GST Network

Ques: What we will get in this post?

Ans: Reason of why there was a need of Amending Constitution of India and how beautifully the Act has been drafted by the Law makers of India.

Considered as one the historic milestone achievement, The Constitution (101st ) Amendment Act, 2016 contains 20

Sections out of which first 10 sections are discussed in detail in this content.

Section 1: Short title and commencement.

(1) This Act may be called the Constitution (One Hundred and First Amendment) Act, 2016.

(2) It shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint, and different dates may be appointed for different provisions of this Act and any reference in any such provision to the commencement of this Act shall be construed as a reference to the commencement of that provision.

ANALYSIS:

(1) The Section seems to be self-explanatory

(2) As this subsection clearly states that CG may appoint different date for bringing into force different sections of the aforesaid act, Using the stated power appointed date for the sections are as follows:

| Sections Notified | Appointed Date | Source |

| 1(2) and 12 | Sep 12’2016 | MOF N/N S.O.2915(E) |

| Remaining Sections | Sep 16’2016 | MOF N/N S.O.2986(E) |

Section 2: Insertion of new article 246A…..Special provision with respect to goods and services

After Article 246 of the Constitution, the following article shall be inserted, namely:-

Explanation:……(Discussed to be discussed after Article 279A(5))

ANALYSIS:

For understanding WHY ARTICLE 246A, let us first understand a bit about the legislative scheme envisaged in our

Constitution by going through few Articles of Constitution of India namely:

“245, 246, 254”

Article 245 states that….

Parliament may make laws for whole or any part of India and

Legislature of a State may make laws for whole or any part of the State.

Article 246 also talks about Legislative power of the Parliament and the Legislature of a State. In short it states that:

| Matters Enumerated in: | Power to Make Law is with |

| List I or the Union List | Parliament/Union |

| List II or the State List | Legislature of any State |

| List III or Concurrent List | The Parliament and the Legislature of any State* |

* “Union Power”will Prevail over “State Power”

The essence of GST is to share power among Centre and States,

thus,

following problems have been done away with:

1) Article 245 gives exclusive power only to one of the two, but we need power to be given to both.

2) Article 246 which gave superior power to Centre over States, but now the sharing is required and not superiority thus for the purpose of this Act, the said article has been overruled.

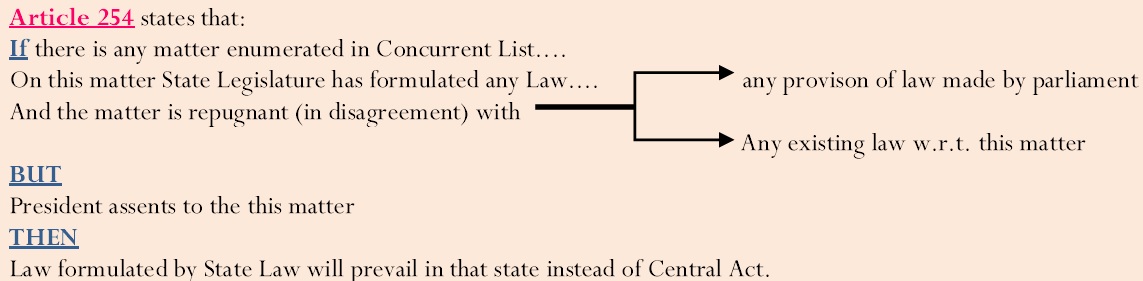

3) Article 254 gives power to States to prevail their own Law in respective states with the consent of President even if the parallel Central Law is in existence, thus for the purpose of this Act, the said article has been overruled by using words notwithstanding (overruling/disregarding) in the opening line of the Article 246A.

Further, Article 246A clearly makes sure that:

1) Parliament has exclusive power to make law w.r.t. goods or service supplied in Inter State Trade.

2) States have power to make laws with respect to goods and services tax imposed by the Union or by such State except in case of Inter State Trade.

3) The words used in 246A(1), “Parliament and States have power to make laws with respect to goods and services tax imposed by the Union or by such State”may lead to confusion

“ki Union ke Tax imposition par State kyun Law banaye Ya State ke Tax imposition par Union kyun Law banaye”!!!

This is due the reason that in present indirect taxation regime, Taxes like VAT, Entry Tax etc. are subject to State Levy and Taxes like Excise, Service Tax are subject to Central Levy.

Hence, the power has been given to both Centre and States in relation to formation of Law on matters which are subject to State as well as Central Levy.

Section 3: Amendment of Article 248

In article 248 of the Constitution, in clause (1), for the word “Parliament”, the words, figures and letter “Subject to article 246A, Parliament” shall be substituted.

Article 248 (Reproduced with changes)

(1) Subject to Article 246A, Parliament has exclusive power to make any Law with respect to any matter not enumerated in the Concurrent List or State List

(2) Such power shall include the power of imposing a tax not mentioned in either of those lists

ANALYSIS:

If we ignore the red words (i.e. the amendment) then

Above Article gives exclusive power to Parliament in case of Residuary entries

and further we all know that no entry in State List or Concurrent List deals with imposition of GST

Thus, it has been made Subject to Article 246A so that Parliament is not able to exercise exclusive power in relation to Goods & Services Tax.

Section 4: Amendment of Article 249

In article 249 of the Constitution, in clause (1), after the words “with respect to”, the words, figures and letter “goods and services tax provided under article 246A or” shall be inserted.

Article 248 (Reproduced with changes in red)

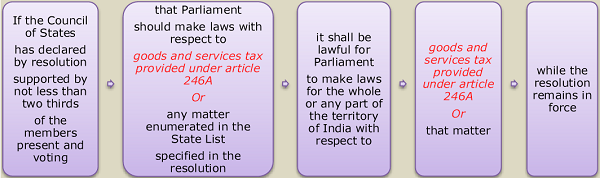

Power of Parliament to legislate with respect to a matter in the State List in the national interest:

ANALYSIS:

Constitution has given option to the Council of states that they can give power to Parliament to make Laws for the matters enumerated in State List.

But State List does not contain any entry for GST, thus to obey with the intent of ancestoral Law makers highlighted words have been inserted in the Article 249.

Now, States can by proper resolution and in National interest can grant power to Parliament for making Law on GST.

Section 5: Amendment of Article 250

In article 250 of the Constitution, in clause (1), after the words “with respect to”, the words, figures and letter “goods and services tax provided under article 246A or” shall be inserted

Article 250 (Reproduced with changes in red)

Notwithstanding anything in this Chapter, Parliament shall, while a Proclamation of Emergency is in operation, have, power to make laws for the whole or any part of the territory of India with respect to goods and services tax provided under article 246A or any of the matters enumerated in the State List

ANALYSIS:

Constitution has given power to the Parliament to make Laws for the matters enumerated in State List in case of an

Emergency.

But State List does not contain any entry for GST, but such power is of utmost importance, thus, highlighted words have been inserted in the Article 250 specifically.

Now, Parliament has the power for making Law on GST for any part of Indian case of Emergency.

Section 6: Amendment of Article 268

In article 268 of the Constitution, in clause (1), the words “and such duties of excise on medicinal and toilet preparations” shall be omitted.

Article 268 (Reproduced with changes in red)

Duties levied by the Union but collected and appropriated by the States

(1) Such stamp duties and such duties of excise on medicinal and toilet preparations as are mentioned in the Union List shall be levied by the Government of India but shall be collected:

(a) in the case where such duties are leviable within any Union territory, by the Government of India, and

(b)in other cases, by the States within which such duties are respectively leviable.

ANALYSIS:

Before amendment, Duties of Excise on Medicinal & Toilet Preparations were levied by Government of India but was collected by the respective States (except in case of Union Territories)

But with introduction of GST, there is no requirement of such clause. Hence, Omitted.

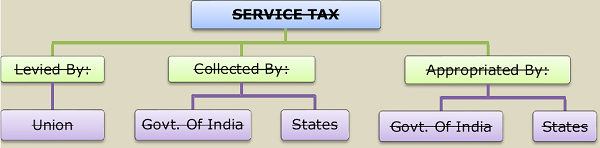

Section 7: Omission of Article 268A

Article 268A of the Constitution, as inserted by section 2 of the Constitution (Eighty-eighth Amendment) Act, 2003 shall be omitted.

Article 268A (Reproduced with changes)

ANALYSIS:

Article 268A was introduced via Eighty Eighth (88th ) Amendment for Levy and Collection of Tax on Services.

Now, this Article is not required at all due to the introduction of GST which itself contains the power to levy and collect tax on services in addition to goods. Hence, Omitted.

Section 8: Amendment of Article 269

In article 269 of the Constitution, in clause (1), after the words “consignment of goods”, the words, figures and letter “except as provided in article 269A” shall be inserted

ANALYSIS:

Article 269 gives the list of various taxes which is levied and collected by Union and the manner of distribution and assignment of Tax to States. List goes like this:

(a) duties in respect of succession to property other than agricultural land

(b) …

(c) …

(h) taxes on the consignment of goods except as provided in article 269A,where such consignment takes place in the course of inter State trade or commerce

Further, new Article 269A has been inserted by way of Section 9 (discussed next) which specifically provides for the manner of distribution of Tax on Goods and Services, thus, the highlighted words have been introduced in the clause (h)

Section 9: Insertion of new Article 269A……. Levy and collection of goods and services tax in course of inter-State

trade or commerce

ANALYSIS:

The newly inserted Article 269A gives power of collection of GST on inter-state trade or commerce to Government of India i.e. the Centre, which is called as IGST by the Model Draft Law.

But out of all the tax collection by Centre there are two ways in which states get their share out of such collection

a) Direct Apportionment (let say out of total net proceeds 42% is directly apportioned to states).

b) Through Consolidated Fund of India (CFI). Out of the total amount in CFI a particular prescribed percentage, say 30%, goes to the States.

Note: As per clause (2) the amount which is directly apportioned to states (say 42% in our example) doesn’t goes into CFI for further distribution.

Now, read the above article 269A again you will get everything.

“Humne to Article 246A mein interstate trade or commerce ke regarding padhatha…ab ye kyahai”

Chalo fir se padhte hain!!!!

Article 246A provides power to make laws on interstate trade or commerce to Union, whereas focus of Article 269A is on levy, collection and distribution of tax collected in interstate trade or commerce.

Article 246A provides power to make laws on interstate trade or commerce to Union, whereas focus of Article 269A is on levy, collection and distribution of tax collected in interstate trade or commerce.

Section 10: Amendment of Article 270

(i) in clause (1), for the words, figures and letter “articles 268, 268A and 269”, the words, figures and letter “articles 268, 269 and 269A” shall be substituted;

(ii) after clause (1), the following clauses shall be inserted, namely:—

(1A)……

(1B)……

Article 270 (Reproduced with changes)

1) All taxes and duties referred to in the Union List, except:

- the duties and taxes referred to in articles 268,

268A and269 and article 269A respectively - ……..

shall be levied and collected by the Government of India and shall be distributed between the Union and the States in the manner provided in clause (2).

(1A) The tax collected by the Union under clause (1) of article 246A shall also be distributed between the Union and the States in the manner provided in clause (2).

(1B) The tax levied and collected by the Union under clause (2) of article 246A and article 269A, which has been used for payment of the tax levied by the Union under clause (1) of article 246A, and the amount apportioned to the Union under clause (1) of article 269A, shall also be distributed between the Union and the States in the manner provided in clause (2)

ANALYSIS:

Few terms for simplifications as used by Model Draft law:

| I | tax collected by the Union under clause (1) of article 246A | Central GST (CGST) |

| II | tax collected by the States under clause (1) of article 246A | State GST (SGST) |

| III | The tax levied and collected by the Union under clause (2) of article 246A and article 269A | Integrated GST (IGST) |

–

| What will not be distributed as per clause (2) | What will be distributed as per clause (2) |

| Duties & Taxies referred in:

> Article 268 (From this excise on medicinal and toilet preparations have been deleted) > Article 268A (It was about Service Tax Levy…It has been omitted) > Article 269 (It deals with list of taxes stated in the said article) > Article 269A (It deals with GST levied by Govt. Of India in intercourse trade or commerce called as IGST by Model Draft Law) The above articles themselves provide the manner of distribution of the stated taxes levied under those articles thus, there is no need for their distribution as per Article 270 |

> As per clause (1A),

> As per clause (1B),

|

DISCLAIMER: This document is being furnished to you for your information. You may choose to reproduce or redistribute this report for non-commercial purposes in part or in full to any other person with due acknowledgement of GST Network India. The opinions expressed herein are entirely those of the author(s). GST Network India makes every effort to use reliable and comprehensive information, but GST Network India does not represent that the contents of the report are accurate or complete. GST Network India is an independent, not-for-profit group. This document has been prepared without regard to the objectives or opinions of those who may receive it.