1. INTRODUCTION

1.1 This Chapter provides the scope and extent of GST, for better understanding of the tax structure under the GST law. The topics covered in this Chapter provide the general idea of the taxation policy and the authority of law, which will aid in the daily working of departmental officers.

1.2 The provisions of CGST Act, 2017 and CGST Rules, 2017, relevant to this Chapter are as under–

| Sr. No. Section/Rule Provision pertaining to | ||

| 1 | Section 7 | Scope of supply |

| 2 | Section 9 | Levy of CGST |

| 3 | Section 9(3) and 9(4) | Reverse Charge Levy |

| 4 | Section 10 | Composition Levy |

| 5 | Rule 3 | Intimation of Composition levy |

| 6 | Rule 4 | Effective date for Composition levy |

| 7 | Rule 5 | Conditions and restrictions for Composition levy |

| 8 | Rule 6 | Validity of Composition levy |

| 9 | Rule 7 | Rate of tax of the Composition levy |

| 10 | Section 11 | Power of Government to exempt |

| 11 | Section 12 | Time of Supply of goods |

| 12 | Section 13 | Time of Supply of services |

| 13 | Section 15 | Valuation of supply of goods and services |

| 14 | Rule 27 | Value of supply of goods where the consideration is not wholly in money |

| 15 | Rule 28 | Valuation of supply between related and distinct persons |

| 16 | Rule 29 | Value of supply of goods made or received through an agent |

| 17 | Rule 30 | Valuation of supply on cost basis |

| 18 | Rule 31 | Residual method of valuation |

| 19 | Rule 31A | Value of supply in case of lottery, betting, gambling and horse racing |

| 20 | Rule 32 | Determination of value in certain circumstances |

| 21 | Rule 32A | Value of supply of services where Kerala Flood Cess is applicable |

| 22 | Rule 33 | Value of supply of services in case of Pure Agent |

| 23 | Rule 34 | Rate of exchange of currency, other than Indian Rupees, for determination of value |

| 24 | Rule 35 | Value of supply inclusive of Integrated tax, Central tax, State tax, Union Territory tax |

| 25 | Section 31 | Tax Invoice |

| 26 | Rule 46 | Tax Invoice |

| 27 | Rule 46A | Invoice-cum-bill of supply |

| 28 | Rule 47 | Time limit for issuing tax invoice |

| 29 | Rule 48 | Manner of issuing invoice |

| 30 | Rule 50 | Receipt Voucher |

| 31 | Rule 51 | Refund Voucher |

| 32 | Rule 52 | Payment Voucher |

| 33 | Rule 53 | Revised tax invoice and credit and debit notes |

| 34 | Rule 54 | Tax invoice in special cases |

| 35 | Rule 55 | Transportation of goods without issue of invoice |

| 36 | Rule 55A | Tax invoice or bill of supply to accompany transport of goods |

| 37 | Section 16 | Input Tax Credit |

| 38 | Rule 36 | Documentary requirements and conditions for claiming input tax credit |

| 39 | Rule 37 | Reversal of input tax credit in the case of non-payment of consideration |

| 40 | Rule 38 | Claim of credit by a banking company or a financial institution |

| 41 | Rule 40 | Manner of claiming input tax credit in special circumstances |

| 42 | Rule 41 | Transfer of credit on sale, merger, amalgamation, lease or transfer of a business |

| 43 | Rule 41A | Transfer of credit on obtaining separate registration for multiple places of business within a State or Union Territory |

| 44 | Section 17 | Apportionment of credit and blocked credits |

| 45 | Rule 42 | Manner of determination of input tax credit in respect of inputs and input services and reversal thereof |

| 46 | Rule 43 | Manner of determination of input tax credit in respect of capital goods and reversal thereof |

| 47 | Section 18 | Availability of credit in special circumstances |

| 48 | Rule 44 | Manner of reversal of credit under special circumstances |

| 49 | Rule 44A | Manner of reversal of credit of Additional duty of Customs in respect of Gold dore bar |

| 50 | Section 19 | Taking input tax credit in respect of inputs and capital goods sent for job work |

| 51 | Rule 45 | Conditions and restrictions in respect of inputs and capital goods sent to the job worker |

| 52 | Section 20 | Manner of distribution of Input Tax Credit by Input Service Distributor (ISD) |

| 53 | Section 21 | Manner of recovery of credit distributed in excess |

| 54 | Rule 39 | Procedure for distribution of input tax credit by Input Service Distributor |

| 55 | Section 49 | Payment of tax, interest, penalty, etc. |

| 56 | Rule 85 | Electronic Liability Register |

| 57 | Rule 86 | Electronic Credit Ledger |

| 58 | Rule 86A | Conditions of use of amount available in electronic credit ledger |

| 59 | Rule 87 | Electronic Cash Ledger |

| 60 | Rule 88 | Identification number for each transaction |

| 61 | Rule 88A | Order of utilization of input tax credit |

| 62 | Section 51 | Tax Deducted at Source (TDS) under GST |

| 63 | Section 52 | Tax Collected at Source (TCS) under GST |

| 64 | Rule 138 | Information to be furnished prior to commencement of movement of goods and generation of e-way bill |

| 65 | Rule 138A | Documents and devices to be carried by a person-in-charge of a conveyance |

| 66 | Rule 138B | Verification of documents and conveyances |

| 67 | Rule 138C | Inspection and verification of goods |

| 68 | Rule 138D | Facility for uploading information regarding detention of vehicle |

| 69 | Rule 138E | Restriction on furnishing of information in Part A of FORM GST EWB-01 |

| 70 | Section 6 | Cross Empowerment |

The relevant Provisions, Forms, Circulars, Notifications, etc., wherever mentioned, can be seen by clicking ctrl+click on the respective hyperlink, which will open the https://taxinformation.cbic.gov.in page. On clicking GST option on the menu bar, ‘Information-GST’ page will appear, below which the option of Act, Rules, Forms, Notification, etc. is provided. The required page of the relevant Provisions/Forms/Circulars/Notifications can be seen by clicking the appropriate option.

1.4 Goods and Services Tax (hereinafter referred to as “GST”), introduced in India with effect from 01.07. 2017, is a comprehensive destination based indirect Value Added Tax on supply of goods as well as services.

1.5 Prior to introduction of GST, both Centre and States were empowered to impose indirect taxes on goods. Centre was imposing Central Excise duty on manufacture of goods and States were imposing Sales tax/VAT on sale of goods. Besides goods, services were also being subjected to Service tax, which only Centre could levy.

1.6 The idea of ‘one tax for entire nation’ was conceptualized and an Empowered Committee of State Finance Ministers was formed to design the road map for GST. The Empowered Committee recommended dual GST model for the country, under which GST had two components, viz. the Central GST (CGST) to be levied and collected by Centre and State GST (SGST) to be levied and collected by the respective States, subsuming most of the indirect taxes being levied. For Inter-State transactions (supplies from one State to another State) an Integrated GST (IGST) to be levied by Centre was recommended.

1.7 GST being a uniform tax system for the entire country, required constitutional amendment. As such Bill in this regard was introduced in both the Houses of Parliament. After the Bills were passed by both the Houses, the Bill received assent from the President of India on 08.09.2016 and also notified on the same day as The Constitution (One Hundred and First Amendment) Act, 2016.

1.8 The structure of GST is such that the Central Government and the State Governments have framed GST laws together. Some of the features include –

(a) Uniform law across the country: The GST law is based on the Model GST law drafted by the Centre and the States. Therefore, the law is more or less identical throughout the country.

(b) Common Procedures: The procedures and formats as prescribed by the CGST and the SGST are identical.

(c) Common Compliance Mechanism: GSTN, promoted jointly by the Central and State Governments, is the common compliance portal for GST.

1.9 The aim of GST was tax integration, tax simplification, promotion of Ease of Doing Business and to instill the feeling of ‘One nation, One tax’.

1.10 A new Article 279A was inserted in the Constitution of India, which prescribes constitution of a ‘GST Council’ for making recommendations on the governance of entire law relating to GST Act.

1.11 Broad meaning of the terms used frequently in this handbook is as under –

- ‘Central Tax’ means tax levied under the CGST Act, 2017.

- ‘State Tax’ means tax levied under the SGST Act, 2017.

- ‘Integrated Tax’ means tax levied under the IGST Act, 2017.

- ‘Union Territory Tax’ means tax levied under the UTGST Act, 2017.

- ‘Assessment’ means determination of tax liability under the CGST Act, 2017.

- ‘Common Portal’ means the common Goods and Services Tax Electronic Portal.

- ‘Composite Supply’ means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business. One taxable supply will be a principal supply (predominant element).

- ‘Consideration’ means any payment made or to be made by the recipient or any other person, either in money or otherwise for the supply of goods and/or services and the monetary value of any act or forbearance for the supply of goods and/or services.

- ‘exempt supply’ means supply of any goods and/or services which attracts ‘nil’ rate of tax or wholly exempt or non-taxable.

- ‘Input’ means any goods other than capital goods used or intended to be used by the supplier in the course of furtherance of business.

- ‘Input service’ means any service used or intended to be used by the supplier in the course of furtherance of business.

- ‘Input Tax’ means the Central Tax, State Tax, Integrated Tax or Union Territory tax charged on any supply of gooods and/or services made to a person.

- ‘Inward supply’ means receipt of goods and/or services by purchase or acquisition or any other means.

- ‘Mixed supply’ means two or more individual supplies of goods or services or any combination thereof, made in conjunction with each other for a single price.

- ‘Output tax’ means the tax chargeable on taxable supply of goods and/or services. Output tax does not include the tax payable under Reverse Charge basis.

- ‘Outward supply’ means supply of goods and/or services by way of sale, transfer, barter, exchange, licence, rental, lease or disposal or any other mode, made or agreed to be made by a person in the course of furtherance of business.

- ‘Recipient’ of supply of goods and/or services means the person who is liable to pay consideration or the person to whom the goods are delivered or to whom the possession or use of the goods is given or the person to whom the service is rendered.

- ‘Registered person’ means a person registered under the CGST Act, 2017.

- ‘Reverse Charge’ means the liability to pay tax by the recipient of supply of goods and/or services instead of the supplier of such goods and/or services.

- ‘Taxable Supply’ means supply of goods or services or both, leviable to tax under the CGST Act, 2017.

- ‘Taxable person’ means a person who is registered or liable to register under the CGST Act, 2017.

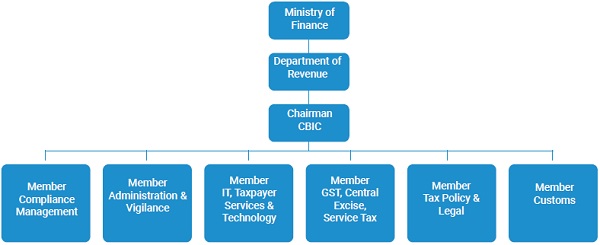

2. CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

2.1. Central Board of Indirect Taxes and Customs (CBIC) is a part of the Department of Revenue under Ministry of Finance, Government of India. It deals with the tasks of formulation of policy concerning levy and collection of Customs, Central Excise duties, Central Goods & Services Tax and IGST, prevention of smuggling and administration of matters relating to Customs, Central Excise, Central Goods & Services Tax, IGST and Narcotics to the extent under CBIC’s purview. CBIC also acts as a regulator with respect to the “dealers in precious metals and precious stones” and “real estate agents” and related matters under Prevention of Money Laundering Act, 2002.

2.2. The Board is the administrative authority for its subordinate organizations, including Custom Houses, Central Excise and Central GST Commissionerates and the Central Revenues Control Laboratory. CBIC administers all the Indirect Tax related matters in India. GST in totality comes under the purview of this Board.

2.3. The CBIC is also charged with creating guidelines for the imposition and collection of Central Excise Duties, Customs, IGST, Central Goods and Services Tax (CGST).

2.4. The CBIC plays a crucial role in enforcing compliance with GST laws. This includes conducting investigations, inspections, and raids to detect and prevent tax evasion. In addition to enforcing compliance, the CBIC also provides support and guidance to taxpayers. This includes providing information on GST laws and procedures, and answering queries and concerns of taxpayers.

2.5. The CBIC maintains a GST portal, which is a digital platform for taxpayers to file GST returns and make tax payments.

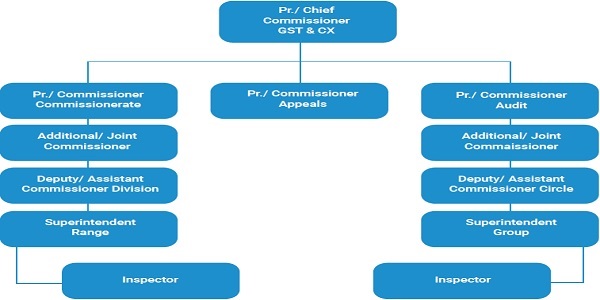

2.6. The CBIC is headed by Chairman and has 6 members in addition to the Chairman. In the performance of its administrative and executive functions, the CBIC is assisted by Principal Chief Commissioners/Chief Commissioners and Principal Director Generals/Director Generals. The Principal Commissioners/ Commissioners working under the Principal Chief Commissioner/ Chief Commissioner’s supervision also discharge executive functions.

Organisational Chart of CBIC

All Members have supervisory control on the Zones and Directorates

Organisational chart at Zonal level

3. GST COUNCIL

3.1. GST Council is a constitutional body, consisting of representatives from both Union and State Governments. It consists of the Union Finance Minister as the Chairperson, Minister of State for Finance (Revenue) as Member and the Minister in-charge of Tax or Finance or any nominated Minister of the State as Member.

3.2. The GST Council is supported by the GST Council Secretariat and headed by the Revenue Secretary.

3.3. The purpose of GST Council is to act as a converging platform for the Union and the State Governments for them to work in a harmonious manner towards a common goal. The GST Council takes decisions in the periodical GST Council Meetings, which are then communicated to the Centre and the State in the form of recommendations. The minutes of GST Council meetings are published in the official website https://gstcouncil.gov.in.

3.4. The aim of the GST Council is to carry out its function in a consensual and harmonious manner with respect to formulation and implementation of GST Law across the country.

3.5. The GST Council is empowered to make recommendations to the Union and the State Governments on –

- the taxes, cesses and surcharges levied by the Union, the States and the Local Bodies (like Municipal Corporation/Council, Panchayats, etc.) which may be subsumed in the GST;

- the goods and services that may be subjected to or exempted from the GST;

- model GST laws, principles of levy, apportionment of GST levied on supplies in the course of inter-State trade or commerce and the principles that govern the place of supply;

- the threshold limit of turnover below which goods and services may be exempted from GST;

- the rates including floor rates with bands of GST;

- any special rate or rates for a specified period, to raise additional resources during any natural calamity or disaster;

- special provision with respect to the States of Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand;

- any other matter relating to the GST, as the Council may decide;

- the date on which the GST be levied on Petroleum Crude, High Speed Diesel, Motor Spirit (Petrol), Natural Gas and Aviation Turbine Fuel.

4. GOODS AND SERVICE TAX NETWORK (GSTN)

4.1. GSTN is a Special Purpose Vehicle and has been set up to cater to the needs of GST. It is an interface between the Government and the taxpayers. The GSTN provides a shared Information Technology (IT) infrastructure and services to Central and State Governments, taxpayers and other stakeholders for implementation of GST. The functions of the GSTN include:

(i) Facilitating registration;

(ii) Return filing and processing and forwarding the returns to Central and State authorities;

(iii) Computation and settlement of IGST;

(iv) Matching of tax payment details with banking network;

(v) Providing various MIS reports to the Central and the State Governments based on the taxpayer return information, need based information and business intelligence;

(vi) Providing analysis of taxpayers’ profile;

(vii) Payment management, including payment Gateways and integration with banking systems;

(viii) Taxpayer management, including account management, notifications, information, and status tracking;

(ix) Tax authority account and ledger Management;

(x) Processing and reconciliation of GST on import and integration with EDI systems of Customs;

(xi) Maintenance of interfaces between the Common GST Portal and tax administration systems;

(xii) Provide training to stakeholders;

(xiii) Carry out research and study best practices.

4.2. The following functions can be performed by taxpayers through GST Common Portal:

(i) Application for registration as well as amendment in registration, cancellation of registration and profile management;

(ii) Creation of Challan for payment of taxes, including penalties, fines, interest, etc.;

(iii) Change of status of a taxpayer from normal to Compounding and vice-versa;

(iv) Uploading of Invoice data & filing of various statutory returns/Annual statements;

(v) Track status of return/tax ledger/cash ledger etc. using unique Application Reference Number (ARN) generated on GST Portal;\

(vi) File application for refund, appeal, advance ruling etc.;

(vii) Status review of return/tax ledger/cash ledger;

(viii) Generation of E-way bill.

(ix) Generation of E-invoice by taxpayers with Annual Turnover of more than 5 crores.

4.3 The officers use information/application submitted by taxpayer on GST Portal for following statutory functions:

(i) Approval/rejection for enrollment/registration of taxpayers;

(ii) Tax administration (Assessment/Audit/Refund/ Appeal/Investigation etc.);

(iii) Business Analytics, MIS and other statutory functions.

4.4. The following are some of the features of the GSTN-BO (Back Office) in the GST Portal for the CGST Tax Officers:

- In addition to the Modules relating to Registration, Refund, Scrutiny of Returns, Enforcement, Show Cause Notice & Adjudication and Recovery on GST Portal, various Modules would be available on BO for Pending actions, wherein the Officer gets the task-list against each Module. These Modules are available depending upon the roles assigned to the Officer.

- Hyperlinks would be available for each Pending action, wherein the Officer gets the list of ARNs for action. The task-list gives the total count as well as critical count of number of days available for completion of task.

- The Officer can also view the Taxpayer Profile on BO, wherein he can see all data of taxpayer, in the same manner in which a Taxpayer views his data.

- List of taxpayers, who have not added Bank details is displayed. This will help the Officer to initiate action for suo-moto cancellation of registration after following the due process.

- List of Defaulters would be available on the BO dashboard, which will help in timely issuance of Notice to Return Defaulters (GSTR-3A).

- The Hyperlinks provided in BO will assist to view the Electronic Cash Ledger, Electronic Credit ledger, Electronic Liability Register (Related to Return), Electronic Liability Register (not related to Return) and Negative Liability Statement.

- Records of Returns filed by the Taxpayers would be available on the Dashboard, helping the Officer to view Tax Liability and ITC comparison (GSTR-1, GSTR-3B and GSTR-2A/2B).

- The Officers can view on Dashboard the List assigned to him, the List assigned from his Desk to other Officer and the List assigned to him from other Officer’s Desk, through the links provided therein. In case of non-availability of an Officer to complete a task, the facility to re-assign such task to other Officer is also available. Work items can also be re-assigned to other Officer in the Role of re-assign cases.

5. SALIENT FEATURES OF GST

5.1. GOODS AND SERVICES TAX (GST) LEVY.

5.1.1 GST is a dual levy with the Centre and States simultaneously levying it on a common tax base. The GST levied and administered by the Centre on intra-State (within a State) supply of goods and/or services is called the Central GST (CGST) and that levied by the States/Union territory is called the State GST (SGST)/UTGST. Similarly, Integrated GST (IGST) is levied and administered by Centre on every inter-state (from one State to another State) supply of goods and services.

5.1.2. The CGST and the SGST is levied simultaneously on every transaction of supply of goods and services made by registered persons, except the exempted goods and services, goods and services which are outside the purview of GST. Further, both are levied on the same price or value.

Illustration I: The rate of CGST is 9% and that of SGST is 9%. When a wholesale dealer of steel in Uttar Pradesh supplies steel bars and rods to a construction company located within the same State for Rs. 100/-, the dealer would charge CGST of Rs. 9/- and SGST of Rs. 9/-, in addition to the basic price of the goods. He would be required to deposit Rs. 9/- as CGST component, which will go into the credit of Central Government account and Rs. 9/- as the SGST component, which will go into the credit of the concerned State Government, i.e. Uttar Pradesh here.

Illustration II: An advertising company located in Mumbai supplies advertising services to a company manufacturing soap also located within the State of Maharashtra for Rs. 100/-. The tax rate for the said service is 9% CGST and 9% SGST. The ad company would charge CGST of Rs. 9/- and SGST of Rs. 9/- to the basic value of the service. He would be required to deposit Rs. 9/- as the CGST component, which will go into the Central Government account and Rs. 9/- as the SGST component which will go into the account of the concerned State Government, i.e. Maharashtra.

Illustration III: The rate of CGST is 9% and that of SGST is 9%. When a wholesale dealer of Chemicals in Karnataka supplies his goods to a company located in Telangana for Rs. 100/-. As this is an inter-State supply, the dealer would charge IGST of Rs. 18/-, in addition to the basic price of the goods. He would be required to deposit Rs. 18/- as IGST which will go into the credit of Central Government account. The tax amount shall be apportioned between the Central Government and the State Government in the prescribed manner.

5.1.3. The following taxes/duties levied by the Central Government and State Government have been subsumed under GST –

(i) Taxes levied and collected by the Centre:

(a) Central Excise duty

(b) Duties of Excise (Medicinal and Toilet Preparations)

(c) Additional Duties of Excise (Goods of Special Importance)

(d) Additional Duties of Excise (Textiles and Textile Products)

(e) Additional Duties of Customs (commonly known as CVD)

(f) Special Additional Duty of Customs (SAD)

(g) Service Tax

(h) Central Surcharges and Cesses so far as they relate to supply of goods and services.

(ii) Taxes levied and collected by the States:

(a) State VAT

(b) Central Sales Tax

(c) Luxury Tax

(d) Entry Tax (all forms)

(e) Entertainment and Amusement Tax (except when levied by the local bodies)

(f) Taxes on advertisements

(g) Purchase Tax

(h) Taxes on lotteries, betting and gambling

(i) State Surcharges and Cesses so far as they relate to supply of goods and services.

5.1.4. GST is a tax levied on all types of supply of goods or services or both, made for a consideration and is for the purpose of business or furtherance of business.

5.1.5. The different types of supplies are –

(i) Taxable supply – Supply of goods or services or both which is leviable to GST.

(ii) Exempt supply – Supply of goods or services or both which attracts nil rate of tax or which is wholly exempt from tax or is non-taxable supply.

(iii) Inter-State supplies – Where the location of the supplier and the place of supply is in different states.

(iv) Intra-State supplies – Where the location of the supplier and the place of supply is in same state.

(v) Composite supplies – Supplies consisting of two or more taxable supplies of goods or services or both, or any combination thereof.

(vi) Mixed supplies – Two or more individual supplies of goods or services, or any combination thereof, made in combination with each other for a single price.

(vii) Zero rated supplies – The following supplies of goods and/or services are ‘zero rate supplies’–

(a) export of goods and/or services; or

(b) supply of goods and/or services to a Special Economic Zone (SEZ) Developer or a Special Economic Zone (SEZ) Unit.

Under zero rating of supplies, the outward supplies as well as the inputs or input services used in supplying the supplies are free of GST. Meaning, the taxes paid on the supplies which are zero rated are refunded, the credit of inputs/ input services is allowed and wherever the supplies are exempted, or the supplies are made without payment of tax, the taxes paid on the inputs or input services i.e. the unutilised input tax credit is refunded.

5.1.6 Goods and Services tax (GST) is a destination based tax, levied as per Section 9 of the CGST Act, 2017. It is levied at all stages right from manufacture up to final consumption with credit of taxes paid at previous stages available as setoff, called as Input Tax Credit (ITC). In other words, only value addition will be taxed and burden of tax is to be borne by the final consumer. (Section 9 of CGST Act, 2017)

5.1.7 As per Section 7 of the CGST Act, 2017, the term ‘supply’ covers all forms of supply of goods or services or both that includes sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. It also includes import of service. (Section 7 of CGST Act, 2017)

5.1.8 There are some transactions which do not meet the aforesaid two conditions of supply i.e consideration and for furtherance of business, but still such transactions are considered as supply of goods and/or services. For example, permanent sale or disposal of business assets, supply to related person (defined in Section 15 of CGST Act, 2017) or distinct person (Two or more units/firms holding different GST registrations in India associated with a single PAN, whether located in India or outside India), inter-State stock transfer of goods without consideration or import of services by a person from a related person or any of his other establishments located outside India in the course or furtherance of business. (Section 15 of CGST Act, 2017)

5.1.9 The types of transaction/activities to be treated as deemed supply even if made without consideration and on which GST is levied, are covered in SCHEDULE I, which are as under –

1) Permanent transfer or disposal of business assets where input tax credit has been availed on such assets.

2) Supply of goods or services or both between related persons or between distinct persons (Individuals with distinct GST Identification Numbers (GSTINs) associated with a single legal entity (single PAN), whether located within the same state, across two different states, or in a different country), when made in the course or furtherance of business:

Provided that gifts not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as supply of goods or services or both.

3) Supply of goods—

(a) by a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

(b) by an agent to his principal where the agent undertakes to receive such goods on behalf of the principal.

4) Import of services by a person from a related person or from any of his other establishments outside India, in the course or furtherance of business.

5.1.10. Certain activities/transactions where there is a likelihood of a dispute whether it is to be treated as supply of goods or supply of services, are categorically classified in SCHEDULE II, which are as under –

1) Transfer-

(a) any transfer of the title in goods is a supply of goods;

(b) any transfer of right in goods or of undivided share in goods without the transfer of title thereof, is a supply of services;

(c) any transfer of title in goods under an agreement which stipulates that property in goods shall pass at a future date upon payment of full consideration as agreed, is a supply of goods.

2) Land and Building-

(a) any lease, tenancy, easement, licence to occupy land is a supply of services;

(b) any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly, is a supply of services.

3) Any treatment or process which is applied to another person’s goods is a supply of services.

4) Transfer of business assets-

(a) where goods forming part of the assets of a business are transferred or disposed of by or under the directions of the person carrying on the business so as no longer to form part of those assets, such transfer or disposal is a supply of goods by the person;

(b) where, by or under the direction of a person carrying on a business, goods held or used for the purposes of the business are put to any private use or are used, or made available to any person for use, for any purpose other than a purpose of the business, the usage or making available of such goods is a supply of services;

(c) where any person ceases to be a taxable person, any goods forming part of the assets of any business carried on by him shall be deemed to be supplied by him in the course or furtherance of his business immediately before he ceases to be a taxable person, unless—

(i) the business is transferred as a going concern to another person; or

(ii) the business is carried on by a personal representative who is deemed to be a taxable person.

5) Supply of services-

The following shall be treated as supply of services, namely:

(a) renting of immovable property;

(b) construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

(c) temporary transfer or permitting the use or enjoyment of any intellectual property right;

(d) development, design, programming, customisation, adaptation, upgradation, enhancement, implementation of information technology software;

(e) agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act; and

(f) transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration.

6) Composite supply-

The following composite supplies shall be treated as a supply of services, namely:—

(a) works contract as defined in clause (119) of section 2; and

(b) supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption), where such supply or service is for cash, deferred payment or other valuable consideration.

5.1.11 SCHEDULE III contains the list of activities/transactions which shall be treated neither as a supply of goods nor a supply of services, i.e. the Negative List supplies. Details of activities/transactions are as under –

(1) Services by an employee to the employer in the course of or in relation to his employment.

(2) Services by any court or Tribunal established under any law for the time being in force.

(3) (a) the functions performed by the Members of Parliament, Members of State Legislature, Members of Panchayats, Members of Municipalities and Members of other local authorities;

(b) the duties performed by any person who holds any post in pursuance of the provisions of the Constitution in that capacity; or

(c) the duties performed by any person as a Chairperson or a Member or a Director in a body established by the Central Government or a State Government or local authority and who is not deemed as an employee before the commencement of this clause.

(4) Services of funeral, burial, crematorium or mortuary including transportation of the deceased.

(5) Sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building.

(6) Actionable claims, other than “specified actionable claims”

(7) Supply of goods from a place in the non-taxable territory to another place in the non-taxable territory without such goods entering into India.

(8) (a) Supply of warehoused goods to any person before clearance for home consumption;

(b) Supply of goods by the consignee to any other person, by endorsement of documents of title to the goods, after the goods have been dispatched from the port of origin located outside India but before clearance for home consumption.”

5.1.12. Alcohol for human consumption is kept out of GST. Further, petroleum products viz. Petroleum Crude, Motor Spirit (Petrol), High Speed Diesel, Natural Gas and Aviation Turbine Fuel have temporarily been kept out. These commodities are presently subjected to Central Excise duty and VAT. GST Council shall decide the date from which they shall be included in GST.

5.1.13. Tobacco and tobacco products is leviable to GST. In addition, the Centre has the power to levy Central Excise duty on these products.

5.2. METHODS OF GST LEVY

5.2.1. There are three methods of GST levy –

(i) Normal levy – The CGST and the SGST is levied simultaneously at the applicable rate on every transaction

of supply of goods and services made by registered persons in the normal course of business. In the case of intra-state sales, Central GST and State GST are charged. All the inter-state sales are chargeable to the Integrated GST. The tax payment is on monthly basis and the taxpayer has to comply with all the prescribed provisions and procedures.

(ii) Composition levy – Composition levy scheme is a simple compliance scheme for small taxpayers with annual aggregate turnover not exceeding Rs. 1.50 Crore (Rs. 75 lakhs for Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Uttarakhand) in goods (including upto 10% value of services) during the previous financial year. As per Notification No. 2/2019-CT (Rate), dated 07.03.2019, for service provider the turnover should not exceed Rs. 50 lakhs during the previous financial year and such supplier is not engaged in making any inter-State outward supply, who is neither a casual taxable person nor a non-resident taxable person, who is not engaged in making any supply through an electronic commerce operator. It is a voluntary and optional scheme. Under the Composition scheme the eligible manufacturer has to pay 1% (0.5% CGST + 0.5% SGST/ UTGST) of turnover, the eligible service providers (or goods and service suppliers) have to pay 6% (3% CGST + 3% SGST / UTGST) of turnover; the eligible supplier of Restaurant Services has to pay 5% (2.5% CGST + 2.5% SGST/UTGST) of turnover and the traders have to pay 1% (0.5% CGST + 0.5% SGST/UTGST) of the taxable turnover.

(iii) Levy under Reverse Charge Mechanism – In normal circumstances, the tax is payable on outward supplies, to be paid by the supplier of goods and/or services. However, in case of certain notified supply of goods and services, including imported goods and services, the tax is required to be paid on the inward supplies by the recipient of such goods and services instead of the supplier of such goods or services. All the provisions of the CGST Act, 2017 shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods and/or services.

5.2.2 The provisions and procedures in detail in respect of the above mentioned methods of levy are explained separately in this Chapter as well as other Chapters.

5.3 COMPOSITION LEVY

5.3.1. The Composition Levy is an alternative method of levy of tax for small taxpayers whose turnover is up to the prescribed limit. To be eligible to opt for Composition levy, the turnover limit presently prescribed for the manufacturer should not exceed Rs. 1.50 Crore (Rs. 75 lakhs for Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Uttarakhand) and that for the service provider should not exceed Rs. 50 lakhs during the previous financial year.

5.3.2 The scheme is optional. The option for Composition Levy has to be given electronically in FORM GST CMP-02, prior to the commencement of the financial year for which the option is exercised.

5.3.3 The taxpayer has to declare the stock of inputs and inputs contained in semi-finished or finished goods held in stock by him on the preceding date on which the Composition Levy starts and has to pay an amount equal to the input tax credit in respect of such stocks. The ITC on inputs shall be calculated proportionately on the basis of corresponding invoices on which credit had been availed by the taxpayer on such inputs. In respect of capital goods held in stock, the input tax credit involved in the remaining useful life in months shall be computed on pro-rata basis, taking the useful life as 5 years. The payment can be made by debiting electronic credit ledger, if there is sufficient balance in the electronic credit ledger, or by debiting electronic cash ledger. If any balance remains in the electronic credit ledger, it would lapse. The taxpayer has to furnish the statement for intimation of Input Tax Credit in FORM GST ITC-03, within a period of sixty days from the commencement of the relevant financial year.

5.3.4. The following taxable persons are not eligible for the Composition Levy scheme:

(a) A casual taxable person – A person who occasionally undertakes supplies in a State or Union Territory where he has no fixed place of business;

(b) A Non-Resident Taxable Person – A person who occasionally undertakes supplies but has no fixed place of business or residence in India;

(c) A person engaged in providing inter-state (from one State to another) supply of goods and services or both;

(d) A person engaged in supply of non-taxable goods i.e. goods which are not taxable under GST law;

(e) A person engaged in supply of goods through an Electronic Commerce Operator (E-Commerce) who is required to collect Tax at source (TCS) under Section 52 of the CGST Act, 2017; (Section 52 of CGST Act, 2017)

(f) A person engaged in manufacturing of goods notified under Section 10(2)(e) of the CGST Act 2017, viz., Ice Cream and other edible Ice, Pan Masala, Aerated Water, Tobacco and manufactured Tobacco substitutes, Fly Ash Bricks, Fly Ash aggregates, Fly Ash Blocks, Brick Fossil Meals or similar Siliceous earthen building bricks and earthen or roofing tiles. (Section 10(2) (e) of CGST Act, 2017)

5.3.5. Section 10 of the CGST Act, 2017 is the charging section which provides for levying the tax at the prescribed rate on the turnover of the eligible taxpayers who have opted for Composition Levy scheme. The tax rates prescribed are (Section 10 of CGST Act, 2017) –

(a) An eligible manufacturer has to pay 1% (0.5% CGST + 0.5% SGST/ UTGST) of turnover in a state or Union Territory.

(b) All eligible service providers (or goods and service suppliers) have to pay 6% (3% CGST + 3% SGST / UTGST) of turnover in a State or Union Territory.

(c) An eligible person engaged in making supply of Restaurant Services [Supply of food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption)], has to pay 5% (2.5% CGST + 2.5% SGST/UTGST) of turnover in a state or Union Territory.

(d) All other eligible suppliers, i.e. traders, have to pay 1% (0.5% CGST + 0.5% SGST/UTGST) of the taxable turnover in a State or Union Territory.

5.3.6. The taxpayers who have opted for the Composition Levy Scheme have to file return in FORM GSTR-04 on annual basis and the tax has to be paid on quarterly basis before 18th of the month succeeding the quarter relating to supplies. The intimation of payment of tax has to be made electronically in FORM GST CMP 01.

5.3.7. The taxpayers who have opted for the Composition Levy Scheme cannot issue taxable invoice under GST law but has to issue bill of supply. He has to mention the words “Composition Taxable Person not eligible to collect tax on supplies” at the top of every bill of supply issued by him.

5.3.8. The Taxpayers who have opted for Composition Levy Scheme can neither collect GST from the customers nor can claim Input Tax Credit on the purchases. Also, the recipient of supply of goods and services from such taxpayers cannot claim Input Tax Credit on the tax paid on such supplies.

5.3.9. The option for Composition Levy shall lapse from the day on which the taxpayer’s aggregate turnover during the financial year exceeds the threshold limit. Once the taxpayer reaches the threshold limit, he shall file an intimation for withdrawal from the scheme in FORM GST CMP-04 within seven days of the occurrence of such event. After furnishing the said intimation, the taxpayer may electronically furnish on the common portal, a statement in FORM GST ITC-01 containing details of the stock of inputs and inputs contained in semi-finished or finished goods held in stock by him on the date on which the option is withdrawn, within a period of thirty days from the date from which the option is withdrawn.

5.3.10. The aggregate turnover shall be computed on the basis of turnover on all India basis, which shall be aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number, excluding Central tax, State tax, Union territory tax, integrated tax and cess.

5.3.11. If it is found that the taxpayer was not eligible to pay tax under Composition Scheme or has contravened the provisions of the Act or provisions of this Chapter, jurisdictional officer may issue a notice to such person in FORM GST CMP-05 to show cause within fifteen days of the receipt of such notice as to why the option to pay tax under this scheme shall not be denied. The taxpayer shall submit reply in FORM GST CMP-06. The proper officer shall issue an order in FORM GST CMP-07 within a period of thirty days of the receipt of such reply, either accepting the reply, or denying the option to pay tax under Composition scheme from the date of the option or from the date of the event concerning such contravention, as the case may be.

5.3.12. Consequent to an order of withdrawal of option in FORM GST CMP-07, the taxpayer may electronically furnish at the common portal, a statement in FORM GST ITC-01 containing details of the stock of inputs and inputs contained in semi-finished or finished goods held in stock by him on the date on which the option is denied, within a period of thirty days from the date of the order passed in FORM GST CMP-07 for availing Input Tax Credit on such stocks.

5.4. REVERSE CHARGE MECHANISM

5.4.1. Section 9(3) and 9(4) of the CGST Act, 2017 provide for levy of GST on reverse charge basis. That is, the liability to pay tax is on the recipient of the goods and services instead of the supplier of such goods or services, in respect of notified categories of supply. (Section 9(3) & 9(4) of CGST Act, 2017)

5.4.2 Normally, the supplier of goods or services is liable to pay GST. However, in specified cases like imports and other notified supplies, the liability may be cast on the recipient under the Reverse Charge Mechanism. For example –

(i) An agriculturist sells 100 kg Shelled Cashew Nuts to a GST registered person @ Rs. 200/- per kg. The total

value of the supply would be Rs. 20,000/-. Shelled Cashew Nuts sold by an Agriculturist directly to a GST registered person is notified under Notification No. 4/2017-CT (Rate), dated 28.06.2017, as amended, for payment of tax under Reverse Charge Mechanism (RCM). As such, the liability to pay tax in this case shifts to the recipient of such Cashew Nuts, i.e. the GST registered person. The applicable rate of tax on Cashew Nuts is 5%. Thus, the said GST registered person will pay tax of Rs. 1000/- (Rs. 500/- CGST + Rs. 500/-SGST) on such goods received.

(ii) A trader registered under GST takes services of Goods Transport Agency (GTA) for transportation of goods. The amount paid by the trader for transportation is Rs. 10,000/-. Transportation of goods service provided by GTA is notified under Notification No. 13/2017-CT (Rate), dated 28.06.2017 for payment of tax under the reverse charge mechanism. Therefore, the trader has to pay tax @ 5% on Rs. 10,000/-, i.e. Rs. 500/- (Rs. 250/- CGST + Rs. 250/- SGST).

(iii) In case transportation service is provided to passengers by a radio-taxi through e-commerce platform (aggregator), viz., Ola, Uber, etc., then in such cases the reverse charge will apply to the e-commerce operator and he will be liable to pay GST at the applicable rate.

5.4.3. As per Section 9(3) of CGST Act, 2017, the Government on the recommendations of the GST Council notifies the categories of supply of goods and/or services, the tax on which is required to be paid on reverse charge basis by the recipient of such goods and/or services. Section 9(4) of CGST Act, 2017 provides that in respect of the supply of taxable goods and/or services by unregistered supplier (who is not registered under GST), to a registered person, the tax shall be paid by the recipient on reverse charge basis.

5.4.4. All the provisions of the CGST Act, 2017 shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods and/or services.

5.4.5. Initially from 01.07.2017 to 12.10.2017, in terms of Notification No. 8/2017-CT (Rate) dated 28.06.2017 exemption from payment of tax on reverse charge basis was given if total value of the purchases in a day by a taxpayer from all unregistered persons was less than Rs. 5000/-. From 13.10.2017 to 31.01.2019 the exemption from payment of tax under reverse charge mechanism (RCM) on purchases from unregistered persons was extended till 31.09.2019 without any capping of value, vide various Notifications amending the said Notification No. 8/2017-CT (Rate) dated 28.06.2017.

5.4.6 However, by the amendment carried out in the Act through CGST (Amendment) Act, 2018, with effect from 01.02.2019 the RCM on purchases from unregistered persons was made applicable to only notified persons. Accordingly, vide Notification No. 07/2019-CT (Rate) dated 29.03.2019, the Builders and Promoters in Real Estate have been notified as persons liable to pay tax under reverse charge on the purchase of goods, viz., Cement and Capital Goods, and services or both which constitute the shortfall from the minimum value of goods or services or both required to be purchased by the promoter for construction of project, i.e. 80% of inputs and input services shall be purchased from the registered persons and on shortfall of purchases tax shall be paid by the builder on reverse charge basis.

5.4.7 In terms of Notification No. 09/2017-CT (Rate), dated 28.06.2017, Government entities who are TDS Deductors under Section 51 of CGST Act, 2017, need not pay GST under reverse charge in case of procurements from unregistered suppliers.

5.4.8 The recipient of goods and/or services making payment of tax under reverse charge has to issue invoice or payment voucher on goods and/or services received from a supplier.

5.4.9 The payment of tax under reverse charge is required to be made in cash only. The reason of this provision is that the definition of ‘output tax’ under Section 2(82) of CGST Act, 2017 categorically excludes tax payable under reverse charge basis and as per Section 49(4) of the CGST Act, 2017, the payment through the electronic credit ledger by utilizing the Input Tax Credit is allowed to be made towards output tax only. (Section 2(82) & 49(4) of CGST Act, 2017)

5.4.10. The taxpayer making payment under reverse charge is required to issue a self-invoice (invoice in his own name), which are required to be uploaded in GSTR-1 for taking Input Tax Credit.

5.4.11. The benefit of exemption from registration for the small scale suppliers with turnover less than the stipulated threshold limit, is not available if they are liable to pay tax under reverse charge. Such suppliers are compulsorily required to obtain registration, as provided in Section 24(iii) of the CGST Act, 2017. (Section 24(iii) of CGST Act, 2017)

5.4.12. The persons engaged only in supplying goods and/or services on which tax is liable to be paid under reverse charge basis by the recipient, is not required to obtain registration.

5.4.13. The registered taxpayer making payment under reverse charge can take input tax credit on the tax paid under reverse charge on the eligible goods and services after making the payment of tax.

5.4.14. The goods on which GST is payable on reverse charge basis, i.e. the tax is required to be paid by the GST registered recipient, notified in Notification No. 4/2017-CT (Rate), dated 28.06.2017, as amended, are as under-

(i) Cashew nuts not shelled or peeled, Bidi wrapper leaves (Tendu), Tobacco leaves and Raw cotton, purchased by any registered person from any Agriculturist;

(ii) Essential oils other than those of citrus fruit, namely, peppermint (Mentha piperita), other mints: Spearmint oil (ex-mentha spicata), Water mint-oil (ex-mentha aquatic), Horsemint oil (ex-mentha ylvestries), Bergament oil (ex-mentha citrate), supplied by unregistered person to registered person;

(iii) Silk Yarn, supplied by a person manufacturing silk yarn from raw silk or silk worm cocoons;

(iv) Lottery supplied by State Government, Union Territory or any local authority to Lottery distributor or selling agent;

(v) Used vehicles, seized and confiscated goods, old and used goods, waste and scrap supplied by Central Government, State Government, Union territory or a Local authority to any registered person;

(vi) Priority Sector Lending Certificate supplied by any registered person to any registered person.

5.4.15. The services on which GST is payable on reverse charge basis notified in Notification No. 13/2017-CT (Rate), dated 28.06.2017, are as under-

(i) Goods Transport Agency Services supplied by a Goods Transport Agency (GTA) in respect of transportation of goods by road to any factory, any registered society, any Cooperative society, any person registered under CGST/ IGST / SGST/or UTGST Act, any Body Corporate, any partnership firm, any casual taxable person located in the taxable territory.

(ii) Legal Services provided by an individual advocate or firm of advocates to any business entity located in the taxable territory.

(iii) Arbitral Services supplied by an arbitral Tribunal to a business entity located in the taxable territory.

(iv) Sponsorship Services provided by way of Sponsorship Service to any Body Corporate or partnership firm.

(v) Services supplied by the Central Government, State Government, Union territory or local authority to a business entity, excluding renting of immovable property service, services by the Department of posts, services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport and transport of goods or passengers.

(vi) Services supplied by the Central Government, State Government, Union territory or local authority by way of renting of immovable property to a person registered under CGST.

(vii) Services by way of renting of residential dwelling to a registered person.

(viii) Services supplied by any person by way of transfer of development rights or Floor Space Index (FSI) (including additional FSI) for construction of a project by a promoter.

(ix) Long term lease of land (30 years or more) by any person against consideration in the form of upfront amount (called as premium, salami, cost, price, development charges or by any other name) and/or periodic rent for construction of a project by a promoter.

(x) Services supplied by a Director of a company or a Body Corporate to the said company or the Body Corporate.

(xi) Services provided by an Insurance Agent to person carrying on insurance business.

(xii) Supply of Services by a music composer, photographer, artist or the like by way of transfer or permitting the use or enjoyment of copyright relating to original dramatic, musical or artistic works to a music company, producer or the like.

(xiii) Supply of services by an author by way of transfer or permitting the use or enjoyment of a copyright relating to original literary works to a publisher.

(xiv) Supply of services by the members of Overseeing Committee to Reserve Bank of India.

(xv) Services supplied by individual Direct Selling Agents (DSAs) other than a body corporate partnership or limited liability partnership firm to bank or non-banking financial company (NBFCs).

(xvi) Services provided by Business Facilitator (BF) to a banking company.

(xvii) Services provided by an agent of Business Correspondent (BC) to Business Correspondent (BC).

(xviii) Security Services (services provided by way of supply of security personnel) provided to a registered person.

(xix) Services provided by way of renting of any motor vehicle designed to carry passengers where the cost of fuel is included in the consideration charged from the service recipient, provided to a body corporate.

(xx) Services of lending Securities under Securities Lending Scheme, 1997 (Scheme). Securities and Exchange Board of India (SEBI), as amended.

5.4.16 In addition, the following two services have been notified in Notification No. 10/2017-Integrated Tax (Rate), dated 28.06.2017 –

(i) Any service supplied by any person who is located in a non-taxable territory to any recipient in India, other than non-taxable online recipient.

(ii) Services supplied by a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the Customs Station of clearance in India.

6. PERSONS LIABLE TO PAY GST

6.1. GST is payable at the prescribed rate by the registered taxable person on the supply of goods and/or services. The CGST/SGST is payable on all intra-State supply (within the State) of goods and/or services and IGST is payable on all inter-State supply (from one State to another State) of goods and/or services.

6.2. The threshold limit of aggregate turnover for exemption from registration and payment of GST for suppliers of goods is Rs. 40 Lakh (Rs. 20 Lakh in the States of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Puducherry, Sikkim, Telangana, Tripura and Uttarakhand). The threshold limit of aggregate turnover for exemption from registration and payment of GST for suppliers of services is Rs. 20 Lakh. The aggregate turnover shall include the aggregate value of all taxable supplies, exempt supplies and exports of goods and/or services, excluding GST and shall be computed on all India basis.

6.3. However, the taxpayers eligible for threshold exemption will have the option of paying tax with input tax credit (ITC) benefits. Taxpayers making inter-State supplies of goods or paying tax on reverse charge basis (where the recipient of the supplies is liable to pay tax) shall not be eligible for threshold exemption, meaning that such taxpayers are liable to pay GST, irrespective of their turnover.

6.4. In respect of the notified supply of goods and/or services, the tax is payable by the recipient of such supplies, as prescribed under Section 9(3) of the CGST Act, 2017. This system of payment of tax by the recipient is known as ‘reverse charge mechanism’. (Section 9(3) & 9(5) of CGST Act, 2017)

6.5. In respect of certain supplies of services through the Electronic Commerce (e-commerce) Operator, GST is neither payable by the supplier nor the recipient of such supplies, but by the e-commerce operator, as provided in Section 9(5) of the CGST Act, 2017. The list of services notified in Notification No. 17/2017-CT (Rate) dated 28.06.2017, as amended, are as under –

(i) services by way of passengers by a radio-taxi, motorcab, maxicab, motor cycle or any other motor vehicle, except omnibus;

(ii) services by way of providing accommodation in hotel, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes, except where the supplier of such service through e-commerce operator is liable for GST registration;

(iii) services by way of house-keeping, such as plumbing, carpentering, etc, except where the supplier of such service through e-commerce operator is liable for GST registration;

(iv) supply of restaurant service, other than the services supplied by restaurant, eating joints, etc., located at hotel providing accommodation with declared value of any unit above Rs. 7500/- per unit per day.

7. CLASSIFICATION OF GOODS AND SERVICES

7.1. Classification is the categorization of goods and services crucial to ascertain whether a subject matter is eligible to tax, exemption and the rate of tax.

7.2. Under GST, all goods and services transacted in India are classified as per the HSN (Harmonised System of Nomenclature) code system or SAC (Services Accounting Code) system.

7.3. HSN code number is an internationally adopted commodity description and coding system developed by the World Customs Organization (WCO). With the HSN code acting as a universal classification for goods, it is adopted for classification of goods under GST and levy of GST.

7.4. There is no separate dedicated Tariff Schedule under GST. However, for the purpose of classification, Customs Tariff has been adopted. The goods are classified from Chapter 1 to Chapter 98A. Services are classified under Chapter 99.

7.5. The rate of GST on goods have been prescribed in Notification No. 1/2017-CT (Rate) dated 28.06.2017 and Notification No. 1/2017-Integrated Tax (Rate), dated 28.06.2017, as amended. The list of goods contained in the said notification provides the description of goods, Chapter/Heading/sub-heading/Tariff Item number and the applicable tax rate mentioned against each goods. Thus, Notification No. 1/2017-CT (Rate) and 1/2017-Integrated Tax (Rate) is useful for determining the appropriate classification of goods and the applicable tax rate.

7.6. As per the said Notifications, the following six GST rate slabs are presently applicable for goods –

(i) 5% (2.50% CGST + 2.50% SGST) in respect of goods specified in Schedule I of the Notification,

(ii) 12% (6% CGST + 6% SGST) in respect of goods specified in Schedule II of the Notification,

(iii) 18% (9% CGST + 9% SGST) in respect of goods specified in Schedule III of the Notification,

(iv) 28% (14% CGST + 14% SGST) in respect of goods specified in Schedule IV of the Notification,

(v) 3% (1.50% CGST + 1.50% SGST) in respect of goods specified in Schedule V of the Notification, and

(vi) 0.25% (0.125% CGST + 0.125% SGST) in respect of goods specified in Schedule VI of the Notification.

7.7. Notification No. 2/2017-CT (Rate) and 2/2017-Integrated Tax (Rate), both dated 28.06.2017 provides list of goods fully exempted from levy of CGST/IGST.

7.8. Services are classified under Chapter 99 of the HSN. This Chapter provides the description of services, Sections, Headings and the notified tax rates. Notification No. 8/2017-Integrated Tax (Rate), dated 26.06.2017, as amended, prescribes GST rate of the services. There are six slabs of tax rates prescribed – Nil, 5%, 9%, 12%, 18% and 28%. With effect from 01.04.2019, the rate of tax for some construction services is 1.50% and 7.50%, subject to fulfilling the conditions prescribed.

7.9. The explanatory notes published by GST Council indicate the scope and coverage of the heading, groups and service codes of the Scheme of Classification of Services, which can be used as a guiding tool for classification of services.

7.10 The rates applicable to any goods or services are published by CBIC and can be viewed on https://cbic-gst.gov.in/gst-goods-services-rates.html.

8. COMPOSITE AND MIXED SUPPLIES

8.1 Composite supply is a supply consisting of two or more taxable supplies of goods or services or both or any combination thereof, which are bundled in natural course and are supplied in conjunction with each other in the ordinary course of business and where one of which is a principal supply (the main goods or service).

For example, when a consumer buys a television set and he also gets warranty and a maintenance contract with the TV, such supply is a composite supply. In this example, supply of TV is the principal supply, warranty and maintenance service are ancillary.

8.2. In Composite supply the principal supply shall be considered for determining the rate of tax.

8.3. Mixed supply is combination of more than one individual supplies of goods or services or any combination thereof made in conjunction with each other for a single price, which can ordinarily be supplied separately.

For example, a shopkeeper selling refrigerator along with storage water bottles. Bottles and the refrigerator can easily be priced and sold separately. Another example is the supply of a package consisting of sweets, chocolates, dry fruits, supplied for a single price. Each of these items can be supplied separately and is not dependent on each other

8.4. Mixed supply would be treated as supply of that particular goods or services which attracts the highest rate of tax.

9. EXEMPTION FROM GST

9.1. Section 11 of the CGST Act, 2017 empowers the Government to exempt either wholly or partly, on the recommendations of the GST Council, the supplies of goods and/or services from the levy of GST either absolutely or subject to conditions. Further the Government can exempt, under circumstances of an exceptional nature, by special order any goods or services or both. (Section 11 of CGST Act, 2017)

9.2 The SGST Act and UTGST Act provide that any exemption granted under CGST Act, 2017 shall be deemed to be exemption under these Acts.

9.3 If exemption from whole of tax on goods or services or both has been granted, the person cannot pay tax on his own volition. Further, if the goods are partly exempted, the person supplying exempted goods or services or both shall not collect the tax in excess of the effective rate.

10. TIME OF SUPPLY OF GOODS AND SERVICES

10.1. The time of supply fixes the point when the liability to charge GST arises. It also indicates when a supply is deemed to have been made. The CGST Act, 2017 provides separate time of supply for goods and services.

10.2. In terms of Section 12(1) of the CGST/SGST Act, the time of supply of goods shall be the earlier of the following – (Section 12(1) & 31 of CGST Act, 2017)

(i) the date of issue of invoice by the supplier or the last date on which he is required to issue the invoice as per Section 31of CGST Act, 2017, with respect to the supply; or

(ii) the date on which the supplier receives the payment with respect to the supply.

10.3. Section 13(1) of the CGST Act, 2017 provides for time of supply of services. The time of supply of services shall be the earlier of the following – (Section 13(1) & 31 of CGST Act, 2017)

(a) the date of issue of invoice by the supplier if the invoice is issued within the period prescribed under Section 31 or the date of receipt of payment whichever is earlier; or

(b) the date of provision of service, if the invoice is not issued within the period prescribed under Section 31 or the date of receipt of payment whichever is earlier;

(c) the date on which the recipient shows the receipt of services in his books of account, in case where the clauses do not apply.

10.4. The time of supply of voucher (e.g. Gift Voucher, etc.) in respect of goods and services shall be;

(a) the date of issue of voucher, if the supply is identifiable at that point; or

(b) the date of redemption of voucher in all other cases.

10.5. If it is not possible to determine the time of supply in the manner stated above, then as per Section 12(5) and 13(5) of the CGST Act, 2017, if periodical return has to be filed, then the due date of filing of such periodical return shall be the time of supply. In other cases, it will be the date on which the CGST/SGST/IGST is actually paid. (Section 12(5) and 13(5) of CGST Act, 2017)

10.6. The time of supply of goods in case of tax payable under reverse charge mechanism will be the earliest of the following dates:

(a) date of receipt of goods; or

(b) date on which payment is made; or

(c) the date immediately following 30 days from the date of issue of invoice by the supplier.

(d) Where it is not possible to determine the time of supply under the above three clauses, the time of supply shall be the date of entry in the books of account of the recipient of supply.

10.7. The time of supply of service in case of tax payable under reverse charge mechanism will be the earliest of the following dates:

(a) date on which payment is made; or

(b) the date immediately following sixty days from the date of issue of invoice by the supplier.

10.8. The time of supply with regard to an addition in value on account of interest, late fee or penalty on delayed consideration shall be the date on which the supplier received such additional consideration.

10.9 In cases where supply is completed prior to change in rate of tax, the time of supply will be-

(i) where the invoice for the same has been issued and the payment is also received after the change in rate of tax, the time of supply shall be the date of receipt of payment or the date of issue of invoice, whichever is earlier. For supply of goods payment of tax need to be made only at the time of issue of invoice; or

(ii) where the invoice has been issued prior to change in rate of tax but the payment is received after the change in rate of tax, the time of supply shall be the date of issue of invoice; or

(iii) where the payment is received before the change in rate of tax, but the invoice for the same has been issued after the change in rate of tax, the time of supply shall be the date of receipt of payment. For supply of goods payment of tax need to be made only at the time of issue of invoice.

10.10. In cases where supply is completed after change in rate of tax, the time of supply will be-

(i) where the payment is received after the change in rate of tax but the invoice has been issued prior to the change in rate of tax, the time of supply shall be the date of receipt of payment. For supply of goods payment of tax need to be made only at the time of issue of invoice; or

(ii) where the invoice has been issued and the payment is received before the change in rate of tax, the time of supply shall be the date of receipt of payment or date of issue of invoice, whichever is earlier. or;

(iii) where the invoice has been issued after the change in rate of tax but the payment is received before the change in rate of tax, the time of supply shall be the date of issue of invoice

10.11. In respect of services between the associated enterprise, the time of supply in the case of supply of services where the supplier is located outside India will be the earlier of date of entry in the books of account of the recipient of supply or the date of payment. That is, the levy under GST is attracted once such book entries are made even if no actual payment takes place or no invoice is issued.

10.12. The time of supply in respect of continuous supply of services will be the date by which the invoice is actually issued or is required to be issued or the date of receipt of payment, whichever is earlier.

11. PLACE OF SUPPLY OF GOODS AND SERVICE

11.1. The basic principle of GST is that it should effectively tax the consumption of such supplies at the destination thereof or as the case may be at the point of consumption. Place of supply provision determines the place i.e. taxable jurisdiction where the tax should reach. The place of supply determines whether a transaction is intra-State or interstate. In other words, the place of Supply of Goods or services is required to determine whether a supply is subject to SGST plus CGST in a given State or Union territory or else would attract IGST if it is an interstate supply.

11.2. The place of supply of goods shall be the location of the goods at the time of delivery to the recipient or at the time at which the movement of goods terminates for delivery to the recipient.

11.3. The place of supply where the goods are supplied on board a conveyance, such as a vessel, an aircraft, a train or a motor vehicle shall be the location at which such goods are taken on board. For instance, if goods are taken on board at Vadodara, Gujarat on Rajdhani Express from Mumbai to Delhi, the place of supply shall be Vadodara, Gujarat. However, in respect of services, the place of supply shall be the location of the first scheduled point of departure of that conveyance for the journey. For example, in India “Enjoy on wheels” is a train which runs from Jaipur to Kanyakumari and provides entertainment services. For outward journey the place of supply will be Jaipur and for return journey it will be Kanyakumari. The second example is a person travelling from Mumbai to Ranchi by Air watches a movie on board by making the payment. The place of supply will be Mumbai, the place of departure of the conveyance

11.4. The place of supply in case of assembly or installation of goods at site will be the place of such installation or assembly.

11.5. The place of supply of goods imported into India shall be the location of the importer and the place of supply of goods exported from India shall be the location outside India.

11.6. The place of supply of services is the location of recipient of service.

11.7. Any service provided directly in relation to an immovable property including services provided by architects, interior decorators, surveyors, engineers and other related experts or estate agents, any service provided by way of grant of rights to use immovable property or for carrying out or coordination of construction shall be the location at which the immovable property is situated.

11.8. In case of an event, if the recipient of service is registered, the place of supply of services for organizing the event shall be the location of such recipient. However, if the recipient is not registered, the place of supply shall be the place where event is held.

11.9. The place of supply of services by way of transportation of goods, including mail or courier, shall be the location of registered recipient. However, if the recipient is not registered, the place of supply shall be the place where the goods are handed over for their transportation.

11.10. Where the transportation of goods is to a place outside India, the place of supply shall be the place of destination of such goods.

11.11. The place of supply of service in respect of goods that are required to be made physically available by the recipient of service to the supplier of service shall be the location where the services are actually performed. For example, if a manufacturer located in Vadodara gets a Electric Pump repaired from a repair service provider located in Mumbai, by sending the Pump to the repairer’s location in Mumbai and receives back the Pump after repairs, in such cases the place of supply would be Mumbai, where the repair service was performed.

If the services are performed from a remote location using electronic means on goods, the place of supply shall be the location where the goods are actually located at the time of supply of services. For example, if a manufacturer located in Mumbai wants to get the issues in the software of a CNC machine installed at the factory in Mumbai resolved and the Engineer providing the repair service located in Delhi repairs the software resolves the issue by sitting in Delhi, then in such cases, the place of supply of this service would be Mumbai, the place where the machine is located.

11.12. For OIDAR services the place of supply will be the location of recipient of services. For the purpose of determining place of supply, the location of recipient of service shall be deemed to be in the taxable territory if any two of the following seven non-contradictory conditions are satisfied, namely:-

(a) the location of address presented by the recipient of services through internet is in the taxable territory;

(b) the credit card or debit card or store value card or charge card or smart card or any other card by which the recipient of services settles payment has been issued in the taxable territory;

(c) the billing address of the recipient of services is in the taxable territory;

(d) the internet protocol address of the device used by the recipient of services is in the taxable territory;

(e) the bank of the recipient of services in which the account used for payment is maintained is in the taxable territory;

(f) the country code of the subscriber identity module card used by the recipient of services is of taxable territory;

(g) the location of the fixed land line through which the service is received by the recipient is in the taxable territory.

11.13. In the case of services supplied in respect of goods which are temporarily imported into India for repairs or for any other treatment or process and are exported after such repairs or treatment or process without being put to any use in India, other than that which is required for such repairs or treatment or process, the place of supply shall be the location of recipient of services. For example, a person located in Dubai sends a machine for repairs by a service provider located in Bengaluru. The service provider has to comply with all the procedures related to import of such machine into India. After carrying out the repairs the said service provider sends the machine back to the sender of the machine located in Dubai, by following export procedure. As the repairs were carried out in Bengaluru and this machine was not put into any use in Bengaluru but returned to the person located in Dubai, the place of supply in this case would be Dubai, as per second proviso to sub-clause (a) to Clause (3) of Section 13 of CGST Act, 2017.

12. TAX INVOICE UNDER GST

12.1. As per Section 31 of CGST Act, 2017, a registered taxable person is required to issue a tax invoice showing description, quantity and value of goods, tax charged thereon and other particulars prescribed in Rule 46 of CGST Rules, 2017, before or at the time of- (Section 31 of CGST Act, 2017 & Rules 46 of CGST Rules, 2017)

(a) removal of goods for supply to the recipient, where supply involves movement of goods; or

(b) delivery of goods or making the goods available to the recipient in other cases.

12.2. In respect of supply of services, a registered person is required to issue a tax invoice before or after the provision of service, but within a period of 30 days from the date of supply of service, showing description, value of goods, tax payable thereon and other prescribed particulars. For Banking and Insurance companies, this period is 45 days. For inter-state self-supplies made by bank, insurance and telecom companies, invoices can be issued before or at the time such supplier records the same in his books of account or before the expiry of the quarter during which the supply was made.

12.3. A registered person liable to pay tax on reverse charge basis is required to issue invoice on the date of receipt of goods or services or both.

12.4. In case of continuous supply of services –

(a) where the due date of payment is ascertainable from the contract, the invoice is required to be issued on or before due date of payment;

(b) where the due date of payment is not ascertainable from the contract, the invoice is required to be issued before or at the time when the supplier of service receives the payment;

(c) where the payment is linked to the completion of an event, the invoice is required to be issued on or before the date of completion of that event.

(d) where successive statements of account or successive payments are involved, the invoice is required to be issued before or at the time each such statement is issued or each such payment is received.

12.5. A registered person supplying exempted goods or services or both or paying tax under the Composition Scheme shall issue a bill of supply instead of a tax invoice.

13. VALUATION OF SUPPLY OF GOODS AND SERVICES UNDER GST

13.1. Section 15 of the CGST Act, 2017 deals with the valuation of taxable supply. (Section 15 of CGST Act, 2017)