Advance Ruling| Section 11 | CGST Act 2017 |Entry No. 74| Power to grant exemption from tax

Overview of Sec 11 : Power to gran exemption from tax

Central or the State Governments are empowered to grant exemptions from GST. Conditions are:

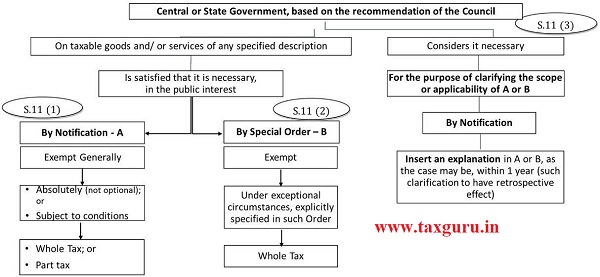

1. Exemption should be in public interest

2. By way of issue of notification

3. Must be recommended by the GST Council

4. Absolute exemption or conditional exemption may be for any services and / or services of any specified description.

5. Exemption by way of special order (not notification) may be granted exceptional circumstances.

6. Registered person supplying the services and/or services is not entitled to collect tax higher than the effective rate, where the supply enjoys an absolute exemption.

Overview of Entry No. 74 of Notification No. 12/2017

Overview of Entry No. 74 of Notification No. 12/2017

Services by way of—

a) health care services by a clinical establishment, an authorized medical practitioner or para-medics;

b) services provided by way of transportation of a patient in an ambulance, other than those specified in (a) above.

Meaning of Healthcare services

As per definition (zg) of Notification No. 12/2017- CT Rate

“Health Care Services” means

any service by way of diagnosis or treatment or care for illness, injury, deformity,abnormality or pregnancy

- in any recognized system of medicines in India and

- includes services by way of transportation of the patient to and from a clinical establishment,

- but does not include hair transplant or cosmetic or plastic surgery,

- except when undertaken to restore or to reconstruct anatomy or functions of body affected due to congenital defects,developmental abnormalities, injury or trauma;

Advance Ruling on Exemption related to serial No. 74 of Notification

Name of the applicant: Alcon Resorts Holding Pvt Ltd..

Order No.: Goa/GAAR/6/2018-19/3749 Dated : 14/11/2018 Authority: AAR (Goa)

Questions Sought by the applicant:

Whether the service provided by the applicant (including all incidental services) amounts to a composite service under the classification of health care services exempt under Entry No 74 of Notification 12/2017 Central Tax?

Submission of Applicant:

1) The supplicant provides health services for both International and Indian patients for Neuro muscular problems, post chemotherapy, post radio therapy treatment, in problem like psoriasis and chronic allergies, metabolic like obesity and other life style problems and orthopedic problems like Rheumatoid Arthritis, osteoarthritis etc.

2) They stated that after completion of check in process, their guests schedule their appointment with doctors for consultation.

Based on the health issues mentioned and analysis by the doctors, the applicant starts with Shaman or Shodhan Chikitsa to their guests.Sham means species in therapies or Shodhan means Panchakarma. The applicant has a team of doctors specialized in Naturopathy, Yoga and Ayurveda for the same. As per their analysis medications, diet restrictions and daily treatment are planned.

The applicant also has an in-house pharmacy from where Ayurvedic products are dispensed for treatment. Everyday treatment and follow up treatment are done to know the progress and responsiveness for the line of treatment prescribed. They also stated that they do not have any Restaurant or Bar for the guests and special diets, fruit, vegetables and juices are served as per the doctor’s prescription only.

Facts and Findings- As per concerned officer :-

In the instant case, the applicant provides health care services by way of appropriate diagnosis, appropriate medicines as well as relevant consumables or implants as part of treatment under supervision of qualified doctors till discharge. Therefore, medicines, implants etc, used in the course of providing health care services to in patients is undoubtedly naturally bundled in the ordinary course of business.

Hence, the stay for various treatments, supply of medicines, consumables and implants used in the course of providing health care services to in-patients for diagnosis or treatment are naturally bundled and are provided in conjunction with each other, would be considered as Composite Supply” and eligible for exemption under the category of health care services Accordingly, this authority holds that;

Ruling:

The applicant qualifies to be a clinical establishment and the services offered provided by the Applicant qualify to be Health Care Services. The intra-state supplies of the said services attract NIL rate of tax as per SL No.74 of the Notification No. 12/2017- Central Tax (Rate) dated 28th June, 2017

Name of the applicant: Shifa Hospitals

Order No.: 42/AAR/2019 Dated : 23/09/2019

Authority: AAR (Tamil Nadu)

Questions Sought by the applicant:

Whether the medicines, consumables, Surgical and implants used in the course of providing health care services to patients admitted to the Hospital for diagnosis or treatment would be considered as “Composite Supply” of health care services under GST and consequently exemption under Notification No. 12/2017 read with section 8 (a) of GST?

Submission of Applicant:

1) The applicant has stated that they are providing health care services to both out-patients and in-patients. In-Patients are those who are admitted in to the hospital for their diagnosis and treatment. The in-patients are provided with the facilities like stay inside the hospital rooms, diagnosis services, treatments including surgical treatments, post-surgery treatment, medicines, consumables, implants, dietary food etc.

2) There is in-house medical stores within the hospital premises owned by shifa hospital itself, from where the procured stocks of medicines, implants, consumables etc., are supplied to various sections like operation theaters, various wards etc., for treatment of in-patients to ensure appropriate diagnosis and timely treatment of in-patients, From the foregoing, it in submitted that though there are both supply of services and medicines etc involved in the process, the supply of medicines, implant, consumables in just incidental and naturally bundled to the supply of healthcare service which in the predominant supply. Hence the supply has to be treated as composite supply with Health Care supply as the predominant supply

Facts and Findings- As per concerned officer :-

1) The facts of the case as available before us, is that the applicant is a polyclinic providing health care services to both out-patients and in patients

2) Presently they do not have an in-house pharmacy The medicine required to be administered for the in patients are purchased by the patients from Shifa Pharmacy which is a separate entity.

3) As seen from the submission bills, the applicant has the in-patients for the Room charges, Nursing charges, lab investigation charge while medicines, consumables, etc are not charged in the hospital bill.

4) The applicant has stated that presently they do not charge anything for the medicines as the medicine prescribed by the hospital is procured by the patients outside the hospital, that the consumables, implants, etc which are essentials for the treatment at operation theaters/ICU wards/post operation wards, etc are supplied during the course of such treatment by the hospital itself and is billed at the time of discharge.

5) It is seen that in patients are provided a comprehensive treatment which includes room rent, nursing care, medicines, consumables, implants etc. The doctors who treat the in patients themselves prescribe the medicines and consumables and implants are used in their treatment and diagnostics. The in patients are charged for all of these when they are admitted to the hospital which provide services to the in patients.

Section 2(30) of CGST ACT

“composite supply” means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply

In the case at hand the hospital provides medicines, consumables, implants, etc to the in patients in the course of treatment on the directions of medical doctor for which the In-patient is billed together by the hospital. The hospital cannot provide health services including diagnostic, treatment surgery etc. without the help of medicines to be taken during treatment, implants and consumables used during their stay in the hospital. Only on using these medicines, consumables and implants as required and prescribed by the doctor and administered during their stay will the treatment be complete. Hence, supply of medicines, implants and consumables are natural bundled with the supply of health services. In this case, supply of health sciences is the principal supply as that is the reason the in patients get admitted to hospital instead of buying the medicines or consumables and using on themselves .Therefore supply of medicine, consumables and implants in patients in the course of their treatment is a composite supply of health services.

This view be straightened by the Circular. No 12/02/2018 which is given below:

a) Retention money: Hospitals charge the patients, say Rs. 10000/- and pay to the consultant/ technicians only Rs 7500/- and keep the balance for providing ancillary services which include nursing care, infrastructure faciities, paramedic care, emergency services, checking of temperature, weight, blood pressure. Will GST be applicable on such money retained by the hospital?

b)

(2) Healthcare services have been defined to mean any service by way of diagnosis or treatment or care for illness, injury, deformity, abnormal or pregnancy in any recognized system of medicines in india (para 2(zg) of notification No. 12/2017 CT(Rate). Therefore, hospitals also provide healthcare services The entire amount charged by them from the patients Including the retention money and the fee/payments made to the doctors etc, is towards the healthcare services provided by the hospitals to the patients and is exempt.

(3) Food supplied to the patients: Health care services provided by the clinical establishments will include food supplied to the patients; but such food may be prepared by the canteens run by the hospitals or may be outsourced by the Hospitals from outdoor caterers. When outsourced, there should be no ambiguity that the suppliers shall charge tax as applicable and hospital will get no ITC. If hospitals have their own canteens and prepare their own food; then no ITC will be available on inputs including capital goods and in turn if they supply food to the doctors and their staff; such supplies, even when not charged, may be subjected to GST.

(4) Food supplied to the in-patients as advised by the doctor/nutritionists is a part of composite supply of healthcare and not separately taxable. Other supplies of food by a hospital to patients (not admitted) or their attendants or visitors are taxable.

Ruling

1. Medicines, consumables and implants used in the course of providing health care services to in-patients by the applicant is a composite supply of Inpatient Services classifiable under SAC 999311.

2. Supply of health care services or inpatient services by the applicant as defined in Para 2(zg) of Notification no 12/2017-C.T. (rate) dated 28.06.2017 .

Similar Advance Rulings On Entry No. 74 of the Notification

Case Name : In re M/s. KIMS Health Care Management Ltd (GST AAR Kerala)

Appeal Number : Advance Ruling Order No. KER/17/2018

Date of Judgement/Order : 20/10/2018

Case Name: M/s Royal Care Speciality Hospital Pvt. Ltd.

Order No.: 46/ARA/2019 Dated : 26/09/2019

Authority: AAR (Tamil Nadu)

Name of the applicant: OPTM Health Care Private Limited

Case Number: 52 of 2019

Order number and date: 46/WBAAR/2019-20

dated 20/03/2020

Question sought by Applicant: Whether health care services provided by way of diagnosis, treatment, care for illness, deformity, injury, pregnancy by way of recognized system of medicine in india is exempt under serial no 74 of the notification or not?

Submission of Applicant:

1) lt, therefore, needs to be examined whether the Applicant is a ‘clinical establishment’ that provides health care services by way of diagnosis, treatment or care for illness in any recognised system of medicines in lndia.

2) The term ‘recognised system of medicine’ is not defined in the GST Act or notifications issued thereunder. lt is defined under section 2 (o) of the CE Act. lt means Allopathy, Yoga, Naturopathy, Ayurveda, Homoeopathy, Siddha and Unani Systems of medicines or any other system of medicine recognised by the State Government.

3) The Applicant claims that it administers certain plant-based medications for the treatment of osteoarthritis and disorders of similar nature. The medicaments are not supplied standalone, but ancillary to the supply of health care service. lt is a composite supply of health care service called ‘phytotherapy’. Applicant further submits that ‘phytotherapy’ is a treatment based on the ayurvedic system of medicine

Facts and Findings- As per concerned officer :-

1) It appears from the submissions of the Applicant that its ‘phytotherapy’ combines application of plant-based preparations with services having some therapeutic value. lf the preparations applied are manufactured exclusively in accordance with the formulae described in any authoritative book of Ayurveda specified in the First Schedule of the Drugs and Cosmetics Act, 1940, for use in the diagnose, treatment, mitigation or prevention of specific disease or disorder, they can be called ayurvedic medicine [refer to section 3 (9) of Drugs and Cosmetics Act, 19401 and the treatment provided may be considered a recognised system of medicine in lndia.

2) The Applicant’s submissions, however, do not clarify or claim that its plant-based preparations are manufactured exclusively in accordance with the formulae described in any authoritative book of Ayurveda specified in the First Schedule of the Drugs and Cosmetics Act, 1940. lt does not claim that the persons administering the plant-based preparations are ‘authorised medical practitioners’ in Ayurveda within the meaning of Para No. 2 (k) of the Exemption Notification. The Applicant has not clarified whether these persons possess the medical qualification included in the Second Schedule of the lndian Medicine Central Council Act, 1970 and registered underthe said Act as medical practitioners.

3) Under the circumstances, this Authority cannot accept the Applicant’s claim that it is a clinical establishment offering treatment in the recognised ayurvedic system of medicine. lts supplies are not, therefore, health care service by a clinical establishment, as defined under Para No. 2(s) of the Exemption Notification.

Ruling

The Applicant’s supply is not exempt under Entry No. 74 of lhe Exemption Notification. lt, therefore, needs to remain registered, as its liability to pay GST does not cease.

Author Bio