I would like to start this article with an important line mentioned by Gujarat High Court to a Central government lawyer that “the Court would rather go to the moon than to understand the policies and complexities of the Goods and Service Tax (GST) regime.”

As we know that the first few months of GST implementation have greater percentage of incorrect data than returns of later period. This was because of confusion and mess in GST implementation similar as demonetization. But now it’s the time to justify the data that has been punched in the GST returns.

Considering the complexities, confusion and mess in GST system, Taxpayer in general are afraid of assessment. Due to this reason, they fear whenever they received any communication from authorities/department. I believe when dealers receive any communication from department that their GSTIN have been picked/selected for scrutiny, many will panic.

It is important to note here that selection of GSTIN for Scrutiny is not manual activity by the department. The same is done with the help of “Advance Analytics in Indirect Taxes” (ADVAIT) & or “Business Intelligence and Fraud Analysis” (BIFA). Today’s Department is better equipped for detecting any kind of error or missed data in returns which plays crucial role in selecting GSTIN for Scrutiny and for investigation or Audits.

This article is written with the objective to reduce the fear of dealers and assist them in handling GST Scrutiny/Assessment. I believe and wish that after going through this article you will be well prepared for handling authorities by responding to their queries swiftly with relevant information and documents.

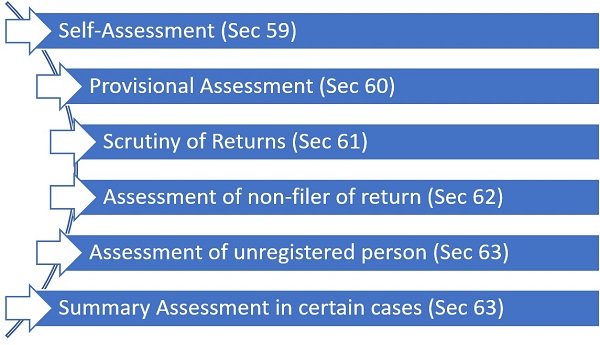

Assessments under GST–

Below type of assessment have been prescribed under the GST Act.

Let’s understand the section wise assessments in summarized manner.

> Self-Assessment– As per Section 59 of CGST Act, every registered person is required to furnish return under Section 39 after self-assessing his GST liability as per the provisions of law and indicate the amount on the invoices.

In general words, self-assessment means an assessment by the registered person himself and not an assessment conducted or carried out by the proper officer.

Accordingly, following are the important points to be noted for the purpose of self-assessment.

- Self-Assessment shall be done by every registered person only.

- Self-Assessment does not apply to unregistered person.

- The same is involved self-assessment of taxes payable.

- Self-assessment implies assessment by the taxpayer himself.

- Tax returns must be filed for each tax period in terms of Section 39 of CGST Act.

> Provisional Assessment– In case a supplier is unable to determine the value of goods or services or both or to determine the rate of tax applicable thereto, he can request the Asst. Commissioner/ Dy. Commissioner of Central Tax in writing, giving reason for payment of tax on a provisional basis.

Process of provisional assessment are as below.

> The provisional assessment can be restored to when an assessee is not sure of either

-

- Value of goods or services or both or;

- Rated Tax

> Assessee to apply for request of tax payment on provisional basis to the proper officer (PO) detailing the reason of such payment (Form GST ASMT-01)

> PO to issue notice in Form GST ASMT-02 and assessee will file a reply in Form GST ASMT-03

> PO to pass an order within 90 days of receipt of request from assessee for provisional payment of taxes detailing the rate of tax and value of supply in Form ASMT-04

> Assessee to furnish the bond (in Form GST ASMT-05) or differential amount between provisional and final tax and security/surety (maximum 25% of bond amount) as prescribed and pay the tax provisional. The security will be made by way of bank guarantee.

> PO to call for information in Form ASMT-06 finalisation of assessment

> PO to finalise the assessment within 6 months of data of provisional order and issue a final assessment order in Form ASMT-07. Such a period can be extended

> Once the assessment if finalized, assessee can file an application for releasing the bond in Form GST ASMT-03

> PO will release the bond after confirming the due taxes have been paid and issue order for releasing the bond in Form GST ASMT-09 within 7 working days of receipt of Form GST ASMT-08

> If final tax more than provisional=Assessee to pay interest at prescribed rate for period starting from next date of payment till the date of payment if final tax less than provisional=Assessee to seek refund and interest will be payable to assessee in accordance with section 56 i.e. from 61st day of refund claim application till date of refund

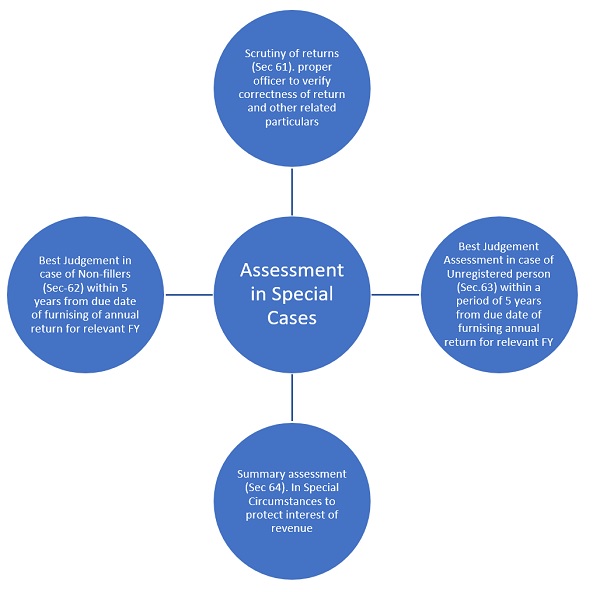

Special type of assessments can be done in four ways

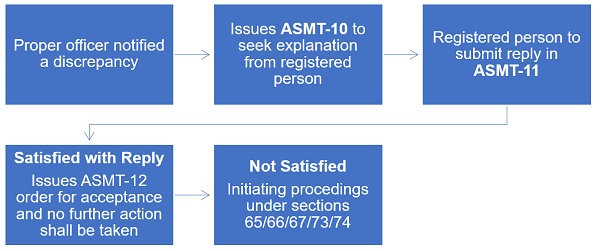

> Scrutiny of Returns (Sec 61)- The CGST Act, 2017 empowers proper officer to scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and informed him of the discrepancies noticed. The procedure followed by the proper officer are as below.

Important Points to be noted while receipt of clarification notice in Form ASMT-10

> There is no requirement to panic on receipt of such notice in ASMT-10 as the same is only discrepancy informative notice and no demanding order will be passed basis on this notice.

> The registered per person may accept the discrepancy and pay the tax, interest and any other amount arising from such discrepancy in case the discrepancies mentioned in the notice are correct.

> However, in case the discrepancies mentioned on the notice are not acceptable by the registered person, the person can file a detailed reply against ASMT-10 at the online portal of GST in Form ASMT-11 in order to avoid below proceedings.

- Initiate Audit of accounts by the tax authorities under Section 65; or

- Initiate special audit under Section 66; or

- Initiate inspection, search and seizure under Section 67;; or

- Proceed to determine the tax and other dues under Section 73 or Section 74.

Note:- No specific timeline has been provided under the GST Act to issue satisfactory order in Form ASMT-12 and accordingly practically in maximum cases the departments are not issuing satisfactory order in ASMT-12. The same can be seen with the status available at the portal post filling of reply in Form ASMT-11 i.e. “reply submitted pending for order”.

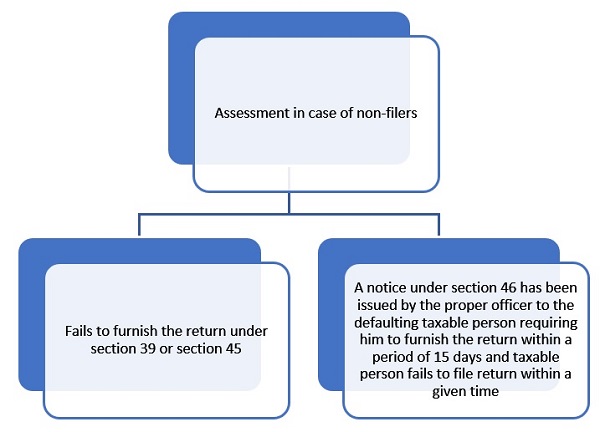

> Best judgement Assessment in case of non-filers –Where a registered person fails to furnish the return under section 39 or section 45, even after the service of a notice under section 46, the proper officer may proceed to assess the tax liability of the said person to the best of his judgement taking into account all the relevant material which is available or which he has gathered and issue an assessment order in Form GST ASMT-13 (Section 62 read with Rule 100 of GST)

Note :- Where a registered person furnish a valid return within 30 days of service of the assessment order under sub-section (1), the said assessment order shall be deemed to have been withdrawn but the liability for payment of interest or for payment of late fee shall continue.

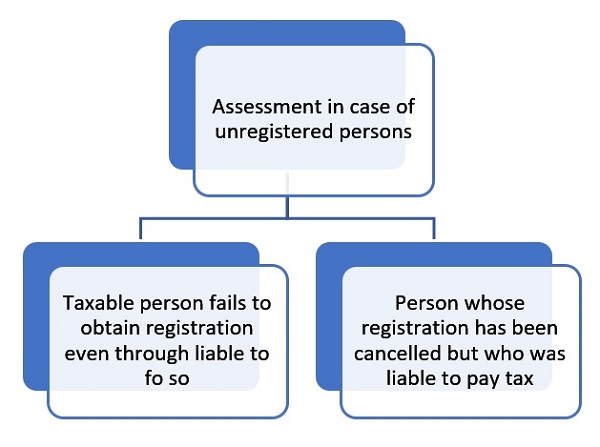

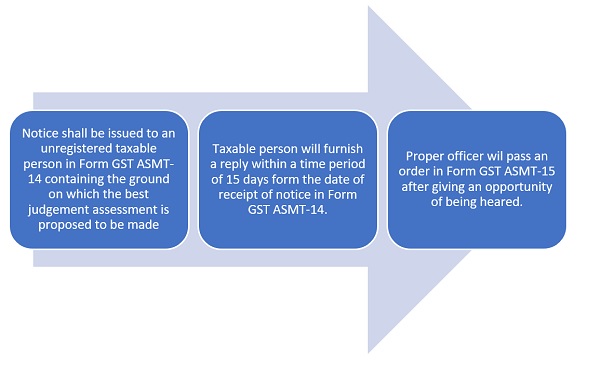

> Best judgement assessment in case of unregistered persons- Where a taxable person fails to obtain registration even through liable to do so or whose registration has been cancelled under sub-section (2) of section 29 but who was liable to pay tax, the proper officer may proceed to assess the tax liability of such taxable person to the best of his judgement for the relevant tax period, and issue an assessment order in Form GST ASMT-15

Process for best judgement assessment in case of unregistered person

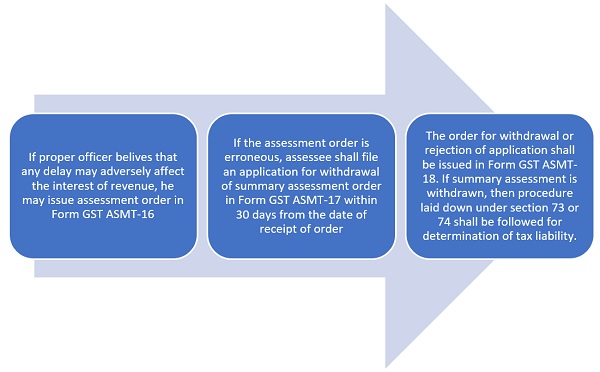

> Summary Assessment- The proper officer may on any evidence showing a tax liability of any person proceed to assess the tax liability of such person with the previous permission of additional Commissioner or joint Commissioner.

Certain important practical approach while replying to the received notices are as below for your ready reference.

| S. No. | Type of discrepancies (Differences ) | Step to be followed for reply |

| 1 | GSTR 1 vs GSTR 3B | Step-1– Check the value as mentioned on the notice with the actual value on filed GSTR 1 and GSTR 3B. You can check the comparative liability as available at the GST portal (Login to GST portal>Service>returns>tax Liabilities and ITC comparison>Select period) for such differences. If it is not matching. Write in reply that there is no difference in the liability as reported in GSTR 1 vis-à-vis the liability disclosed in GSTR 3B as per the comparative liability available the GST portal and accordingly notice should be dropped. Screenshot of the comparative liability can be attached with the reply as annexure for supporting.

Step-2– Take below actions in case the same is not matching -Tax more in GSTR 3B– The dealer will be required to check if the same is actually additionally paid via GSTR 3B. Write in reply that the additional tax has been made in GSTR 3B which is adjusted in subsequent period (<check the status of adjustment>) or will be adjusted in the subsequent period. -Tax more in GSTR 1– Check in previous year filed GSTR 1/GSTR 3B, if more tax liability has been paid in the previous year. This could be the reason of short payment in GSTR 3B as the earlier excess payment must be adjusted with current period liability. You can check the comparative liability as available at the GST portal (Login to GST portal>Service>returns>tax Liabilities and ITC comparison>Select period) to understand the same. Also check if the additional tax has been discharged using DRC-03 challan. Step-3– In case you find that short payment of tax liability as per notice is correct. Make the payment of additional tax liability along with interest @18% using DRC-03 and submit the same to the department along with reply. |

| 2 | Output Tax in GSTR 3B vs Form 9 i.e. Annual return | Step-1– Check the total liability as disclosed in table 9 and total payment. In case total payment is less than total liability, check the previous FY form 9 if the excess payment of the same is adjusted in current period.

Step-2– Check if the additional liability has been paid in subsequent year GSTR 3B or if the additional tax has been discharged using DRC-03 challan. |

| 3 | Between ITC as per GSTR 3B vs ITC as per 2A/2B | Step-1– Check the FY of the notice as GSTR 2A was not available in October 2018. There is a concept of “Lex non cogit impossibilia” i.e., the law can not compel a person to do anything that is impossible. Asking someone to match the form for July 2017 which was visible in October 2018 is impossible.

Step-2– Check the comparative ITC as available at the GST portal suing the steps i.e. You can check the comparative liability as available at the GST portal (Login to GST portal>Service>returns>tax Liabilities and ITC comparison>Select period) and take following action. – If the ITC as appearing in GSTR 2A/2B is more than the ITC availed in GSTR 3B, write in reply that the ITC as per GSTR 2A/2B is more than the ITC as availed in GSR 3B and accordingly proceedings should be dropped on this ground only. -If the ITC as appearing in GSTR 2A/2B is less than the ITC availed in GSTR 3B, check the difference with the ITC availed in current year for the documents pertaining to the previous FY and write in reply that the difference is on account of ITC pertaining to previous financial year which have been availed in current FY. Certain details of invoice wherein ITC has been availed in current FY are annexed and marked as…… Step-3– In case above two steps are not working, match invoice wise ITC with GSTR 2A/2B and submit reply accordingly. |

Certain important tips

♦ Keep necessary evidence handy with a proper explanation to deal with situations like assessment, investigations, audits, etc.

♦ Compare the rates you charge with your competitors to re-confirm the tax rates along with corresponding HSN.

♦ Also, take due care about the HSN/SAC classification in case the same HSN/SAC are being used for different rates

♦ Check if the ITC has not been availed on the below type of goods/services as the same are blocked ITC as per GST Act.

- Motor vehicles, conveyance, and related services

- Vessels, aircraft, and related services

- Membership of a club, health & fitness centre

- Works contract service

- Self-construction of immovable property

- Inward supplies of restaurants who opted to pay GST at a reduced rate

- Inward supplies of composition taxpayer

- Inward supplies of composition taxpayer

- Inward supplies used for personal consumption

- Free samples, gifts, goods lost, etc.

- Travel benefits to employees

- Inward supplies of the non-resident taxable person

- Food and beverages m health services beauty treatment services and other services

- Tax paid in fraud cases, detention, confiscation, etc.

Disclaimer – Except the quoted version, interpretation made and all other views expressed here are my personal views. Readers are advised to follow the provisions of the law before acting upon the views expressed here.

Author Bio