ITC Puzzle in GST for Used Cars -“GST Council minutes referred to “such vehicles”, the notification used the phrase “such goods”

“Notification 08/2018-CT (Rate) sparked disputes as the GST Council used the term ‘such vehicles’ while the notification issued says ‘such goods’. This article explains why ITC restriction applies only to old and used motor vehicles, not all goods, with references to GST Council minutes, notification text, and legal interpretation.”

Background

The taxation of the pre-owned motor vehicle industry has been a contentious issue under the GST regime. Initially, the supply of used cars was taxed at the highest slab of 28% GST, along with applicable Compensation Cess, creating hardship and double taxation concerns.

Recognizing this, the 25th GST Council Meeting held on 18 January 2018 deliberated on industry representations and recommended concessional tax rates for old and used vehicles. These recommendations were later implemented through Notification No. 08/2018-Central Tax (Rate) dated 25 January 2018.

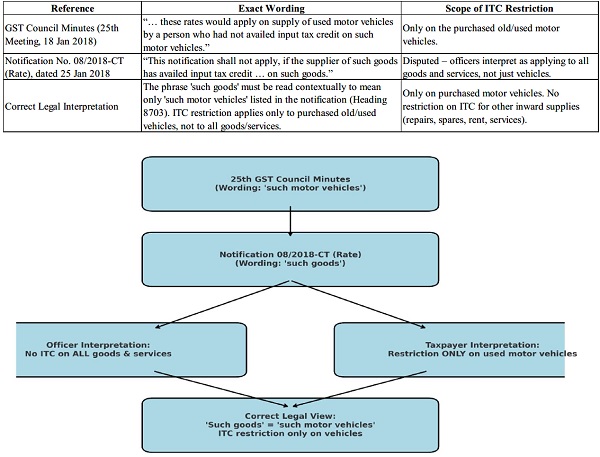

However, while the GST Council minutes referred to “such vehicles”, the notification used the phrase “such goods”. This drafting difference has led to disputes between taxpayers and officers regarding the scope of Input Tax Credit (ITC) restrictions.

Issue

- Council’s Intent: Restrict ITC only on the purchase of used motor vehicles where the concessional rate is applied.

- Notification Wording: Uses the broader term “such goods”, leading some officers to argue that dealers availing concessional rates cannot claim ITC on any inward supplies (repairs, spares, rent, services, etc.).

This divergence has resulted in audit objections and litigation, though the legislative intent seems much narrower.

Text of Notification No. 08/2018-CT (Rate)

The key extract from the notification reads as follows:

“This notification shall not apply, if the supplier of such goods has availed input tax credit as defined in clause (63) of section 2 of the Central Goods and Services Tax Act, 2017, CENVAT as defined in CENVAT Credit Rules, 2004 or the input tax credit of Value Added Tax or any other taxes paid, on such goods.”

At first glance, the phrase “such goods” appears wide. But in context, the notification applies only to Heading 8703 (old and used motor vehicles). Hence, “such goods” should logically mean only such vehicles.

Extract from 25th GST Council Meeting Minutes

The relevant excerpt from the minutes (Agenda Serial No. 9 – Used Motor Vehicles) reads:

“The Hon’ble Minister from Punjab stated that this proposal seemed to cause double taxation. The Secretary explained that the proposal was not to impose double taxation but only to impose tax on the margin of the supplier of a motor vehicle and the GST rate recommended by the Fitment Committee was 12% and Nil Compensation Cess on all motor vehicles under HSN Code 8702 (other than medium and large cars and SUVs), and 18% and Nil Compensation Cess on medium and large cars and SUVs, on the margin of the supplier of such motor vehicles. He added that these rates would apply on supply of used motor vehicles by a person who had not availed input tax credit on such motor vehicles. He further added that for a registered entity, value for tax purpose shall be the difference between the sale value and the depreciated value of the motor vehicle.”

“After discussion, the Council agreed to the tax proposal of the Fitment Committee in respect of used motor vehicles, contained at Serial No. 9 of Annexure I of this Agenda item.”

This makes it crystal clear that the Council intended restriction of ITC only on the purchased motor vehicles and not on other inward supplies.

Relevant Press Release Clarification

The GST Council, through its Press Release dated 15 July 2017, had earlier clarified the working of the margin scheme for second-hand goods. The important extracts are:

“Notification No. 10/2017-Central Tax (Rate), dated 28.06.2017 exempts central tax leviable on intra-State supplies of second-hand goods received by a registered person, dealing in buying and selling of second-hand goods (who pays the central tax on the value of outward supply of such second-hand goods as determined under sub-rule (5)) from any supplier, who is not registered. This has been done to avoid double taxation on the outward supplies made by such registered person, since such person operating under the margin scheme cannot avail input tax credit on the purchase of second-hand goods.”

“Thus, margin scheme can be availed of by any registered person dealing in buying and selling of second-hand goods [including old and used empty bottles] and who satisfies the conditions as laid down in rule 32(5) of the Central Goods and Services Tax Rules, 2017.”

This press release again confirms that ITC restriction applies only on the purchase of second-hand goods themselves (in this case, used motor vehicles).

Legal Analysis

1. Contextual Reading – Notification 08/2018 applies only to Heading 8703 (motor vehicles). The phrase “such goods” must be confined to this heading, not all goods generally.

2. Principle of Ejusdem Generis– General words following specific ones must be interpreted in the same context. Since the notification deals exclusively with motor vehicles, “such goods” can only mean those vehicles.

3. Role of Punctuation -The comma before “on such goods” indicates that the ITC restriction qualifies only the motor vehicles in question. Judicial precedents such as Sree Durga Distributors vs. State of Karnataka and Sunil Ranjan Das v. State reinforce this interpretation.

4. Constitutional Limitations (Article 279A)– The Council can recommend special rates only for specified goods/services. In this case, the recommendation was limited to used motor vehicles. Extending ITC denial beyond this scope would render the notification ultra vires.

5. Practical Consequences

-

- If the department’s wider interpretation is adopted, even a registered taxpayer selling one second-hand car would lose ITC on all unrelated inputs (rent, office supplies, utilities).

- Such an outcome would be inequitable and contrary to GST’s design as a value-added tax.

Notification_08_2018_Comparison

Conclusion

The phrase “such goods” in Notification No. 08/2018-CT (Rate) must be interpreted contextually and legally. It refers only to old and used motor vehicles covered under Heading 8703 of the notification and not to all goods or services procured by the dealer.

Accordingly:

- Concessional rates of 12% / 18% apply on margin value of old/used motor vehicles.

- ITC restriction applies only to the vehicles themselves, not to other inward supplies.

- Any wider interpretation contradicts the Council’s recommendation, constitutional provisions, and settled principles of interpretation.

Disclaimer

This article is based on the author’s personal interpretation and understanding of Notification No. 08/2018-CT (Rate), GST Council minutes, and related clarifications. It is meant purely for academic and informational purposes. The views expressed are personal and not legally binding. Readers are advised to seek professional advice before taking any decisions.

Suggested Tags: GST Council, ITC, GST Rate, Used Cars, Notification 08/2018, Margin Scheme, Second-Hand Vehicles

Author Bio