Commission Agents Represent Companies and provide Services and Liaisons to Assist Businesses to Expand. Commission Agents, generally are well versed in the Specific Industry Product or Services and are Subject Experts having Solid Reputation and Wide Network of Contacts in the industry; Substantial Marketing Experience for Reaching a Targeted Demographic Region. A commission Agent can have various responsibilities including Marketing Research, Lead Generation – Arranging Buyer & Seller Connections, Creating Proposals, Participating in Sales Negotiations and Closing, Product Delivery, Brand & Image Building and Account Management.

Commission Agents may act as Intermediaries who Receives a Commission for Arranging & Facilitating Buying or Selling. The Fee or Commission of Commission Agent is based on how much effort the agent puts into the Service and the Cost of the Product or Service itself. The Fee may be based on Specific Amount or a Certain Percent of the Transaction Value as mutually being agreed upon.

Commission Agents may be Categorized as Buying Agents or Selling Agents. Buying Agents or Purchasing Agents are Professionals or Companies that Represent and offer Services to Buyers to Buy Goods or Avail Services from Third Party. On the other hand Selling Agents Represent the Sellers for Marketing & Selling the Product or Goods of the Company. In brief Commission Agents Represent Principals (Buyers or Sellers).

Definitions :

Sec 2(5) of CGST Act

The term “Agent” has been defined under sub-section (5) of section 2 of the CGST Act as follows: “agent” means a person, including a factor, broker, commission agent, arhatia, del credere agent, an auctioneer or any other mercantile agent, by whatever name called, who carries on the business of supply or receipt of goods or services or both on behalf of another.

Section 182 of Indian Contract Act, 1872

As per section 182 of the Indian Contract Act, 1872, an “agent” is a person employed to do any act for another, or to represent another in dealings with third person.

The person for whom such act is done, or who is so represented, is called the “principal”. As delineated in the definition, an agent can be appointed for performing any act on behalf of the principal which may or may not have the potential for representation on behalf of the principal. So, the crucial element here is the representative character of the agent which enables him to carry out activities on behalf of the principal

Scope of Principal – Agent Relationship :

In terms of Schedule I of the Central Goods and Services Tax Act, 2017, the supply of goods by an agent on behalf of the principal without consideration has been deemed to be a supply.

As per para 3 of Schedule I which is reproduced hereunder

3. Supply of goods—

(a) by a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

(b) by an agent to his principal where the agent undertakes to receive such goods on behalf of the principal.

It is worth noticing that all the activities between the principal and the agent and vice versa do not fall within the scope of the said entry. Firstly, the supply of services between the principal and the agent and vice versa is outside the ambit of the said entry, and would therefore require “consideration” to consider it as supply and thus, be liable to GST. Secondly, the element identified in the definition of “agent”, i.e., “supply or receipt of goods on behalf of the principal” has been retained in this entry.

Circular No. 57/31/2018-GST Dated- 4th September, 2018

Intermediary Services

The term “INTERMEDIARY” has been defined under Section 2(13) of IGST Act :

“Intermediary” means:

> a broker, an agent or any other person,

> by whatever name called,

> who arranges or facilitates the supply of goods or services or both,

> or securities,

> between two or more persons,

> but does not include a person who supplies such goods or services or both or securities on his own account.

Place of Supply Provisions for Services:

> Place of Supply when Both the Supplier & Recipient are in India. Default Provision in Section 12(2) of IGST Act, 2017 : Place of Supply would be Location of Recipient.

> Place of Supply when Either the Supplier or the Recipient are Outside India : Section 13 of IGST Act

> Section 13(1) would apply to determine the place of supply of services where the location of the supplier of services or the location of the recipient of services is outside India.

> Default Section 13(2) states that the place of supply of service except the services specified in sub-sections (3) to (13) shall be the Location of Recipient of Service.

> In terms of Section 13(8)(b) of IGST Act, 2017, the place of supply for the intermediary services would be the location of the supplier of such services (i.e. location of intermediary service provider)

Applicability of GST on Commissions Received by Commission Agents

When the essential character of services provided by Service Provider to Local / Foreign Principal customer is that of Commission Agent for enabling Sourcing or Sale of Goods, the as per the composite supply concept, the principal supply is that of intermediary service.

With this understanding let’s now discuss Applicability of GST on Commissions Received by Commission Agents. We shall discuss here under in different Scenarios:

> Scenario – 1 : Commission Agent & Principal, both are in India

> Scenario – 2 : Commission Agent is in India & Principal is Outside India

> Scenario – 3 : Commission Agent is Outside India & Principal is in India

> Scenario – 4 : Commission Agent is Outside India & Principal is also Outside India.

Let’s now Discuss each Scenario with Examples and Applicability of GST:

Scenario – 1 : Commission Agent & Principal, both are in India

In this Scenario, both the Commission Agent & Principal, both are in India.

For Example SNP Exim Services, in India acting as an Agent arranging a Buyer / Seller or Sourcing / Buying Arrangement for his Principal M/s Hindusthani who is also in India. Since both the Supplier (Commission Agent) and Recipient (Principal) are in India, therefore Place of Supply would be governed by the Default Provision in Section 12(2) of IGST Act, 2017 and accordingly the Place of Supply would be Location of Principal. Thus, it would be Taxable in GST similar to any Normal Supply within India.

The Commission Agent should Charge GST as Applicable. In case both the Commission Agent & Principal are in the Same State, then CGST + SGST; or in Different States, then IGST applicable.

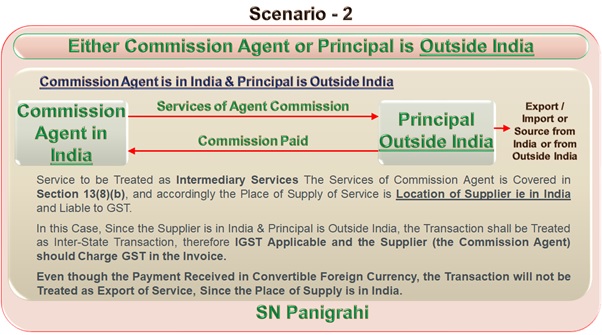

Scenario – 2 : Commission Agent is in India & Principal is Outside India.

In this Scenario, the Indian Commission Agent providing services to Overseas Principal. Since the Nature of Transaction is Agent and Principal Relation where Agent is Providing Services on Commission basis, Services to be Treated as Intermediary Services. The term “INTERMEDIARY” has been defined under Section 2(13) of the IGST Act :

“Intermediary” means:

> a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account.

For understanding the Place of Supply, we need to refer Section 13 of IGST Act, which states as below :

Section 13(1) shall apply to determine the place of supply of services where the Location of the Supplier of Services or the Location of the Recipient of Services is Outside India.

Default Section 13(2) states that the place of supply of service except the services specified in sub-sections (3) to (13) shall be the location of recipient of service.

The Default provision shall not apply, since the Intermediary Services is specifically Covered in Section 13(8) of IGST Act, 2017.

Section 13(8) of IGST Act, 2017 provides that the place of supply of following services shall be the location of the supplier of service:

(a) …

(b) Intermediary Services,

(c) …….

Accordingly, the Place of Supply of Service is Location of Supplier ie in India and Liable to GST.

In this Case, Since the Supplier is in India & Principal is Outside India, the Transaction shall be Treated as Inter-State Transaction as per Sec 7(5) of IGST Act, 2017, therefore IGST Applicable and the Supplier (the Commission Agent) should Charge IGST in the Invoice.

Even if the Payment Received in Convertible Foreign Currency, the Transaction will Not be Treated as Export of Service, since the Place of Supply is in India.

To Qualify as Export of Service, as per Section 2 (6) of IGST Act, 2017, All the Following 5 Conditions should satisfy:

(i) The Service Provider is situated in India;

(ii) The Recipient of Service is situated Outside India;

(iii) The Place of Supply of that service is also Outside India;

(iv) The Payment for such service has been received by the supplier of service in Convertible Foreign Exchange or in Indian rupees wherever Permitted by the Reserve Bank of India; and

(v) The supplier of service and the recipient of service are Not Merely Establishments of a Distinct Person in accordance with Explanation 1 in section 8; .

Case Study – 1 : GST payable on Back Office Support Services and are not Exports

In re Vservglobal Private Limited (AAR Maharastra); GST-ARA-03/2018-19/B-59; 07/07/2018

It was held that back office support services to overseas companies undertaken by the applicant are for and on behalf of the clients to facilitate supply of goods and services between their clients and their customers. Applicant clearly is covered and falls in the definition of “intermediary” as defined under the IGST Act and, therefore, provisions pertaining to ‘place of supply’ in case of intermediary services as provided in sub-section 8 of section 13 are relevant.

Comments: The AAR has not considered the aspect of main service provided by applicant to overseas company on its own account. The service provided on principal to principal basis and not acting as an agent is completely ignored in the above said AAR.

In re Vservglobal Pvt. Ltd. (GST AAAR Maharastra); MAH/AAAR/SS-RJ/22/2018-19; 26/02/2019

Uphold the Ruling of AAR

Case Study : 2 : “Commission” received in convertible Foreign Exchange as an “Intermediary”

Facts: Micro Instruments (In short ‘MI’) in India is providing services to its Principals at Germany, by way of procuring Purchase Orders (P.O.) from the parties in India, for which MI receives commission in CFE. After the negotiations are concluded, the prospective customer in India places the order directly on the Principals at Germany, arranges for remittance of purchase price arrived at and the material is directly supplied to customers by the foreign Principals.

Question :- (i) Whether the “Commission” received by the Applicant in convertible Foreign Exchange for rendering services as an “Intermediary” between an exporter abroad receiving such services and an Indian importer of an Equipment, is an “export of service” falling under section 2(6) & outside the purview of section 13 (8) (b), attracting zero-rated tax under section 16 (1) (a) of the Integrated Goods and Services Tax Act, 2017?

Answer :- Answered in the negative.

Question :- (ii) If the answer to the Q. (i) is in the negative, whether the impugned supply of service forming an integral part of the cross-border sale/purchase of goods, will be treated as an “intra-state supply” under section 8 (1) of the IGST Act read with section 2(65) of the MGST Act attracting CGST/MGST ? And, if so at what Rate?

Answer: The said supply will be treated as Inter-State Supply and not Intra State Supply and IGST will be levied @ 18%.

In this case the Services are to be Treated as Intermediary Services, and therefore the Indian Agent Providing Services to the Overseas Principal is Not Treated as Export of Services as the Place of Supply is Location of the Supplier which is in India. Therefore, the Provision Depriving the Export Benefits to the Indian Supplier to Overseas Principal.

It is in fact a contentious issue and is being debated for quite Long time. The matter even referred in the 139th Report of Rajya Sabha in December 2017, which proposed for intermediary services to be treated as Exports. Unfortunately, till date the GST Council has not taken decision on the issue and CBIC not issued any Notification or Circular in this regard.

Such Intermediary Services are treated as Exports and are allowed all the Export Benefits in many of the Countries like EU, but in India the Export benefits are denied to Indian Suppliers who are providing Services to Clients Abroad and Earning Valuable Forex, therefore the Place of Supply provisions under Section 13(8)(b) of IGST Act, 2017 need to be Amended.

Scenario – 3 : Commission Agent is Outside India & Principal is in India

The Agent Services are in the nature of Intermediary Services, therefore the Place of Supply provisions as per Section 13(8)(b) of IGST Act, 2017 is applicable which states that Place of Supply shall be the Location of the Supplier and accordingly in this case the Location of the Commission Agent which is Outside India. That means the Location of the Supplier is Outside India (Non-Taxable Territory) the Location of the Recipient is in India (Taxable Territory) but the Place of Supply is also Outside India, therefore the Transaction is Not Treated as Import of Services.

To Qualify as Import of Services as per Section 2(11) of IGST Act 2017 Services must satisfy all the follows conditions :

Import of services means the supply of any service where-

(i) The supplier of service is located outside

(ii) The recipient of service is located in India; and

(iii) The place of supply of service is in India;

Since it is Not Treated as Import of Services, No IGST shall be payable on Reverse Charge basis by the Recipient ie Principal.

Example : 1

Exporter in India paying commission to a foreign commission agent

If an exporter in India pays commission to a foreign commission agent, the place of supply is out of India and hence no GST is payable (and no reverse charge applicable to Indian exporter) – FAQ on GST Chapter 21 Q No. 25 issued by CBI&C on 15-12-2018.

Example : 2

Branch office outside India providing service to Indian parent company is not import of service

Bharat Business – An Indian parent company has a Liaison Office Outside India. The Indian parent company receiving services from overseas Liaison Office for which it l remits some amount to liaison office Outside India. In that case, that liaison office is ‘intermediary’ located Outside India providing services to Principal – the Parent Company in India.

As per section 2(11) of IGST Act, one of the conditions for treating a service as “import of service” is that place of supply of service should be in India. Since Place of Supply of Service as per Sec 13(8)(b) of IGST Act is Outside India, so this condition is not satisfied, the service received by Indian parent company cannot be Treated as ‘import of service’. Consequently, Indian company will not be liable to pay service tax under reverse charge

Scenario – 4 : Commission Agent is Outside India & Principal is also Outside India.

Both the Supplier of Service (Commission Agent) & Principal are Located in a Non-Taxable Territory, the Transaction will not be Treated as Supply under GST Law, therefore No GST Applicable

Now let’s Discuss the Situations where, the Supplier & Recipient are not having the Relation as Agent & Principal. Supplier may be providing Services such as Engineering Services, Architectural Services, Management or Accounting Services, Presale Activities of Nature of Market Surveys, Feasibility Surveys, Recommending Suitable Suppliers, Maintain Supplier List, and Post Order Activities such as Sourcing / Supply Market Survey, Supplier Order Status, Guidance to Manufacturers on Trends / Developments, Supplier Inspection, Product Quality and Delivery Schedule, Advise on International Norms and Standards etc……….etc…….In such cases the dominant nature of service appears to be that of outsourced business support services, which in normal course could be done between Supplier & Recipient and the Fee Paid is Not in the Nature of Commission or Agent Fee.

Here we shall discuss Two More Different Scenarios:

> Scenario – 5 : Supplier of Services is Outside India & Recipient is in India

> Scenario – 6 : Supplier of Services is in India & Recipient is Outside India

In the above Two Scenarios, the Supplier and Recipient Relations are other than Agent & Principal Relation.

Scenario – 5 : Supplier of Services is Outside India & Recipient is in India

If the supplier of service is located in a non-taxable territory, the recipient of services located in the taxable territory is Treated as Import of Service as per Section 2(11) of IGST Act 2017, and Recipient is Liable to Pay IGST under Reverse Charge under Section 5(3) of IGST Act,2017. Notification Nos. 13/2017-CT (Rates)and 10/2017-IT (Rates) dated 28-6-2017

Import of Services as per Section 2(11) of IGST Act 2017 Services must satisfy all the follows conditions :

Import of services means the supply of any service where-

(i) The supplier of service is located outside

(ii) The recipient of service is located in India; and

(iii) The Place of Supply of service is in India;

Here for determining Place of Supply, we need to follow Default Section 13(2) that states that the place of supply of service except the services specified in sub-sections (3) to (13) shall be the Location of Recipient of Service.

In this case the Place of Supply is the Location of the Recipient ie in India. Accordingly, all the 3 Conditions are being Satisfied under Section 2(11) of IGST Act 2017 to Qualify as Imports, therefore IGST is Payable by the Recipient on RCM basis.

However, IGST is not payable on import of services under reverse charge if value of royalty and license fee was included in customs value of goods imported – (Notification No. 6/2018-IT (Rate) dated 25-1-2018 and FAQ issued by CBI&C on 15-12-2018.)

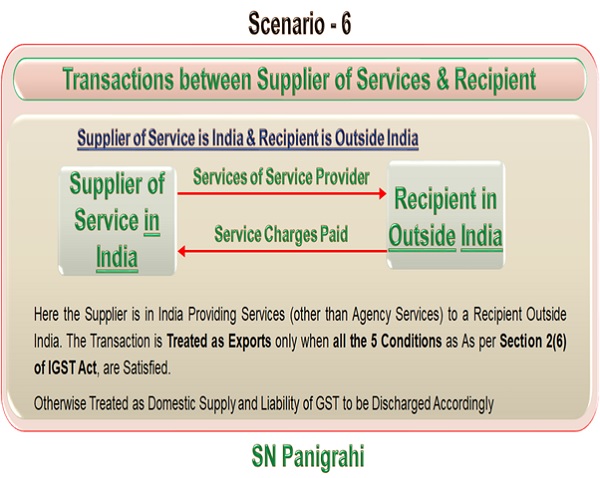

Scenario – 6 : Supplier of Services is in India & Recipient is Outside India

Here the Supplier is in India Providing Services (other than Agency Services) to a Recipient Outside India. The Transaction is Treated as Exports only when all the 5 Conditions as discussed blow are Satisfied.

As per Section 2(6) of IGST Act, “Export of Services” means the supply of any service when, –

(i) the Supplier of Service is Located in India;

(ii) the Recipient of Service is Located Outside India;

(iii) the Place of Supply of service is Outside India;

(iv) the Payment for such service has been received by the supplier of service in Convertible Foreign Exchange; or in Indian rupees wherever permitted by RBI, [inserted vide IGST (Amendment) Act 2018, w.e.f. 1-2-2019 and

(v) the Supplier of Service and the Recipient of Service are not merely establishments of a distinct person. if place of supply is out of India (Notification No. 9/2017-IT (Rate) dated 28-6-2017 as inserted w.e.f. 27-7-2018.)

In case the Transaction is not Treated as Export of Services, then the Transaction is Treated as Domestic Supply and Liability of GST to be Discharged Accordingly

Case Law : 1: Manpower Services

NES is supplier of manpower services to highly technical industries such as Oil & Gas, Power etc. NES India and NES Abu Dhabi have proposed to enter into a Master service agreement (MSA) through which NES India will provide support service in respect of the foreign business carried on by NES Abu Dhabi

Held: Transaction covered under the MSA between the applicant and NES Abu Dhabi is a Zero-rated supply and is to be considered as an export of service under the GST Act

Bank Remittance Certificate (BRC) or Foreign Exchange Remittance Certificate (FIRC) is required only in case of export of services (clarified vide CBI&C circular No. 37/11/2018-GST dated 15-3-2018)

Case Law : 2 : Marketing & Pre sales Technical Support Services

Marketing & pre sales technical support services – In this applicant undertakes the understanding of customer’s requirement, presentations, demonstrations, explores business opportunity, once the order is placed applicant used to co-ordinate with the customers, helps in follow up for collection of invoice value from customers in India, applicant receives consideration fixed as a percentage sale of the order value.

Questions :

a) Whether Marketing & Pre-Sales Technical Support Services provided by the applicant will be classified as Intermediary services in terms of Section 2(13) of the Integrated Goods and Services Tax Act, 2017?

Held: The services provided is intermediary services falling under purview of S. 2(13) of IGST Act.

Comments: The authority has notedly grasped the actual nature of transaction which are required to be treated separately rather than treating them as ancillary services with conjunction to the principal supply as different contracts were entered for the transactions and concluded accordingly.

b) Whether the Post- Sales Technical Support Services provided by the applicant would be classified as Information Technology Support Services falling under HSN Code 998313?

Held: The Post-Sales Technical Support Services provided by the applicant is classified as Information Technology Support Services falling under Service Code 998313.

Conclusion

From the above discussions it is very Clear that the Applicability of GST depends on the Nature of Transaction that defines the Relationship between the Supplier and the Recipient ie either Agent – Principal Relationship or otherwise (Criteria may be Receipt of Consideration by way of remuneration, a commission or percentage upon the amount involved in such transaction); Contractual Terms & Determination of Place of Supply.

Therefore, it is utmost necessary for the person to determine the correct nature of supply and pay the tax accordingly in correct way.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade & Project Consultant, Practitioner, International Corporate Trainer & Author.

Author can be Reached @ snpanigrahi1963@gmail.com

Author Bio

This is incorrect with regard to commission received by an intermediary, if the location of supply of goods by the buyer and seller happens outside the taxable territory. Vide notification under IGST no 19-2019 Sep 30th, the IGST rates for such intermediary services has been kept as ” Nil” ( HSN 9961).

The crux in the notification is narrated below for reference.

“Services provided by an

intermediary when location of

both supplier and recipient of

goods is outside the taxable

territory”.

Since this notification was issued in Sep 30, 2019 , when the contentious Sec 13(8)(b) was very much is vogue, makes it clear that the purpose of this notification was to fully exempt the ” commission” earned from overseas Suppliers who sell goods to overseas buyers otherwise known as “Merchant Trade”.

This notification when specifically exempts such intermediary service arising in the course of Merchant Trade, this has an overriding power to by pass what is said in Sec 13(8) (b).

So despite the supply of service is from India to an overseas seller to in turns sells it to an overseas buyer was also spotted by the Indian intermediary, the GST on commission earned is nil by virtue of this notification. Hope you will concur with me.

We are based in India and providing engineering services to overseas clients. Generally get all orders thru overseas agent only who works with is on commission basis.

when we pay commission to a non resident agent, who has no PE in India, against the service contract with overseas clients, will it attract TDS or not.

We are agents for foreign company in India and book contracts with Govt of india in foreign currency for our Principals supply of goods. We get 3% agency commission and that the govt of india orgn asks us to get agency commission deducted from foreign bill and that agency commission will be paid to us in equivalent indian rupees. We raised the invoice for equivalent Indian rupees to claim our commission by adding IGST. But the buyer (govt dept) refused to pay IGST and they deducted 2% IT from the proceeds. Now I want to know whether IGST is applicable for Service as an agent of foreign supplier ? The buyer is in Indore and we are in Mumbai.

Please guide us.

My queary a commission agent arrange a buyer for saler and saller despached goods in the month sept. and received payment in month of december and paid commission to agent in december gst on commission charged in dec. by agent it is right ? pls. clear gst liability of agent in the month of sept. or dec. becouse commission on payment only