In The World of Digitization and Automation, we are dealing with various E-Commerce Operator from Cab Services, Hotel Accommodation Services, Food Services, etc on constantly basis in our daily life. With Introduction of GST, Scope is widen on services provided through ECO. Will explain the Various Provision applicable to E-Commerce Operator.

Definition:-

- E-Commerce Operator: – As per Section 2(45) of the CGST Act, 2017, electronic Commerce operator means any person who owns, operates or manages digital or electronic facility or platform for electronic commerce.

- Electronic Commerce: – As per Section 2(44) of the CGST Act, 2017, electronic Commerce means the supply of goods or services or both, including digital products over digital or electronic network.

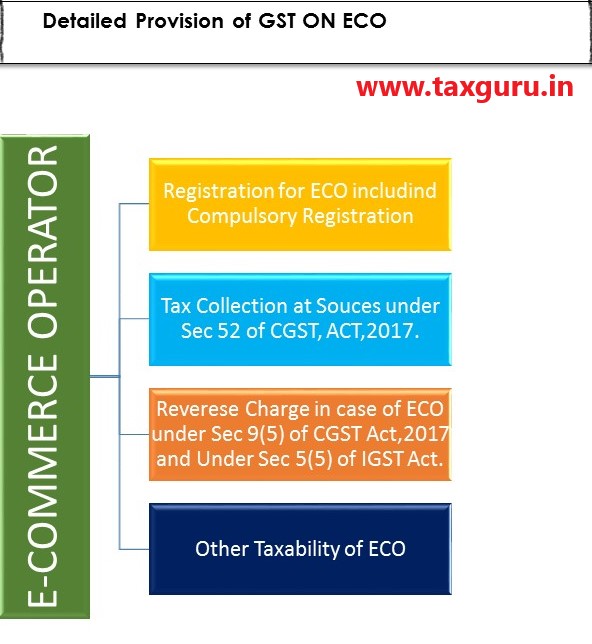

Registration under GST for E-Commerce Operator:

- Every Electronic Commerce Operator who is required to be paid tax under RCM pursuant to Sec 9 (5) and Sec 5 (5) of IGST Act, irrespective of his turnover, is mandatorily required to Obtain GSTIN registration through form GST REG-06 (Registration Certificate).

- In addition to that, E-Commerce Operator has to obtain the separate registration (Mandatorily) under Section 52 of CGST Act, 2017, through form GST REG-07 (Application for Registration Tax Collector at Sources).

- Earlier ECO is required to obtain mandatory registration. Post Amendment in CGST, ACT, 2017, (dated 01-02-2019), E-Commerce Operator, other than Operator who is required to deduct TCS & Operator liable under sec 9 (5) RCM provision, is eligible to threshold limit prescribed under GST.

- The proper officer may grant registration after due verification and issue a certificate of registration in FORM GST REG-06 within 3 working days from date of submission of application.

- Registration for TCS would be required in each State / UT as the obligation for collecting TCS would be there for every intra-State or inter-State supply. In order to facilitate the obtaining of registration in each State / UT, the e-commerce operator may declare the Head Office as its place of business for obtaining registration in that State / UT where it does not have physical presence. It may be noted that each State/UT has indicated one administrative jurisdiction where all e-commerce operators having business (but not having physical presence) in that State/UT shall register. The proper officer for the purpose of registration of ECOs has also been notified by each State/UT.

Registration for Supplier Supplying through E-Commerce Operator

- As per Section 24(ix) of the CGST Act, 2017, every person supplying goods or services through an ecommerce operator is mandatorily required to register.

- However, vide Notification 65/2017-Central Tax dated 15th November, 2017 a person supplying services, other than supplier of services under section 9 (5) of the CGST Act, 2017, through an e-commerce platform were exempted from obtaining compulsory registration provided their aggregate turnover does not exceed INR 20 lakhs (or INR 10 lakhs in case of specified special category States) in a financial year. Since such suppliers are not liable for registration, e-commerce operators are not required to collect TCS on supply of services being made by such suppliers through their portal

RCM provision for Specified Services u/s 9(5) of CGST Act and u/s 5 (5) of IGST Act:-

- The Government may, on the recommendation of the Council, specify categories of Services, the tax on which shall be paid by the electronic commerce operator (ECO) under RCM if such services are supplied through it and all the provisions of the Act shall apply to such electronic commerce operator as if he is the supplier liable to pay tax in relation to the supply of such services. A similar provision for inter-State supply is provided for in Sec. 5(5) of the IGST Act, 2017.

- E-Commerce Registered due to Provision of RCM, as specified, will be treated as a Normal Registered GSTIN Entity.

- Accordingly required to file GSTR-3B/GSTR-1 & Annual Return in GSTR-9.

Details of Services specified by Government under Sec9 (5), where ECO will be treated as supplier for supplies made through its platform:-

| S. No. | Des cription of supply of Service | Supplier of service | Person Liable to Pay GST | Notification No. | Remarks |

| 1 | Transportation of passengers by a radio-taxi, motorcab, maxicab and motor cycle | Any person | E-commerce operator | Notification No. 17/2017-Central Tax (Rate) dt 28th June, 2017

Corresponding IGST Noti fication No. 14/2017-Integrated Tax (Rate) dt 28th June, 2017 |

Thus in these cases, even though the services are provided by the taxi drivers, the onus to pay the taxes will lie solely on the ‘elect ronic commerce operator. ‘The rules will impact companies such as Meru Cabs, Mega Cabs, Ola, Uber, and car rental services such as Zoom Car and Myles. |

| 2 | Providing accommodation in hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes | Any person except who is liable for registration under sub-section (1) of section 22 of the said CGST Act(if turnover exceed the 20 Lakh Rupees or 10 Lakh Rupees in Special Category State) | E-commerce operator | Notification No. 17/2017-Central Tax (Rate) dt 28th June, 2017

Corresponding IGST Noti fication No. 14/2017-Integrated Tax (Rate) dt 28th June, 2017 |

We can take example of players like OYO, Make My Trip, etc. who are majorly involved in providing services by way of accom modation in hotels, guest house, clubs, etc. |

| 3 | Services by way of house-keeping, such as plumbing, carpentering etc | Any person except who is liable for registration under sub-section (1) of section 22 of the said CGST Act(if turnover exceed the 20 Lakh Rupees or 10 Lakh Rupees in Special Category State) | E-commerce operator | Notification No. 23/2017-Central Tax(Rate) dated 22nd Aug, 2017

Corresponding Notification No. 23/2017-Integrated Tax (Rate) dated 22nd Aug, 2017 |

We can take example of Urban clap, etc. who is majorly involved in providing services by way of misce llaneous utilities at the doorstep of the service recipient. |

Note:-

For Point no. 2 & 3, there may be 2 type of situation arise:-

Where the actual supplier is not liable to get registered under GST:

In this case, where actual supplier is not registered due limit of (20/10 Lakhs), the E-commerce operator will be treated as Supplier of Services due to Notification issued by Government pursuant to Sec 9(5). There will be single invoice which will be issue by E-Commerce Operator to Actual Recipient of Services.

Where the actual supplier is liable to get registered under GST:

In this Case, where Actual Supplier is registered supplier but he is provisioning his services through ECO platform. So there will be 2 transaction of GST chargeability, first will be between Actual Supplier and Actual Recipient for Accommodation or Housekeeping Services & Second will be for Commission amount services invoices issue by ECO to Actual Supplier.

Section 52:- Collection of Tax at Sources by ECO:

As per Section 52 of CGST Act, every Electronic Commerce Operator, Not being an Agent, shall deduct tax at source on the consideration collected by them where the supplies are made by Supplier`s through the operator portal.

Some Important Points:-

- Supplies made by the electronic commerce operator on its own account are not subject to TCS requirements.

- If the supply has been made through the portal of the Operator but consideration has not been received by the Operator but directly goes to the Supplier account then TCS on such supply shall not be collected and provisions of TCS shall not be applied on such supply.

- Supplier supplying Good or Services through ECO liable to deduct TDS is required to obtain registration under GST Mandatorily irrespective of Turnover Limit as specified.

- Operator are required to collect Tax @Rate of TCS is 0.5% under each Act (i.e. the CGST Act, 2017 and the respective SGST Act / UTGST Act respectively) and the same is 1% under the IGST Act, 2017. TCS will be collected on “Net Value of Taxable Supplies”.

- The “net value of taxable supplies” means the aggregate value of taxable supplies of goods or services or both, other than the services on which entire tax is payable by the e-commerce operator, made during any month by a registered supplier through such operator reduced by the aggregate value of taxable supplies returned to such supplier during the said month.

- The value of net taxable supplies is calculated at GSTIN level.

- TCS is to be collected once supply has been made through the e-commerce operator and where the business model is that the consideration is to be collected by the e-commerce operator irrespective of the actual collection of the consideration. For example, if the supply has taken place through the e-commerce operator on 30th June, 2018 but the consideration for the same has been collected in the month of July, 2018, then TCS for such supply has to be collected and reported in the statement for the month of October, 2018.

- If Supplies are made through ECO are exempted under GST, then TCS is not required to be collected on exempt supplies.

- Payment of TCS is not allowed through Input Tax Credit of e-Commerce operator, it has to be paid through cash ledger

- The amount of TCS deposited by the operator with the appropriate Government will be reflected in the electronic cash ledger of the actual registered supplier (on whose account such collection has been made) on the basis of the statement filed by the operator in FORM GSTR-8 in terms of Rule 67 of the CGST Rules, 2017. The said credit can be used at the time of discharge of tax liability by the actual supplier.

- Every operator is required to furnish a statement, electronically, containing the details of outward supplies of goods or services effected through it, including the supplies of goods or services returned through it, and the amount collected by it as TCS during a month within 10 days after the end of such month in FORM GSTR-8. The operator is also required to file an annual statement by 31st day of December following the end of the financial year in which the tax was collected in FORM GSTR-9B.

Charges and Levy for Other Operation of Ecommerce Operator

Levy and Collection of GST is specified under section 9 of CGST Act, 2017, and Sec 5 of IGST Act, 2017.

Under E-Commerce, There are two type of GST transaction are involved, which is specified below-

Between E-Commerce Supplier and End Customer:-

Supplying Goods or Service to Recipient through E-Commerce Platform consider as Supply of Goods or Services or Both under GST and levied to Taxes.

For Example, ABC Pvt. LTD. sale, the children toy through Amazon and accordingly they listed their product catalog on Amazon with Price Inclusive of GST. Mr. Been order the Baby Walker of ABC on Amazon. So Transaction between, ABC Pvt. LTD., and Mr. Been is Chargeable to GST @rate specified for Children Toys.

Between E-Commerce Supplier and E-Commerce Operator

ECO allow supplier to List his product on its Platform, which help supplier to reach vast number of Customer.

ECO also provide vide no. of services to Supplier Such as Shipping, Packaging, etc.

Against this ECO Charges commission and Other Services Charges, which is chargeable to GST as Supply of Services.

For Example: In Example Cited Above, If Value of Baby Walker is Rs.10, 000 and GST on Baby Walker is @18% is Rs.1800. Total Value is Rs.11, 800. If ECO charge the 10% Commission, which Amount to Rs.1000. Let say, GST rate on Commission is 12%, then GST amount on Commission value will be Rs.120.

For Commission Amount, ECO will issue invoice to Supplier

Author can be Communicate through manishkalwani1996@gmail.com.

Author Bio

Nice Article.