Recently it is a matter of contention between the GST Intelligence and The Flour Mills whether ‘Crushing of whole, unpolished Grain” service provided to Governments shall be liable to GST as a supply of services or not. In this regard, the following are the legal submissions of the author on the basis of the various rulings and facts –

Facts –

1. The Owner of wheat (State Govt.) will send to the Flour Mills the whole, unpolished food grain for processing.

2. The Flour Mill will return the grain after crushing.

3. The processed grain may be used for various purposes i.e. for commercial sale or for distribution through the Public Distribution System (PDS).

4. The State Govt. will retain ownership of the grain.

5. The Flour Mills deliver the crushed food grains packed in the manner as the recipient (State Govt.) requires.

6. The packing material is supplied by the Flour Mills.

7. Vitamin (Fortification) is also added to the Crushed Flour.

8. The Flour Mills is therefore making supply of a bundle consisting of the service of crushing the grains and supply of materials required to pack the crushed grains, where the former is the predominant supply.

9. They are supplied in conjunction with each other in the ordinary course of business as food grain cannot be transported without proper packing. It is, therefore, a composite supply of goods and services where service of crushing food grains is the principal supply and providing packing materials is ancillary to it

10. The terms of the agreement with the recipient is such that it binds both the supplier and the recipient in a way that neither can divert the food grains to any use other than distribution through PDS, the Applicant’s supply can be related to distribution through PDS, which is covered under Entry No. 28 of the Eleventh Schedule of the Constitution. It will be an activity in relation to a function entrusted to a Panchayat under article 243G of the Constitution, and its supply to the State Government should be exempt under Sl No. 3A of the Exemption Notification, provided the proportion of the packing materials in the composite supply in value terms does not exceed 25%.

11. The packaging also very clearly states “For PDS..” Hence furthermore, the supplier and the recipient cannot divert the food grains to any use other than distribution through PDS.

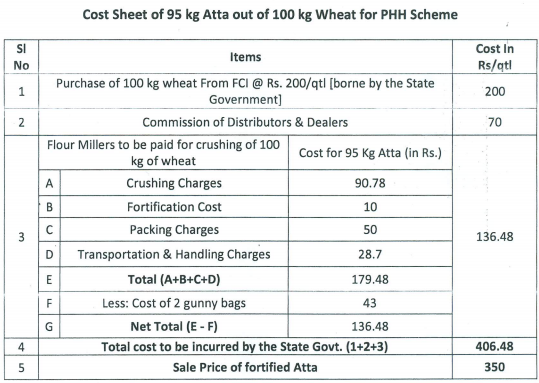

The cost sheet as laid down by Govt. of West Bengal for PHH Scheme is as follows –

12. The Government sends 100 Kgs of Wheat for Crushing to the Millers.

13. 100 kgs would tentatively produce 95 Kgs of Flour

14. 10 is paid for Fortification i.e. addition of vitamins

15. 50 is paid for packaging bags

16. The Consideration for Crushing, Fortification, Packing and Transportation for Atta is Estimated to be calculated at Rs 179.48.

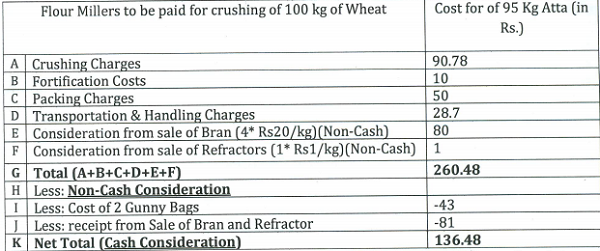

17. The cost of Bags used by the State Government for furnishing the wheat to the Milling Company is sold by the Milling Company in open market @Rs.43. The expected compensation received from sale of gunny bags is reduced as they are equivalent to consideration other than cash.

18. Hence the cash Consideration paid for crushing is Rs.136.48

19. Furthermore there are 4 Kgs of Bran and 1 kg of refractor generated as by product which is sold in open market realising Rs 81/Quintal.

Hence the final calculation for the Four Mill Owners is as follows –

Legal Documents –

1. Circular No 51/35/2018 states as follows –

..service tax exemption at serial No. 25(a) of notification No. 25/2012 dated 20.06.2012 has also been substantially, although not in the same form, continued under GST vide Sl. No. 3 and 3A of the notification No. 12/2017- CT (R) dated 28.06.2017.

| Sl. No.25(a):

Services provided to Government, a local authority or a governmental authority by way of water supply, public health, sanitation conservancy, solid waste management or slum improvement and upgradation |

Sl. No. 3:

Pure services (excluding works contract service or other composite supplies involving supply of any goods) provided to the Central Government, State Government or Union territory or local authority or a Governmental authority or a Government Entity by way of any activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243 W of the Constitution. |

| Sl. No. 3A:

Composite supply of goods and services in which the value of supply of goods constitutes not more than 25 per cent. of the value of the said composite supply provided to the Central Government, State Government or Union territory or local authority or a Governmental authority or a Government Entity by way of any activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243 W of the Constitution. |

2. Exemption under SI No. 3 or 3A of Notification No 12/2017 CT (Rate) dated 28/06/2017 states as under –

| 3 | Chapter 99 | Pure services (excluding works contract service or other composite supplies involving supply of any goods) provided to the Central Government, State Government or Union territory or local authority or a Governmental Authority 16[or a Government Entity] by way of any activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243W of the Constitution. | Nil | Nil |

| 17[3A | Chapter 99 | Composite supply of goods and services in which the value of supply of goods constitutes not more than 25 per cent. of the value of the said composite supply provided to the Central Government, State Government or Union territory or local authority or a Governmental authority or a Government Entity by way of any activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243W of the Constitution. | Nil | Nil] |

3. In the case of SAKSHI JHAJHARIA, AUTHORITY FOR ADVANCE RULING, WEST BENGAL held –

..The Applicant intends to deliver the crushed food grains packed in the manner the recipient requires. The packing material is supplied by the Applicant. The Applicant is, therefore, making supply of a bundle consisting of the service of crushing the grains and supply of materials required to pack the crushed grains, where the former is the predominant supply. They are supplied in conjunction with each other in the ordinary course of business as food grain cannot be transported without proper packing. It is, therefore, a composite supply of goods and services where service of crushing food grains is the principal supply and providing packing materials is ancillary to it – The Applicant intends to make the composite supply to the State Government. The recipient is, therefore, the State Government.

It will be an activity in relation to a function entrusted to a Panchayat under article 243G of the Constitution, and its supply to the State Government should be exempt under Sl No. 3A of the Exemption Notification, provided the proportion of the packing materials in the composite supply in value terms does not exceed 25%.

Legal Issues & Submissions –

In the instant case –

- The cost of goods (packaging charges and vitamins) compromises of Rs.50/- plus Rs.10/-. Hence the total cost of goods in the supply is Rs.60

- The Cost of packing material is 19.2%

- The Cost of packing material and fortification is 23.03%

There is a Composite supply of goods and services in which the value of supply of goods constitutes less than 25% of the value of the said composite supply provided to the State Government or a Governmental authority. The distribution through PDS is covered under Entry No. 28 of the Eleventh Schedule of the Constitution. It is an activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243W of the Constitution.

Hence, it was accordingly held by The Authority of Advance Ruling in West Bengal that the said activity of “Crushing of whole, unpolished wheat” should be exempt under Sl No. 3A of the Exemption Notification.

In view of the above, it appears that GST is not applicable on Flour Mills for Crushing of wheat into Fortified Atta under The Govt. Scheme for PDS. MoF Govt. of WB has already moved for issuing necessary clarification. The same has been laid down by The Special Secretary to The Govt. of West Bengal.

Notwithstanding the above, it may be contended by the revenue that it would be a service covered under any of the below heads of Notification No 11/2017 CGST (R) –

| 26 | Heading 9988

(Manufacturing services on physical inputs (goods) owned by others) |

(i) Services by way of job work in relation to-

(a) Printing of newspapers; 6[(b) Textiles and textile products falling under Chapter 50 to 63 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975);] 22[(c) all products 58[, other than diamonds,] falling under Chapter 71 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975);] (d) Printing of books (including Braille books), journals and periodicals; 23[(da) printing of all goods falling under Chapter 48 or 49, which attract CGST @ 2.5per cent. or Nil;] (e) Processing of hides, skins and leather falling under Chapter 41 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975). 36[(ea) manufacture of leather goods or footwear falling under Chapter 42 or 64 in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) respectively;] (f) all food and food products falling under Chapters 1 to 22 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975); (g) all products falling under Chapter 23 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975), except dog and cat food put up for retail sale falling under tariff item 23091000 of the said Chapter; (h) manufacture of clay bricks falling under tariff item 69010010 in the First Schedule to the Customs Tariff Act, 1975 (51of 1975);] 7[Omitted] 34[(i) manufacture of handicraft goods. Explanation. – The expression “handicraft goods” shall have the same meaning as assigned to it in the notification No. 32/2017-Central Tax, dated the 15th September, 2017 published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 1158 (E), dated the 15th September, 2017 as amended from time to time.] |

2.5 | – |

| 25[(ia) Services by way of job work in relation to-

(a) manufacture of umbrella; (b) printing of all goods falling under Chapter 48 or 49, which attract CGST @ 6per cent. |

6 | -] | ||

| 58[(ib) Services by way of job work in relation to diamonds falling under chapter 71 in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975); | 0.75 | – | ||

| (ic) Services by way of job work in relation to bus body building;

65[Explanation- For the purposes of this entry, the term “bus body building” shall include building of body on chassis of any vehicle falling under chapter 87 in the First Schedule to the Customs Tariff Act, 1975.] |

9 | – | ||

| (id) Services by way of job work other than (i), (ia), (ib) and (ic) above; | 6 | -] | ||

| 8[(ii) Services by way of any treatment or process on goods belonging to another person, in relation to-

(a) printing of newspapers; (b) printing of books (including Braille books), journals and periodicals. 26[(c) printing of all goods falling under Chapter 48 or 49, which attract CGST @ 2.5 per cent. or Nil.] |

2.5 | – | ||

| 27[(iia) Services by way of any treatment or process on goods belonging to another person, in relation to printing of all goods falling under Chapter 48 or 49, which attract CGST @ 6per cent. | 6 | –] | ||

| 35[(iii) Tailoring services. | 2.5 | – | ||

| (iv) Manufacturing services on physical inputs (goods) owned by others, other than (i), (ia), 58[(ib), (ic), (id),] (ii), (iia) and (iii) above. | 9 | –] |

Author Bio

Informative article sir