INTRODUCTION

Fast moving consumer goods (FMCG) is the 4th largest sector in the Indian economy. There are three main segments in the sector – food and beverages, healthcare and household and personal care which accounts for almost half of the sector.

FMCG Companies are looking to invest in energy efficient plants to benefit the society and lower costs in the long term. Growing awareness, easier access, and changing lifestyles are the key growth drivers for the consumer market. The focus on agriculture, MSMEs, education, healthcare, infrastructure and employment policies by the Government also have an impact on the growth of this sector.

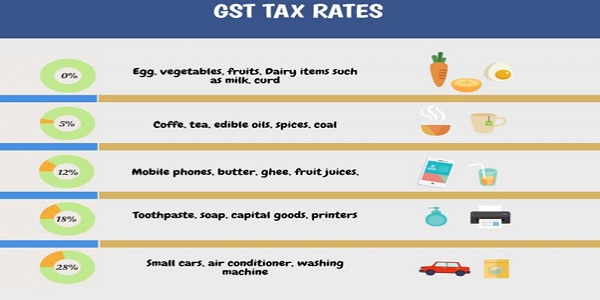

Since different products are taxed at different rates under GST, on a macro level, the average tax and the final prices that the end customer ends up paying have averaged out post implementation of GST, with some products becoming more expensive (aerated beverages, shampoos etc.) and others becoming cheaper (toothpaste, soaps etc.).

As the retail sector witnesses unprecedented growth, India has emerged among the most desirable retail destinations in the world. Even though modern trade is growing at 15 to 20% per annum, it has a low organized retail penetration of just 8%. Further, various infrastructural challenges remain.

India’s economic growth and its demographic profile make the country a compelling business case for global retailers planning an international foray. The strong economic growth is attributed to high disposable incomes, growing middle-class influence, increasing individual wealth and the country’s large young population. The untapped rural sector and the lesser developed Tier II and Tier III cities provide ample opportunities for growth. The liberalization of FDI in single-brand retail and the expected opening-up of FDI in multi-brand retail have generated significant interest among multinational retailers.

FAST-MOVING CONSUMER GOODS (FMCG) are goods that sell quickly and for a low price. Consumer packaged goods is another name for these goods. This is one of the industries that makes a significant contribution to our economy. India is one of the largest producers of FMCG products. The FMCG industry is divided into three categories.

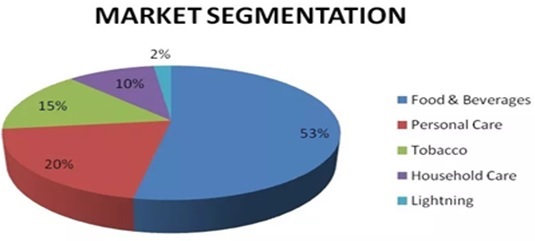

In India, there are three main segments in the FMCG sector:

- Household and Personal Care – 50%

- Healthcare – 31%

- Food and Beverages (F&B) – 19%

Following models of supply chain are present in the FMCG sector

- Manufacturer – Customer (Bata)

- Manufacturer – Dealer – Customer

- Manufacturer – Distributor – Dealer – Customer

___

___

_____

HERE ARE FEW DIFFERENT TYPES OF FMCG:

Processed foods: Cheese products, cereals, and boxed pasta.

Prepared meals: Ready-to-eat meals.

Baked goods: Cookies, croissants, and bagels

Fresh, frozen foods, and dry goods: Fruits, vegetables, frozen peas and carrots, and raisins and nuts.

Beverages: Bottled vitamin water, energy drinks, and juices.

Medicines: Aspirin, pain relievers, and other medication that can be purchased

without a prescription.

Cleaning products: Baking soda, oven cleaner, and window and glass cleaner.

Cosmetics and toiletries: Hair care products, toothpaste, and soap.

Office supplies: Pens, pencils, and market

FMCG AND E-COMMERCE

Increased reliance on online purchasing, as well as improved infrastructure and living standards, has provided FMCGs with new distribution channels and prospects.

Shoppers all over the world are increasingly buying products they need online because it provides advantages that traditional retailers cannot, such as doorstep delivery, a large selection, and reasonable costs.

FMCG AND E-COMMERCE

The online market for grocery and other consumable products is expanding as companies rethink delivery logistics efficiency to reduce delivery times.

While non-consumables may continue to outnumber consumables in terms of volume, improvements in transportation efficiency have expanded the usage of e- commerce channels for FMCG acquisition.

INFLUENCE ON PRICES

FMCG goods are sold to the end consumer based on Maximum Retail Price (“MRP”), which is inclusive of all taxes, including the GST.

Any reduction in rate of tax on any supply of goods or services, or the advantage of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices, according to Section 171 of the CGST Act, 2017 which provides for anti- profiteering measure.

Impact of GST on FMCG

Since FMCG products typically include repeat and daily usage items, taxes on the same have repercussions not only for industry participants but also the massive consumer base.

Under the pre-GST regime, this industry has faced multiplicity of taxes such as excise duty, entry tax as well as different state VATs & in addition, CST on interstate transactions. There was cascading effect of taxes. Further, the set-off of excise and service tax was not available against VAT and CST which added to the cost

GST has resulted in reduction in costs, as GST paid across the supply chain (including manufacturing stage) on inputs as well as on input services is available for setoff against GST on supply of goods.

The companies began revising their rates and prices in response to the GST implementation, which benefited the factory by reducing costs, the distributors by reducing transportation costs, and, of course, the consumers by obtaining products at a lower price because the companies began to revise their prices.

Few popular exemptions in the FMCG sector:

Notification 2/2017 – CT(R) dt. 28.06.2017, as amended, prescribes the goods which are wholly exempt from payment of tax. Products belonging to FMCG: –

- Vegetables, whether fresh or chilled; fresh fruits; nuts such as almonds, pistachios, whether shelled or peeled;

- Milk, curd, butter milk;

- Contraceptives;

- Fabrics such as raw silk, uncombed wool, khadi yarn, etc.

Rate rationalization

The biggest challenge since the GST implementation for the FMCG and retail sector has been the effective rate of tax. While GST was expected to simplify taxation and bring uniformity, the different tax rate slabs and higher rates for consumer durables led to an increase in the cost of some items of mass consumption.

Given the same, the GST council has been working on rationalization of rates. In a recent GST council meeting6 broad rate reductions were introduced with a specific focus on products such as sanitary napkins, domestic electrical appliances/ white goods (food grinders, mixers, shavers, hair dryers etc.). Businesses continuously need to analyze the impact of the rate rationalization, especially from an anti-profiteering perspective.

Exposed to Multiple Tax Rates

FMCG industry is exposed to multiple tax rates (5%/ 12% / 18%) which has complicated the taxation system.

Unwarranted classification disputes due to classification based on specification and composition of the product. Aerated drinks (28% + cess) fruit-juice based drinks (12%), served in a restaurant 5% with no ITC; Industrial usage water (18%) v drinking water other than one sold in sealed container (Nil).

The Government has indicated that it will continue to work on rationalization of rates and try to move towards a simplified tax rate structure including merger of slabs.

Classification related issues (medicaments vs. cosmetics) –

The classification of certain cosmetics such as skin care preparations which also have medicinal properties and contain recognized medical ingredients has been historically subject to litigation since medicaments or ayurvedic items are taxed at a lower rate, whereas cosmetics are typically taxed at a higher rate.

The test for determining whether a preparation can be classified as a medicament or not depends upon whether it is meant primarily for use in treatment of skin disorders or diseases and whether the ingredients therein have known or recognized therapeutic value or not.

While there is an advance ruling on this issue that discusses some of the jurisprudence under the previous regime, and sets out some principles on how preparations can be classified as medicaments, a clarification in this regard with more concrete parameters could go a long way in ensuring consistent treatment and minimal disputes. However, there is difficulty in providing absolute guidance as the products are themselves unique in nature.

Composite vs Mixed Supply

> Supply of two or more goods may be naturally bundled (composite supply) or may not be naturally bundled but supplied for single consideration (mixed supply).

> The character of the supply involving bundle of goods, whether composite or mixed supply, is important for ascertaining the rate of tax applicable on such supply. Sec. 8 defines how such supplies are to be taxed.

> Combo of Toothpaste with Toothbrush; Shampoo with Soap, etc. What tax rate should be applicable on the single consideration charged?

> Goods are normally not naturally bundled as they are capable of being sold independently. A common example of composite supply can be – supply of charger along with electric shaver/trimmer.

> Artificial bundling of goods in FMCG sector is very common. During the festive season, several packaged foods and beverages are artificially bundled together and sold as a package for single price as gift items. If the invoice does not mention the consideration for each product separately, the concept of mixed supply shall become applicable, and the single price shall be taxed at the highest rate.

> Usually, the stores specify the price separately for each item on the invoice and apply tax rate individually.

2(74) “mixed supply” means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply;

Illustration: A supply of a package consisting of canned foods, sweets, chocolates, cakes, dry fruits, aerated drinks and fruit juices when supplied for a single price is a mixed supply. Each of these items can be supplied separately and is not dependent on any other. It shall not be a mixed supply if these items are supplied separately.

VALUE OF SUPPLY

Section 15 provides for the Value of Supply leviable to tax under the charging section. Value of supply is the transaction value, which is the price actually paid or payable for the supply of goods where the supplier and the recipient are not related, and the price is the sole consideration. . Otherwise, value of supply is to be determined as per the Valuation Rules.

Section 15(3): The value of the supply shall not include any discount which is given–

(a) before or at the time of the supply if such discount has been duly recorded in the invoice issued in respect of such supply; and

(b) after the supply has been effected, if–

(i) such discount is established in terms of an agreement entered into at or before the time of such supply and specifically linked to relevant invoices; and

(ii) input tax credit as is attributable to the discount on the basis of document issued by the supplier has been reversed by the recipient of the supply.

Place of Supply – International supplies

No specific provisions for FMCG Sector.

Section 11 of the IGST Act prescribes the Place of Supply of Goods imported into, or exported from India.

POS of goods imported into India shall be the location of the importer.

POS of goods exported from India shall be the location outside India.

Sec. 2(5) “export of goods” with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India;

Export of goods, or Supply of goods to SEZ for authorised operations qualifies as Zero-rated supply under GST u/s 16(1) of the IGST Act.

Place of Supply – Domestic supplies

No specific provisions for FMCG Sector.

Section 10 of the IGST Act prescribes the Place of Supply of Goods other than in the course of Import or Export

Broadly speaking, where two parties are involved, Place of Supply is the location where movement of goods terminates for delivery to the recipient. [Sec. 10(1)(a)]

Where three parties are involved (bill to ship to), Place of Supply of the first sale is the location of the person on whose direction the goods are delivered to the third person. [Sec. 10(1)(b)]

Over the Counter [OTC] sales of FMCG products to consumers is treatable as an intra-state supply, liable to CGST + SGST.

Time of Supply – As applicable to Goods

No specific provisions for FMCG Sector.

Section 12 provides that the time of supply of goods shall be the earlier of the following dates, namely:-

The date of issue of invoice or the last date on which he is required u/s 31 to issue the invoice with respect to supply; or

The date on which supplier receives the payment with respect to the supply

Notification 66/2017 – CT dt. 15.11.2017 has prescribed that all taxable persons are required to pay GST on outward supply of Goods at the time of issue of invoice or the last date on which they are required to issue the Invoice. Tax is not payable on advance.

Input Tax Credit

Section 16(1): Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person.

Like any industry, suppliers in the FMCG industry are entitled for ITC of goods or services used by them in the course or furtherance of their business. Other provisions of Section 16 (conditions), 17 (proportionate availment; blocked credits) and 18 (special circumstances) are equally applicable.

Blocked Credit – 17(5)(h)

(5) Notwithstanding anything contained in sub-section (1) of section 16 and subsection (1) of section 18, input tax credit shall not be available in respect of the following, namely:-

(h) goods lost, stolen, destroyed, written off or disposed of by way of

gift or free samples; and

Marketing/ discount schemes

While all business has to offer different types of marketing schemes and offers, in the FMCG and retail the industry is structured in a way that the manufacturers/ importers offer a variety of pre- and post-sale discounts nd incentives, free samples etc. to dealers/ distributors. While the industry players, during implementation of

♦ GST have taken positions relating to different types of marketing schemes, a conclusive clarification on the same is still not available. Further, in some States, officers at the ground level have also commenced raising ueries relating to the practices adopted. Key issues pertaining to the same are as follows: Tax treatment of different types of schemes –

♦ There are diverse range of schemes offered by FMCG and retail players to its distribution network, and due to the ecosystem, these keep evolving. Various categories of such transactions are as follows: –

♦ Post-sale discounts such as price discount, purchase based schemes, category growth, trade discount, turnover target discounts – Special discounts such as festival price discount, liquidation support and other seasonal rebates Merchandiser support, visibility allowance and security deposits received from exclusive outlets Corporate or bulk buy discounts Other allowances such as loading/ unloading allowance, freight allowance and event support the aforesaid schemes can either be cash discount or it could also be additional quantity supply.

♦ It also requires factual examination whether the secondary market schemes qualify as post sale discounts eligible for deduction under section 15(3)(b) or be considered as a ‘subsidy directly linked to price’ under Section 15(2)(e) of the CGST Act. If it qualifies as ‘subsidy directly linked to price’, it would attract GST in the hands of recipient. It is essential to ascertain the tax treatment, ITC impact of different types of schemes, as well as maintain appropriate documentation so that the entire value chain adopts appropriate tax practices.

Volume discounts: Buy more save more offers

Illustration: ‘Get additional discount of 10% if you purchase 10000 pieces of Apple Juice in a year, get additional discount of 20% if you purchase 15000 pieces in a year’

Such discounts are established in terms of an agreement entered into at or before the time of supply. In commercial parlance, such discounts are referred to as “volume discounts”.

Such discounts shall be excluded to determine the value of supply provided they satisfy the parameters laid down in Sec. 15(3), including the reversal of ITC by the recipient of the supply as is attributable to the discount based on credit note issued by the supplier.

Promotional schemes, off take discounts – Company issues promotional schemes and provides off take discounts to stockiest/ retailer wherein on buying some specified quantity of a product, the distributors will get additional quantity of that product free of cost (e.g.. buy 10 items with additional 2 items free).

Further, the chargeable as well as free supplies are mentioned on the face of the same invoice (e.g. it is mentioned 10 units chargeable and 2 units free). Basis the above, the issue under consideration is whether input tax credit is required to be reversed on the goods supplied based on commercial terms without consideration under the said transaction. One view on this issue is that the free goods supplied are not in the nature of ‘gifts’ but are akin to a quantity discount and thus, no input credit reversal should be required for the same. However, this view has to be formally confirmed by the GST authorities.

Free samples given to potential customers/ Gifts to dealers/ distributors – Company distributes its products as a part of marketing initiatives, etc. as free samples or gifts to dealers/ distributors for reaching targets such as gold coins etc. As per Section 17(5)(g), input tax credit shall not available for goods supplied as free samples. While currently, credit reversal is required, industry is representing that credit reversal should not be required as distribution of the said goods as free samples is required for promotion of the sale of these goods and are thus used in course and furtherance of business.

Further, while generating e-way bill for the same, industry should seek clarification regarding the taxable value to be reported on the e-way bill for such FOC supplies. Procedure/ mechanism for computation of credit reversal on account of goods distributed as free samples, used for personal use etc. is not clear in the law. Further, no specific provision is there in the CGST Act for requirement to reverse credit in case of free of cost services (such as free trips to customers on achieving certain targets, etc.).

Combo packs

There are various marketing campaigns operative in this sector to increase customer engagement and combo packs (combinations of different types of products) is a regular phenomenon. For combo packs where price breakup is also shown on the invoice, an issue may arise as to whether the same can be treated as mixed supply (and therefore taxable at highest rate applicable to the individual items) or individual supply (taxable at tax rates applicable to respective individual products).

Given the statutory norm, mere mention of the price breakup on the invoice may not always change the characterization of a mixed supply to an individual supply. However, there is no clarification on the practical constituents of qualifying as a mixed supply and the issue needs to ideally be analyzed based on facts of each situation.

Post-Sales Discounts (with additional obligations)

illustration: FMCG Companies providing additional discounts to retailers

/whole-sellers for undertaking specific brand promotion activities, special

sales drive, etc.

In such scenario, the discount so offered by the supplier is consideration paid (indirectly) by the supplier to the dealer/retailer to undertake such brand promotion activities, and hence this transaction is separate from the original sales (supply) made by the supplier to the dealers/retailers and is to be treated accordingly. Does it have any financial implications except imcrease in aggregate turnover to the extent of brand promotion activity?

Illustration: Retailer displaying the supplier’s products at a prominent place in its shop, or at the top of the counter which can easily catch attention of the customer. Carrying out such an activity by the retailer is an independent supply of service than the regular supply of goods by the supplier to the retailer.

Herein, supplier will be entitled to claim ITC of the GST so charged by the retailer/dealer for the supply of service.

Post-Sales Discounts (without additional obligations)

Illustration: M/s ABC Ltd supplies Paper Boat bottles to Mr. XYZ Ltd at Rs. 1000/- per carton but afterwards M/s ABC Ltd re values it at Rs. 950/-per carton and issues a credit note of Rs. 50/- per carton to M/s XYZ Ltd.

These are the discounts which are not known at the time of supply or are offered after the supply is already over. In such cases, the supplier will not be allowed to reduce original GST liability in terms of Section 15(3) of the CGST Act.

The dealer will not be required to reverse ITC attributable to the tax already paid on such post-sale discount received by him through issuance of financial / commercial credit notes by the supplier of goods, provided dealer pays the value of the supply as reduced by the amount of post-sale discount plus the amount of original tax charged by the supplier.

Loyalty points redemption

Various retailers run different kinds of loyalty schemes where customers accumulate points and subsequently, on purchase of goods, can make full or part payment through the accumulated points. At present, there is some ack of clarity on the treatment of these points. While some treat it as a discount, some choose to pay GST on the entire value of the goods (including the equivalent of points).

The question is whether GST should be paid on the amount after reducing the sum attributable to loyalty points, as it is essentially in the nature of quantity or off-take discount offered to frequent customers (provided the other prescribed conditions are met).

Further, given the extensive supply chain in this industry, the loyalty point redemption transaction through the supply chain also needs to be evaluated to ensure appropriate tax treatment at each leg of the transaction.

Goods return including of expired goods

Return of goods is inevitable in any trade and industry, particularly FMCG where shelf-life of goods is comparatively less.

Sales Returns can be accounted for through following 2 options [Circular 72/46/2018-GST dt. 26.10.2018]:

Option 1: Return by issuing GST credit note u/s 34 or Financial CN if time limit of following September has lapsed; or

Option 2: Treating the return as fresh supply.

Sales returns, customer refunds and other miscellaneous transactions

Excess collection of money from customers – In case of excess collection of money from customers on account of rounding off difference, the issue is as to whether GST to be paid on additional amount recovered. There is no specific relaxation in GST law as regards non-payment of GST on excess amount or net amount collected from customer due to rounding-off difference.

Sales return from a different State – In case of inter-State supply, where goods are returned by customer in a State different from where the goods were issued (say from Delhi), whether credit note (and subsequent tax adjustment) can be claimed by the State which originally invoiced the good (in the absence of receipt back of goods to such State).

Sales return in case of closure of branch/ warehouse in a State – Similarly, where the customer returns goods in different State due to closure of the office/ warehouse of the State from where the invoice was issued (say in Delhi) , whether there would be credit blockage in the State of Delhi on account of making a non-taxable supply from Delhi (in so much so that Delhi would not make any taxable supply of goods in future once returned by the dealer since the goods would be lying at different State).

Refund provided to customers – In certain cases, if the customer is unhappy with the product or in case of an expired/ faulty product, refund is provided to the customers. The issue to be considered is whether the same may be construed as a separate supply liable to GST.

In this case, a position is possible that there is no underlying supply of goods in the course of furtherance of business by the customer is such a scenario and thus, this should not qualify as a separate supply.

Compliance requirements for credit note/ debit notes – Given the quantum of low value high volume of transactions, the requirement for raising one credit note/ debit note per invoice was creating a compliance and administrative nightmare for the industry. Given the same, in order to simplify the compliances, an amendment to the law is issued allowing for issuance of a consolidated debit note/ credit note covering multiple invoices

Return of expired goods

Section 142 of the Central Goods and Service Tax Act, 2017 (CGST Act) prescribes that if goods are returned by a registered person on which duty was paid not prior to 1 January 2017, such returns will be treated as a supply. Separately, where goods are written off or destroyed, input tax credit of such goods will not be available as per

Section 17(5)(g) of the CGST Act. In this regard, as per the letter issued by the GST authorities on return of expired stock8, it has been clarified that ITC taken on expired / damaged go should be reversed basis the aforementioned provision.

Further, on return of goods, a deduction of GST paid cannot usually be claimed since the return occurs after September of the following financial year. The aforementioned clarifications leads to the following issues:

Company is burdened with double tax cost on account of input credit reversal and no deduction of tax paid Section 142 of the Central Goods and Service Tax Act, 2017 (CGST Act) prescribes that if goods are returned by Company is burdened with double tax cost on account of input credit reversal and no deduction of tax paid

It leads to a confusion as to whether the tax credit to be reversed is that of the tax amount to be charged by the returning person or that of the inputs that were consumed in the manufacture of the expired goods.

The ultimate manufacturer of the expired goods, who paid the tax to the Government at the time of the original sale / supply, should not be required to reverse any ITC, at the destruction of the expired goods, as the goods were already tax paid.

The supply chain is extensive and often involves multiple stockiest/ sub-stockiest, maintaining a paper trail in case of sales return (especially of expired stock) may become effort intensive. Further, in case the goods are sold by sub-stockiest to each other (especially across States), there is no way of identifying the original invoices.

Treating return of expired goods as fresh supply

When the manufacturer receives the expired goods, he needs to destroy the expired goods If the return of goods is being treated as fresh supply, this return would be purchase for manufacturer. Manufacturer is required to reverse the ITC which was availed at the time of the receipt of the expired goods u/s 17(5)(h) of the Act.

It is important to note that the ITC which needs to be reversed is the one availed at the time of return of expired goods, however, ITC availed at the time of manufacture of expired goods is not to be reversed.

If the goods are returned as fresh supply under the cover of a tax invoice, interest on reversal of ITC on account of GST credit note is saved.

Fresh supply of time expired goods is supported by CBIC circular 72/46/2018 dated 26.10.2018. Whether the legality of such supply of expired goods can be challenged?

Whether valuation of expired goods u/s 15 can be challenged? In our opinion, it is not a violation of Section 15(1).If a policy exists that in the event of expiry, manufacturer will buy-back the goods?

Input Service Distributor vs. Cross Charge

Under GST, supplies between State registrations of an entity are subject to tax, even if the same is without consideration. In view of this, companies are required to undertake analysis of activities undertaken by Head office for its branches and vice versa; identify the value of such services and discharge tax liability thereon or distribute it in by obtaining an Input Service Distributor registration. The said exercise involves huge effort and time. Further, it leads to complexities and additional GST compliances.

Concept of ISD

ISD is an office of supplier of goods and services. A supplier may have number of establishments located in different States, however, as regards input services, a supplier may insist for obtaining invoices in the name of its one central location, irrespective of which establishment has actually received the services. The purpose could be centralized accounting, centralized payment system, master agreement with head office or for any other reason.

ILLUSTRATION:

XYZ Ltd may have head office in Mumbai and establishments in Delhi, Chennai and Kolkata. Although certain services are received at Delhi, an invoice may be issued in the name and address of Mumbai Head Office. Let’s say a supplier P in Delhi makes an intra-State supply (CGST+SGST) and supplier Q of Gujarat makes an inter-state supply (IGST) to Delhi establishment, however, invoices are raised in the name of corporate office at Mumbai. In GST it is must in order to satisfy the conditions of section 16(2) for claim of credit.

What’s the concept of Cross Charge?

Generally, ISD is a concept used for ‘distribution’ of ITC to one or more supplying units, whereas cross charge is the concept for ‘accumulation’ of ITC scattered at different location to a central location.

Example of Cross Charge:

ABC India has a plant at Maharashtra, but representative offices at Delhi, Chennai, Kolkata and Tamil Nadu which is only engaged in marketing activities. All supplies are happening directly from Plant at Maharashtra to customers across India. In this case, ITC of local taxes (CGST+SGST) in respect of services obtained at local offices at Delhi, Chennai and Kolkata shall be accumulated at those respective offices unless the cross charging is not adopted. If cross charging is adopted, then such offices will do cross charge on their plant at Maharashtra for business support services and consequently, accumulated ITC at those offices will be used effectively.

E-way Bill

The generation of an E-way Bill is required under the GST regime to transfer any consignment of products with a value over Rs. 50,000, whether it is for sale, job work, or exhibition.

Because of the magnitude of the FMCG sector’s operations, they move a lot of items in a day, whether it’s shipping transactions, client deliveries, or exports. This places a significant burden on the sector to fully comprehend the E-way Bill requirements and assure full compliance with all required documentation.

E-Invoicing

Applicable to taxpayers having aggregate turnover of more than Rs. 50 crores w.e.f. 1.04. 2021.FMCG companies are now required to prepare an e-invoice for each and every supply and this imposes procedural burden on themE-invoicing for B2B supplies and affixing of QR codes on B2C invoices is in addition to the E-way bill requirements.

Area based exemptions/ Benefits under State Industrial policy

In pre-GST regime, industry used to enjoy fiscal benefits in the North Eastern region, Himachal Pradesh, Uttarakhand and J&K in the form of excise duty exemptions/ refunds. Now under GST, those refund benefits have been withdrawn and are proposed to be compensated/refunded as budgetary support. The current proposal restricts refunds to the extent of prescribed percentage of CGST / IGST payout in cash (i.e. after adjusting all input credits) for units in the fiscal benefit zones for area based exemptions whereas percentage of

SGST benefit for State Industrial policy.

This may result in substantial reduction of GST refunds as compared to the present benefits granted and may make certain units unviable. Further, it is to be highlighted that the proposed refund model seems to restrict the eligibility of refund to only actual manufacturers, thereby not addressing concerns related to principal manufacturers who operates through business models such as third party manufacturer (3Ps) and job working arrangements, mainly in Himachal & Uttarakhand. Thus, the quantum impact of such change in the benefit schemes should be carefully evaluated to enable that the principle of promissory estoppel is not deviated from.

Also, if the flow of benefits stand altered (eg. Benefit earned per year in absolute terms remains constant), the question whether this be factored as a cost increase for anti-profiteering purposes needs to be debated. Further, some industry players have filed writ petitions against this reduction in the quantum of benefits, which are currently pending.

Impact of GST on FMCG business costing-

Logistics costs

The GST has put up a positive effect on reducing the logistics cost, which has benefitted the FMCG companies a lot. GST is helping the FMCG companies to save some amount of logistic and transport charges. Previously, the distribution costs was around 2 to 7% of the total cost, but now it has now dropped to 1.5%. Now, at least, the companies save their costs and do more towards the society’s welfare. So, the GST has impacted in a very positive way for companies, as they have made the supply chain management to run smoothly and effectively, in regards to timely payment of tax, correct claims of input credit, and CST removal too. This tax deduction in logistics and transports have benefitted the consumers to avail the company products in much cheaper rates.

Warehouse

Warehouses are used to distribute the goods locally. The finished goods from the factory arrives at warehouses and they get distributed to retailers and customers in the specific areas. Previously, the warehouses were set up on at those states where the effective tax were low, and this also affected the transport costs for the distributors and the manufacturers. But now, the distributors and the manufacturers don’t have to worry about their costs, as GST is helping them to cut their costs. With the execution of GST in the country, the FMCG companies can set up their warehouses anywhere, in any state.

Foreign Investment

The foreign investments has now increased in India. Our country is now a unified market. Thanks to GST. The FMCG goods that are manufactured in India has now become more competitive in the international markets, because of its low production cost. As the GST has reduced its export cost and production cost both. The implementation of GST has lowered almost all taxes and made it easier for manufacturers and business owners to sell in the global and international market without any hassle.

Business Cost

The GST implementation has reduced all taxes and some taxes have been totally removed from the Indian Market and the CST has been removed under the GST regime. The CGST and SGST has replaced many other taxes such as Service Tax, Central Excise Duty, Custom and Octroi Duty etc. You might have noticed these replacements and cost reductions on your restaurant bills, shopping bills. It feels really good, when you see your money is getting saved on your bills. The business cost have also been reduced and totally cut. GST have changed VAT. Now if you are a business owner, you don’t have to pay the different amount of taxes in every state.

Road Ahead

Rural consumption has increased, led by a combination of increasing income and higher aspiration levels. There is an increased demand for branded products in rural India .On the other hand, with the share of unorganised market in the FMCG sector falling, the organised sector growth is expected to rise with increased level of brand consciousness, augmented by the growth in modern retail.

Another major factor propelling the demand for food services in India is the growing youth population, primarily in urban regions. India has a large base of young consumers who form majority of the workforce, and due to time constraints, barely get time for cooking.Online portals are expected to play a key role for companies trying to enter the hinterlands. Internet has contributed in a big way, facilitating a cheaper and more convenient mode to increase a company’s reach. The number of internet users in India is likely to reach 1 billion by 2025. It is estimated that 40% of all FMCG consumption in India will be made online by 2020. The online FMCG market is forecast to reach US$ 45 billion in 2020 from US$ 20 billion in 2017.

It is estimated that India will gain US$ 15 billion a year by implementing GST. GST and demonetization are expected to drive demand, both in the rural and urban areas, and economic growth in a structured manner in the long term and improved performance of companies within the sector.

Important case laws:

[2019] 110 taxmann.com 496 (AAR – KERALA)/[2020] 32 GSTL 105..

GST : Where applicant is an authorized distributor of Castrol India Ltd. (principal company) for supply of Castrol brand industrial and automotive lubricants and principal company is having various rate schemes with dealers and principal company is issuing invoice at a price to its distributors and distributors supplying goods to dealers issue invoice after deducting discount based on various rate scheme pre-fixed by principal company and such discount/rebate is subsequently reimbursed by principal company as commercial credit notes, applicant is eligible to avail input tax credit shown in inward invoice received by it from principal company

Where applicant is an authorized distributor of Castrol India Ltd. (principal company) for supply of Castrol brand industrial and automotive lubricants and principal company is having various rate schemes with dealers and principal company is issuing invoice at a price to its distributors and distributors supplying goods to dealers issue invoice after deducting discount based on various rate scheme pre-fixed by principal company and such discount/rebate is subsequently reimbursed by principal company as commercial credit notes, discount reimbursed by principal company to applicant is liable to be added to consideration payable by customer to applicant to arrive at value of supply under section 15 at hands of applicant

The applicant is liable to pay GST at the applicable rate on the amount received as reimbursement of discount/rebate from the principal company.

003 taxmann.com 1002 (Mumbai – CESTAT)/[2003] 156 ELT 857 (…

[2003] 2003 taxmann.com 1002 (Mumbai – CESTAT) CESTAT, MUMBAI BENCH

Asian Paints (India) Ltd.

section 4(4)(d)(ii) of the Central Excise Act, 1944 – Assessable value – Trade discount – Bonus scheme and Dealer discount scheme – Details of scheme are not known in advance and discount is not given uniformly to all dealers – Not admissible – Appeals rejected (Paras 3, 4, 5 & 6)

2019] 108 taxmann.com 65 (AAAR – TAMILNADU)/[2019] 75 GST 5…

GST: Where a post-purchase discount is extended by supplier of goods or services to appellant MRF Ltd. on account of their registering in interactive automated data exchange arrangement setup by C2FO India LLP, appellant is entitled to avail ITC of full GST charged on undiscounted supply invoice of goods/services by their suppliers

2014] 45 taxmann.com 162 (Karnataka)

HIGH COURT OF KARNATAKA

Maya Appliances (P.) Ltd.

Additional Commissioner of Commercial Taxes, Zone-I*

DILIP B BHOSALE AND B. MANOHAR, JJ.

STA NOS. 120 OF 2012 & 1-10 OF 2013†

MARCH 19, 2014

Section 2(35), read with section 2(34), of the Karnataka Value Added Tax Act, 2003 and rule 3 of the Karnataka Value Added Tax Rules, 2005 – Total turnover – Allowable deductions – Quantity discount – Period April, 2006 to March, 2009 – Assessee-company was engaged in manufacture of home appliances like mixer, grinder, gas stoves, etc. – It allowed quantity discount to its distributors and claimed same as deduction from total turnover while arriving at taxable turnover – Quantity discount was by way of incentive to distributors for doing good business during 3-6 months prior to date of sale and it was not relatable to sale of goods reflected in sale invoice – Whether in terms of rule 3(2)(c) quantity discount was not allowable as deduction from total turnover – Held, yes [Paras 13 & 14] [In favour of revenue]

Penna Cement Industries Ltd. [2020] 116 taxmann.com 876 (AAR- TELANGANA)-Place of Supply in case of Ex-Factory Sales-Section 10(1)(a) of IGST Act, 2017

Held-In case of ex-factory inter-State sales affected by applicant, goods are made available by the supplier to the recipient at the factory gate, but this is not the point where movement terminates since the recipient subsequently assumes the charge for transportation of the goods up to the destination in another state. Thus, termination of the movement of goods evidently takes place at the location (in a different state) to which the goods are consigned/destined and such movement is effected by the recipient or by any other person such as transporter authorized by the recipient.

Applying the inference made by us in the preceding para to the facts of the case on hand, the place (in the other state) where the goods are destined turns out to be the ‘place of supply’ in terms of section 10(1)(a) ibid. Consequently, the ‘location of supplier’ and the ‘place of supply’ fall under different states and the supply qualifies as inter State supply. Accordingly, it was held that, supplier in the stated instance is liable to charge IGST in respect of ex-factory inter-State supplies made by them.

N.V.K. Mohammed Sulthan Rawther and Sons and Willson [2019] 101 taxmann.com 24 (Kerala)

1. Question before the High Court

Can the State Tax Officer invoke Section 129 of the Act and detain goods on the ground the tax paid on the product is less?

2. Fact:

Petitioner consigned a load of Roja betel nut to its dealer, through tax invoice dated 22.09.2018 alongwith eway bill with “HSN 0802”, and paid the tax at 5%. On 26.09.2018 ASTO detained goods, alleging that first petitioner’s product fits the description “HSN 2106” and attracts 18% tax-not 5%.

3. Contention of the Petitioner:

The consignment carried all the valid documents and they cannot be accused of evading tax; the worst that can be attributed to them is about the correct rate of tax. Detention power conferred on the officers, either under Section 68 or Section 129, must be exercised only under the circumstances and grounds set out in those provisions.

The dispute about the rate of tax is not a matter for adjudication in a proceeding under Section 68 or 129 of the GST Act. Section 122 of the GST Act defines the offences warranting imposition of penalty. Misclassification of goods in the invoice, according to him, is not an offence falling under either Section 122, 67, or 68 of the Act.

The adjudication of the rate-issue is a matter to be undertaken by the assessing officer alone, but not by the inspecting officials exercising powers under Sections 67, 68, 69 or 129 of the CGST Act/ KGST Act, 2017 relying upon the judgement in the matter of Rams v. STO [1993] 91 STC 216.

4. Contention of the Respondent

ASTO has plenary powers under that Section to intercept any goods and detain them on any ground enumerated in Section 129 of CGST Act, 2017. ASTO’s entertaining a doubt about the misclassification and the exigibility of tax at a particular rate cannot be assailed.

5. Discussion by the Court

A literal reading of Section 129 of the Act presents a different picture and, perhaps, lends support to the State’s view. But purposive interpretation and the practical commercial considerations trump that view.

J.K. Synthetics Ltd.v. CTO 1994 taxmann.com 370 (SC)

Apex Court held that a dealer must deposit full tax due, based on the information furnished and that information must be correct and complete to the best of the dealer’s knowledge and belief. If the dealer has furnished full particulars regarding his business, without wilfully omitting or withholding any particular information affecting the assessment of tax, and if he honestly believes to be ‘correct and complete’, the dealer is said to have acted ‘bona fide‘ in depositing the tax due and filing the return. Of course, the tax so deposited is to be deemed to be provisional and subject to necessary adjustments under the final assessment. The court finally held that if the assessee pays the tax, which according to him is due based on the information supplied in his return, there would be no default on his part to meet his statutory obligation. Therefore, it would be difficult to hold that the ‘tax payable’ by him ‘is not paid’ and that he is liable for consequences.

Rams v. STO [1993] 91 STC 216

The matter in the given case was regarding situations where there is a genuine dispute of whether there was any taxable sale or not. The court observed that it is not for check-post authority to act on mere suspicion and to find that there is any attempt at evasion of payment of tax, which alone vests him with the jurisdiction to act under S. 29A. At best, he can only alert the assessing authority in Ernakulam to initiate proceedings for assessment of any alleged sale, at which the petitioner will have all his opportunities to put forward his picas on law and on fact. The process of detention of the goods at the check post, cannot be resorted to in such cases when there is a bona fide dispute regarding the very existence of a sale and exigibility for tax. S. 29 A is not intended to subserve such an object.

6. Findings

In light of Judgement of Apex Court in the matter of J .K. Synthetics: The petitioner has declared the HSN Code he has felt his product would attract and paid the tax accordingly. The returns are very much on record before the assessing officer. Therefore, to that extent the first petitioner’s conduct cannot be faulted, nor can he be accused of evading the tax.

In light of Judgement of Kerala High Court in the matter of Rams: If the inspecting authority entertains any suspicion that there is an attempt to evade tax, they can at best alert assessing authority to initiate the proceedings “for assessment of any alleged sale, at which the petitioner will have all his opportunities to put forward his pleas on law and on fact.” The process of detention of the goods cannot be resorted to when the dispute is bona fide, especially, concerning the exigibility of tax and, more particularly, the rate of that tax.

7. Held: The case falls within the adjudicatory ambit of both J.K. Synthetics Limited (supra) and Rams and accordingly detention was held to be arbitrary and unsustainable, and set aside. As a result, the Assistant State Tax Officer was required to release the goods.

*****

Authors name: M.S. VIJAYAKUMAR

Qualification: M.COM. B. ED.M.B.A.M. PHIL.HDNC.,

OCCUPATION: ASSISTANT COMMISSIONER GST (RETD.)

Location: MADURAI TAMILNADU. Author can be reached in 9442022874; 8838052001

mail4rvijay@gmail.com; sva_vijay@yahoo.com about the author

- The author has more than 30 years of Experience in the state commercial/GST department

- The author is interested in giving lectures on indirect taxation, management, accounting AND other motivational areas.

- Wrote articles in a e-journal published from Hyderabad.

- Delivered lectures on Tamilnadu General Sales Tax Act CST Act Entertainment Tax ACT VAT ACT.

- Master trainer on GST and delivered lectures on GST in all areas to Officers and the author gave lectures on GST in various Arts and Science Colleges in tamilnadu.

- Gave more than 15 webinars during covid pandemic period.

- He is also a part time faculty in the Department of Management Studies/Commerce in Madurai Kamaraj University since 1998.

- Attending regularly various GST webinars, zoom meeting conducted by various NIRC’s voice of CA, and in different forums.

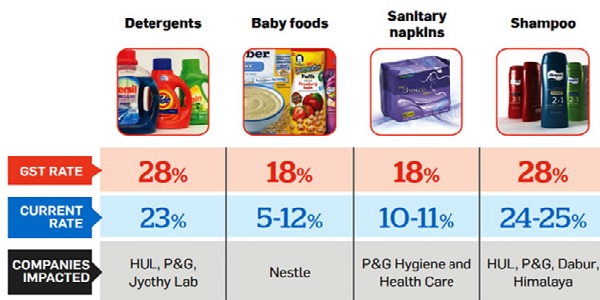

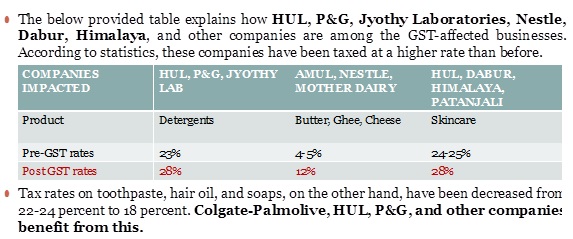

28% slabs are for sins and luxury items. The chart is misleading or wrongly shown. Detergent, face creams comes under 18% earlier it was higher and different in different states. Again butter in north it was 5% vat and 18.5% in South, since igst it’s one tax across 12% with ITC across. That’s what it meant to be.

The case laws mentioned are of cements, tyres etc not of fcmg products.