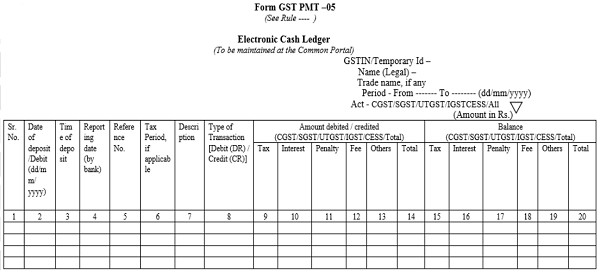

Electronic Cash Ledger

- The electronic cash ledger under sub-section (1) of section 49 shall be maintained in FORM GST PMT-05 for each person, liable to pay tax, interest, penalty, late fee or any other amount, on the Common Portal for crediting the amount deposited and debiting the payment there from towards tax, interest, penalty, fee or any other amount.

- Any person, or a person on his behalf, shall generate a challan in FORM GST PMT-06 (Form attached in Next slide) on the Common Portal and enter the details of the amount to be deposited by him towards tax, interest, penalty, fees or any other amount.

Note:-

1. Reference No_ includes BRN (Bank Reference Number), debit entry no., order no.: if any, and acknowledgment No of return in case of TDS TCS credit.

2. Tax period; if applicable, for any debit will be recorded, otherwise it will be left blank.

3. GS TIN of deductor or tax collector at source, Challan Identification Number (CIN) of the challan against which deposit has been made, and type of liability for which any debit has been made will also recorded under the head “description”.

4. Application no., if any, Show Cause Notice Number: Demand ID, pre- deposit for appeal or any other liability for which payment is being made will also be recorded under the head “description” .

5. Refund claimed from the ledger or any other debits made against any liability will be recorded accordingly.

6. Date and time of deposit is the date and time of generation of CIN as reported by bank.

7. ‘CGST’ stands for Central Goods and Services Tax; cSGST’ stands for State Goods and Services Tax; ‘UTGST: stands for Union territory Goods and Services Tax; ‘IGS7 st2thgt for Integrated Goods and Services Tax and Tess’ stands for Goods and Services Tax (Compensation to States)

Note:- UTR stands for Unique Transaction Number for NEFT/ RTGS payment

Electronic Cash Ledger Refund & Rejection of Refund

- If the refund so claimed is rejected, either fully or partly, the amount debited under sub-rule (10), to the extent of rejection, shall be credited to the electronic cash ledger by the proper officer by an order made in FORM GST PMT-03.

- Where a person has claimed refund of any amount from the electronic cash ledger, the said amount shall be debited to the electronic cash ledger.

Author Bio

Yes if service charges are not more than 20 lacs than no need to get registration under GST. but those who are having registration in existing law need to get registration in GST and after registration they are file application for cancellation of registration.

Refer section-22 of CGST Act-Every supplier shall be liable to be registered under this Act in the State or Union territory, other than special category States, from where he makes a taxable supply of goods or services or both, if his aggregate turnover in a financial year exceeds twenty lakh rupees:

for more clarification you may send email on support@tipsntricksguru.com or goyalmohit28@gmail.com.

I am a retired Railway officer working as Advisor with professional fees of >11Lakhs/yr from this financial year 2017-18. Am I supposed to pay new GST in lieu of the service tax immediately earlier charged @15 %for those whose yearly income of professional fees >10Lakhs/yr each month and reimbursed in next month salary.Now what is rule for new GST? Limit is increased to 20 lakhs and rate increased to 16 or 18%