Case Law Details

Sandeep Garg Vs DCIT (ITAT Delhi)

Held that assessee established identity of the creditors by bringing on record their PANs and complete addresses of the creditors. Hence addition u/s 68, without bringing out any adverse or cogent material to dispute the credit worthiness of the creditors and genuineness of the transactions, is unsustainable

Facts-

The assessee contented that CIT(A) has erred in confirming addition of Rs. 14,25,000 in unsecured loan u/s 68 for unexplained cash credit as the assessee has proved identity, creditworthiness and genuineness of these loans.

Conclusion-

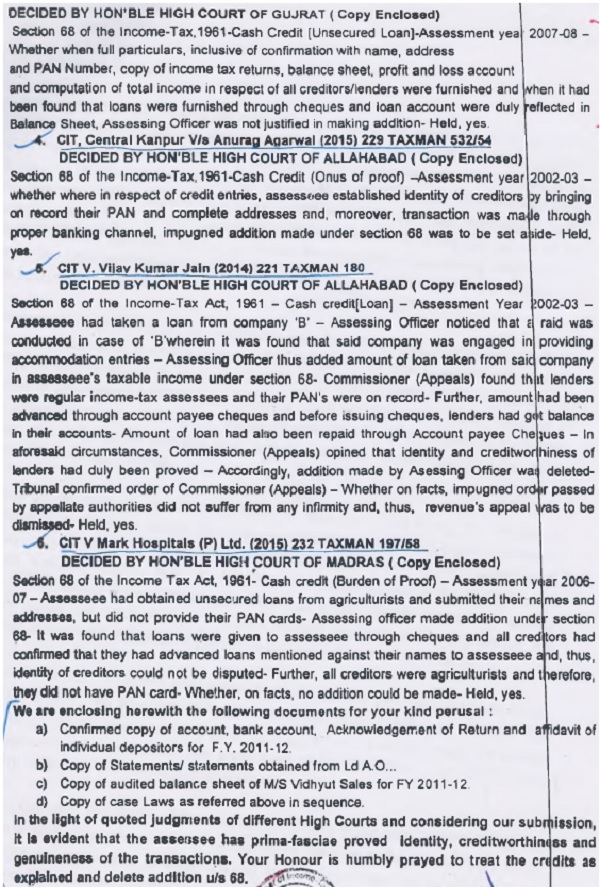

The Hon’ble jurisdictional High Court of Allahabd in the case of CIT, Central vs. Anurag Agarwal and CIT vs. Vijay Kumar Jain where in respect of credit entries found in the books of account of the assessee, the assessee established identity of the creditors by bringing on record their PANs and complete addresses and the transactions were made through banking channel, the impugned addition was to be set aside.

Held that without bringing out any adverse or cogent material to dispute the credit worthiness of the creditors and genuineness of the transactions, no addition could have been made in the hands of the assessee treating the same as unexplained cash credit u/s 68 of the Act. We, therefore, decline to accept the reasoning recorded by the ld.CIT(A) while confirming the part addition in the hands of the assessee with regard to eight creditors totaling to Rs.14,25,000/-. We, therefore, allow the sole ground of the assessee and direct the AO to delete the entire addition confirmed by the ld.CIT(A).

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal filed by the assessee is directed against the order dated 04.05.2017 of the CIT(A), Meerut, relating to Assessment Year 2012-13.

2. The sole ground of the assessee reads as follows:-

“2. That on the facts of the case CIT(Appeal) has erred in confirming addition of Rs.14,25,000/- in unsecured loan u/s 68 of the IT Act, 1961 for unexplained cash credits. The assessee has proved identity, creditworthiness and genuineness of these loans as per law. CIT (Appeals) is not justified in confirming this addition and addition is against law and natural justice.”

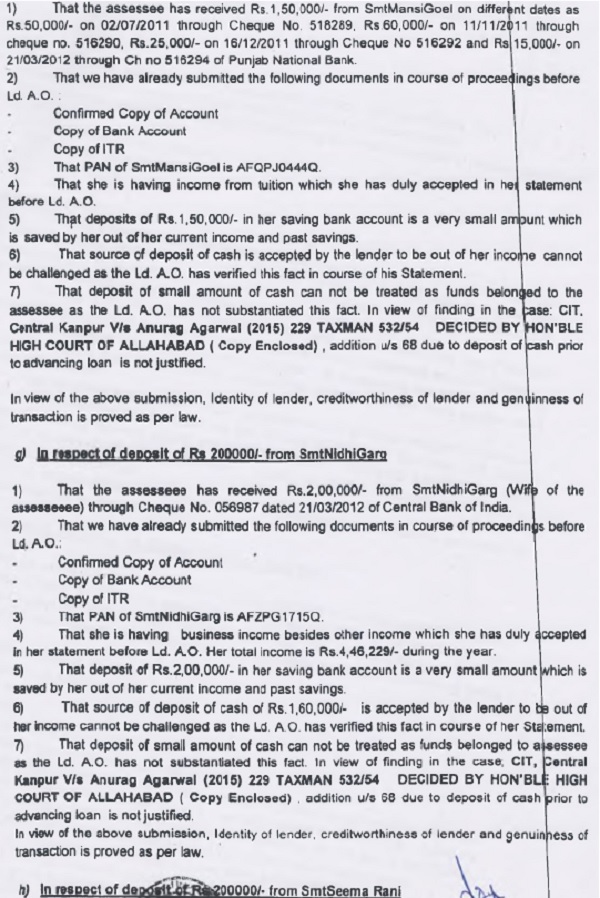

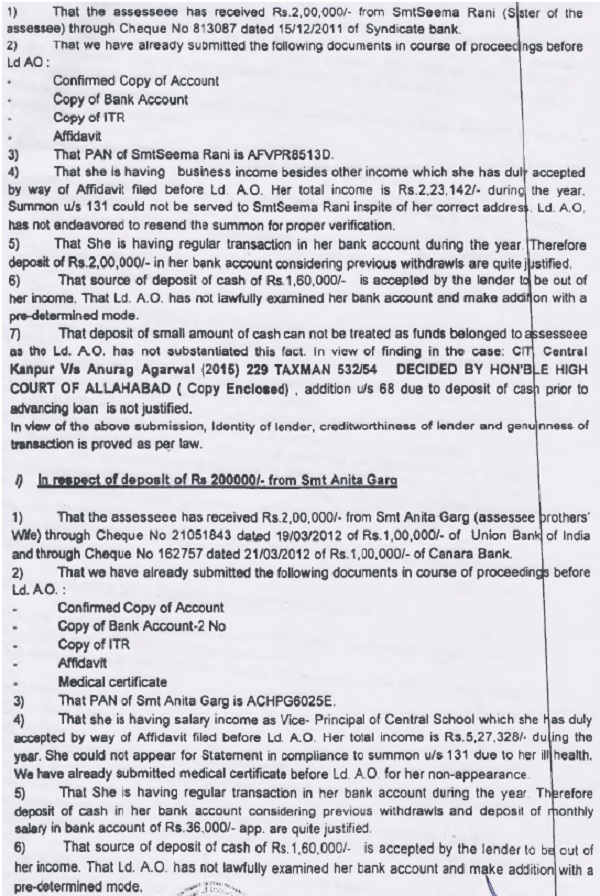

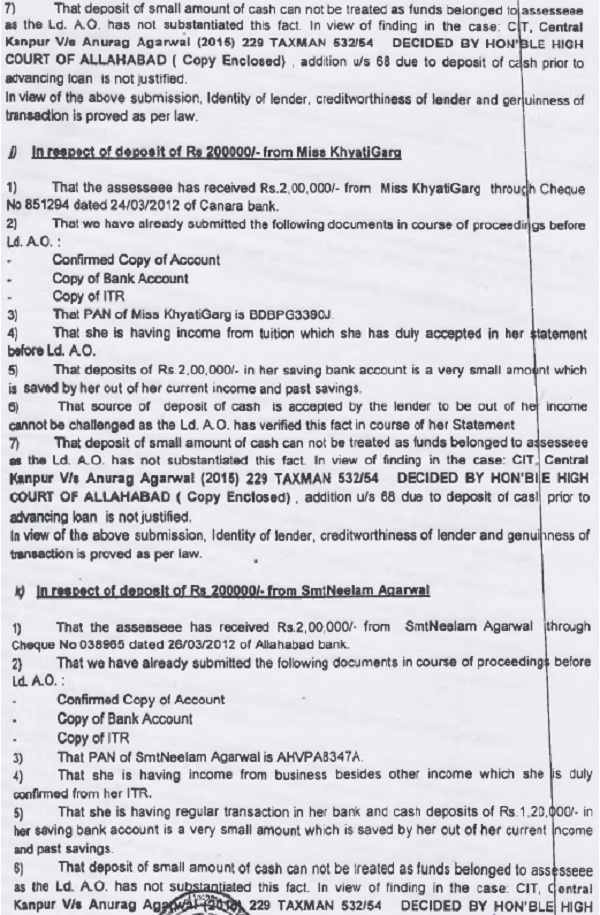

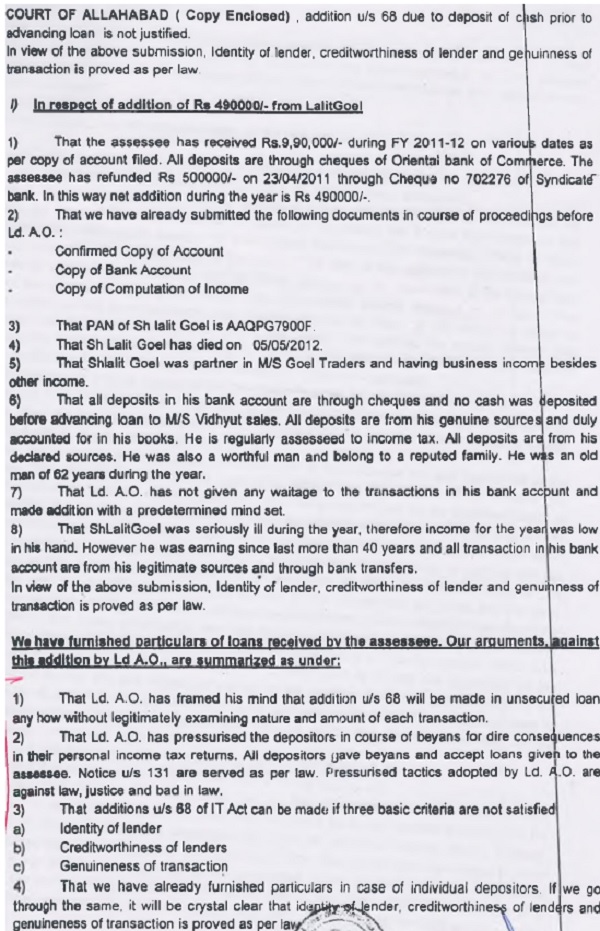

3. The ld. Counsel for the assessee submitted that the AO has framed his mind that addition u/s 68 will be made in unsecured loan and without logically examining the nature and amount of his transaction, the AO has made the impugned addition. The ld. AR submitted that the AO has pressurized the depositors for not recording the statements and warned of dire consequences if done so in their personal income-tax returns. But, all depositors, in their statements, accepted to have given loans to the assessee. He vehemently pointed out that the addition u/s 68 cannot be made if the assessee has successfully satisfied the AO about the identity of the lender, creditworthiness of the lender and genuineness of the transaction. The ld. AR submitted that during the course of assessment proceedings as well as first appellate proceedings, the assessee furnished addresses of all individual creditors and if these particulars are analysed and evaluated independently, then, it would be crystal clear that the identity of the lenders, credit worthiness of the lenders and the genuineness of the transaction have been established as per the requirement of section 68 of the Act. The ld. AR submitted that before the authorities below, the assessee submitted confirmed copies of creditors’ accounts, bank accounts, acknowledgement of returns and affidavits of individual creditors for AY 2012-13. He further submitted photocopies of statements of creditors, copy of audited balance sheet of M/s Vidyut Sales and copy of case law referred to in the written submissions of the assessee. The ld. AR submitted that in the light of the various judgments including the judgment of the Hon’ble jurisdictional High Court of Allahabad in the case of CIT vs. Anurag Agarwal, reported in 229 taxman 532 and second judgment in the case of CIT vs. Vijay Kumar Jain (2014) 221 taxman 180 (All) where in respect of credit entries the assessee established identity of creditors by bringing on record their PANs and complete addresses and transaction was made through proper banking channel and the addition made u/s 68 of the Act was set aside being not sustainable. The ld. Counsel also placed reliance on various judgments including that of the Hon’ble Delhi High Court in the case of CIT vs. Shiv Dhooti Pearls & Investment Ltd., 237 Taxman 104 and submitted that the assessee must establish the genuineness and the transaction as well as the credit worthiness of the creditor, the burden of the assessee to prove the genuineness of the transactions as well as the creditworthiness of the creditor must remain confined to the transactions, which have taken place between the assessee and the creditor and not beyond doubt. The ld. Counsel submitted that for AY 2012-13 it was not the requirement from the assessee to establish source of the source, therefore, the addition made by the AO and partly confirmed by the ld.CIT(A) may kindly be deleted.

4. Replying to the above, the ld. Sr. DR strongly supported the assessment and first appellate orders and submitted that it was the duty of the assessee to prove the identity of the creditor, credit worthiness of the creditors and genuineness of the transaction and the assessee failed to discharge the onus lay on the shoulders, therefore, the authorities below were right in making the addition in the hands of the assessee.

5. First of all, we may point out that the ld.CIT(A) has, in para 3.2, has noted the submissions of the assessee. For the sake of completeness of our findings, we find it appropriate to reproduce the same as follows:-

6. From the relevant operative portion of the first appellate order, we find that the ld.CIT(A) has allowed part claim of the assessee pertaining to four creditors, i.e., Smt. Saroj Garg, Smt. Nidhi Garg, Smt. Anita Garg and Shri Lalit Goel and granted relief to the assessee amounting to Rs.11,10,000/-. However, regarding other eight credits, totaling to Rs.14,25,000/-, the ld.CIT(A), on the similar facts and circumstances, confirmed the part addition by observing that the onus has been cast upon the assessee to establish the identity, capacity and creditworthiness of the creditors as well as the genuineness of the transaction and as the assessee failed to discharge the onus regarding the eight creditors, he took an adverse view and confirmed the part addition of Rs.14,25,000/-. From the written submissions of the assessee, we clearly observe that the assessee before the ld.CIT(A) categorically repeated the submissions and submitted confirmations, copy of bank accounts and PANs of almost all creditors, but, the ld.CIT(A) accepted the same material with regard to the four creditors granting part relief to the assessee and denied to accept the identity and credit worthiness of the creditors and genuineness of the transaction in the case of other eight creditors without showing any distinct and dissimilar position. Since as per the judgment of the Hon’ble jurisdictional High Court of Allahabd in the case of CIT, Central vs. Anurag Agarwal (supra) and CIT vs. Vijay Kumar Jain (supra) where in respect of credit entries found in the books of account of the assessee, the assessee established identity of the creditors by bringing on record their PANs and complete addresses and the transactions were made through banking channel, the impugned addition was to be set aside. In the present case, the authorities below have disputed credit entries of Rs.14,25,000/- from eight creditors with amounts between Rs.65,000/- to Rs.2,10,000/- and all creditors are relatives/friends of the assessee. Therefore, without bringing out any adverse or cogent material to dispute the credit worthiness of the creditors and genuineness of the transactions, no addition could have been made in the hands of the assessee treating the same as unexplained cash credit u/s 68 of the Act. We, therefore, decline to accept the reasoning recorded by the ld.CIT(A) while confirming the part addition in the hands of the assessee with regard to eight creditors totaling to Rs.14,25,000/-. We, therefore, allow the sole ground of the assessee and direct the AO to delete the entire addition confirmed by the ld.CIT(A).

7. In the result, the appeal filed by the assessee is allowed.

Order pronounced in the open court on 29.07.2022.