Various Definition:

Under Section 16 of the IGST Act, 2017

“Zero rated supply” means any of the following supplies of goods or services or both, namely:

a) export of goods or services or both; or

b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

What is Export of Goods under GST?

a) As per IGST Act Section 2(5) Export of goods with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India. Export means trading or supplying of goods and services outside the domestic territory of a country.

What is Export of Services under GST?

As per IGST Act Section 2(6) “Export of services” means the supply of any service when, –

a) (i) the supplier of service is located in India;

b) (ii) the recipient of service is located outside India;

c) (iii) the place of supply of service is outside India;

d) (iv) the payment for such service has been received by the supplier of service in convertible foreign exchange;

e) (v) the supplier of service and the recipient of service are not merely establishments of a distinct person

f)Supply of services having place of supply in Nepal or Bhutan, against payment in Indian Rupees is exempted even if the payment is received in Indian Currency looking at the business practices and trends.

What is Export of Services under GST?

As per IGST Act Section 2(6) “Export of services” means the supply of any service when, –

a) (i) the supplier of service is located in India;

b) (ii) the recipient of service is located outside India;

c) (iii) the place of supply of service is outside India;

d) (iv) the payment for such service has been received by the supplier of service in convertible foreign exchange;

e) (v) the supplier of service and the recipient of service are not merely establishments of a distinct person

f)Supply of services having place of supply in Nepal or Bhutan, against payment in Indian Rupees is exempted even if the payment is received in Indian Currency looking at the business practices and trends.

Refund Provision:

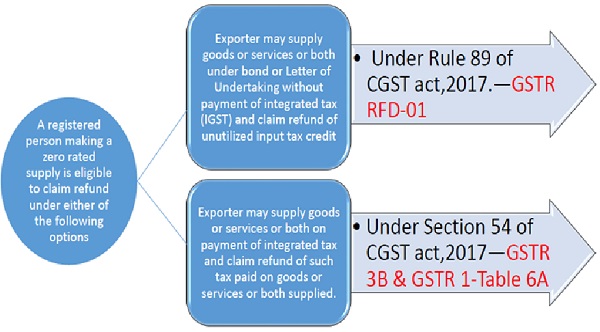

The objective of zero rating of exports and supplies to SEZ is sought to be achieved through the provision contained in Section 16(3) of the IGST Act, 2017, which mandates that a registered person making a zero rated supply is eligible to claim refund in accordance with the provisions of section 54 of the CGST Act, 2017, under either of the following options, namely: –

a) he may supply goods or services or both under bond or Letter of Undertaking, subject to such conditions, safeguards and procedure as may be prescribed, without payment of integrated tax (IGST) and claim refund of unutilised input tax credit of Central tax (CGST), State tax (SGST) / Union territory tax (UTGST) and integrated tax (IGST); or

b) he may supply goods or services or both, subject to such conditions, safeguards and procedure as may be prescribed, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied.

Rule 89 of CGST rules,2017:

As per provisions of sub rule (1) of rule 89 of the Central goods and service tax Rules, 2017.

a) Application for refund of tax, interest, penalty, fees or any other amount.-

b) Any person, except the persons covered under notification issued under section 55,claiming refund of any tax, interest, penalty, fees or any other amount paid by him, other than refund of integrated tax paid on goods exported out of India, may file an application electronically in FORM GST RFD-01 through the common portal, either directly or through a Facilitation Centre notified by the Commissioner

As per provisions of sub rule (4) of rule 89 of the Central goods and service tax Rules, 2017

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷ Adjusted Total Turnover

Where, –

a) “Refund amount” means the maximum refund that is admissible;

b) “Net ITC” means input tax credit availed on inputs and input services during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both;

c) Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both;

d) “Turnover of zero-rated supply of services” means the value of zero-rated supply of services made without payment of tax under bond or letter of undertaking, calculated in the following manner, namely:- Zero-rated supply of services is the aggregate of the payments received during the relevant period for zero-rated supply of services and zero-rated supply of services where supply has been completed for which payment had been received in advance in any period prior to the relevant period reduced by advances received for zero-rated supply of services for which the supply of services has not been completed during the relevant period;

e) “Adjusted Total Turnover” means the sum total of the value of- (a) the turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding the turnover of services; and 69 (b) the turnover of zero-rated supply of services determined in terms of clause (D) above and non-zero-rated supply of services, excluding- (i) the value of exempt supplies other than zero-rated supplies; and (ii) the turnover of supplies in respect of which refund is claimed under sub-rule (4A) or sub-rule (4B) or both, if any, during the relevant period. (F) “Relevant period” means the period for which the claim has been filed.

Section 54 of CGST Act,2017

Section 54 of CGST Act,2017 from bare act : –

Any person claiming refund of any tax and interest, if any, paid on such tax or any other amount paid by him, may make an application before the expiry of two years from the relevant date in such form and manner as may be prescribed: Provided that a registered person, claiming refund of any balance in the electronic cash ledger in accordance with the provisions of sub-section (6) of section 49, may claim such refund in the return furnished under section 39 in such manner as may be prescribed.

Steps Under this section to claim refund:

The normal refund application in GST RFD-01 is not applicable in this case.

As per rule 96 of the CGST Rules, 2017, the shipping bill filed by an exporter shall be deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application shall be Refund of Integrated Tax paid on account of zero rated supplies deemed to have been filed only when:-

(a) the person in charge of the conveyance carrying the export goods duly files an export manifest or an export report covering the number and the date of shipping bills or bills of export; and

(b) the applicant has furnished a valid return in FORM GSTR-3 or FORM GSTR3B, as the case may be.

Thus, once the shipping bill and export general manifest (EGM) is filed and a valid return is filed, the application for refund shall be considered to have been filed and refund shall be processed by the department.

Since the system of filing of return in FORM GSTR- 3 has not started so far, the refund of integrated tax on export of goods would be granted based on FORM GSTR-1 and FORM GSTR-3B for the time being. The details of the relevant export invoices contained in FORM GSTR-1 (or Table 6A thereof ) shall be transmitted electronically by the common portal to the system designated by the Customs and the said system shall electronically transmit to the common portal, a confirmation that the goods covered by the said invoices have been exported out of India.

Following Conclusions can be drawn

a) Form RFD-01 is filed when exporter is claiming for GST Refund as per sub rule (1) of rule 89 of the Central goods and service tax Rules, 2017 read with Section 16(3)(a) of IGST Act 2017.

b) As per definition of Net ITC given in sub rule (4) of rule 89 of the Central goods and service tax Rules, 2017

Net ITC means input tax credit availed on inputs and input services during the relevant period. It however does not includes ITC on capital goods therefore he cannot apply for refund of ITC paid on capital goods.

c) However ITC on capital goods can be utilised when exporter is claiming for GST Refund as per Section 16(3)(b) of IGST Act 2017 i.e. after payment of IGST taxes read with section 54 of CGST act,2017.

d) Therefore in absence of any clarification from Government one should not file RDF-01 for claiming ITC refund of capital goods without payment of integrated tax.

Question raised during refund order by Commissioner of GST:

For claiming GST input tax credit refund which has once been partially rejected by the commissioner ofGST , for an entity that makes only export supply of services without payment of tax. The order is non speaking. Also, it has been rejected on the grounds that input of certain goods and services refund cannot be availed because they were capitalized in the claimant’s book, however those goods and services were of revenue nature and have not been capitalized. The same clarification was also submitted by the claimant in form GST RFD-09 but was not remanded by the Adjudicating Authority and the refund was partially sanctioned in form GST RFD-06. Therefore allowing partial refund of ITC is not justifiable by the commissioner

As per reading of all above provision it is concluded as follow:

a) That if Claimant supply goods or services or both under bond or Letter of Undertaking, without payment of integrated tax (IGST) and claim refund of unutilized input tax credit. So he filled RFD-01 as per Sec16 (a) of IGST act read with section 54 of CGST act,2017, and their rules(Rule 89).——- Then ITC on capital goods will not be available(READ PROVISION`S ELABORATED ABOVE)—( As per current case specified above)

b) That if Claimant supply goods or services or both, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied. So he will file shipping bill/ export manifest and GSTR 3B & GSTR 1 and claim refund of Taxes paid on GST.

Section 2(19) of CGST Act: Definition of “Capital Goods”

“Capital goods” means goods, the value of which is capitalized in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business.

So as per above case law one can argue with Commissioner of GST for refund of Capital Goods, if same is not capitalized in books of Claimant.

However one can also argue for the difference in provision of law, where one allowed ITC on capital goods where other restrict the refund on same. Which ultimately lead to affect the working capital of Exporter.

manishkalwani1996@gmail.com

Author Bio

Can we claim refund on Capital Goods ITC in case Export Service Under LUT

No, we cannot claim ITC on Capital goods in case Export service under LUT as per rule 89 & 96 of CGST Act, 2017

Is it allowable and legally valid if we declare part of sales with Payment of Tax (To claim the refund of ITC of Capital Goods) & part of sales without payment while all are exports ? Even we have applied for LUT ?