Bank auditing is the procedure of reviewing the services and procedures adopted by banks and other financial institutions. It is a routine procedure that all financial services entities must undergo in order to ensure that they are in compliance with industry standards and jurisdictional regulations.

In this Presentation let’s Discuss Bank Audit from GST Point of View

Bank Transactions under GST are pretty critical and complex as Banking Operations involves a variety of transactions like issuing cheques / Drafts / cards / issue process, ATM operations, credit wing, securities, letter of credit, net banking, cash backs and reward points, loans and advances, deposits, point of sale transactions, etc. ………

Banks and NBFCs also involve in different nature and volume of other services such as lease transactions, hire purchase, actionable claims, fund and non-fund based services etc.,

Unlike in Service Tax regime, where banks were used to take Single Registration Centrally on Pan India basis applicable to all the branches across the country, in GST Banks need to take Separate Registration for each state of operation.

Banks generally have multiple branches on pan India basis and each one is unique in its own nature of supplies, the transaction flow, types of customers & their unique requirements apart from various statutory obligations and local requirements, overly burdened banking sector with complexity of compliance and voluminous tax accounting records and returns filling, reconciliation and audit requirements.

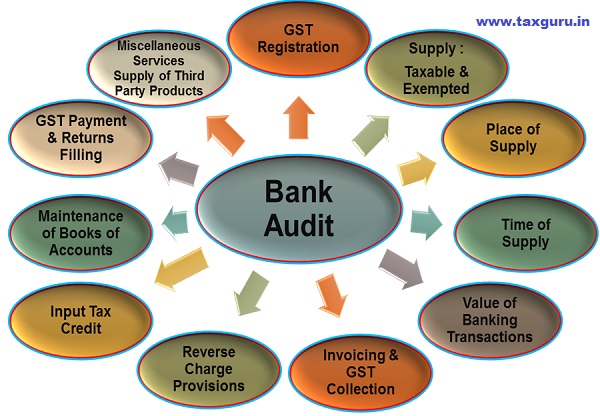

Bank Audit from GST Angle: Major Areas to Cover:

We shall Discuss in this Article on the following Aspects

State-wise Requirement of GST Registration

Since, GST Registration is a State Specific and most banks have a pan-India presence which means they are required to register under GST in ALL states.

However, multiple branches in a same state are required to be registered under a single GST Number.

Auditors to Verify : Registration Related

- Whether the banks have taken the Registration of GST in all the States where they have Operations?

- Whether all the Braches in the State are added as Additional Place of Business in the Registration obtained in that State?

- Whether the banks (HO/ZO/RO) have sought registration as Input Service Distributor (ISD)?

- Whether Registration Certificate Exhibited in Prominent places of all the branches?

Bank Outward Supply : Taxable & Exempted

Banks and financial institutions provide a bouquet of financial services relating to lending or borrowing of money or investments in money and other related services. For such services invariably a variety of instruments are used in the financial markets.

Transactions in such instruments have to be examined from the basis of very definition of supply which involves Goods or Services or both. The definition of ‘goods’ and ‘services’ in Section 2(52) and Section 2(102) of the CGST Act, 2017 specifically excludes money and securities respectively. ‘Money’ has been defined in Section 2(75) of the CGST Act, 2017 to include instruments like cheques, drafts, pay orders, promissory notes, letters of credit, etc. Therefore, activities that are only transactions in such Instruments would be outside the definition of service and hence GST is not applicable.

However, if separate consideration is charged for any related activity, GST applicable. Therefore, GST would be levied on service charges normally charged for various transactions in money including charges for making drafts, issuance charges for letter of credit, Bank Guarantee Commission Charges, Processing Fees on Loans, Documentation Charges, Ledger Folio Charges, Bank Statement Charges, Inspection & Survey Charges etc.

Exempted Services

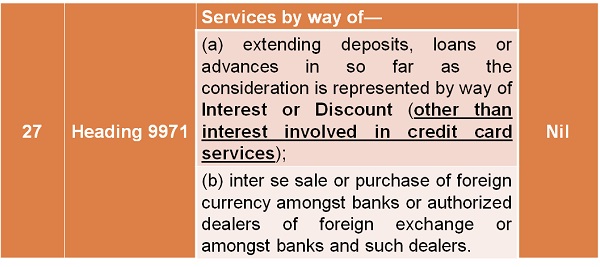

Vide Notification No. 12/2017- Central Tax (Rate); Dated 28th June, 2017, certain Exemptions are granted as follows:

- By this entry the interest / discounts on loans / deposits / advance are being given exemption.

- The sale and purchase among the banks and authorised dealers of foreign exchange are also given exemption. The interest on credit card has been specifically excluded

Exempted Services:

- Interest / Discount earned or paid for Loans, Deposits or Advances etc

Taxable Services:

- Any upfront or regular charges such as Processing Fees, Documentation Charges, Service Charges, Collection Charges, Inspection Charges, Repossession Charges, Foreclosure or Prepayment Charges etc

- Interest involved in Credit Card Services

Auditors to Verify : GST Taxable & Exempted Supply Related

- Whether any In-Build System arrangements are made to ensure that Different Types of Supplies are Identified and Separately Recognized as Taxable Supply & Exempted Supply?

- Verifying Whether all Transactions are made as per Check List of Exempted & Taxable Supplies (Banks must have Charted out such List for Internal Circulation to Branches as Guidelines, which auditors may demand before audit)?

- Verifying Whether Any Wrong Collection or No-Collection of Taxes?

Place of Supply of Banking and Financial Services

Place of Supply in Banking Sector is schematically explained below:

Auditors to Verify : Place of Supply Related

- Whether Place of Supply properly Understood & Accordingly Charged the Taxes?

- Whether Invoices or in any Bank Statement issued with Correct Place of Supply?

- Whether Taxes are Collected with Proper understanding of Nature of Supply?

(Intra-State : CGST + SCGST / UT GST; Inter-State : IGST)?

- Whether Returns are Filled with Proper Place of Supply & Type of Tax?

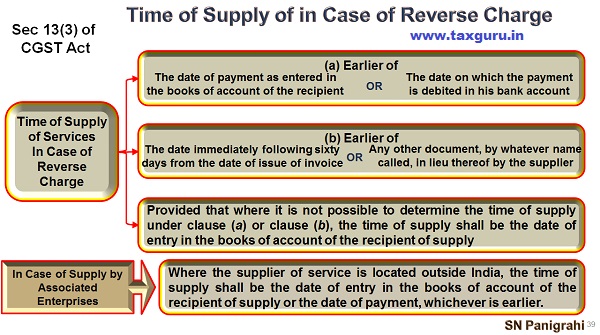

Time of Supply of Banking and Financial Services

Time of supply relevant to Banking and Finance Sector is depicted below:

Auditors to Verify : Time of Supply Related

- Whether Invoice / Bank Statement is Issued within Forty Five (45) Days from the Date of the Supply of Service?

- Whether Tax Liabilities if any Discharged Following Time of Supply?

- Verify whether any internal controls are in place to ensure that the provisions of the Time of Supply are adhered.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author Can be reached @ snpanigrahi1963@gmail.com

Author Bio

“Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.”

ALL said, (and READ to the FInish) – thast stands out as a copious ‘caution’, hence not to miss out/ ignore, – same way as a sign board – ‘Drive slow- DANGER Ahead”