![]()

The transitional provisions of GST Act deal with the migration of existing taxpayers into the GST regime.

“Existing Taxpayer”refers to those entities which are currently registered, under any of the Acts as specified, i.e., Central Excise, Service Tax, State Sales Tax/VAT (except exclusive liquor dealers if registered under VAT), Entry Tax, Luxury Tax and Entertainment Tax (except levied by the local bodies).

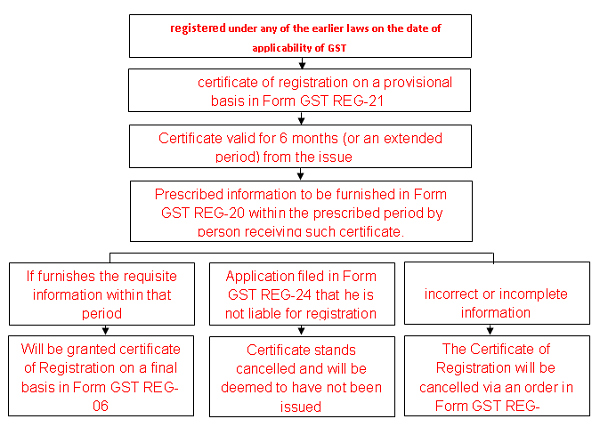

Provisional Registration

All the existing registrants having a Permanent Account Number will be issued a provisional registration certificate in Form GST REG-21.Such Certificate shall be valid for an initial period of six months (or an extended period, as may be notified by the Central Government/State Government on recommendation of the Council) from the date of issue.

Final Registration

After obtaining the provisional registration, an application in Form GST REG-20 needs to be submitted along with the requisite information and documents. This needs to be furnished within 6 months(or an extended period, as may be notified by the Central Government/State Government on recommendation of the Council) from the date of issue of provisional registration. If such information is found to be correct and complete, the final registration will be granted in Form GST REG-06.

Cancellation of Provisional Registration

In the following situations, the registration will stand cancelled through an order in Form GST REG-22:

> information is not furnished within the prescribed time limit

> information is found to be incorrect

> information is found to be incomplete

Such cancellation of registration can be effected only after serving show cause notice in Form GST REG-23 and providing the concerned person a reasonable opportunity of being heard.

If an existing registrant is not liable to be registered under GST, then he needs to file an application in Form GST REG-24. Henceforth, the proper officer will make an enquiry and if he deems fit, the registration will stand cancelled. Once cancelled, it will be deemed to have not been issued.

ENROLMENT – Of Existing Taxpayers under GST Portal

Enrolment under GST refers to validation of the latest data of the existing taxpayers and filling up the remaining key fields in GST Database, as required, thereby allowing smooth transition to the GST regime.

GST System Portal

The GST regime proposes to move towards a paperless administration, where technology will play a pivotal role.This will cause the discarding of the process of physical verification of premises and result in introduction of the GST system portal. The portal shall enable a registrant to carry out GST related Compliances, viz. return filing, tax payment, etc. This will also ensure that the existing data with the tax authorities stand complete and there is no need of amending / updating the data afterwards.

Timeline for enrolment

All the existing taxpayers are required to enroll with the GST system portal. It has been proposed that the enrolment process should be completed on the GST system portal as per the schedule below:

| States | Start Date | End Date |

| Puducherry, Sikkim | 08/11/2016 | 23/11/2016 |

| Maharashtra, Goa, Daman and Diu, Dadra and Nagar Haveli, Chhattisgarh | 14/11/2016 | 30/11/2016 |

| Gujarat | 15/11/2016 | 30/11/2016 |

| Odisha, Jharkhand, Bihar, West Bengal, Madhya Pradesh, Assam, Tripura, Meghalaya, Nagaland, Arunachal Pradesh, Manipur, Mizoram | 30/11/2016 | 15/12/2016 |

| Uttar Pradesh, Jammu and Kashmir, Delhi, Chandigarh, Haryana, Punjab, Uttarakhand, Himachal Pradesh, Rajasthan | 16/12/2016 | 31/12/2016 |

| Kerala, Tamil Nadu, Karnataka, Telangana, Andhra Pradesh | 01/01/2017 | 15/01/2017 |

| Enrolment of Taxpayers who are registered under Central Excise Act/ Service Tax Act but not registered under State VAT | 01/01/2017 | 31/01/2017 |

| Delta All Registrants (All Groups) | 01/02/2017 | 20/03/2017 |

However, the enrolment shall be open till 31/01/2017 for those who miss the above dates. Also, the taxpayers registered under Service Tax need to enroll on a later date which is yet to be notified.

Frequently Asked Questions

1) Whether separate enrolment is required with Central and State Authorities under GST?

Enrolment under GST is common for both Central GST and the State GST. There will be common registration, common return and common challan for Central and State GST. Hence, taxpayers are not required to enroll separately with the Central and State Authorities.

2) Is there a requirement of separate enrolment under GST for each business, in case of multiple businesses in one state under the same PAN?

Since one PAN allows only one GST Registration in a State, therefore only one business vertical (out of multiple business verticals within a State) can be registered using a single PAN. For the remaining business verticals within the State, one needs to contact the jurisdictional authority.

3) Is the enrolment process same for taxpayers registered under the Centre/State/UT tax Acts?

Yes, the enrolment process is common for all the taxpayers registered under different acts.

4) Whether any fee is to be charged for the enrolment on GST System Portal?

No, there are no charges for the enrolment of a taxpayer with the GST system portal.

5)What is the format of Provisional ID?

The Provisional ID shall be a 15-digit alphanumeric id beginning with the state code (two digits), followed by PAN of the entity (ten digits), the entity number of the same PAN holder in a state(one digit), the default alphabet ‘Z’, and the check sum digit (one digit).

6) What are the information/documents which are required before starting with the process of enrolment under GST?

Before enrolling under GST, one must ensure that the following information are available: –

> Provisional ID received from State/Central Authorities

> Password received from State/Central Authorities

> Valid Email Address

> Valid Mobile Number

> Bank Account Number

> Bank IFSC

The documents required are: –

> Proof of Constitution of Business: –

- In case of Partnership Firm: Partnership Deed of Partnership Firm (PDF and JPEG Format in maximum size of 1 MB)

- In case of Others: Registration Certificate of the Business Entity (PDF and JPEG Format in maximum size of 1 MB)

> Photograph of Promoters/Partners/Karta of HUF (JPEG format in maximum size of 100 KB)

> Proof of Appointment of Authorized Signatory (PDF and JPEG Format in maximum size of 1 MB)

> Photograph of Authorized Signatory (JPEG format in maximum size of 100 KB)

> Opening page of Bank Passbook/Statement containing Bank Account Number, Address of Branch, Address of Account Holder and few transaction details (PDF and JPEG Format in maximum size of 1 MB)

7) Can amendments be made (like change in mobile no., email id) after submission of the enrolment application?

Yes, amendments can be made to the enrolment application from the appointed date.

8) When will the Provisional Registration Certificate be granted?

The Provisional Registration Certificate will be made available on the dashboard of the registrant, on the appointed date, if the enrolment application has been filled successfully.

9) Can the enrolment application get rejected?

The application for enrolment on the GST system portal can be rejected in case wrong/fake/incorrect document has been furnished/uploaded, with the DSC or E-Sign of the authorized person. However, the applicant will be provided reasonable opportunity of being heard where the applicant taxpayer can present his/her view on the mistake committed therein.

10) For enrolling with GST, which of the details are prefilled in the enrolment application?

The following details are auto-populated in the enrolment application based on one’s existing data: –

> PAN of the Business

> Legal Name of the Business

> State

> Reason of liability to obtain registration

> Email Address and Mobile Number of Primary Authorized Signatory entered during enrolling with GST System Portal

11) Will there be any reference number that is sought to be received on submission of the application for enrolment by an existing taxpayer registered under Central Excise/Service Tax/State VAT?

An ARN will be generated after the successful submission of the enrolment application at the GST system portal.

ARN stands for Application Reference Number, which is a unique number assigned to each transaction completed at the GST system portal.

The ARN has the following uses: –

> To track the status of one’s Application

> For Future Correspondence with GSTN

Conclusion

With the dates of enrolment lurking around the corner, it is imperative that every existing taxpayer should acquaint themselves with the process of enrolment and migration to GST. This will ensure that he will not have to go through the process of amendment when the provisional registration is issued to the registrant. Also once this filed, the latest data will be available with the Department.

(Author can be reached at shubham@cakhaitan.com)

Author Bio

If person not liable to register under GST but was registered under Service tax/VAT , he can cancel Provisional ID till 31st July 2017

which official notification says this statement