The industry holds a prominent position in the Indian economy contributing about 30 percent of total gross value added in the country. In FY23, the Indian industry faced some extraordinary challenges as the Russian-Ukraine conflict broke out. That led to a sharp rise in the prices of many commodities. Prices of edible oil, crude oil, fertilisers and food grains rose sharply. They remained at elevated levels for several months. The risk of another round of supply chain disruptions emerged, but they were not as severe as feared. Nonetheless, both the price and the availability of essential commodities had the potential to dent the industry’s optimism on consolidating the recovery of FY22 and further accelerating it. It is fair to say that the Indian industry acquitted itself rather well under trying circumstances. Overall Gross Value Added (GVA) by the Industrial Sector, based on data available for the first half of the FY23, rose 3.7 per cent, which is higher than the average growth of 2.8 per cent achieved in H1 of the last decade.

Robust domestic conditions since FY22 have provided a demand stimulus to industrial growth. Private Final Consumption Expenditure (PFCE) as a share of GDP in H1 of FY23 was the highest among all half years, H1 or H2, since FY15. Further, the strong export performance of FY22 continued somewhat in the first half of FY23. In this half of the year, exports of goods and services as a share of GDP have been the highest since FY16. However, the performance began to wane in the first half itself as the Year-on-Year (YoY) growth of exports declined from Q1 to Q2 due to persistently high inflation and rising interest rates in the advanced economies. The increase in investment demand has emerged as another powerful stimulus to industrial growth. It has been triggered by the augmented capex of the central government in the current and the previous year as compared to the pre-pandemic years. The leap also has crowded in private investment, already upbeat on the pent-up demand, export stimulus, and strengthening of the corporate balance sheets.

The supply response of the industry to the demand stimulus has been robust, as seen in high-frequency indicators. PMI manufacturing has remained in the expansion zone for 18 months since July 2021, and its sub-indices indicate an easing of input cost pressures, improving supplier delivery times, robust export orders, and future output. While growth in the consumer durables component of the Index of Industrial Production (IIP) is on account of the release of ‘pent-up’ demand, the increase in capital goods and infrastructure/ construction goods is indicative of the beginnings of a virtuous investment cycle that is expected to be led by the private sector. The growth of the eight core industries of coal, fertilisers, cement, electricity, steel, and refinery products has held steady, reflecting a broad momentum in industrial activity. However, the manufacturing landscape further shows uneven growth across various categories, with industries such as automobiles and electronics registering impressive performances while sectors such as textiles have been showing tepid growth, as export demand for these products has been mellowing with the slowing of global output and demand.

Industrial activity has been supported by an upswing in bank credit to the sector. Credit to industry started recovering from the beginning of the year and has been growing in double digits since July 2022. Credit to MSMEs has also seen a significant increase in part, assisted by the introduction of the Emergency Credit Linked Guarantee Scheme (ECLGS). While the growth in total credit has been driven by an increase in credit demanded by MSMEs, large industries have begun to increase the pace of their credit offtake too since the beginning of FY23 as they look to reduce their pace of capital raising from volatile debt and equity markets. The robust growth in credit demand combined with rising capacity utilisation and investment in manufacturing underscores businesses’ optimism regarding future demand.

Amidst heightened global uncertainty, Foreign Direct Investment (FDI) in the manufacturing sector moderated in the first half of FY23. However, inflows stayed well above the pre-pandemic levels, driven by structural reforms and measures improving the ease of doing business, making India one of the most attractive FDI destinations in the world.

The electronics industry continues to ascend in importance as its applications become pervasive. Electronics, supported by continuously improving communication services, will significantly enhance productivity, efficient service delivery, and social transformation. This industry’s significant growth drivers are mobile phones, consumer electronics, and industrial electronics. In the mobile phone segment, India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from 6 crore units in FY15 to 29 crore units in FY21.

The Indian Pharmaceuticals industry plays a prominent role in the global pharmaceuticals industry. India is ranked 3rd worldwide in the production of pharma products by volume and 14th by value. The sector is the largest provider of generic medicines globally, occupying a 20 per cent share in global supply by volume, and is also the leading vaccine manufacturer globally with a market share of 60 per cent. The performance of pharma exports has been robust, sustaining positive growth despite the global trade disruptions and drop in demand for Covid-19-related treatments. The cumulative FDI in the pharma sector crossed the US$ 20 billion mark by September 2022.

The pandemic and the Russia-Ukraine conflict have demonstrated the risk of supply chain shocks to the global economic order. As companies adapt their manufacturing and supply chain strategies to build resilience, India has a unique opportunity to become a global manufacturing hub this decade. In this context, the government’s Make-in-India initiative has facilitated investment, fostered innovation and built world-class infrastructure while addressing the gaps in domestic manufacturing capabilities. The Production Linked Incentive (PLI) schemes across 14 categories has further complemented it with an estimated Capex of around ₹3 lakh crore over the next five years and the potential to generate over 60 lakh jobs. In the medium term, the scheme will help reduce net imports by building domestic manufacturing capacity that will cater to domestic and global needs.

Introduction

9.1 Industry holds a prominent position in the Indian economy, accounting for 31 per cent of GDP, on average, during FY12 and FY21 and employing over 12.1 crore people. The sector’s relevance can be identified through various direct and indirect linkages with other sectors, contributing to economic growth and employment. First, it ensures that domestic production can accommodate domestic demand and reduces the reliance on imports. Thereby assisting in the improvement of trade and current account balances. Second, industrial growth has multiplier effects, which translates into employment growth. Some industries, such as textiles and construction, have high employment elasticities. Third, industrial growth spurs growth in services sectors such as banking, insurance, logistics, etc.

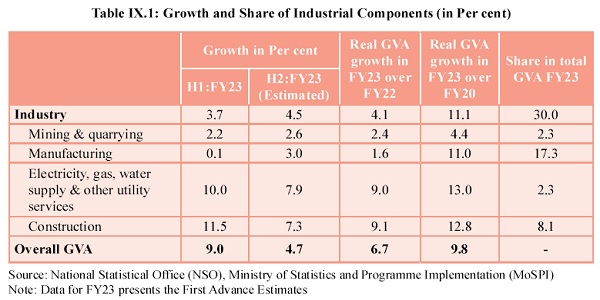

9.2 Industrial production is a means to increase industrial income in the country. As measured by industrial GVA, growth in industrial income has kept pace with overall GVA growth in the economy since the pre-pandemic year of FY20. Manufacturing GVA, which contributes more than 50 per cent of industrial GVA, has grown at an even higher rate when compared to overall GVA. In FY23, the Industry sector witnessed modest growth of 4.1 per cent compared to the strong growth of 10.3 per cent in FY22. This is likely on account of input cost-push pressures, supply chain disruptions and the China lockdown impacting the availability of essential inputs and slowing the global economy. The fading away of the base effect must have also weighed on growth in FY23. On a positive note, estimates of H2:FY23 shows improvement in overall industrial growth, especially in the manufacturing sector, both yearly and sequentially. Easing input prices and conducive demand conditions will support growth, ceteris paribus.

9.3 In this chapter, the survey will review the performance of the Indian industry in the current financial year. It explores the demand stimulants to industrial growth, the supply response of the industry, trends in credit to the industry and foreign investment in India’s industrial sector. The chapter also addresses the developments in key sub-industries and their challenges. Towards the end, it evaluates India’s aspirations and prospects of becoming a key player in global value chains.

Demand Stimulus to Industrial Growth

9.4 FY23 began with the month-old Russian-Ukraine conflict showing no signs of relenting. As the year draws to a close, the conflict appears to have plateaued, although global commodity prices are yet to deescalate to their pre-pandemic levels. Industry, throughout the year, has thus faced high input costs imported into the country. Fearing demand impact, the industry has been gradually passing on the higher production costs, which has led to sticky but non-rising core retail inflation. Non-core retail inflation, on the other hand, comprising food and energy components, has been declining as local weather extremities have eased and interventions by the government to restrict price rises have proven effective. The consequent decrease in overall retail inflation has thus sustained the pent-up consumer demand in the post-pandemic Indian economy, inducing an industrial recovery despite the global headwinds. With world commodity prices now also on a downward trajectory and showing up in declining rates of India’s wholesale inflation, core retail inflation is expected to relent, making domestic consumption demand much stronger to further induce industrial growth in the country. PFCE as a share of GDP in H1 of FY23 was the highest since FY15.

9.5 Strong external demand also served the Indian industry well in FY22 when manufactured exports soared, responding to a rebound in global growth. Trade had also recovered and grown as bottlenecks in global supply chains eased. The export stimulus for the Indian economy persisted in the first half of FY23. In this half of the year, exports of goods and services as a share of GDP have been the highest since FY16. However, the export impulse has been waning in the first half itself as the YoY growth of exports has declined from Q1 to Q2 due to persistently high inflation and rising interest rates in the advanced economies. Export growth may slow further in the second half of the current financial year and remain weak beyond that, too, if the global economy falls into recession. However, the strong domestic consumption growth and investment revival is expected to keep industrial production humming.

9.6 Indeed, an increase in investment demand has emerged as another powerful stimulus to industrial growth. It has been triggered by a jump in the Capex of the central government in the current and the previous year as compared to the pre-pandemic years. The leap also has crowded-in private investment, already upbeat on the pent-up consumption demand, export stimulus, and strengthening of the corporate balance sheets. Capacity utilisation at 74.3 per cent in Q1 of FY23 has already reached the tipping point of 75.3 per cent in Q4 of FY22, at which investments in building new capacities are undertaken. New Investment announced in the manufacturing sector during April-December of FY23 was five times the corresponding level in FY20. The surge in investment is also attributable to the policy actions taken by the Government over the past several years. A beginning has been made in H1 of FY23, which recorded the highest share of Gross Fixed Capital Formation (GFCF) in GDP among all half-years since FY15.

Box IX.1: Unfolding of Private Capital Investment Cycle

A view is fast emerging that the private sector is predisposed to increasing investment in the third decade of the new millennium. This has roots in the first decade of the new millennium when a credit boom financed rising levels of investment rates. Consequently, by the time the second decade began, the balance sheets of both the corporates and banks became stressed. As a result, corporates switched focus from investment to deleveraging while banks slowed credit disbursement in view of high Non-Performing Assets (NPAs). Consequently, the investment rate declined, and the economy began to slow. Midway into the second decade, the problems were identified, and mitigation measures were initiated. For the banks, the Insolvency and Bankruptcy Code (IBC) was instituted to resolve their stressed assets while the equity base of public sector banks was strengthened. For the corporates, the Goods and Services Tax (GST) rollout improved their ease of doing business while the corporate tax rate was slashed to increase their profits/ investible reserves for financing investment. During the pandemic, the implementation of ECLGS lent additional support to the MSMEs. Maturing digital infrastructure and easy and cheap data access have further enriched the investment climate.

Source: Bank for International Settlements (BIS)

Note: Credit to the non-financial sector captures the borrowing activity of the private non-financial sector.

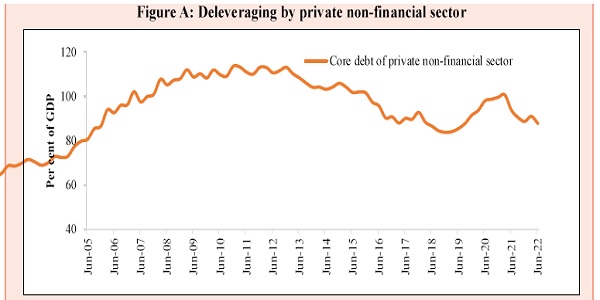

Deleveraging has strengthened the corporate balance sheets, as evident in the declining core debt of the private non-financial sector. Credit to the private non-financial sector as a percentage of GDP in India had come down from a peak of 113.0 per cent in December 2010 to a low of 83.8 per cent in December 2018. This shows that de-leveraging was completed by the end of 2018. With the elections out of the way in May 2019 and with corporate tax cuts announced in September 2019, it would have resulted in an improvement in investment and economic growth cycles, but it was delayed due to the disruption caused by the pandemic for two years. Deleveraging resumed from the beginning of FY22 as core debt of the private non-financial sector decreased to 87.8 per cent of GDP in the June 2022 quarter from 100.7 per cent in the March 2021 quarter on the back of improved corporate performance and a recovery in GDP levels.

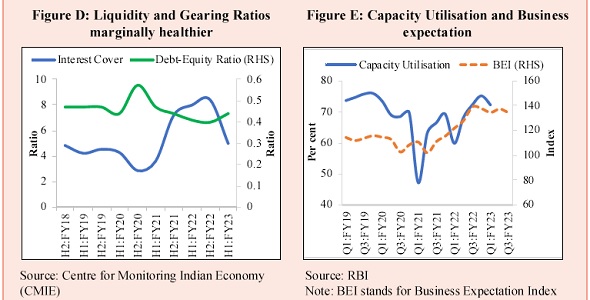

During H1 :FY23, the interest coverage ratio was 5, higher than its five-year (FY20) average of 3. The debt-equity ratio also declined from 0.8 to 0.4. These improvements have further absorbed the increase in working capital requirements triggered by volatility in global commodity prices and supply chain disruptions. On the other hand, profit margins peaked in the second half of FY21 as low inflation kept input costs from rising while restricted mobility reduced overheads. Subsequently, profit margins started to decline as input costs rose on the back of rising global commodity prices. With global commodity prices declining, input costs are set to fall, and profit margins are expected to increase. Expected increases in profits and strengthened balance sheets have made the corporate sector financially stronger and optimistic about increasing net sales. The Reserve Bank of India’s (RBI) Industrial Outlook Survey conducted during July-September 2022 points towards optimism about production, order books, employment, and profit margins for the period covered until Q1 of FY24.

The credit boom in the first decade increased the banking sector advances to the non-financial sector from 36.5 per cent of GDP in 2004 to 57.3 per cent in 2014 (Bank for International Settlements). This led to the RBI imposing a more stringent assessment of NPAs. Consequently, NPAs rose from 4.3 per cent of gross bank advances in FY15 to 11.2 per cent in FY18. However, with the enforcement of the IBC code and a more disciplined approach to credit disbursements, NPA fell to 7.3 per cent in FY21 and to a seven-year low of 5.0 per cent in September 2022. The Capital-to-Risk-Weighted Assets Ratio (CRAR) and provisioning coverage ratio (PCR) have also improved and stood at 16.0 per cent and 71.5 per cent, respectively, in September 2022. With well-capitalised banks ready and willing to lend and corporates financially stronger and willing to borrow, the credit-investment cycle is poised for an upturn in the third decade.

Supply Response of Industry

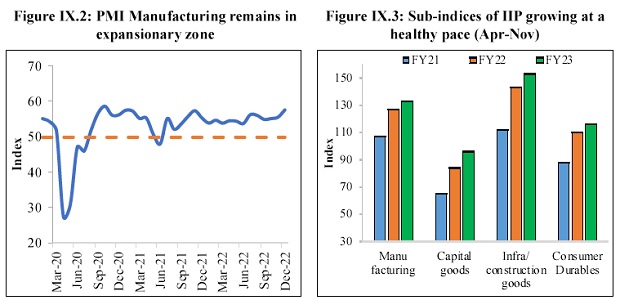

9.7 The supply response of the industry to the demand stimulus has been robust, as seen in high-frequency indicators. The PMI-Manufacturing, for example, has remained in the expansionary zone for 18 months since July 2021. In December 2022, the sub-indices of the PMI-Manufacturing indicated an easing pace of input cost pressures, improving supplier delivery times, robust export orders, and future output. The moderation in input cost inflation has also led to an easing in the momentum of output prices. However, the pace of expansion in new export orders decreased, reflecting a subdued global demand.

9.8 The sustained growth of manufacturing output is also seen within the overall IIP producing consumer durables in sync with the “pent-up” consumption demand. Robust growth in the production of capital goods and infrastructure/construction goods is indicative of the beginnings of an investment cycle in the private sector in the next financial year.

Source: IHS Markit Source: MoSPI

9.9 The eight core industries of coal, fertilisers, cement, steel, electricity, refinery products, crude oil, and natural gas are critical in meeting the demand for inputs across industries. The growth in these industries has held steady, reflecting a broad momentum in industrial activity. Their growth underscores the importance that nations have been attaching to the indigenous presence of core capacities in the aftermath of the pandemic and the Russia-Ukraine conflict breaking down the global supply chain.

Source: Department for Promotion of Industry and Internal Trade (DPIIT)

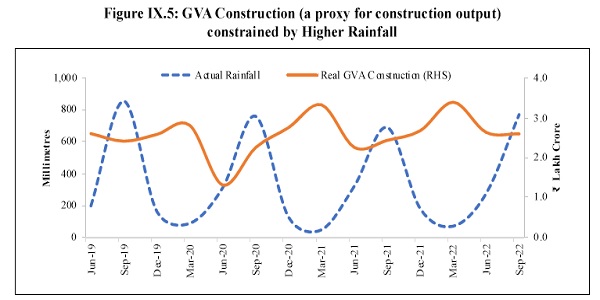

9.10 Growth in industrial output would have been higher, but for some constraints it faced in the first half of FY23. Seasonality has contributed to constraining the growth of production in respect of mining and quarrying, and construction, as total rainfall in Q2 of FY23 was about 12 per cent higher than in Q2 of FY22. Further, as higher rainfall cooled temperatures, electricity demand fell, and hence output rose by less than 5 per cent in Q2 of FY23 over Q2 of FY22.

Source: MoSPI

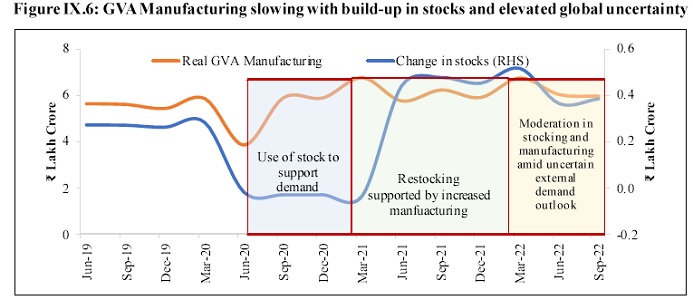

9.11 Manufacturing output appears to have been constrained by a large build-up in inventory. For five consecutive quarters ending in Q2 of FY23, an increase in stocks had accumulated to more than 1.3 per cent of the annual GDP. A typical cycle of change-in-stocks juxtaposed with the growth of manufacturing GVA (a proxy for manufacturing output) suggests that the build¬up of stock allows manufacturing to slow its pace with the accumulated stock meeting current demand. When stocks start shrinking, manufacturing output increases to meet current demand and replenish stocks before the onset of the next cycle. Stock build-up appears to have thus played an important role in keeping the growth of manufacturing output restrained in Q2.

Source: MoSPI; Note: Change in stocks refers to change in stocks of GFCF.

9.12 The manufacturing landscape shows uneven growth across various categories. For example, the motor vehicles manufacturing segment’s performance continues to improve, induced by robust demand and an easing of chip shortage. The manufacturing of ‘computer, electronic and optical products’, an upcoming industry, has also been rising. Multiple players looking to make India a manufacturing hub of semiconductors have made the investment outlook in this sector positive. Production of coke and refined petroleum has also increased, fetching high returns in a global market where crude oil prices were higher than in FY22. Chemicals and chemical products such as caustic soda, soda ash, fertilisers and petroleum products have also performed well, contributing to sustaining the growth momentum in the agriculture sector while increasing exports. At the same time, a few product categories, including textiles, apparel and leather, have been showing tepid growth, as export demand for these products has been mellowing with the slowing of global output and demand. Growth in pharmaceutical output has slowed due to an unfavourable base effect and the waning of the pandemic.

Robust Growth in Bank Credit to Industry

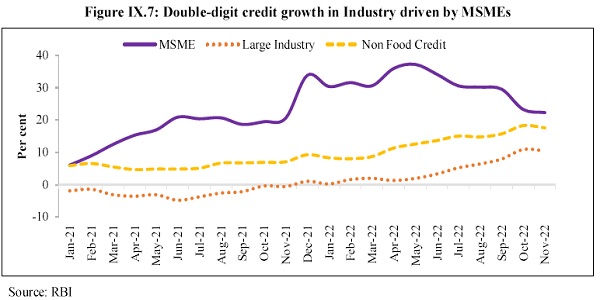

9.13 Growth in bank credit has kept pace with industrial growth, with a sequential surge evident since January 2022. While a large share of bank credit continues to be assigned to large industries, credit to MSMEs has also seen a significant increase in part assisted by the introduction of the ECLGS, which supports around 1.2 crore businesses of which 95 per cent are MSMEs 1. The impact of ECLGS on increasing the growth of credit to MSME was felt most during the pandemic impacted years of 2020 and 2021. It continued in 2022 as the scheme was extended to March 2023. Furthermore, growth in credit to MSME was buttressed by rebounding consumption levels, particularly in the services sector. Consequently, the share of MSMEs in gross credit offtake to the industry rose from 17.7 per cent in January 2020 to 23.7 per cent in November 2022. While the growth in total credit has been driven by an increase in credit demanded by MSMEs, large industries have also begun to increase the pace of their credit offtake since the beginning of FY23. With the spread between corporate bond yields and marginal costs of funds-based lending rate (MCLR) narrowing, and the volatility in the corporate bond market remaining high, corporates appear to be shifting their sources of financing from bond markets to bank capital, where rates have remained stable and predictable. Robust growth in credit demand combined with rising capacity utilisation and investment in manufacturing underscores businesses’ optimism regarding future demand.

9.14 All segments within the manufacturing sector except the textile industry witnessed growth in credit offtake in November 2022. While segments such as “Petroleum, coal products and nuclear fuels”, “Rubber, plastic and their products”, and “Engineering” have had a steady credit appetite, the improvement in growth of credit to the cement and construction sectors over the past year reflects the improved outlook of the construction sector.

Resilient FDI inflow in Manufacturing Sector

9.15 Annual FDI equity inflows in the manufacturing sector have been steadily increasing over the last few years. It jumped from US$ 12.1 billion in FY21 to US$ 21.3 billion in FY22 as the pandemic-driven expansionary policies of advanced economies led to a surge in global liquidity. With the rise in global uncertainty in the wake of the Russia-Ukraine conflict, FDI equity inflow in manufacturing in the first half of FY23 fell below its corresponding level in the first half of FY22. The monetary tightening at the global level has further restricted the FDI equity inflows. A rebound in FDI inflows is, however, expected as the Indian economy sustains its high growth while monetary tightening the world over eventually eases with the weakening of inflationary pressures.

9.16 Notwithstanding an overall drop in FDI in the first half of FY23, inflows have stayed above the pre-pandemic levels, driven by structural reforms and measures improving the ease of doing business, making India one of the most attractive FDI destinations in the world. The government has implemented an investor-friendly FDI policy under which FDI up to 100 per cent is permitted through automatic route in most sectors. India continues to open up its sectors to global investors by raising FDI limits, removing regulatory barriers, developing infrastructure, and improving the business environment.

Box IX.2: FDI Policy Reforms to bolster Investment

- India continues to open up its sectors to global investors by raising FDI limits and removing regulatory barriers to attracting increased investments, in addition to developing infrastructure and improving the business environment. To make India a more attractive investment destination, the Government has implemented several radical and transformative FDI reforms across sectors such as Defence, Pension, e-commerce activities etc.

- In FY20, 100 per cent FDI under automatic route was permitted for the sale of coal, and coal mining activities, including associated processing infrastructure, subject to provisions of relevant acts. 26 per cent FDI under the government route has been permitted for uploading/ streaming of News & Current Affairs through Digital Media. 100 per cent FDI has been permitted in Intermediaries or Insurance Intermediaries, including insurance brokers, reinsurance brokers, insurance consultants, corporate agents, third-party administrators, Surveyors and Loss Assessors and such other entities as may be notified by the Insurance Regulatory and evelopment Authority from time to time.

- To curb opportunistic takeovers/acquisitions of Indian companies due to the Covid- 19 pandemic, the government amended the FDI policy, according to which an entity of a country which shares a land border with India or where the beneficial owner of investment into India is situated in or is a citizen of any such country, can invest only under the Government route. Further, in the event of the transfer of ownership of any existing or future FDI in an entity in India, directly or indirectly, resulting in the beneficial ownership falling within the restriction/purview of the said policy amendment, such subsequent change in beneficial ownership will also require government approval.

- To simplify the approval process of foreign Investment and to promote ease of doing business, the erstwhile Foreign Investment Promotion Board (FIPB) was abolished in May 2017, and a new regime has been put in place. Under the new regime, the process for granting FDI approvals has been simplified, wherein the work relating to the processing of applications for FDI has been delegated to the concerned Ministries/ Departments, and DPIIT is the nodal department for facilitating the process.

- A revamped portal, “Foreign Investment Facilitation Portal (FIF Portal)”, has been launched as the online single-point interface of the Government of India for investors to facilitate Foreign Direct Investment. The portal facilitates single window clearance of applications which are through the government approval route. The FIF Portal has been integrated with the National Single Window System (NSWS).

Industry Groups and their Challenges

Micro, Small and Medium Enterprises (MSMEs) post smart recovery from pandemic

9.17 While the contribution of the MSME sector to overall GVA rose from 29.3 per cent in FY18 to 30.5 per cent in FY20, the economic impact of the pandemic caused the sector’s share to fall to 26.8 per cent in FY21. MSME contribution to the manufacturing sector’s GVA also marginally fell to 36.0 per cent in FY21.

9.18 Through the AatmaNirbhar Bharat Package, the government has taken multiple steps to cushion the economic impact of the pandemic on MSMEs. Some of the measures undertaken include the modification of the definition of MSMEs; the provision of ₹20,000 crore subordinate debt for stressed MSMEs, ₹50,000 crore equity infusion through Self Reliant India fund; the waiving of the global tender requirement for procurement of up to ₹200 crore; launching of the Udyam portal for MSME registration, a paperless, zero-cost registration portal that is based on self-declaration and only requires Aadhaar. Registrations on the Udyam portal crossed the one¬crore mark in August 2022, surpassing the total registration done in the past 14 years under the old regime in just 2.5 years. As of 7th January 2022, the portal has a total registration count of 1.32 crore, of which 1.27 crore have been classified as micro-enterprises. Enterprises registered on the portal employ 9.6 crore people, of which 2.3 crore are women. There are 1.5 lakh exporting units, which have contributed a cumulative ₹9.7 lakh crore worth of exports.

9.19 The government’s initiative of the Samadhaan Portal, set up under the Micro, Small and Medium Enterprises Development (MSMED) Act to monitor the outstanding dues to the MSME sector, is helping MSMEs in resolving their cashflow difficulties. As of 7th January 2022, the portal has received a total of 1.3 lakh applications, of which 16.8 per cent have been disposed while 25.0 per cent are currently under consideration, and 25.1 per cent have been rejected. In order to fast-track this process, the government has instructed Central Public Sector Enterprises (CPSEs) and all companies with a turnover of ₹200 crore or more to get themselves onboarded on the Trade Receivables Discounting System (TReDS) platform for facilitating the discounting of trade receivables of MSMEs through multiple financiers. CHAMPIONS, the single-window grievance redressal portal for MSMEs launched by the Ministry of MSME in June 2020, has received 56,825 grievances as of 16th January 2023, of which 55,878 grievances have been responded to. The portal continues to be improved through initiatives such as the localisation of the portal in 11 regional languages and the introduction of a Chatbot.

9.20 The government has also initiated the ‘Raising and Accelerating MSME Performance’ scheme (RAMP) in FY23. The World Bank-supported scheme aims at strengthening institutions and governance at the Centre and State, improving Centre-State linkages and partnerships and improving access of MSMEs to market and credit, technology upgradation and addressing issues of delayed payments and greening of MSMEs. The RAMP programme will be implemented over a period of five years. The total outlay for the scheme is ₹6,062.4 crore, out of which ₹3750 crore would be a loan from the World Bank, and the Government of India would fund the remaining ₹23 12.4 crore.

9.21 The bouquet of measures introduced by the government aided the resilience of the MSME sector. Data from the National Credit Guarantee Trustee Corporation (NCGTC) shows that as of 30th November 2022, 1.2 crore MSME units availed the ECLGS scheme and raised collateral-free resources to the tune of ₹3 .6 lakh crore. A recent CIBIL report2 showed that 83 per cent of the borrowers who availed of the ECLGS were micro-enterprises, and more than half of these borrowers had an exposure of less than ₹10 lakh. The NPA rate in banks for the category of MSME borrowers who availed of ECLGS was lower than the category that did not avail of the scheme. The recovery of the MSME sector from the pandemic-induced shock is evident in the trend in GST paid by MSME units. The GST paid by the sector in FY22 has crossed the pre-pandemic level in FY20.

Electronics industry to be a key driver of manufacturing output and exports.

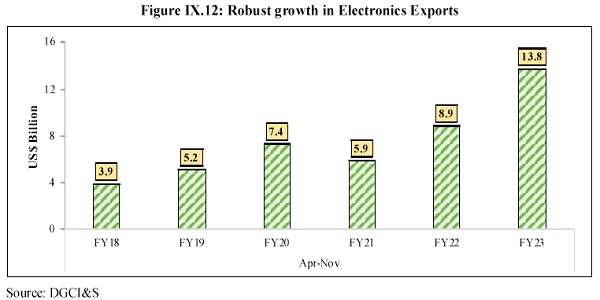

9.22 The electronics industry continues to ascend in importance as its applications become pervasive, particularly in the socio-economic development of a country. Electronics, supported by continuously improving communication services, will significantly enhance productivity, efficient service delivery, and social transformation. The domestic electronics industry, as of FY20, is valued at US$118 billion. India aims to reach US$300 billion worth of electronics manufacturing and US$ 120 billion in exports by FY263, supported by the vision of a US$ 1 trillion digital economy by 2025. Improvement in manufacturing and export over the past five years ensures that India is on the right trajectory to achieve this target. Electronic goods were among the top five commodity groups exhibiting positive export growth in November 2022, with the exports in this segment growing YoY by 55.1 per cent.

9.23 The major drivers of growth in this industry are mobile phones, consumer electronics, and industrial electronics. In the mobile phone segment, India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from six crore units in FY15 to 31 crore units in FY22. These numbers are expected to improve as more domestic and global players set up and expand their bases in India. Two major global and domestic players in electronic manufacturing services have already embraced the PLI scheme4. Participation in the PLI scheme will help many more domestic players to attain economies of scale in production through localising. Hence, this will further enhance export competitiveness and increase India’s participation in the global value chain. The industrial electronics sector is also seeing growth due to improved digitisation and robotics applications in Industry 4.0. Additionally, the impetus on Smart Cities and the Internet of Things (IoT) will streamline the demand for smart and automated electronics.

9.24 Some of the initiatives and incentives provided by the government to nurture and enhance the electronics manufacturing base include the PLI scheme for Large Scale Electronics Manufacturing, the PLI scheme for IT hardware, the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS). Additionally, under the Programme for Development of Semiconductors and Display Manufacturing Ecosystem in India, the Cabinet approved the comprehensive development of a sustainable semiconductor and display ecosystem in the country with an outlay of ₹76,000 crore, the details of which are in Box 3. These schemes and initiatives are expected to boost India’s manufacturing capacity, reduce import dependence, and also contribute to achieving the country’s ambitions of becoming a major player in global supply chains.

Box IX.3: Incentives to encourage semiconductor manufacturing in the US and India

The global economic recovery from the Covid-19 pandemic exposed the frailties in the supply chains of many goods and services. One product that was under the spotlight was the semiconductor (more commonly referred to as ‘chips’), and the effect of its shortage was particularly amplified in the automotive industry globally. While the situation has limped back to normalcy, it has prompted a policy response by countries towards diversifying the semiconductor supply chain.

One of the most notable policies is the United States’Creating Helpful Incentives to Produce Semiconductors and Science Act, 2022 (CHIPS and Science Act, 2022). The legislation aims to catalyse investments in the domestic semiconductor manufacturing capacity of the US. The country produces about 10 per cent of the world’s semiconductors and relies heavily on East Asia to import chips. The CHIPS and Science Act directs US$ 280 billion in spending over the next ten years, with the bulk of it going to Research and Development (R&D).

In the pursuit of Aatmanirbharta and with the objective of plugging itself into the global value chain, India has announced multiple incentives to attract investment for developing a semiconductor manufacturing ecosystem. To this end, a comprehensive programme with an outlay of ₹76,000 crore (approx. US$ 10 billion) was approved by the Government of India in September 2022. The government will provide financial support for 50 per cent of the capital expenditure to be incurred by the investing firms.

Recognising that even though India possesses 20 per cent of the world’s semiconductor design engineers but a minuscule share in the intellectual property (IP), the Government of India has also announced a Design Linked-Incentive (DLI) scheme. The scheme’s objectives include the nurturing and facilitation of domestic companies of semiconductor design, achieving significant indigenisation of semiconductor products and IPs deployed across the country, and strengthening the infrastructure for design. The scheme will provide financial support of 50 per cent of eligible expenditure the design, subject to a ceiling of ₹15 crore per applicant and a deployment-linked incentive 4 per cent to 6 per cent of net sales achieved over five years, subject to a ceiling of ₹30 crore per applicant. While these are early stages, global and domestic players have evinced interest based on the prospects for the semiconductor industry in India and the fiscal incentives provided. Israel-based International Semiconductor Consortium has signed a Memorandum of Understanding (MoU) to invest ₹22,900 crore in Karnataka to set up India’s first chip-making plant. Domestic players such as Vedanta and Tata have also indicated plans to establish semiconductor fabs in the country.

CoaI Industry: Key in maintaining energy self-reliance during uncertain times

9.25 At the beginning of the fiscal year, coal availability became a challenge for India’s largely thermal-based power generation plants because of a resurgence in economic activity and the emergence of intense heat waves from early March to mid-May of 2022, increasing the demand for power in the country. In addition, in the wake of rising international coal prices, the power sector curtailed coal import drastically from 69 MT in FY20 to 45 MT in FY21 and further to 27 MT in FY22. As domestic coal production could not keep pace with its rising demand from power-generating plants, its availability got limited. Resultantly, in April 2022, even as coal offtake rose to meet higher demand, coal stock with power plants, as on 31st April 2022, fell to 8 days from 12 days a year ago.

9.26 The government of India undertook several steps on a priority basis through April and May of 2022 to address the supply constraints of coal. First, all generators were asked to import coal to the extent of 10 per cent of their requirements (as against 4 per cent earlier). Penalties, including curtailment of domestic coal entitlements, were announced if power plants failed to import coal. Second, Section 11 of the Electricity Act 2003 (Act) was invoked to direct imported coal-based plants to run at full capacity with the assurance that their enhanced cost of operation would be compensated. Third, tolling was enabled, which allowed states to transfer their allotted coal to private generators near the mines instead of transporting it too far away from state generators. This move eased the burden on the availability of railway rakes. Fourth, Rural Electrification Corporation (REC)/ Power Finance Corporation (PFC) and commercial banks were advised to facilitate the availability of additional working capital to power generating plants.

9.27 Well-timed measures have placed India in a better position to cater to excess energy demand. The coal production for FY23 is estimated to increase to 911 million tonnes, about 17 per cent higher compared to the previous year. In April-December, 2022, coal production rose by 14 per cent on a YoY basis and was 21 per cent higher than the pre-pandemic of FY20. Further, the coal stock at power plants improved to 12 days as of 30 December 2022 compared to 10 days on 30 June 2022 and 8 days a year ago.

9.28 Different measures have been initiated towards achieving self-reliance in coal production, including private participation in coal production, FDI under the automatic route, auctioning of coal blocks for commercial production, expansion of existing mines and opening of new mines, greater use of mass production technology in mining, mechanisation of loading, development of evacuation infrastructure etc.

9.29 The coal industry is expected to grow at 6-7 per cent annually to reach a production level of 1 billion tonnes by FY26 and about 1.5 billion tonnes by 2030. The enhanced domestic coal production is expected to meet domestic coal demand, replace substitutable imports, and escalate exports. There has also been a persistent effort to improve system capacity utilisation from about 80 per cent to above 90 per cent.

Re-invigorated infrastructure sector & construction activity to drive steel industry.

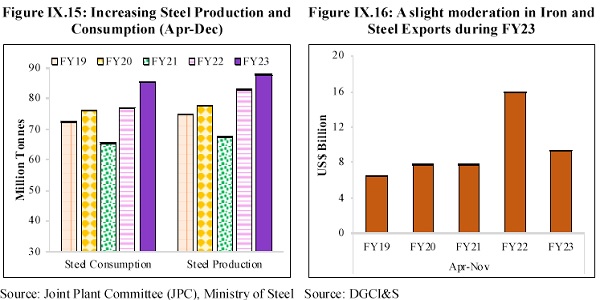

9.30 Steel Sector plays a pivotal role in crucial sectors such as construction, infrastructure, automobile, engineering and defence. Over the years, the steel sector has witnessed tremendous growth. The country is now a global force in steel production and the 2nd largest crude steel producer in the world. The steel sector’s performance in the current fiscal year has been robust, with cumulative production and consumption of finished steel at 88 MT and 86 MT, respectively, during April-December 2022, higher than the corresponding period during the previous four years. The growth in finished steel production is aided by double-digit growth in consumption (11 per cent on a YoY basis), bolstered by a pick-up in the infrastructure sector significantly driven by increased Capex of the government.

9.31 Further, 67 applications from 30 companies have been selected under the PLI Scheme for speciality steel. This will attract a committed investment of ₹42,500 crore, with an increase in capacity by almost 26 million tons and an employment generation potential of nearly 70,000 people. Further, domestic steel makers’ stable credit profiles, deleveraged balance sheets, and robust cash accrual support continue to support their capex. Iron and steel exports moderated in the first eight months of the current fiscal owing to a slowdown in the global economy, particularly in Europe and China, and export duty levied to enhance domestic availability. Yet, iron and steel exports are higher by 20 per cent over the corresponding pre-pandemic levels of FY20.

9.32 In the future, the government’s thrust towards infrastructure projects, pick-up in construction and real estate activity, and healthy demand from the automobile sector augur well for the demand for steel products. However, export demand may remain subdued with the global slowdown.

Government support to help textile Industry weather current challenges.

9.33 The Textile industry is one of the country’s most significant sources of employment generation, with an estimated 4.5 crore people directly engaged in this sector, including a large number of women and the rural population. In the current financial year, the textile industry has been facing the challenge of moderating exports compared to FY22. However, the levels in the eight six months still prevail, 9.5 per cent higher than the corresponding pre-pandemic level of FY20. Export of readymade garments registered a growth of 3.2 per cent YoY basis during the same period. FDI inflows into the textile sector are yet to recover to pre-pandemic levels.

9.34 To develop integrated large-scale and modern industrial infrastructure facilities for the entire value chain of the textile industry, the government approved the setting up of seven PM Mega Integrated Textile Region and Apparel (PM MITRA) Parks. The parks will not only reduce logistics costs and improve the competitiveness of Indian Textiles but also boost employment generation, attract domestic investment and FDI, and position India firmly in the global textile market. The parks are expected to create a total of one lakh direct and two lakh indirect employment.

9.35 Further, to boost the production capacity, the government launched the Textile PLI Scheme with an approved outlay of ₹10,683 crore over five years starting from 1st January 2022 to promote investments and increase the production of Man-Made Fibre (MMF) Apparel, MMF Fabrics and Products of Technical Textiles. This will enable the textile sector to achieve size and scale, enhancing export competitiveness. In the approved 64 applications so far, the proposed total investment commitment is ₹19,798 crore, with projected turnover and employment generation of ₹1 .9 lakh crore and 2.5 lakh, respectively.

Growth momentum in pharmaceuticals industry sustains after the pandemic

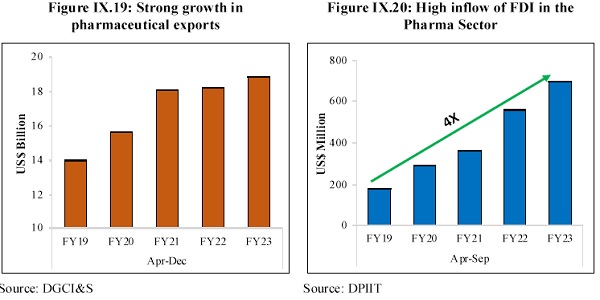

9.36 The Indian Pharmaceuticals industry plays a prominent role in the global pharmaceuticals industry. India’s domestic pharmaceutical market is estimated at US$ 41 billion in 2021 and is likely to grow to US$ 65 billion by 2024 and is further expected to reach US$ 130 billion by 20305. India is ranked 3rd worldwide in the production of pharma products by volume and 14th by value. The nation is the largest provider of generic medicines globally, occupying a 20 per cent share in global supply by volume, and is the leading vaccine manufacturer globally with a market share of 60 per cent.

9.37 Indian pharmaceutical exports achieved a healthy growth of 24 per cent in FY21, driven by Covid-19-induced demand for critical drugs and other supplies made to over 150 countries. The performance of pharma exports in FY22 has been robust, sustaining growth despite the global trade disruptions and drop in demand for Covid- 19-related treatments. Carrying forward this growth momentum, drug and pharmaceutical exports during April-October 2022 was 22 per cent higher than the corresponding pre-pandemic period of FY20. Cumulative FDI in the pharma sector crossed the US$ 20 billion mark in September 2022. Further, FDI inflows have increased four-fold over five years until September 2022, to US$ 699 million, supported by investor-friendly policies and a positive outlook for the industry.

9.38 The government has undertaken various measures to improve the infrastructural facilities of the pharma sector. The concerned scheme, Strengthening the Pharmaceutical Industry (SPI), was launched on 11th March 2022 with a total financial outlay of ₹500 crore for five years from FY22 to FY26 with multiple objectives. First, it aims to strengthen the existing infrastructure facilities by providing financial assistance to pharma clusters to create common facilities. Second, it upgrades the production facilities of MSMEs to meet national and international regulatory standards by providing interest subvention or capital subsidy on their capital loans. Third, it also promotes knowledge and awareness about the pharmaceutical and medical devices industry by undertaking studies, building databases and bringing industry leaders, academia and policymakers together to share their knowledge and experience.

India becomes the world’s 3rd largest automobile market

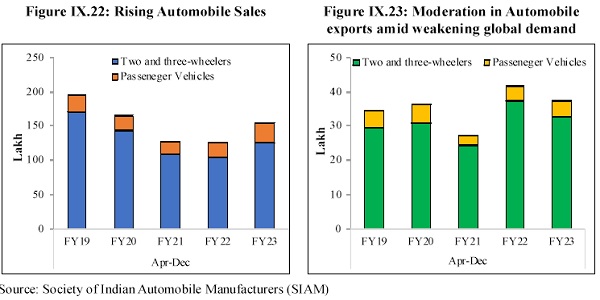

9.39 The automobile sector is a key driver of India’s economic growth. In December 2022, India became the 3rd largest automobile market, surpassing Japan and Germany in terms of sales. In 2021, India was the largest manufacturer of two-wheeler and three-wheeler vehicles and the world’s fourth-largest manufacturer of passenger cars. The sector’s importance is gauged by the fact that it contributes 7.1 per cent to the overall GDP and 49 per cent to the manufacturing GDP while generating direct and indirect employment of 3.7 crore at the end of 2021.

Figure IX.22: Rising Automobile Sales Figure IX.23: Moderation in Automobile

exports amid weakening global demand

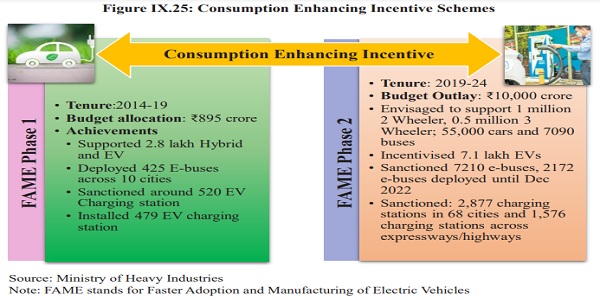

9.40The automotive industry is expected to play a critical role in the transition towards green energy. The domestic electric vehicles (EV) market is expected to grow at a compound annual growth rate (CAGR) of 49 per cent between 2022 and 2030 and is expected to hit one crore units annual sales by 2030. The EV industry will create 5 crore direct and indirect jobs by 20306. To support and nurture this development, the government has undertaken multiple steps.

9.41 Despite the upbeat outlook, the automotive industry faces certain challenges. Higher borrowing costs and tempering global demand are expected to be near-term hurdles. Amongst structural issues, the increase in long-term third-party vehicle insurance premiums has increased the total upfront insurance cost by about 10-11 per cent, especially for two-wheelers. Therefore, the two-wheeler segment is the most affected and witnessed the lowest sales in the last ten years. Addressing these challenges will boost the automobile industry.

India’s Prospects as a Key Player in the Global Value Chain

9.42 The risk of supply chain shocks has never been more palpable than today, following compounding crises from the US-China trade war, the Covid- 19 pandemic, and the war in Ukraine. In this fast-evolving context, as global companies adapt their manufacturing and supply chain strategies to build resilience, India has a unique opportunity to become a global manufacturing hub this decade. The three primary assets to capitalise on this unique opportunity are the potential for significant domestic demand, the Government’s drive to encourage manufacturing, and a distinct demographic edge, including a considerable proportion of the young workforce. The manufacturing sector in India is gradually shifting to more automated and process-driven manufacturing, which is expected to increase efficiency and boost the production of the industry. The ‘Make-in-India’ Initiative was launched in 2014 to make India a hub for manufacturing, design, and innovation. Since then, it has facilitated investment, fostered innovation and built world-class infrastructure. The progress made in infrastructure development is discussed in chapter 12 “Physical and Digital Infrasturcture: lifting potential growth”.

Make in India 2.0 and the PLI schemes

9.43 To further enhance India’s integration in the global value chain, ‘Make in India 2.0’ is now focusing on 27 sectors, which include 15 manufacturing sectors and 12 service sectors. Amongst these, 24 sub-sectors have been chosen while keeping in mind the Indian industries’ strengths and competitive edge, the need for import substitution, the potential for export and increased employability. Efforts are on to boost the growth of the sub-sectors in a holistic and coordinated manner.

9.44 In pursuit of the objectives of the Make-in-India programme and with a vision to achieve Aatmanirbharta, the government launched the PLI scheme. The scheme is expected to attract a capex of approximately ₹3 lakh crore over the next five years. It has the potential to generate employment for over 60 lakh in India and increase the share of the manufacturing sector in total capital formation, which currently stands at around 17-20 per cent between FY12 and FY20. It is further believed that there will be a significant reduction in the trade deficit with domestic production substituting for imports. Sectors under which the PLI scheme has been announced currently constitute around 40 per cent of the total imports. The scheme, spread across 14 sectors, can enhance India’s annual manufacturing capex by 15 to 20 per cent from FY23.

9.45 PLI Scheme across these key specific sectors is poised to make Indian manufacturers globally competitive, attract investment in the areas of core competency and cutting-edge technology; ensure efficiencies; create economies of scale; and make India an integral part of the global value chain. The scheme will benefit the MSME ecosystem in the country. The anchor units built in every sector will require a new supplier base in the entire value chain. Most of these ancillary units will be built in the MSME sector.

9.46 As of 31st December 2022, 717 applications have been approved under 14 Schemes. More than 100 MSMEs are among the PLI beneficiaries in sectors such as Bulk Drugs, Medical Devices, Telecom, White Goods and Food Processing. As per recent reporting from implementing Ministries/ Departments, around ₹47,500 crore (US$ 6 billion) of actual investment has been made; production/ sales of ₹3.85 lakh crore (US$ 47 billion) of eligible products and employment generation of around 3 lakh has been reported and 106 per cent achievement of actual investment reported versus the corresponding projections of FY227. Key sectors such as Large-Scale Electronics Manufacturing, Pharmaceuticals, Telecom & Networking Products, Food Processing and White Goods have contributed considerably to investment, production, sales and employment.

9.47 Some of the latest developments under the PLI programme include the launch of a design-led PLI in June 2022 to promote the entire value chain in telecom manufacturing and to build a strong ecosystem for 5G as part of the PLI Scheme for Telecom & Networking products. Approvals under this Scheme have already been granted to eligible companies. In September 2022, the Cabinet recently approved PLI Scheme (Tranche II) on ‘National Programme on High-Efficiency Solar PV Modules’, with an outlay of ₹1 9,500 crore to build an ecosystem for manufacturing of high-efficiency solar PV modules in India, thus reducing import dependence in the area of renewable energy.

Box IX.4: Shipbuilding Sector: Achieving Self-Reliance and promoting Make in India

The Shipbuilding industry is a strategically important industry due to its role in energy security, national defence and the development of the heavy engineering industry. It has the potential to increase the contribution of the industry and the services sector to the national GDP. With its immense direct and indirect linkages with most other leading industries, such as steel, aluminum, electrical machinery and equipment etc., and its huge dependence on infrastructure and services sectors of the economy, the shipbuilding industry has the potential to strengthen the mission of an ‘Aatmanirbhar’ Bharat. The Indian Navy (IN) shipbuilding projects currently in progress at various Indian shipyards are poised to provide the requisite impetus to the industry. With the objective to achieve strategic independence in shipbuilding and development of niche technology, as of date, more than 130 IN warships have been constructed at Indian shipyards, and presently, 41 of 43 ships and submarines are being constructed at various public and private sector Indian shipyards. These initiatives, through various channels, are contributing to economic growth and employment in the country.

Boost to Ancillary Industry

Shipbuilding with its links to other ancillary industries, including steel, engineering equipment, port infrastructure, trade and shipping services has the potential to create a collaborative production eco-system. With the development of these ancillary industries, the sector generates opportunities for smaller businesses and strengthens supply chain networks. It is noteworthy that a significant proportion of value addition, approximately 65 per cent, in the construction of a ship is derived from manufacturers of shipboard materials, equipment, and systems.

Significant Investment and Employment Generation Multiplier Effects

Based on International shipbuilding statistics, if one takes a conservative Marginal Consumption to GDP Ratio (MCGR) of 0.45 for the shipbuilding sector, the investment multiplier would be approx. around 1.82. For example, an injection of approx. ₹1 .5 lakh crore in naval shipbuilding projects would accrue a circulation of ₹2.73 lakh crore in the shipbuilding sector due to the multiplier effect.

Among manufacturing activities, shipbuilding has one of the highest employment multipliers of 6.48. It is capable of generating mass employment in remote, coastal and rural areas, thereby absorbing the labour migrating from agricultural pursuits to manufacturing facilities established by shipyards and their ancillary industries. The Indigenisation initiatives implemented by the IN have resulted in a significant infusion of economic activity by creating employment opportunities for MSMEs and other industries. For instance, the recently commissioned INS Vikrant alone engaged approximately 500 MSMEs, 12,000 employees from ancillary industries, and 2,000 shipyard employees.

Further, a study undertaken by the IN for the construction of seven P1 7A ships reveals that around three-fourths of the total project cost of warships is invested back into the Indian economy. This investment is ploughed back into the economy through indigenous sourcing of raw materials, development of equipment and systems installed onboard ships and other manpower services.

Besides benefiting the ancillary industries and creating massive employment opportunities, an indigenous shipping and shipbuilding industry can also reduce freight bills and forex outgo, thereby reducing the current account deficit.

Thus, we see that the strong forward and backward linkages of the shipbuilding sector play an important part in the creation of a self-relient India.

Fostering Innovation

9.48 The government’s efforts towards fostering innovation include incubation, handholding, funding, industry-academia partnership and mentorship. The government has also strengthened its IPR regime by modernising the IP office, reducing legal compliances and facilitating IP filing for start-ups, women entrepreneurs, small industries and others. This has resulted in a 46 per cent growth in the domestic filing of patents over 2016-2021, signalling India’s transition towards a knowledge-based economy.

9.49 These measures have begun to pay dividends. The Global Innovation Index (GII) ranks the countries based on innovation performance, comprising around 80 indicators, including measures on the political environment, education, infrastructure and knowledge creation of each economy. As per the GII 2022 report, India entered the top 40 innovating countries for the first time in 2022 since the inception of the GII in 2007 by improving its rank from 81 in 2015 to 40 in 2022. Further, India became the most innovative nation in the lower middle-income group overtaking Vietnam (48th) and leading the Central and Southern Asia region.

Box XI.5: ‘Flipping and Reverse Flipping: the recent developments in Start-ups’

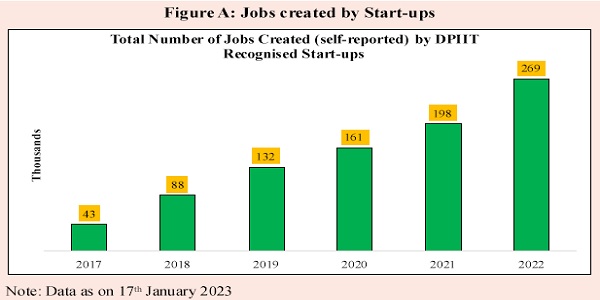

India ranks amongst the largest startup ecosystems in the world. An impressive 9 lakh+ direct jobs have been created by the DPIIT recognised startups (self-reported), with a notable 64 per cent increase in 2022 over the average number of new jobs created in the last three years. About 48 per cent of our startups are from Tier II & III cities, a testimony of our grassroots’ tremendous potential.

Various targeted initiatives of the Government have given a major boost to start-ups. For instance,under the Start-up India Initiative, eligible companies get recognised as Start-ups by DPIIT to access a host of tax benefits, easier compliance, and IPR (Intellectual Property Rights) fast-tracking. As part of the umbrella schemes of the National Initiative for Developing and Harnessing Innovations (NIDHI) and Atal Innovation Mission (AIM), entrepreneurship and innovation are fostered across the start-up ecosystem in the country. The Fund of Funds for Start-ups (FFS) and Credit Guarantee

Scheme for Start-ups (CGSS) support seed funding and successive credit needs. The R&D platform for technology sectors is offered by schemes such as MeitY Start-up Hub (MSH) and Technology Incubation and Development of Entrepreneurs (TIDE 2.0), among others. Engaging Indian start-ups with global peers is another essential pillar of Start-up India and is facilitated through Government-to-Government partnerships, participation in international forums, and hosting of global events. Further, the Support for International Patent Protection in E&IT (SIP-EIT) Scheme encourages international patent filing by Indian MSMEs and start-ups9.

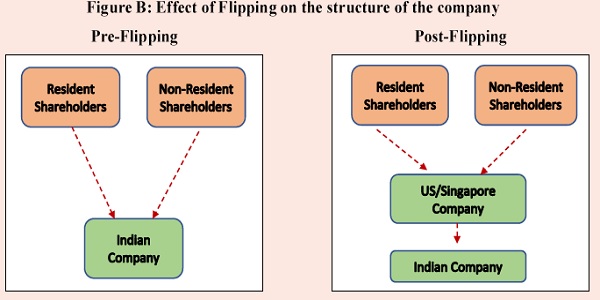

While external support from the government has made it relatively easier than before for entrepreneurship to thrive, there are several inherent challenges faced by start-ups. Be it ever-elusive funding, revenue generation struggles, lack of easy access to supportive infrastructure, or wading through the regulatory environment and tax structures. It has also been observed that many Indian companies have been getting headquartered overseas, especially in destinations with favourable legal environments and taxation policies. The technical jargon for this may be identified as ‘Flipping’, which is the process of transferring the entire ownership of an Indian company to an overseas entity, accompanied by a transfer of all IP and all data hitherto owned by the Indian company. It effectively transforms an Indian company into a 100 per cent subsidiary of a foreign entity, with the founders and investors retaining the same ownership via the foreign entity, having swapped all shares.

Typically, “Flipping” happens at the early stage of the Start-ups, driven by commercial, taxation and personal preferences of founders and investors. Some companies decide to “Flip” because the major market of their product is offshore. Sometimes, investor preferences like access to incubators drive the companies to “Flip” as they insist on a particular domicile. Some companies prefer to domicile in countries where they would like to access Capital Market later for better valuations and ticket size. Better protection and enforcement of IP and tax treatment of Licensing revenue from IP, residential status of Founders, and agile corporate structures have been the reasons for “Flipping” in the Past.

In popular holding company jurisdictions like Singapore, dividends received from a Singaporean company/subsidiary are not taxed at the holding level. There are no withholding taxes when distributing dividends to residents or non-resident shareholders. This is a critical component since the dividend is one of the most popular repatriation tools. There are no withholding taxes in the United Arab Emirates (UAE) under current legislation. These jurisdictions have tailor-made their policies and tax and incentive structures to incentivise companies to store IPs and create Holding companies as Regional Headquarters. European jurisdictions, such as the Netherlands, provide for participation exemptions on dividends and capital gains (based on certain shareholding thresholds, i.e., 5 per cent and other tests). These exemptions are currently unavailable in India, and any migration of existing structures to India triggers capital gains tax. However, of late, with relatively easy access to Capital through a vibrant Private Equity/Venture Capital Ecosystem, changes in rules regarding round-tripping, and the growing maturity of India’s capital markets have not only slowed down the Flipping, but companies are also exploring “Reverse Flipping”.

To accelerate ‘Reverse Flipping’, certain measures are possible, some of which are listed below:

i. Simplifying the process for grant of “Inter-Ministerial Board (IMB) certification” for Start-ups

ii. Further simplification of taxation of Employee Stock Options (ESOPs)

iii. Simplifying multiple layers of tax and uncertainty due to tax litigation

iv. Simplifying procedures for capital flows: Many countries, such as US and Singapore, have easier corporate laws, with lesser restrictions on the inflow and outflow of capital and treatment of Hybrid Securities

v. Facilitating improved collaboration and partnerships with established private entities to develop best practices and state-of-the-art start-up mentorship platforms

vi. Exploring the incubation and funding landscape for start-ups in emerging fields like social innovation and impact investment.

The flipping phenomenon mentioned above reflects start-ups venturing out for short-term gains in the dynamic, uncertain geopolitical world. However, the flip can be reversed with the collective action by the Government related regulatory bodies and other stakeholders. With solution-oriented strategies, start-ups will continue to be the messengers of India’s entrepreneurial dynamism.

Structural reforms have enhanced the Ease of Doing Business

9.50 The ‘Make in India’ initiative has been striving to ensure that the business ecosystem in the nation is conducive for investors doing business in India and contributing to the growth and development of the Nation. This has been done through various reforms that have led to increased investment inflows and economic growth. The reform measures include amendments to laws and liberalisation of guidelines and regulations to reduce compliance burdens, bring down costs and enhance the ease of doing business in India. Burdensome compliances with rules and regulations have been reduced through simplification, rationalisation, decriminalisation, and digitisation. Steps to promote manufacturing and investments include reduction in corporate taxes, public procurement and Phased Manufacturing Programme.

9.51 The DPIIT’s Business Reform Action Plan (BRAP) 2020 (fifth edition), based on the implementation of reforms by States/UTs, was released on 30th June 2022. It shows that 7,496 reforms were implemented across States and UTs as part of the BRAP 2020 assessment, thereby significantly enhancing the Ease of Doing Business across the country. Reducing the Compliance Burden (RCB) on businesses and citizens is a continuous exercise to leapfrog to the next level of governance excellence and improve Ease of Living. Ministries and States/UTs have reduced more than 39,000 compliances (as on 17th January 2023). Specifically, more than 3,500 provisions related to minor technical or procedural defaults have been decriminalised by Ministries and States/UTs based on details uploaded on DPIIT’s Regulatory Compliance Portal as on 17th January 2023. Further, the NSWS was soft-launched in September 2021 to improve the ease of doing business by providing a single digital platform to investors for approvals and clearances. The portal is rapidly gaining traction amongst the investor community and, as of 10th January 2023, has about 4.3 lakh plus unique visitors. 8 1,000+ approvals have been facilitated through NSWS, and 43,000+ approvals are currently under process. The portal will progressively onboard more approvals and licenses based on user /industry feedback. This portal has integrated multiple existing clearance systems of the various Ministries/Departments of the Government of India and State Governments to enhance investor experience.

India and Industry 4.0

9.52 The advent of the fourth industrial revolution or industry 4.0 as it’s commonly referred to, has begun. The transformation integrates new technologies such as cloud computing, IoT, machine learning, and artificial intelligence (AI) into manufacturing processes, leading to efficiencies across the value chain. While the adoption of these technologies in the Indian manufacturing sector is underway, large-scale adoption is yet to happen. However, an enabling environment is rapidly developing. In recent years, India has made significant strides in internet penetration which is one of the key requisites of industry 4.0. The push towards self-reliance in semiconductor technology and production will help India erect another pillar of this revolution – hyper-efficient processing technology.

9.53 The government is cognisant of the importance of industry 4.0 in achieving the goals of Aatmanirbharta and its ambitions of becoming a key player in global value chains. A few initiatives by the government include the SAMARTH (Smart Advanced Manufacturing and Rapid Transformation Hubs) Udyog Bharat 4.0 under the Ministry of Heavy Industries and Public Enterprises, which aims to encourage technological solutions to Indian manufacturing units through awareness programmes and demonstrations. Another initiative is the establishment of the Centre for Fourth Industrial Revolution in India in 2018, which looks to develop policy frameworks for emerging technologies.

Conclusion and Outlook

9.54 Despite global headwinds, industrial production expanded during FY23, backed by sustained demand conditions. The growth in bank credit has kept pace with industrial growth, with a sequential surge evident since January 2022. Credit to MSMEs has seen a significant increase in part, assisted by the introduction of the ECLGS. Amidst heightened global uncertainty, FDI in the manufacturing sector moderated in the first half of FY23. However, inflows stayed well above the pre-pandemic levels, driven by structural reforms and measures improving the ease of doing business, making India one of the most attractive FDI destinations in the world.

9.55 On the positive side, easing input cost pressures owing to a fall in international commodity prices augurs well for company margins. Capacity utilisation in the manufacturing sector has been rising. It bodes well for new investment activity in creating additional capacity. Credit growth in the industry has also increased remarkably, suggesting that prospects for Capex investments by companies are brighter. The PLI schemes are set to unlock manufacturing capacity, boost exports, reduce import dependence and lead to job creation for both skilled and unskilled labour. On the downside, exports are slowing down and are likely to moderate along with the probable global economic slowdown. Volatile international commodity prices and supply disruptions in raw materials can weigh on industrial growth in the wake of new disruptions at the global level. The re-emergence of Covid-19 in China can trigger supply chain disruptions, as was the case during the pandemic period. On the other hand, if China returns to normalcy from Covid-19, there can be an increase in commodity demand – thus reversing the recent decline in commodity prices. Of course, the strength and duration of the recovery in commodity prices will be a function of many factors, such as the pace of China’s economic recovery and growth outlook in North America and Europe. Notwithstanding such open questions, industrial output in India should continue to grow steadily based on resilient domestic demand.

Note:

1 As per the National Credit Guarantee Trustee Company Ltd. (NCGTCL), the agency which operates the ECLGS

2 https://www.transunioncibil.com/resources/tucibil/doc/insights/reports/eclgs-insights-report.pdf

3 https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1792189

4 https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1885189

5 https://pib.gov.in/Pressreleaseshare.aspx?PRID=1660739

6 https://www.investindia.gov.in/team-india-blogs/electric-vehicle-ev-sector-india-boost-both-economy-and-environment

7 https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=1884181

8 https://pib.gov.in/Pressreleaseshare.aspx?PRID=1593424

9 Source: PIB https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1884256, https://pib.gov.in/PressReleaseIframePage.aspx-?PRID=1 884069#:~:text=PLI%20Scheme%20extends%20an%20incentive,2020