability of the nation to infuse capital for progressive activities. Without adequate capital, the production of goods and services is hindered which in turn impacts consumption thereby, effecting the flow of funds in the economy. So, here the challenge arises as to the methods and routes through which capital can be infused inside the economy to drive it towards growth.

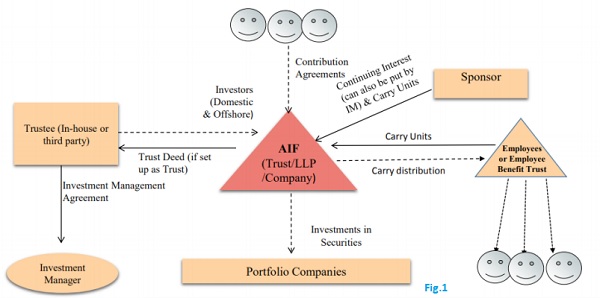

One of the methods for infusing capital in the Indian economy is through the private route of Alternative Investment Funds (AIFs). These funds are important facets of the financial system and economy. As the name suggests, AIFs are alternative investment options acting as privately pooled investment vehicles. The funds from domestic and foreign investors are collected for investing in well-defined investment policies for the benefit of investors.

In the Indian context, the investment momentum in AIFs has gained popularity and investor’s attention. In 2018, the commitments raised through AIFs were worth over INR 2 lakh crore, and corporate funds worth INR 1 lakh crore were raised. In the first quarter of 2019, commitments worth INR 1.79 lakh crore were raised and INR 97,611.73 crore worth of funds were raised.1 The capital pumped in by AIFs rose to nearly INR 1.1 trillion in the January-March quarter of 2019, which is nearly 79% higher than it was in the same period a year ago.2

As we all understand, AIFs grant support towards economic stability as existing, new and emerging entrepreneurs are accorded with the right financial support for growth. The induced capital enhances the production of goods and services and allows companies to generate revenue for many years by adding or improving production facilities and boosting operational efficiency. This, in turn, grants a strong backbone for economy to remain stable and further in multiplication of GDP.

We believe that AIFs widen the scope of capital infusion as they explore the catena of investment options without residing in traditional investment methods such as stocks, bonds or commodities. The large scope of investment options enable the investors to park funds in India which are recurrently put to use for the furtherance of economic activities, resolving the problems affiliated to economic slowdown in terms of capital infusion to a certain extent. In that regard, AIFs help to reform the macroeconomic drivers, post-crisis financial industry regulation and critical industry trends. The investment in AIFs are largely accommodated by high net worth individuals (HNI) or private equity (PE) investors with higher appetite for risk and return. The investments by HNI and PE investors not only bring in exponential returns for such investors but also promote innovation in the field of technology, finance and for that matter the advanced fin-tech arena.

EXISTING FRAMEWORK

The Securities and Exchange Board of India (SEBI) grants approval to an AIF to commence operations and continues to monitor AIFs through SEBI (Alternative Investment Funds) Regulation 2012 (hereinafter ‘SEBI Regulations’).

AIFs can be structured in the form of a company, trust, corporate body or limited liability partnerships (LLPs) with funds from either domestic or foreign investors.3

Categories of Alternative Investment Funds

Under the SEBI Regulations, the private investment funds can be structured under any of the three categories as per the functioning of the fund. The minimum corpus amount for each scheme of these AIFs shall be at least INR 20 Crores with the exception of one sub-category of AIF-I which is Angel Funds. Angel Funds are prescribed to have a lesser corpus amount of INR 10 Crores.4

Table 1

| Title | Category I AIF | Category II AIF | Category III AIF |

| Investment | Start-ups, early stage ventures, small and medium enterprises (SMEs), sectors with beneficial socio-economic impact as defined by the regulator or government | Funds which do not fall within Category I or II; Funds which do not undertake leverage or borrowing except for meeting operational requirement | Employ diverse or complex trading strategies and may use leverage in listed or unlisted derivatives |

| Class of Funds | Venture Capital Funds, SME funds, Social Venture Funds, Infrastructure Funds | Private Equity Funds, Realestate Funds, Debt Funds | Hedge Funds, Funds which trade to make short-term investments, open ended funds |

| Additional incentives by regulator or government | Specific concessions or incentives are granted for beneficial socioeconomic funds | No specific concessions or incentives are granted | No specific concessions or incentives are granted |

| Pass-over benefit of taxation | Liability to pay tax on income passed over to investors | Liability to pay tax on income passed over to investors | Liability to pay tax on income cannot be passed over to investors (Double Taxation)1 |

| Open-ended/ Closed ended | Only closed-ended | Only closed-ended | Can be open-ended and closed ended |

| Listing of fund | Cannot list fund | Cannot list fund | Can list open-ended fund post closure of the scheme |

TAXATION OF ALTERNATIVE INVESTMENT FUNDS

Prior to 2007, venture capital funds (VCF) registered with SEBI were regulated by Securities and Exchange Board of India (Venture Capital Funds) Regulations 1996 (Old VCF Regulations). Under the Old VCF Regulations, VCFs were accorded a tax pass-through5 benefit on their income. The income of a VCF earned from its investment in any venture capital undertaking was exempt from tax in the hands of the fund and was only taxable in the hands of the limited partners of the fund thereby prohibiting double taxation.6 In 2007, this tax ‘pass-through’ benefit was restricted only to income from venture capital undertakings that operated in nine specified sectors. However, the Finance Bill 2012 once again reverted to the pre-2007 position by extending this tax ‘pass-through’ benefit to income of a venture capital fund arising from investment in any venture capital undertaking, regardless of the sector in which the venture capital undertaking operates.

Post notification of Securities and Exchange Board of India (Alternative Investment Funds) Regulations 2012 (AIF Regulations), the tax ‘pass-through’ status was only accorded to Category I AIF which was later extended to Category II AIF. This tax ‘pass-through’ status is comparable to the position under Old VCF Regulations under which the liability to pay tax is shifted to the investors. For doing so, the investment in AIF is presumed to be made directly by the investor without routing the same through the financial intermediary.7

In order to avail this tax pass-through status, such Fund has to comply with the conditions under Section 10(23FB) the Income Tax Act 1961 and shall not violate the SEBI Regulations.8 However, when the income of the investment fund is characterized as ‘Profits and gains of business or profession, the liability to pay tax is upon the investment fund for such income at a maximum marginal rate of tax. In relation to the losses incurred by the AIFs, no tax pass through status has been accorded through which they can pass their losses to their investors which is a rising concern among investors.

No tax pass-through has been granted to Category III AIF due to which the income from the investment of these funds is taxed twice, firstly when such income arises or accrues in favour of the AIF and secondly when such income accrues or arises in the favour of individual investor. In 2015, SEBI constituted the Alternative Investment Policy Advisory Committee (AIPAC) headed by Infosys Ltd co-founder Murthy which recommended that the tax pass-through status shall be accorded to Category III AIF as well.

The Income Tax Act 1961, exempts the income earned by a VCF from investments in a venture capital undertaking. However, to avail this exemption, the VCF shall operate under a duly registered trust deed with a certificate of registration before May 21, 2012 under Old VCF regulations.9

RECENT DEVELOPMENTS

Tax Treatment of Offshore Investments by Non–residents Through AIFs

Many non-resident investors contribute into AIFs. The AIFs often use such capital investments to make overseas investments. Multiple references were made seeking clarity over the tax treatment of these investments in India under Section 5 which defines the scope of total income for the purpose of computation under the Income Tax Act 1961. Section 5(2)10 of the Income Tax Act 1961 imposes source-based taxation on non-residents whereby income received or arising or deemed to be received or arising to a non-resident in India would be subject to tax in India.

The CBDT in its recent circular11 stated that an income earned from such off-shore investments made through AIFs of Category I and II by Non-Residents could be deemed to be direct investment by a non-resident, and hence not subject to tax in India under the Income-tax Act. The circular also went on to clarify that any losses suffered from such offshore investments, shall not be allowed to be set-off or carried forward against the income of the AIFs of Category I and II.

Pass-Through Treatment Extended to Losses of AIFs

The Finance Act 2015 had extended the tax pass-through status to Cat I and Cat II AIFs. As per the existing provisions, any income, barring business income, earned by such AIFs would be exempt in the hands of such AIFs, and taxable directly in the hands of its investor(s) in the same manner and proportion as it would have been, had such investor received such income directly and not through such AIFs. With respect to the losses incurred by such AIFs, whether in the nature of business losses or otherwise, the same could be set-off or carried forward by such AIFs. However, losses suffered by such AIFs (not being in the nature of business losses) could not be passed through to its investors for them to claim set-off of such losses against income earned by them.

In order to address the above anomaly, the Finance Act 2019 has allowed losses incurred by such AIFs (those not in the nature of business losses) to be passed through to its investors to be able to set-off or carry forward such losses while computing their income. However, in order to avail such pass-through benefit, such investors should have held the unit in the AIF for a period of more than 12 months.

In addition to this, the Finance Act 2019 has inserted a new Sub-section under Section 115UB12 of the Income-tax Act whereby, accumulated or unabsorbed losses (those not in the nature of business losses) of such AIFs as on March 31, 2019 would be passed through to its investors to be carried forward/ set-off against their income, provided that the investor was a holder of units of the AIF as on March 31, 2019. Such losses could be carried forward and accordingly set-off by investors from the year in which the loss first occurred, subject to the period of limitation provided with respect to set-off and carry forward of losses under the Income-tax Act 1961.

This provision shall not be applicable to the investors that acquire units of an AIF on or after April 1, 2019 and it would not be applicable to investors holding units as on March 31, 2019, who have been accorded the set-off/ carrying forward loss pass-through status.

Revisions to Angel Tax Provisions

In the Finance Act of 2012, a 30% tax was imposed on this excess value to arrest laundering of funds. Angel tax is a term used to refer to the income-tax payable on capital raised by unlisted companies via issue of shares where the share price is seen in excess of the fair market value of the shares sold under Section 56(2)(viib)13of the Income-tax Act 1961. It lays down that the difference between the excess of the fair market value of the shares shall be considered for taxation under the head ‘income from other sources’. It does not apply to firms registered as ‘start-ups’, with the government or those raising money from venture capital funds, which come under Category I of AIFs14 or by a company from a class or classes of persons as may be notified by the Government in this behalf.

Source: India Private Equity Report 2019 by Indian Private Equity & Venture Capital Association and Bain & Company15

Under the Finance Act 2019, this exemption has been extended to venture capital undertakings to receive funds from Category II of AIFs as well. This is seen as a good move, since most AIFs fall under Category II.

Taxation and Investment in Start–up Companies

Through a February 2019 circular16 issued by the DPIIT, start-up companies which have registered themselves with the DPIIT shall be eligible for tax exemption under Section 56(2)(viib) of the Income-tax Act 1961. To be eligible for this exemption, the aggregate amount of paid up share capital and share premium of these start-up companies, after issue or proposed issue of shares, must not exceed INR 25 Crore. While calculating the share capital, shares issued to a non-resident or a venture capital company or a venture capital fund have not been included.

To provide a conducive environment for start-up companies, some relaxations with regard to direct tax assessment of start-up entities for Section 56(2)(viib) of the Income-tax Act 1961 were introduced17. Where the start-up company has been recognized by the DPIIT but the case is selected under ‘limited scrutiny’ on the single issue of applicability of the section, no verification on such issues will be done by the Assessment Officers during the proceedings under Section 143(3) and Section 147 of the Income-tax Act 1961 and the contention of such recognized start-up companies on these issues will be summarily accepted. Secondly, if the case is selected under ‘limited scrutiny’ with multiple issues or under ‘complete scrutiny’ under the section, the issue of applicability of the section will not be pursued during the assessment proceedings as well. For the companies which have not been approved by DPIIT, the case is selected for scrutiny, inter alia on the grounds of applicability of Section 56(2)(viib), then inquiry or verification in such cases shall be carried out by the Assessment Officers, as per due procedure, only after obtaining approval of their supervisory officer.

The CBDT circular in March 2019 provided exemption from Section 56(2)(viib) for entities recognized by the DPIIT from taxation on consideration received by a company for issue of shares received from a resident person.

These exemptions were extended to a recognized start-up entities which would have filed a declaration under Form 2. In addition to this, the proceedings appeal against the assessment is pending before the Commissioner of Income-tax (Appeal), the appellate order should be passed by CIT(A) on or before 31st December, 2019 and the department shall not file an appeal in the same matter. As for the appeal before Income Tax Appellate Tribunal, the Department shall not press the ground relating to addition under Section 56(2)(viib) of the Income-tax Act 1961.18

INTERNATIONAL BEST PRACTICES IN TAXATION OF AIFS

Luxembourg

The Reserved Alternative Investment Fund (RAIF) vehicle was set to change Luxembourg’s Alternative Investment Fund (AIF) landscape when it was introduced in July 2016 due to its flexibility and ability to be deployed quickly. The credit for the same is attributable to regulation through an Alternative Investment Fund Manager (AIFM).19

A fund set up under Part II of the Luxembourg Law of 17 December 2010 on undertakings for collective investment (UCIs) is an investment fund that can invest in all types of assets. It qualifies as alternative investment fund (AIF) and can be sold to all types of investors.20 These Part II funds are exempted from any Luxembourg tax on income, withholding, capital gains or net wealth tax or any other direct tax.

No withholding tax is levied on distribution made by a Luxembourg based AIF to residents or non-resident, whereas the distribution made by an unregulated AIF is subjected to a withholding tax of 15%. The income distributed by AIF should not be taxed in the country of residence or the non-resident or pension fund investor. The capital gains can only be taxed for the unregulated AIFs, where no Dividend Distribution Tax is available or under certain specific circumstances. Capital gains arising from the sale of the shares of AIF or units, except the speculative gains (considered to be the ones which are realized within 6 months after acquisition) are exempted in the hands of the resident individual investor. However, investors holding more than 10% of the capital of the SICAV21 or SICAF22 the 10% being determined on the umbrella fund. Dividend distributed by the AIF is subjected to a progressive tax rate depending on the income level of the recipient and matrimonial situation with the marginal tax rate of 45.78% (including the employment contribution fund).23

Singapore

Limited partnerships are not treated by Revenue Authority of Singapore (IRAS) as legal person and hence no tax is levied at the partnership level. However, the number of shares held by the partners shall be taxed at the applicable rate. Although Singapore taxes income accruing in or derived from Singapore and on foreign-sourced income received or construed to have been received in Singapore, subject to certain exceptions. Singapore does not tax on capital gains, but the income arising out of disposal of any investment shall be considered for the purposes of taxation. However, where a gain is considered to be revenue in nature, such gain could be subject to tax if it is sourced in Singapore or in the case of foreign-sourced gain, if it is remitted into Singapore.24

AIFs in Singapore often face an issue, whether gains are capital in nature and hence not taxable or they are taxable as trading income. AIFs in Singapore are generally taxed at a fixed rate of 17% on their chargeable income. However, there exists an exemption where if an AIF holds 20% or more of the share capital of another company for a time period of 24 months or more, then the gains will be exempted from tax, provided that they are disposed of between 1 June 2012 and 31 May 2022.

Singapore also offers various tax incentives for AIF to promote the use of city-based managers in the AIF structure. Monetary Authority of Singapore rolls out various schemes for such AIFs, including qualifying conditions to enjoy complete exemption from all incidents of income tax for income sources from immovable properties in Singapore. This regime can be viewed to be a well-balanced regime.

FOOD FOR THOUGHT

Preferred Country to Route Investments in Asia

From companies encouraging consumption of fresh foods to food delivery and ride-hailing apps, all are causing behavioural changes whose momentum is changing habits, preferences, and lifestyles. Venture Capital Funds capitalize on the growth trajectory of the Indian start-up ecosystem and behavioural changes permeating Indian society. The venture capital space in India also has government backing in the form of frameworks that institutionalize it. Such institutionalization gives investors clarity about the structure, process, and due diligence of investments in start-ups making investing in Venture Capital Funds attractive. The recent government decision to ease norms for start-ups including exemptions for AIFs investing in start-ups makes Venture Capital Funds even more attractive. With certain relaxation in the regime, the venture capital business in India is expected to flourish. It can additionally act as the base of Alternative Investment Funds in South Asia.

Uniform Taxation Structure

A cross-border uniform AIF taxation structure is required in order to supress the effect of loopholes existing in taxation structure of different jurisdictions and further motivate investors to park funds in India without bearing the burden of tax related ambiguities. The investors seek benefits of these existing loopholes and route transactions in a way to gain maximum benefits from the deficient structures. To the extent that all investments are taxed similarly, there will be no incentive to try to come within the scope of tax-favoured treatment. Moreover, there will be incentive for investors to invest in a taxation regime which is uniform and free of ambiguities and discrepancies. A uniform taxation structure shall further enable equitable sharing of tax revenue between transacting countries which is generally leaked due to evasion and avoidance. This shall help in furtherance of the government’s objective of ‘ease of doing business in India’ and clarity in the taxation structure will provide a competitive edge to the domestic fund managers and will improve the prospects of an appropriate risk-return profile of these pooled investment vehicle.

Identification of Ultimate Beneficiary and Easier Compliance

One single efficient system is required which discourages forum shopping. The government needs to devise a strategy to ascertain whether tax benefits shall be given to the AIFs or the investors. If AIFs are incentivized then another issue at hand which emerges is other investment platforms shall also be looking forward for the upcoming incentives. In that regard, the revenue loss and market consequences needs to be weighed appropriately. The absence of a complex structure allows easier compliance with tax regulatory requirements which encourages investors to infuse capital in the Indian economy.

Notes:-

1See: https://www.financialexpress.com/market/alternate-investment-funds-aif-investments-in-india-set-to-hit-record-high/1414360/

2See: https://timesofindia.indiatimes.com/business/india-business/aif-investments-surge-79-to-rs-1-10-lakh-cr-in-march-qtr/articleshow/69146567.cms

3Regulation 3(4)(a), SEBI (Alternative Investment Funds)

4The income is taxed twice, firstly, in the hands of the Category III AIF and secondly, as the income of individual investor.

5Tax pass-through status implies that the liability to pay tax on the income earned by the AIF shall be passed from the hands of the AIF to the individual income attributable to each investor.

6Section 10(23FB) read with Section 115UB, Income Tax Act 1961.

7Section 33, Finance Act 2015 and Section 115UB (1), Income-tax Act 1961.

8M/s HDFC Property Fund vs. Income Tax Officer, February 2019.

9Section 10(23FB), Income Tax Act, 1961

10Section 5, Income Tax Act, 1961

11CBDT Circular dated 3 July 2019 on ‘Clarification regarding taxability of income earned by a non-resident investor from off-shore investments routed through an Alternate Investment Fund reg’, Circular No. 14/2019, https://www.incometaxindia.gov.in/communications/ circular/circular_no_14_2019.pdf

12Section 115UB, Income Tax Act, 1961

13Section 56(2) In particular, and without prejudice to the generality of the provisions of Sub-section (1), the following incomes, shall be chargeable to income-tax under the head “Income from other sources”, namely:—

(viib) Where a company, not being a company in which the public are substantially interested, receives, in any previous year, from any person being a resident, any consideration for issue of shares that exceeds the face value of such shares, the aggregate consideration received for such shares as exceeds the fair market value of the shares:

Provided that this clause shall not apply where the consideration for issue of shares is received—

(i) by a venture capital undertaking from a venture capital company or a venture capital fund [or a specified fund]; or

(ii) by a company from a class or classes of persons as may be notified by the Central Government in this behalf.

14Gazette Notification No. G.S.R. 127(E) dated February 19, 2019 of Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, https://dpncindia.com/blog/wp-content/uploads/2019/02/ DIPP-Notification-dated-19-Feb-2019.pdf

15https://www.bain.com/contentassets/1b165fbff096473685e36a3b10df09a0/ bain_report_india_private_equity_report_2019.pdf

16G.S.R. 127, 19 February 2019, Notification, Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, Government of India, New Delhi.

17‘Clarification with respect to assessment of Startup companies involving application of sSection 56(2)(viib) of Income Tax Act, 1961-reg.’, Circular No. 16/2019, Central Board of Direct Taxes, Department of Revenue, Ministry of Finance, Government of India, New Delhi.

18‘Consolidated circular for assessment of Startups – reg.’, Circular No.22/2019, 30 August 2019, Central Board of Direct Taxes, Department of Revenue, Ministry of Finance, Government of India, New Delhi.

19http://www.mondaq.com/x/731878/ Fund+Management+REITs/ What+has+the+RAIF+brought+Luxembourg

20https://www.luxembourgforfinance.com/publication/a-non-ucits-part-ii-fund/

21A SICAV (Société d’Investissement à Capital Variable) in Luxembourg is an investment fund in the form of an Investment Company whose share capital is variable and the value of which at any time matches the value of the net assets of all the sub-funds, constituted as shares without a statement of their nominal value.

22A SICAF Investment Fund (Société d’Investissement a Capital Fixe) in Luxembourg exists in the form of an Investment Company whose share capital is fixed.

23https://iclg.com/practice-areas/alternative-investment-funds-laws-and-regulations/luxembourg

24https://home.kpmg/content/dam/kpmg/pdf/2015/11/ singapore-asean-tax-2015.pdf

About Author

|

|

|

Mr. P.K. Dash, IRS (Retd.) (IT: 1982) prasana.k.dash@incometax.gov.in Mr. Prasana Kumar Dash is an Indian Revenue Service (IRS) officer of 1982 batch. He retired from the service as Member, CBDT, Delhi. He has worked in I.T. Deptt at various levels dealing with Assessment, Investigation, Administration etc. He has been on deputation to Election Commission of India, Ministry of Environment, Forest and Climate Change, New Delhi, NALCO etc. |

Mr. Anuroop Omkar Partner at AK and Partner anuroop@akandpartners.in Anuroop Omkar, Founding at AK & Partners Partners Assisted by Aditi Jha, Consultant, Bridge Policy Think Tank and Srishti Dembla, Associate, AK & Partners |

Source- Taxalogue 3- April to June 2020