GST Council Secretariat, New Delhi

On 26th January, the Country celebrated the 74th Republic Day therein honoring the adoption of our Constitution that has vested the supreme authority of the Republic in “We, the people”. Our country is entering into a crucial phase wherein we as a nation endeavor to achieve an empowered and inclusive economy over the next 25 years in lead up to the 100 years of our Independence.

The Indian Economy is on course of becoming one of the leading economics in the world powered with a young population and the Governments thrust for development of domestic markets thereby aiming to become a production powerhouse. Inclusive development, Technological advancements and productivity enhancements are key elements in achieving this agenda. The GST regime would evidently play an important role in achieving these goals as it has stabilized as a vital revenue source for Central and State governments, with the gross GST collections increasing at 24.8 per cent on YoY basis during April —December 2022. 0n 27th January, 2023 an interactive programme was held in Gangtok, Sikkim wherein the officers of GST Council Secretariat held an interactive session with the State officers and local stakeholders in order to understand the functioning of GST at local ground level. We plan to undertake similar initiatives in future in order to facilitate the stakeholders

GST Revenue Collection

₹ 1,55,922 crore gross GST revenue collected in the month of January, 2023, records 2nd highest Gross GST collection

The gross GST revenue during January, 2023 as on 31.01.2023, till 05:00 PM is ₹ 1,55,922 crore of which CGST is ₹ 28,963 crore, SGST is ₹ 36,730 crore, IGST is ₹ 79,599 crore (including ₹ 37,118 crore collected on import of goods) and cess is ₹ 10,630 crore (including ₹ 768 crore collected on import of goods).

The Government has settled ₹ 38,507 crore to CGST and ₹ 32,624 crore to SGST from IGST as regular settlement. The total revenue of Centre and the States in the month of January, 2023 after regular settlement is ₹ 67,470 crore for CGST and ₹ 69,354 crore for the SGST.

The revenues in the current financial year upto the month of January, 2023 are 24% higher than the GST revenues during the same period last year. The revenues for this period from import of goods are 29% higher and from domestic transaction (including import of services) are 22% higher than the revenues from these sources for the same period last year.

This is for the third time, in the current financial year, GST collection has crossed ₹ 1.50 lakh crore mark. The GST collection in January, 2023 is the second highest next only to the collection reported in April, 2022. During the month of December, 2022, 8.3 crore e-way bills were generated, which is the highest so far and it was significantly higher than 7.9 crore e-way bills generated in November, 2022.

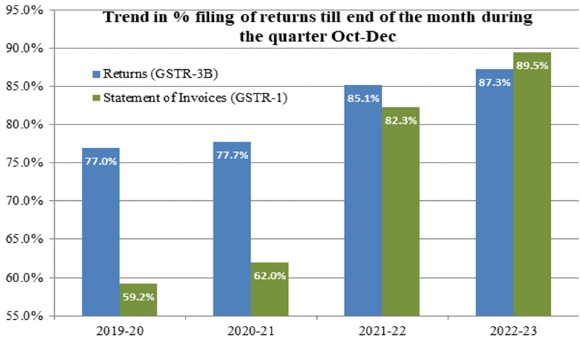

Over the last year, various efforts have been made to increase the tax base and improve compliance. The percentage of filing of GST returns (GSTR-3B) and of the statement of invoices (GSTR-1), till the end of the month, has improved significantly over years. The trend in return filing in the Oct-Dec quarter over last few years is as shown in the graph below. In the quarter Oct-Dec 2022, total 2.42 crore GST returns were filed till end of next month as compared to 2.19 crore in the same quarter in the last year.

This is due to various policy changes introduced during the course of the year to improve compliance.

The chart below shows trends in monthly gross GST revenues during the current year.

Source: PIB Press release dated 31.01.2023

Notifications

> Notification No 01/2023-Central Tax dated 04.01.2023 o assign powers of Superintendent of central tax to Additional Assistant Directors in DGGI, DGGST and DG Audit.

The Central Government vide the said Notification has made amendments in Notification No. 14/2017 – Central Tax dated July 1, 2017 for assigning jurisdiction and power of superintendent to officers of the rank of Additional Assistant Directors in Directorate General of Goods and Services Tax Intelligence (“DGGSTI”), Directorate General of Goods and Services Tax (“DGGST”) and Directorate General of Audit (“DGA”), The relevant extract is as follows:

| Sl. No. | Officers | Officers whose powers are to be exercised |

| 8A | Additional Assistant Director, Goods and Services Tax Intelligence or Additional Assistant Director, Goods and Services Tax or Additional Assistant Director, Audit | Superintendent |

Circulars

> Circular No. 190/02/2023-GST dated 13.01.2023 pertaining to clarification regarding GST rates and classification of certain services.

The Central Government vide the said Circular has clarified that accommodation services provided by Air Force Mess and other similar messes, such as, Army mess, Navy mess, Paramilitary and Police forces mess to their personnel or any person other than a business entity, are covered by Sl. No. 6 of Notification No. 12/2017 – Central Tax (Rate) dated 28.06.2017, if the services supplied by such messes qualify to be considered as services supplied by Central Government, State Government, Union Territory or local authority.

Further, it is also clarified that incentives paid by Ministry of Electronics and Information Technology to acquiring banks under the Incentive scheme for promotion of RuPay Debit Cards and low value BHIM-UPI transactions are in the nature of subsidy and thus not taxable under GST.

> Circular No. 189/01/2023-GST dated 13.01.2023 pertaining to clarification regarding GST rates and classification of certain goods.

The Central Government vide the said Circular has issued clarification regarding GST rates and classification of certain goods based on the recommendations of the GST Council in its 48th meeting held on 17th December, 2022. The key clarifications issued are as follows:

1. No GST to be levied on by-products of milling of Dal/ Pulses such as Chilka, Khanda and Churi/Chuni w.e.f January 1st, 2023

2. ‘Carbonated Beverages of Fruit Drink’ or ‘Carbonated Beverages with Fruit Juice’ would fall under HSN 2202 99 and GST would be levied at the rate of 28% and Compensation Cess at the rate of 12%.

3. Snack pellets (such as ‘fryums’), which are manufactured through the process of extrusion, are appropriately classifiable under tariff item 1905 90 30 and taxable at 18%.

4. Compensation Cess at the rate of 22% is applicable on Motor vehicles, falling under heading 8703, which satisfy all four specifications i.e. these are popularly known as SUVs; the engine capacity exceeds 1,500 cc; the length exceeds 4,000 mm; and the ground clearance is 170 mm and above.

GST Outreach Programmes

> Sikkim outreach programme

On 27.01.2023, an interactive programme was organized jointly by State of Sikkim and GST Council Secretariat with trade and CGST officers. The objective of the program was to understand the issues faced by various stakeholders at ground level while implementing GST and to obtain feedback from trade about their experience.

The programme was hosted by Shri Manoj Rai, Commissioner CTD, State of Sikkim; Ms. Asha Subba, Joint Commissioner; Shri. Dorjee W. Bhutia, Deputy Commissioner and Ms. Pema Lepcha, Deputy Commissioner and attended by eminent stakeholders from the industry.

Shri Manoj Rai, Commissioner, CTD, State of Sikkim, appreciated the initiative of GST Council Secretariat to hold such outreach programs at ground level as it would provide an opportunity for the State and other stakeholders to place their constraints before the authorities.

Shri Pankaj Kumar Singh, Additional Secretary GST Council Secretariat, during the address emphasized on the role played by GST Council Secretariat in acting as a platform between the various stakeholders and he stressed that the office strives to place the various representations received from stakeholders across various States before the competent authority for speedy resolution.

> 3rd Online All India training programme on the topic “48 Meeting of GST Council: Recommendations” under the aegis of New Series “….” (Abhigya) on 11.01.2023.

NACIN, Mumbai conducted 3rd Online All India training program under “…..” (Abhigya) series on 11.01.2023 on the topic “48th Meeting of GST Council: Recommendations”.

There was an overwhelming response from All India CGST formations as well as 16 State Tax formations from Goa, Kerala, Madya Pradesh, Chennai, Rajasthan, Nagaland, Manipur, Himachal Pradesh, Assam, Gujrat, Tamil Nadu, Meghalaya, Bihar Maharashtra, Jammu and Kashmir. Around 1362 officers from CGST and SGST formations have attended the online training sessions.

The objective of this programme was to sensitize the field formations about the Recommendations of 48th Meeting of the GST Council held on 17th December, 2022.

The introduction to the session was given by Shri Rajiv Kapoor, Pr. ADG, NACIN, Mumbai. Shri Arun Mishra, Special Secretary (Retd) and Tax Expert, Govt. of Bihar gave the introductory session wherein he discussed the background and important features of the recommendations given by the members of GST Council in the 48th Meeting.

In the second session, the recommendations of the 48th GST council were discussed in detail by Ms. Ashima Bansal, Joint Secretary, GST Council. She discussed the GIC agenda, Law Committee agenda and Fitment Agenda in detail giving the background of the amendments and also the recommendations of the GST Council Regarding these agendas.

GST Portal Update

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

To view module wise functionalities deployed on the GST Portal and webinars conducted/Videos posted on our YouTube channel, refer to table below:

Portal update on 12.01.2023

> Advisory on taxpayers facing issue in filing GSTR-3B

According to Hon’ble Supreme Court’s directive filing of TRAN forms was made available for aggrieved taxpayers during 01.10.2022 to 30.11.2022. It has been observed that, in the process of filing TRAN forms, few taxpayers have submitted their forms on the portal but did not finally File it within the specified time. After submitting the Tran Forms, only filing was to be done with e-sign. Further, it is seen that such taxpayers have not raised any ticket for difficulty faced by them in filing Tran Forms. Some taxpayers were also contacted by GSTN and they informed that they do not intend to file TRAN forms. As the TRAN forms of these taxpayers are submitted but not filed, these taxpayers are not able to file their GSTR-3B.

The TRAN filing window has already been closed. Hence, such taxpayers are advised to raise a ticket on GST Grievance Portal giving consent that their TRAN filing status may be reset by GSTN. Once the consent for resetting their unfiled TRAN forms is received, the TRAN forms will be reset and the taxpayer will be able to file their GSTR-3B.

Portal update on 16.01.2023

> Advisory on facility of ‘Initiating Drop Proceedings’ of Suspended GSTINs due to Non-filing of Returns

1. If such taxpayers have filed all their pending returns, the system will automatically drop the proceedings and revoke suspension.

2. If the status of the GSTIN does not automatically turn ‘ACTIVE’, then taxpayers are advised to revoke the suspension once the due returns have been filed, by clicking on ‘Initiate Drop Proceeding’ for which navigation is as follows:

“Log on to GST Portal > Services > User Services > View Notices and Orders > Initiate Drop Proceeding”

3. In case the system does not automatically drop the proceedings or taxpayer is unable to revoke the suspension by clicking on ‘Initiate Drop Proceeding’, then taxpayer is advised to contact Jurisdictional Officer.

Note: This functionality is applicable to the taxpayers whose GSTINs have been suspended after 1st December, 2022.

Portal update on 24.01.2023

Legal Corner

> Delegatus Non-Potest Delegare:

The maxim Delegatus Non-Potest Delegare is a principle of administrative law and it means that a person to whom a power has been delegated cannot further sub-delegated that power unless it is provided for by law or the person delegating the authority permits sub-delegation of authority. Pertinently, the maxim does not lay down a rule of law, it is a rule of construction to the effect that a discretion conferred by a statute is prima facie intended to be exercised by the authority on which the statute has conferred it and by no other authority unless so provided.

This principle is an essential corollary to the doctrine of separation of powers (i.e. one organ of the Government cannot encroach upon the powers of another). For example, legislative authority cannot be transferred or delegated to another authority without proper sanction by any superior authority of law. However, there arises situation such as of emergency which necessities such delegation but in such cases the delegated power can be exercised and to the extent to which it is delegated.

The maxim rests on the principle that a person wishes to act through another, confers a power on that other person but this doesn’t imply that the person who delegates such power parts with his power or his authority. Delegation of power would always be abrogated by the grantor at any time.

In order to check excessive delegation of power and to ensure that there is separation of power between various organs of the government, various checks have been devised by the Apex Court in the matter of In re Delhi Laws Act, wherein the Apex court held that there is a limitation on delegation of power and that essential function cannot be delegated.

> Lex Posterior Derogat Priori

Lex Posterior Derogat Priori is a Latin maxim that connotes that a later law repeals an earlier law as in a later statute derogates from a prior. This maxim embodies a principle of statutory interpretation which is to be followed in the case of conflict between two different statutes. The general rule to be followed in case of conflict between two statutes is that the latter abrogates the earlier one. But the later statue must either expressly repeal the earlier one or manifestly reduce the ambiguity of the earlier statue. In other words, a prior special law would yield to a later general law, if either of the two following conditions is satisfied i.e, the two statues in question are inconsistent with each other or if there is some express reference in the later to the earlier enactment. If either of these two conditions is fulfilled, the later law, even though general, would prevail.

This maxim is generally linked with lex specialis derogat generali which means that the special law taken away the effect of a general law. This doctrine implies that if two statues govern the same factual situation, the statue governing the specified subject matter overrides the statue governing the general situation.

In-house Activity

> 74th Republic Day Celebrations in GST Council Secretariat

The 74th Republic Day was celebrated in the office of GST Council Secretariat (GSTCS) with much patriotic fervor. On this occasion the GSTCS organized various events such as Essay writing, Slogan writing and Painting , in order to stir up the patriotic feelings amongst the Officers and staff alike.

The Constitution of India, which was adopted by the Constituent Assembly on November 26, 1949, came into effect on January 26, 1950 the Republic Day is celebrated as a mark of honor. The Constitution of India is an embodiment of people’s faith and aspirations. The Constitution of India is flexible and has stood well in emerging circumstances and situations from time to time, therefore it is often termed as an organic living document. The Constitution was framed to establish the concept of democracy, equality, liberty, not only in the bigger political domain but also in our personal existence. The Indian Constitution is unique in its contents and spirit as it has borrowed several good features and experiences from different Constitutions around the world like the Concept of Fundamental Rights was borrowed from the Constitution of USA and likewise the concept of Directive Principles was taken from Ireland. Our Constitution is a balance between rigidity and flexibility which enables us to sustain the core basic structure while amending some provisions according to changing requirements of the society and this shows that the Constitution has successfully steered us towards the path of advancement.

On this occasion, the Additional Secretary Sh. Pankaj Kumar Singh addressed the officials of GST Council Secretariat and encouraged everyone to participate effectively in the In house events. He also appreciated the efforts of the participants.

Source of Newsletter – https://gstcouncil.gov.in/