Six years after the rollout of the biggest indirect tax reform of India, the consistent monthly revenue of Rs 1.5 lakh crore from the Goods and Services Tax (GST) has established itself as the new normal. India implemented the Goods and Services Tax (GST) on July 1, 2017, marking a significant milestone in tax reform. This comprehensive initiative merged various distinct tax jurisdictions, different tax levies, and multiple types of cess and surcharges governed by eight constitutional entries into a unified system.

In pre-GST era, the movement of goods was hindered by barriers such as various e-way bills and checkpoints across the country. However, with the introduction of the unified GST, over 100 different statutes pertaining to value-added tax (VAT), entry tax, entertainment tax, luxury tax, and advertisement tax were replaced. Now, only two statutes remain— one for the intra-state supplies and another for inter-state and international supplies.

The implementation of the e-way bill as a single document for the transportation of goods, along with the removal of check posts, has resulted in a remarkable transformation in logistics operations. This positive change has led to a reduction of over 50 percent in the turnaround time for goods vehicles, consequently decreasing logistics costs.

Moving forward, tax officers are focused on combating fraudulent practices and preventing revenue loss to the exchequer. To apprehend those engaging in fraudulent activities, such as syndicates creating fictitious entities based on forged documents to claim input tax credit (ITC), tax officers have begun utilizing data analytics, artificial intelligence, and machine learning.

GST Revenue Collection

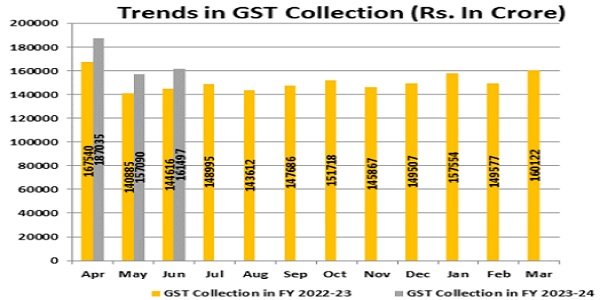

₹1,61,497 crore gross GST revenue collected for June 2023; records 12% Year-on-Year growth Gross GST collection crosses ₹1.6 lakh crore mark for 4th time since inception of GST; ₹1.4 lakh crore for 16 months in a row; and ₹1.5 lakh 7th times since inception

The gross GST revenue collected in the month of June, 2023 is ₹1,61,497 crore of which CGST is ₹31,013 crore, SGST is ₹38,292 crore, IGST is ₹80,292 crore (including ₹ 39,035 crore collected on import of goods) and cess is ₹11,900 crore (including ₹ 1,028 crore collected on import of goods).

The Government has settled ₹36,224 crore to CGST and ₹30269 crore to SGST from IGST. The total revenue of Centre and the States in the month of June, 2023 after regular settlement is ₹67,237 crore for CGST and ₹68,561 crore for the SGST.

The revenues for the month of June, 2023 are 12% higher than the GST revenues in the same month last year. During the month, the revenues from domestic transactions (including import of services) are 18% higher than the revenues from these sources during the same month last year.

It is for the fourth time, the gross GST collection has crossed Rs. 1.60 lakh crore mark. The average monthly gross GST collection for the first quarter of the FY 2021-22, FY 22-23 & FY 23-24 are Rs. 1.10 lakh crore, Rs. 1.51 lakh crore and Rs. 1.69 lakh crore respectively.

The chart below shows trends in monthly gross GST revenues during the current year.

GST Day 2023 celebrated to mark six years of GST

The Sixth GST Day with the vision GST@6 सरलीकृ त कर, सम वकास, commemorating six years of the Goods and Services Tax (GST), was celebrated with great enthusiasm in New Delhi. The event was graced by the presence of distinguished guests, including Hon’ble Union Finance Minister Smt. Nirmala Sitharaman and Hon’ble MoS (Finance) Sh. Pankaj Chaudhary, who inaugurated the celebrations of GST Day 2023. Sh. Sanjay Malhotra, Revenue Secretary, Sh. Vivek Johri, Chairman CBIC, and Sh. Shashank Priya, Member (GST) CBIC were also present at the celebration.

The august gathering at the Vigyan Bhawan, New Delhi was privileged to witness the address by Union Finance Minister Smt. Nirmala Sitharaman, who emphasized the pivotal role of taxpayers as co-equals and the driving force behind the success of the GST regime. Sh. Vivek Johri, Chairman, CBIC, delivered the opening address, shedding light on the transformative journey of GST over the past six years.

As part of the GST Day 2023 celebrations, officers from various CGST zones across the country shared their experiences and insights on the six years of GST. Additionally, a captivating film titled “GST Leveraging Technology for Nation Building” was showcased, highlighting the pivotal role of technology in revolutionizing GST compliances and bridging the gap between the government and taxpayers through online platforms.

Furthermore, Hon’ble Union Finance Minister Smt. Nirmala Sitharaman inaugurated “तदन” (Pratidin), a web-based daily performance management system implemented in CBIC to monitor crucial tasks, reduce delays, and enhance operational efficiency.

To commemorate the milestone of six years of GST, a melodious song illustrating the positive impact of GST on various stakeholders, including citizens, was composed and performed by officers of the CGST Guwahati Zone. Hon’ble Union Finance Minister Smt. Nirmala Sitharaman felicitated 24 dedicated officers of CBIC on GST Day 2023 for their unwavering commitment and devotion to duty. Sh. Sanjay Malhotra, Revenue Secretary congratulated the awardees and urged the department to focus on three key aspects: Taxpayers, Technology, and Team Work.

The sixth GST Day with the vision GST@6 was a remarkable occasion that celebrated the achievements and progress made in the GST regime over the past six years. The event served as a testament to the collective efforts and continuous commitment of the government and stakeholders in building a simplified tax structure for the nation’s growth and development.

In the Picture above: Hon’ble Union Finance Minister Smt. Nirmala Sitharaman, Hon’ble Union MoS (Finance) Sh. Pankaj Chaudhary and Sh. Sanjay Malhotra, Revenue Secretary inaugurating the GST Day 2023

Finance Minister chaired a Review Meeting of the ongoing Fake Registration drive

Hon’ble Union Finance Minister Smt. Nirmala Sitharaman, took a comprehensive review of the ongoing efforts to combat fraudulent invoicing for GST evasion. The session was attended by Mr. Sanjay Malhotra, Revenue Secretary and Mr. Vivek Johri, Chairman of the Central Board of Indirect Taxes and Customs (CBIC). The Finance Minister received a detailed briefing on the actions taken against counterfeit registrations, with a staggering 11,140 such instances already identified and corresponding measures initiated. The Finance Minister was apprised of the methods being adopted like identity theft of people. She acknowledged the existing measures being undertaken by the ministry, including OTP based verification of Aadhar and pilot of biometric-based Aadhar authentication at the time of registration in high risk cases. The Revenue Secretary and Chairman, CBIC highlighted the extensive use of AI/ML tools to identify potential fake networks. The Finance Minister emphasized the need to bolster the GST registration process using technology to prevent the entry of fraudulent entities into the GST ecosystem. Additionally, she called for a nationwide campaign to explain the objectives of the special drive to weed out fake entities.

In the Pictures above (left to right): Sh. Sanjay Malhotra, Revenue Secretary; Smt. Nirmala Sitharaman, Union Finance Minister; Sh. Vivek Johri, Chairman CBIC

In the Pictures above (left to right): Sh. Vivek Johri, Chairman CBIC; Smt. Nirmala Sitharaman, Union Finance Minister; Sh. Sanjay Malhotra, Revenue Secretary

Notifications

Notification No. 14/2023 – Central Tax (Rate), Notification No. 15/2023 – Central Tax (Rate) and Notification No. 16/2023 – Central Tax (Rate) dated 19.06.2023 issued to extend due date for furnishing FORM GSTR-1, FORM GSTR-3B and FORM GSTR-7 for the tax periods April and May, 2023

The Central Government vide the said Notification No. 14/2023 – Central Tax (Rate), Notification No. 15/2023 – Central Tax (Rate) and Notification No. 16/2023 – Central Tax (Rate) dated 19.06.2023 has extended the due date for furnishing FORM GSTR-1, FORM GSTR-3B and FORM GSTR-7 for registered persons whose principal place of business is in the State of Manipur for the tax periods April and May, 2023 till thirteth day of June, 2023.

> Notification No. 17/2023 – Central Tax (Rate) dated 27.06.2023 issued to extend due date for furnishing FORM GSTR-3B for the month of May, 2023

The Central Government vide the said Notification No. 17/2023 – Central Tax (Rate) dated 27.06.2023 has extended the due date for furnishing FORM GSTR-3B for registered persons whose principal place of business is in the districts of Kutch, Jamnagar, Morbi, Patan and Banaskantha in the state of Gujarat and are required to furnish return under sub-section (1) of section 39 read with clause (i) of sub-rule (1) of rule 61 of the Central Goods and Services Tax Rules, 2017 for the month of May, 2023 till thirtieth day of June, 2023.

Instructions

> Instruction No. 03/2023-GST dated 14.06.2023 issued regarding guidelines for processing of applications for Registration

The Central Government vide the said Instruction No. 03/2023-GST dated 14.06.2023 has issued guidelines for strengthening the process of verification of applications for registration at the end of tax officers in a uniform manner. As the fake registration drive is going on, various instances of unscrupulous individuals obtaining fake or bogus registrations under GST and defrauding the government have been noticed. Such registrations are used to fraudulently pass on input tax credit by issuing invoices without any genuine supply of goods or services. This problem of fake registrations and bogus invoicing has become a serious issue, involving dubious and complex transactions that result in revenue loss. Central and State Tax administrations have detected various methods used to obtain these fake registrations, including misuse of identities and forged documents. To address this problem, Instruction No. 01/2023-GST has been issued for concerted and coordinated action on a mission mode by Central and State tax authorities in the form of a Special All-India Drive against fake registrations.

Accordingly, the following guidelines are issued for strengthening the process of verification of applications for registration at the end of tax officers in a uniform manner:

i. Immediately on receipt of the application for the registration in the Task List of the concerned officer on ACES-GST application, the officer shall initiate the process of scrutiny and verification of the details filled by the applicant in the application for registration in FORM GST REG-01 and the documents uploaded by the applicant along with the said application.

ii. The proper officer shall scrutinize the said documents to ensure that the documents are legible, complete and relevant. Further, the address details and supporting documents provided for principal and additional places of business may be closely examined to ensure accuracy and completeness. To the extent feasible, the authenticity of these documents as proof of address should be cross verified with publicly accessible sources like land registries, electricity distribution companies, municipalities, and local bodies etc.

iii. To facilitate the targeted approach n verification and processing of registration applications, the Directorate General of Analytics and Risk Management (DGARM) and GSTN are conducting risk rating assessments using data analytics and risk parameters. This risk rating, categorized as High, Medium, or Low, is provided to CGST field formations through Report Series 400 on the DDM portal on regular basis. Proper officers should consider this risk rating while verifying and processing applications, with particular focus on cases assigned a “High” risk rating.

iv. The proper officer should verify if the registration has been previously obtained on the same PAN, either within the same state or in other states, and check the PAN’s status and compliance record of the said GSTINs from the portal. Special attention should be given to cases involving circumstances such as previous cancellations or suspensions of the registrations or any previous rejections of registration application on the applicant’s PAN, place of business based on local risk parameters, and suspicious/doubtful proof of address of business on the basis of scrutiny of the application and the documents.

v. The proper officer shall issue a notice to the applicant electronically in FORM GST REG-03 within the prescribed time limit, where the application is found to be deficient.

vi. The proper officer may seek clarification/information/documents where any document is not legible or is incomplete, the address of place of business does not match with the document uploaded or the document does not appear to be valid, the address of place of business is vague or incomplete, any GSTIN linked to the PAN of the applicant is found cancelled or suspended.

vii. The proper officer will carefully examine Form GST REG-04 furnished by the applicant in response to the notice issued in Form GST REG-03. If satisfied, the officer will approve the registration within the prescribed time. If not satisfied, the officer will reject the application and inform the applicant in writing through Form GST REG-05. Where no reply is furnished within the prescribed time, the officer may also reject the application and inform the applicant through Form GST REG-05.

viii. The proper officer must ensure that the said notice in FORM GST REG-03 is issued electronically within a period of seven working days from the date of submission of the application in cases where the applicant has undergone Aadhaar authentication.

ix. The proper officer shall immediately initiate the process for physical verification of the place of business in accordance with the provisions of the CGST Rules, where the applicant either failed to undergo or did not opt for Aadhar authentication.

x. In cases where the proper officer deems it necessary to physically verify the place of business for authenticity, even if the applicant has undergone Aadhaar authentication, the officer may conduct physical verification in a time-bound manner. Until the functionality for marking an application for physical verification in Aadhaar authenticated cases is available on the portal, the Centralized Processing Centre officer can coordinate with jurisdictional officers for conducting physical verification.

xi. While processing registration applications, the proper officer will ensure timely rejection, acceptance, or query raising. Registration granted on deemed approval basis or registration assigned with high-risk ratings in DGARM Report Series 400 require immediate communication to jurisdictional Commissionerate for post-registration physical verification within 15 days. Commissionerates may conduct physical verifications based on risk parameters and reports provided by DGARM to verify authenticity. Non-existent or fictitious registrations should be addressed promptly. Strict action will be taken for gross negligence by officers.

xii. The Principal Chief Commissioner/Chief Commissioner of CGST Zones may closely oversee the processing of registration applications and physical verifications within their zones. If any application is granted deemed approval, the reasons should be examined for subsequent timely remedial action in a time bound manner.

GST Portal Updates

> Advisory for e-invoice Verifier App by GSTN

1. The e-invoice Verifier App developed by GSTN, has been introduced which offers a convenient solution for verifying e-invoices and other related details. GSTN understands the importance of efficient and accurate e-invoice verification, and this app aims to simplify the process for your convenience.

2. e-invoice Verifier App – Key Features and Benefits:

i. QR Code Verification: The app allows users to scan the QR code on an e-invoice and authenticate the embedded value within the code. This helps in identifying the accuracy and authenticity of the e-invoice.

ii. User-Friendly Interface: The app provides a user-friendly interface with intuitive navigation, making it easy for users to navigate through the app’s features and functionalities.

iii.Comprehensive Coverage: The app supports verification of e-invoices reported across all six IRPs, ensuring comprehensive coverage and convenience.

iv.Non-Login Based: The app operates on a non-login basis, meaning users are not required to create an account or provide sensitive personal information to access its functionalities. This simplifies the user experience and makes it more convenient for users.

> How to use the e-invoice Verifier App:

i. Download the App: Visit the Google Play Store and search for “e-invoice QR Code Verifier.” Download and install the app on your mobile device free of charge. The iOS version will be available shortly.

ii. QR Code Scanning: Utilise the app to scan the QR codes on your e-invoices. The app will authenticate the information embedded in the code and one can compare it with information printed on the invoice.

4. GSTN emphasizes that the e-invoice Verifier App does not require any user login or authentication process. Anyone can freely scan QR codes and view the available information.

5. For more detailed information please see the FAQs in the app. This comprehensive FAQ document will provide you with additional guidance on using the app and resolving any queries you may have.

6. GSTN is dedicated to enhancing your experience with the e-invoice Verifier App and providing a process of seamless e-invoice verification. GSTN is also working towards launching Version 2 with the Search IRN functionality, which will further streamline your e-invoice verification.

> Advisory on Update on Enablement Status for Taxpayers for e-invoicing

1. It is to inform that as per Notification No. 10/2023 – Central Tax dated 10th May, 2023, the threshold for e-invoicing for B2B transactions has been lowered from 10 crores to 5 crores. This change will be applicable from 1st August, 2023.

2. To this effect GSTN has enabled all eligible taxpayers with an Aggregate Annual Turnover (AATO) 5 crores and above as per GSTN records in any preceding financial year for e-invoicing. These taxpayers are now enabled on all six IRP portals including NIC-IRP for e-invoice reporting.

3. You can check your enablement status on the e-invoice portal at https://einvoice.gst.gov.in .

4. It would be in the interest of trade to register and utilize the sandbox testing facility available at the IRP portals. This will help taxpayers to familiarize themselves with the invoice reporting mechanism and ensure a seamless transition to the e-invoice system.

5. Please note that the enablement status indicated on the e-invoice portal does not indicate a legal obligation on taxpayers to use e-invoicing. However, actual liability to generate IRN shall be checked by taxpayers with respect to applicable notification in the light of facts pertaining to them.

6. While the listing of enabled GSTINs is purely based on the turnover criteria reported in GSTR-3B, it is essential for taxpayers to confirm whether they fulfil the conditions outlined in the notification/rules. Thus, it is the legal responsibility of the concerned taxpayer, both buyers and suppliers, to ensure compliance.

7. In case, a taxpayer who is otherwise but not auto enabled on the e-invoice portal, can self-enable for e-invoicing using the functionality provided on the portal.

8. GSTN once again emphasises that all eligible taxpayers should familiarize themselves with the e-invoicing requirements and take the necessary steps to ensure compliance with the new threshold.

> Advisory on Online Compliance Pertaining to Liability / Difference Appearing in R1 – R3B (DRC-01B)

The GSTN has developed a functionality to enable the taxpayer to explain the difference in GSTR-1 & 3B return online as directed by the GST Council. This feature is now live on the GST portal. The functionality compares the liability declared in GSTR-1/IFF with the liability paid in GSTR-3B/3BQ for each return period. If the declared liability exceeds the paid liability by a predefined limit or the percentage difference exceeds the configurable threshold, taxpayer will receive an intimation in the form of DRC-01B.

Upon receiving an intimation, taxpayer must file a reply in Form DRC-01B Part B, providing clarification through reason in automated dropdown and details regarding the discrepancy, if not included in the dropdown.

To further help taxpayer with the functionality, a detailed manual containing the navigation details is available on the GST portal. It offers step-by-step instructions and addresses various scenarios related to the functionality. The link is stated below:

https://tutorial.gst.gov.in/downloads/news/return_compliance_in_form_drc_01b.pdf

In-House Activities

The GST Council Secretariat enthusiastically participated in commemorating the International Day of Yoga on 21.06.2023, promoting physical and mental well-being among its staff members.

The event featured energizing yoga sessions led by experienced instructors, guiding participants through various asanas (postures) and pranayama (breathing exercises). These sessions aimed to enhance flexibility, reduce stress, and promote overall wellness.

Additionally, the celebration included informative discussions on the origins and philosophy of yoga, enlightening participants about its holistic benefits. By observing Yoga Day, the GST Council Secretariat displayed its commitment to fostering a healthy work environment and prioritizing the well-being of its staff. Yoga serves as a powerful tool for stress management and self-care, aligning with the Secretariat’s dedication to maintaining a balanced work-life equilibrium.

We encourage all readers to embrace the principles of yoga, integrating its transformative effects into their daily lives.

Legal Corner

> Quo warranto

Quo warranto is a legal concept derived from Latin, meaning “by what authority.” It is a legal action used to challenge the authority or legitimacy of a person or entity holding a public office, franchise, or position of power. The principle underlying quo warranto is to ensure that those who exercise governmental powers or hold public offices do so lawfully and with the proper authorization.

Quo warranto is employed as a mechanism to inquire into the legal basis or entitlement of an individual or organization to hold a particular position. It can be initiated by the government or any interested party with standing. The purpose is to determine if the person or entity possesses the necessary qualifications and has the right to occupy the office or exercise the powers they claim.

The legal application of quo warranto involves a court proceeding where the challenging party presents evidence to prove that the respondent obtained the position unlawfully, lacks the required qualifications, or has usurped the powers associated with the office. If the court finds in favor of the challenging party, the respondent may be removed from the office, and other appropriate remedies or penalties can be imposed.

Conditions For Issue of Quo Warranto:

1. The office must be a public one and it must be created by the constitution.

2. It must be a substantive one.

3. There must be a contravention in constitution in appointing the person for that office.

Quo warranto serves as a vital legal safeguard to prevent the abuse of power and maintain the integrity of public offices. It ensures that public positions are filled by individuals who meet the necessary legal requirements and are legitimately entitled to hold the office. By examining the authority of those in power, quo warranto reinforces the principles of legality, accountability, and fair governance within a society.

Mistake of Fact

Mistake of fact as a general exception refers to a legal principle that recognizes that a person may not be held fully responsible for their actions if they made a genuine mistake about the facts of a situation. Unlike mistake of law, mistake of fact acknowledges that individuals may have acted in good faith based on their understanding of the circumstances.

The principle behind mistake of fact as a general exception is rooted in the idea that it would be unfair to hold someone accountable for a crime or wrongdoing if they honestly and reasonably believed that their actions were lawful. It recognizes that individuals should not be penalized for their actions if they were operating under a mistaken belief about key facts.

The legal application of this principle involves considering the state of mind and belief of the individual at the time the offense was committed. If it can be shown that the person had a genuine and reasonable belief in a set of facts that, if true, would render their actions lawful, then their mistake of fact may serve as a defence. However, it is important to note that the mistake must be both honest and reasonable, meaning that it should be one that a reasonable person in a similar situation would have made.

The usage of mistake of fact as a defence varies depending on the jurisdiction and the specific circumstances of the case. It is often invoked in criminal cases where the accused argues that they did not have the requisite intent or knowledge to commit the offense due to a genuine mistake about a material fact.

Overall, mistake of fact as a general exception recognizes that individuals may not be held fully accountable for their actions if they acted in good faith based on a mistaken belief about the facts. It aims to strike a balance between justice and fairness, ensuring that individuals are not unduly punished for innocent or unintended conduct.

Source of Newsletter – https://gstcouncil.gov.in/