GST Registration

Persons Liable for Registration {Sec.22 of CGST Act, 2017}:-

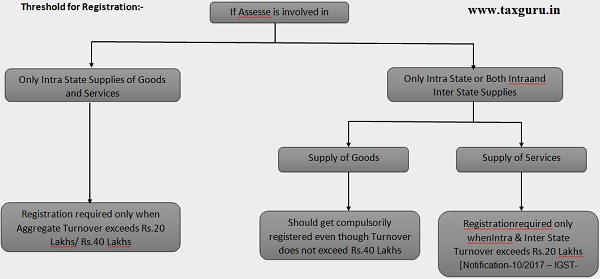

1. Every supplier shall be liable to be registered under this Act in the State or Union territory, other than special category States, from where he makes a taxable supply of goods or services or both, if his aggregate turnover in a financial year exceeds twenty lakh rupees[1].

Provided that where such person makes taxable supplies of goods or services or both from any of the special category States, he shall be liable to be registered if his aggregate turnover in a financial year exceeds ten lakh rupees.

2. Every person who, on the day immediately preceding the appointed day, is registered or holds a license under an existing law, shall be liable to be registered under this Act with effect from the appointed day.

3. Where a business carried on by a taxable person registered under this Act is transferred, whether on account of succession or otherwise, to another person as a going concern, the transferee or the successor, as the case may be, shall be liable to be registered with effect from the date of such transfer or succession.

4. Notwithstanding anything contained in sub-sections (1) and (3), in a case of transfer pursuant to sanction of a scheme or an arrangement for amalgamation or, as the case may be, demerger of two or more companies pursuant to an order of a High Court, Tribunal or otherwise, the transferee shall be liable to be registered, with effect from the date on which the Registrar of Companies issues a certificate of incorporation giving effect to such order of the High Court or Tribunal.

Note:-

- Supply of goods, after completion of job work, by a registered job worker shall be treated as the supply of goods by the principal referred to in section 143, and the value of such goods shall not be included in the aggregate turnover of the registered job worker;

Threshold for Registration:-

Aggregate Turnover {Sec. 2(6) of CGST Act}:-

- Includes:- 1) Taxable Supplies

2) Exempt Supplies

3) Export Turnover

4) Outward Supplies taxable as Reverse Charge

- Excludes:- CGST; SGST; UTGST and IGST

Persons not Liable for registration {Sec.23 of CGST Act, 2017}:-

1. Person engaged exclusively in supplying goods/services/both not liable to tax

2. Person engaged exclusively in supplying goods/services/both wholly exempt from tax

3. Agriculturist to the extent of supply of produce out of cultivation of land

4. Persons making only reverse charge supplies (Notification No. 5/2017)

Compulsory registration in Certain Cases {Sec.24 of CGST Act, 2017}:-

Notwithstanding anything contained in sub-section (1) of section 22, the following categories of persons shall be required to be registered under this Act:-

I. Persons making any inter-State taxable supply

II. Casual taxable persons making taxable supply

III. Persons who are required to pay tax under reverse charge

IV. Non-resident taxable persons making taxable supply

V. Persons who are required to deduct tax under section 51, whether or not separately registered under this Act

VI. Persons who make taxable supply of goods or services or both on behalf of other taxable persons whether as an agent or otherwise

VII. Input Service Distributor, whether or not separately registered under this Act

VIII. Persons who supply goods or services or both, other than supplies specified under sub-section (5) of section 9, through such electronic commerce operator who is required to collect tax at source under section 52 [Exception: – Service providers providing services on e-commerce platforms are exempted from registration if their annual turnover is below 20 lakhs (As per Notification No: – 65/2017, dated.15-11-2017)].

IX. Every electronic commerce operator

X. Every person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered person and

XI. Such other person or class of persons as may be notified by the Government on the recommendations of the Council.

Procedure for registration {Sec.25 of CGST Act, 2017}:-

1. Every person who is required to get registered U/s.22 or U/s.24 shall apply for registration in every such state or Union territory in which he is so liable within 30 days from the date on which he becomes liable to registration.

Provided that a casual taxable person or a Nonresident taxable person shall apply for registration at least 5 days prior to the commencement of business.

2. A person seeking registration under this Act shall be granted a single registration in a State or Union territory

Provided that a person having multiple business verticals in a State or Union territory may be granted a separate registration for each business vertical, subject to such conditions as may be prescribed.

3. Further, within a State, an entity with different branches would have single registration wherein it can declare one place as principal place of business (PPOB) and other branches as additional place of business (APOB).

4. A person, though not liable to be registered under section 22 or section 24 may get himself registered voluntarily, and all provisions of this Act, as are applicable to a registered person, shall apply to such person.

5. If one of the multiple registration of a taxable person is paying tax under normal levy [Section 9], no other registration shall be granted registration to pay tax under composition levy [Section 10].

6. If one of the separately registered unit becomes ineligible to pay tax under composition levy, all other registered units would also become so ineligible.

7. A person who has obtained/ is required to obtain more than one registration, whether in one State/ Union territory or more than one State/Union territory shall, in respect of each such registration, be treated as distinct persons.

Display of registration certificate and GSTIN on the name board [Rule 18]:-

- Every registered person shall display his registration certificate in a prominent location at his PPoB and at every APoB.

- Further, his GSTIN also has to be displayed on the name board exhibited at the entry of his PPoB and at every APoB.

Furnishing of Bank Details within 45 days (Rule 10A):-

- After a certificate of registration in Form GST Reg-06 has been made available on the common portal and GSTIN has been assigned, the registered person shall as soon as possible but not later than 45 days from the date of grant of registration furnish information with respect to details of Bank account or any other further information, as may be required on the common portal in order to comply with any other provision.

Penalty for not registering under GST:-

- He has not registered under GST although he is required to by law, Penalty will be:-

i. An offender not paying tax or making short-payments has to pay a penalty of 10% of the tax amount due, subject to a minimum of Rs.10000/-.

ii. Therefore, the penalty will be high at 100% of the tax amount when the offender has evaded i.e., where there is a deliberate fraud.

[1] States with Threshold limit of Rs.10 Lakhs for both Goods & Services: – Manipur; Mizoram; Nagaland; Tripura.

States with Threshold limit of Rs.20 Lakhs for both Goods & Services:- Arunachal Pradesh; Meghalaya; Sikkim; Uttarakhand; Pondicherry; Telangana

States with Threshold limit of Rs.20 Lakhs for Services & Rs.40 Lakhs for Exclusive supply Goods: – J&K; Assam; Andhra Pradesh and all Other States.