Introduction of QRMP Scheme

The Central Board of Indirect Taxes & Customs (CBIC) introduced Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme under Goods and Services Tax (GST) to help small taxpayers whose turnover is less than Rs.5 crores. The QRMP scheme allows the taxpayers to file GSTR-3B on a quarterly basis and pay tax every month.

Migration into QRMP Scheme

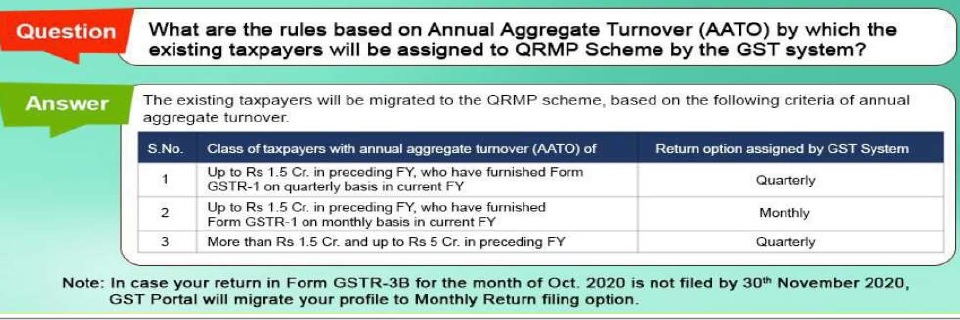

Automatic migration into QRMP scheme of existing taxpayers

Who can opt for QRMP Scheme?

Let ’s see the eligibility

How to opt in for the scheme?

How to opt in the scheme?

- Taxpayer can opt out from the GST portal GST.GOV.IN > Services > Returns > Opt-in for Quarterly Return option to opt in or opt out of the QRMP scheme.

- Option to exercise the scheme will be available throughout the year.

- Can opt in for any quarter from first day of second month of preceding quarter to the last day of first month of quarter for which want to opt for the scheme.

- Example: If a taxpayer wants to opt in for January to March quarter can exercise option during 1st November to 31st January.

- Taxpayer have option to avail the scheme GSTIN Wise i.e. Some GSTINs for a PAN can opt in and other can opt out.

- Option once exercised shall be valid for succeeding quarters also.

Option to opt-in/opt-out of the scheme

| S No | Quarter of a particular year | QRMP Scheme can be opted in or opted out during |

| 1. | Q1 (April – May – June) | 1st February’ to 30th April’ |

| 2. | Q2 (July – August – September) | 1st May’ to 31st July’ |

| 3. | Q3 (October – November – December) | 1st August’ to 31st October’ |

| 4. | Q4 (January – February – March) | 1st November’ to 31st January of next year |

For More details on opting in and out of the scheme , please refer the manual provided by GST portal

https://tutorial.gst.gov.in/userguide/ret urns/manual_change_profile.htm

Returns to be filed under QRMP

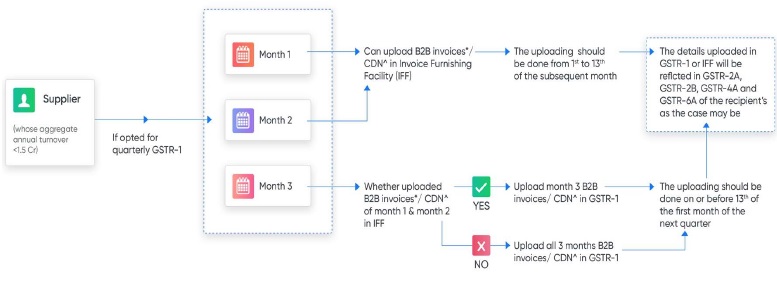

Information Furnishing Facility (IFF)

Information Furnishing Facility

⇒ The registered persons opting for this scheme can furnish the details of outward supplies using the Invoice Furnishing Facility (IFF). It can’t be furnished after 13th of month succeeding the quarter

⇒ Such IFF details shall reflect in GSTR-2A and GSTR-2B of the recipient.

⇒ The details of outward supplies furnished using the IFF, for the first and second months of a quarter, shall not be furnished in FORM GSTR-1 for the said quarter.

⇒ IFF is an optional facility and attracts no late fees/penalty.

Summary of IFF

Monthly Payment of Taxes

The registered person under the QRMP Scheme would be required to pay the tax due in each of the first two months of the quarter by depositing the due amount in Form GST PMT-06.

The amount shall be deposited by the 25th day of next month.

The amount deposited by the registered person in the first two months shall be debited solely for the purposes of offsetting the liability furnished in that quarter’s Form GSTR-3B.

Options for Monthly Payment of Taxes

| Method

|

Amount of Tax to be Paid Actual Liability in Form GST PMT-06 Differs with the

|

Interest in Case Amount of Tax to be Paid Actual Liability in Form GST PMT-06 Differs with thei Tax Payment

|

Late Fees |

| Fixed Sum Method

|

a) If the last return is furnished quarterly, an amount equivalent to 35% of the tax liability paid for the previous quarter shall be paid

b) If the last return is furnished monthly, the tax liability paid in the return for the previous month shall be paid |

No interest would be required to be paid, provided tax is paid by the due date

|

No late fee would be applicable on delay in payment of tax using Form PMT-06

|

| Self-Assessment Method

|

The persons can pay the tax due by considering the tax liability on inward and outward supplies and the input tax credit available.

|

Interest would be applicable

|

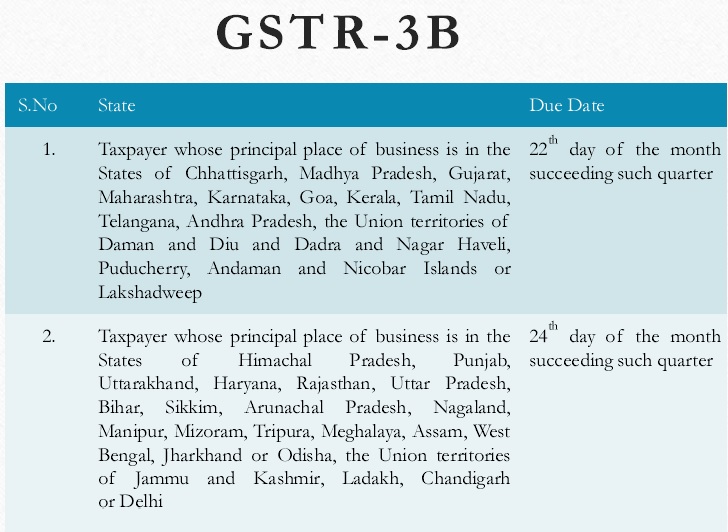

Due Date for Quarterly filing of Returns

GSTR -1 – 13th of the Month Succeeding the Quarter

GSTR -3B

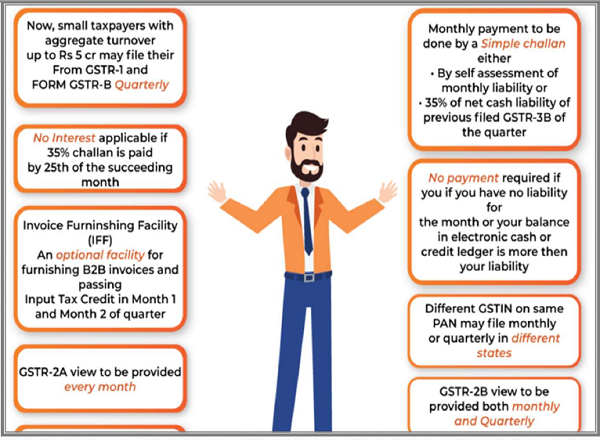

Summary of QRMP Scheme

Benefits of the QRMP Scheme

> Compliance burden of the taxpayer has reduced significantly.

> Taxpayers needs to file only 4 GSTR-3B returns instead of 12 GSTR-3B returns in a year.

> Taxpayers would be required to file only 4 GSTR-1 returns since Invoice Filing Facility (IFF) is provided under this scheme.

> Furnish invoice details in IFF depending upon the requirement of their recipient, for first two months of the quarter. The remaining invoice details can be furnished in the quarterly GSTR-1.

> Pay monthly tax conveniently using Fixed Sum Method (Pre-filled Challan) or Self-Assessment Method (actual tax due after adjusting ITC) in first two months of a Quarter

> Easily opt in and opt out of the Scheme

Author Bio