India’s services sector witnessed a swift rebound in FY22 driven by growth in the contact-intensive services sub-sector, which bore the maximum burden of the pandemic. This sub-sector completely recovered from the pre-pandemic level in Q2 of FY23, driven by the release of pent-up demand, ease of mobility restriction, and near-universal vaccination coverage. Going forward, strong momentum growth and an uptick in the High-Frequency Indicators (HFIs) for the contact-intensive services sector reflect a strong growth opportunity in the next fiscal. PMI services, indicative of service sector activity, has also witnessed a strong rebound in recent months with the retreating of the price pressures of inputs and raw materials.

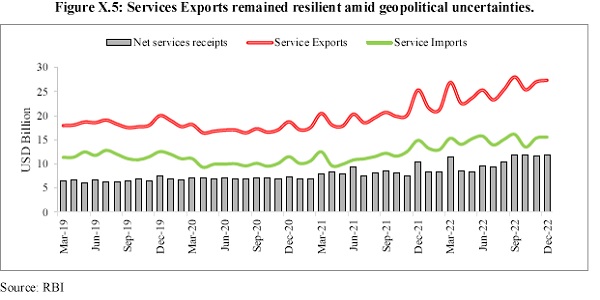

India has been a major player in services trade, being among the top ten services exporting countries in 2021, having increased its share in world commercial services exports from 3 per cent in 2015 to 4 per cent in 2021. India’s services exports have remained resilient during the Covid-19 pandemic and amid current geopolitical uncertainties, driven by higher demand for digital support, cloud services, and infrastructure modernisation catering to new challenges.

To ensure the liberalisation of investment in various industries, the Government has permitted 100 per cent foreign participation in telecommunication services including all services and infrastructure providers, through the Automatic Route. The FDI ceiling in insurance companies was also raised from 49 to 74 per cent. Measures undertaken by the Government, such as the launch of the National Single-Window system and enhancement in the FDI ceiling through the automatic route, have played a significant role in facilitating investment.

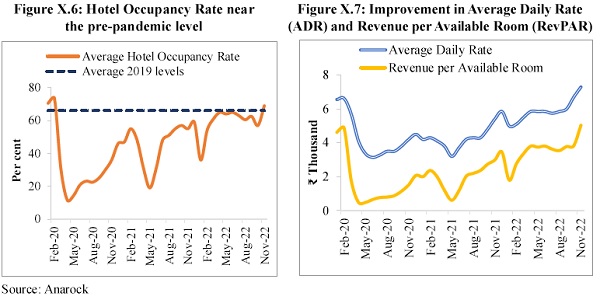

With the waning of the pandemic and external shocks on account of the Russia-Ukraine conflict, there is evidence of improvement in the performance of various services sub-sectors. The hotel industry is thriving with improvements in occupancy rate, increase in the Average Room Rate (ARR) and rise in Revenue Per Available Room (RevPAR) which are now much nearer to the pre-pandemic level of FY20. The tourism sector is also showing signs of revival, with foreign tourist arrivals in India in FY23 growing month-on-month with the resumption of scheduled international flights and the easing of Covid-19 regulations. The Real Estate sector has witnessed resilient growth in the current year, with housing sales and the launch of new houses surpassing in Q2 of FY23 the pre-pandemic level of Q2 of FY20. Information Technology-Business Process Management (IT-BPM) and the E-commerce industry have been exceptionally resilient during the Covid-19 pandemic, driven by accelerated technology adoption and digital transformation. The Government’s push to boost the digital economy, growing internet penetration, rise in smartphone adoption and increased adoption of digital payments have also given a renewed push to these industries. The introduction and piloting of Central Bank Digital Currency (CBDC) will also provide a significant boost to digital financial services. They may lay the framework for another generation of financial innovation.

Introduction

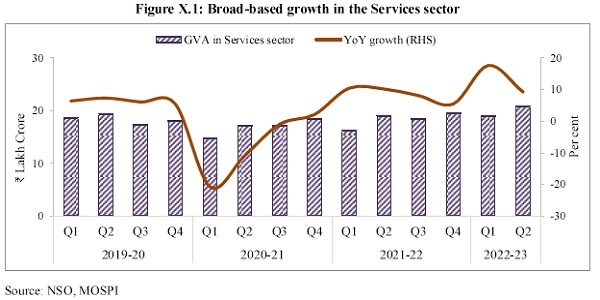

10.1 The Covid-19 pandemic hurt most sectors of the economy, with the effect particularly profound for contact-intensive services sectors like tourism, retail trade, hotel, entertainment, and recreation. On the other hand, non-contact services such as information, communication, financial, professional, and business services remained resilient. However, the services sector witnessed a swift rebound in FY22, growing Year-on-Year (YoY) at 8.4 per cent compared to a contraction of 7.8 per cent in the previous financial year. The improvement was driven by growth in the ‘Trade, Hotel, Transport, Storage, Communication and Services related to broadcasting’ sub-sector, which bore the maximum burden of the pandemic. The growth momentum has continued in FY23 as well. As per the First Advance Estimates, Gross Value Added (GVA) in the services sector is estimated to grow at 9.1 per cent in FY23, driven by 13.7 per cent growth in contact-intensive services sector.

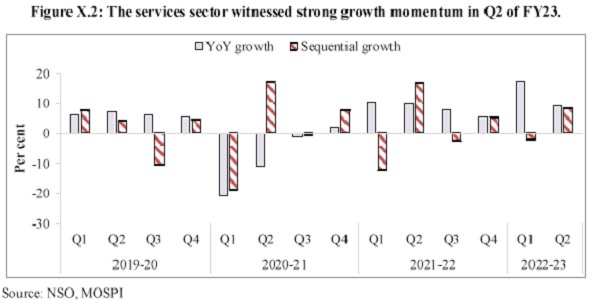

10.2 Even on a sequential basis, the rebound continued in Q2 of FY23, with the services sector recording 8.7 per cent sequential growth. The contact-intensive services sub-sector completely recovered the pre-pandemic level and registered sequential growth of 16 per cent, driven by the release of pent-up demand, ease of mobility restriction, and near-universal vaccination coverage. Going forward, the buoyant recovery of the contact-intensive services sector, accompanied by the robust performance of HFIs, suggests that the sector is likely to be the growth driver in the next fiscal.

10.3 The following sections discuss the trend in various HFIs to track the growth momentum of the services sector as a whole and also discuss the performance of various services sub-sectors.

Trends in High-Frequency Indicators

Services PMI

10.4 India’s services sector activity, gauged by PMI Services, which remained in the contractionary zone for several months during 2020 and 2021 on account of the restrictions imposed to tackle the Covid-19 pandemic, recovered swiftly with the waning of the Omicron variant at the beginning of 2022. However, PMI services again witnessed a setback with the outbreak of the Russia-Ukraine conflict. The indicator moderated from May to September 2022 as economic uncertainty resulted in weaker sales growth and inflationary pressures restricting the upturn in business activity. Further, price pressures and unfavourable weather also dampened domestic demand. However, following an overall easing of retail inflation leading to retreating price pressures of inputs and raw materials, PMI services witnessed an uptick and expanded to 58.5 in December 2022.

Bank Credit

10.5 Bank credit to the services sector has witnessed significant growth since October 2021 with the improvement in vaccination coverage and recovery in the services sector. The credit to services sector saw a YoY growth of 21.3 per cent in November 2022, the second highest in 46 months, compared to a 3.3 per cent growth in November 2021. Within the services sector, credit to wholesale and retail trade increased by 10.2 per cent and 21.9 per cent in November 2022, respectively, reflecting the strength of the underlying economic activity. Credit to NBFCs grew by 32.9 per cent as NBFCs shifted to bank borrowings because of high bond yields. Uncertain growth prospects in the global markets and uneven credit allocation to the transport sector led to a decline in credit to the shipping and aviation sector by 7.9 per cent and 8.7 per cent respectively in November 2022.

Services Trade

10.6 World services trade volume finally surpassed its pre-pandemic peak in the second quarter of 2022 and was expected to remain strong in the third quarter, buoyed by spending on travel, Information and Communication Technology (ICT) services, and financial services. However, WTO’s Services Trade Barometer Index reading fell to 98.3 for October 2022 (slightly below its baseline value of 100), well below the previous reading of 105.5 in June 2022 indicating that YoY growth in real commercial services began moderating in the third quarter of 2022 and may slow further in the fourth as well as into the first quarter of 2023 due to declining growth prospects in major service industry economies. Financial and ICT Services have been so far most resilient to the slowing global economy, whereas, construction services and container shipping fell into contraction territory.

10.7 Insofar as India is concerned, some headwinds may be observed in the coming months because of the slowing growth in some of India’s major trading partners. On the contrary, India’s services exports may improve as runaway inflation in advanced economies drives up wages and makes local sourcing expensive, opening up avenues for outsourcing to low-wage countries, including India. India is a significant player in services trade, being among the top ten services exporter countries in 2021, having increased its share in world commercial services exports from 3 per cent in 2015 to 4 per cent in 2021. A further increase in the share is likely, with the services exports registering growth of 27.7 per cent during April-December 2022 as compared to 20.4 per cent in the corresponding period last year.

10.8 Among services exports, software exports have remained relatively resilient during the Covid-19 pandemic as well as amid current geopolitical uncertainties, driven by higher demand for digital support, cloud services, and infrastructure modernisation catering to new challenges. Transport and travel exports have been the most impacted sub-components of the services exports in FY21 and FY22, which contracted due to the imposition of restrictions on international travel and tourism during the Covid-19 pandemic. If there is a meaningful economic slowdown in advanced nations, tourism and travel earnings in FY24 may be on the lower side.

Foreign Direct Investment (FDI) in Services

10.9 The World Investment Report 2022 of UNCTAD places India as the seventh largest recipient of FDI in the top 20 host countries in 2021. In FY22 India received the highest-ever FDI inflows of US$ 84.8 billion including US$ 7.1 billion FDI equity inflows in the services sector. To facilitate investment, various measures have been undertaken by the Government, such as the launch of the National Single-Window system, a one-stop solution for approvals and clearances needed by investors, entrepreneurs, and businesses. To ensure the liberalisation of investment in various industries, the Government has permitted 100 per cent foreign participation in telecommunication services, including all services and infrastructure providers, through the Automatic Route. The FDI ceiling in insurance companies was also raised from 49 to 74 per cent, under Automatic Route. Further, Government has allowed 20 per cent foreign investment in Life Insurance Corporation (LIC) under the automatic route.

Box X.1: Initiatives in the Insurance Sector by the Insurance Regulatory and Development Authority of India (IRDAI) in FY231

The Indian Insurance sector is at an inflexion point. India will be one of the main drivers of global insurance industry growth over the next decade. Indian Insurance Market is the 10th largest in the world and is poised to become the 6th largest by 2032, ahead of Germany, Canada, Italy, and South Korea2. The insurance regulator, IRDAI, has taken up the mission of universal insurance, which is expected to lead to a significant increase in insurance penetration such that, when India celebrates 100 years of its independence in 2047, every Indian has appropriate life, health, and property insurance cover and every enterprise is supported by appropriate insurance solutions. Towards this objective, the insurance regulator has taken various steps to promote healthy growth of the insurance industry, rationalise the regulatory framework, and reduce the compliance burden of regulated entities.

In line with the Government of India’s vision towards Financial Inclusion and a strong emphasis on accelerating reforms, IRDAI, during FY23, has implemented the following measures to increase accessibility, innovation, competition, distribution efficiency, and choice availability while mainstreaming technology and moving towards principle-based regime: –

i. Easy entry into the insurance sector: A Single Window NOC Portal (www.noc.irdai.gov.in) was launched to facilitate the incorporation of an insurer by making the NOC available in a hassle-free and timely manner.

ii. Quick launch of Insurance Products: Insurers can now launch all Health & General Insurance products, as well as the majority of Life Insurance products, without seeking prior approval from IRDAI, thereby reducing the time taken to launch a new product in the market from a few months to a few days.

iii. Ease of doing business: IRDAI has taken several actions to lessen the burden of compliance. In this direction, so far, 70 returns have been rationalised, and about 85 circulars have been repealed while dispensing with the prior approval requirements in certain identified areas.

iv. Providing further impetus to the industry: Given that the sector has reached a level of maturity that may not necessitate closer supervision, more flexibility to the regulated entities in the areas of operational and business decisions is being considered.

v. Addressing dynamic needs of the industry: IRDAI has facilitated various measures as per the evolving needs of the sector, such as Tech-based add-ons (General insurers have been permitted to introduce tech-enabled concepts for Motor Insurance such as Pay as You Drive, Pay How You Drive, etc.), expansion in the scope of the cashless facility in health insurance, Innovative products in Fire Insurance, Ease of living for Senior Citizen.

Major Services: Sub-Sector-Wise Performance

Tourism and Hotel Industry

10.10 The post-pandemic scenario of global tourism is gradually converging to the pre-pandemic one. With travel restrictions and health concerns subsiding, tourism has become a vital driver of a strong upswing in contact-intensive activity. As per the World Tourism Barometer of the United Nations World Tourism Organisation (November 2022), international tourism showed robust performance in January-September 2022, with international tourist arrivals reaching 63 per cent of the pre-pandemic level in the first nine months of 2022, boosted by strong pent-up demand, improved confidence levels and the lifting of restrictions. The pace of recovery would have been even stronger but for the lingering global uncertainties and higher inflation in advanced nations.

10.11 The Covid-19 pandemic affected the fortunes of the hospitality and tourism industries in recent years. The hotel industry closed the year 2020 with an average hotel occupancy rate of 3336 per cent, reflecting a decline of 32 per cent3. In the wake of falling demand and occupancies, hotels reduced tariffs significantly to attract business, thus, pulling down Revenue per Available Room (RevPAR) to a dismal low of 21,500 – 21,800, a decline of around 57-59 per cent. However, hotel occupancy began a strong recovery in the third quarter of 20214, driven by domestic leisure travel growth, partial resumption of business travel in the country, as well as wedding and social events. Small-to-medium-sized domestic MICE (Meetings, Incentives, Conference, Exhibitions) events also made a comeback, fuelling demand for hotels. The sector ended the year with an average occupancy of 42-45 per cent, up 10-13 percentage points over the previous year.

10.12 The reintroduction of travel restrictions across States at the beginning of 2022 due to the emergence of a new Covid-19 strain, Omicron, again threw the Indian hospitality sector into an upheaval. Other leisure and business travel plans were put on hold, barring critical and urgent travel as people exercised caution. The low demand resulted in an average hotel occupancy rate of 50 per cent during January-March 2022. However, due to the lower severity and hospitalisation rate of the Omicron variant, travel demand in India began its return to normalcy in March 2022. Aiding the revival of travel demand was the high vaccination rate in the country, as also effective pandemic management that ensured speed in imposing as well as the lifting of mobility restrictions closely tracking the spread and subsiding of the virus. After a two-year hiatus, India also resumed all regular international flights at full capacity as 2021-22 came to a close. Consequently, the entire aircraft movement (cargo aircraft + passenger aircraft) in the country increased by 52.9 per cent YoY between April and November 2022, reaching 93.9 per cent of the movement recorded between April and November 2019. Presently, the hotel industry is thriving with improvements in occupancy rate, an increase in Average Room Rate (ARR) and a rise in RevPAR5. The occupancy rate in November 2022 stood at around 68-70 per cent, completely recovering the average pre-pandemic level of 2019-20.

10.13 Tourism industry was another sector that was adversely impacted by the pandemic. A significant decline in Foreign Tourist Arrivals in India was witnessed in FY21. As per a study6 conducted by the Ministry of Tourism in collaboration with the National Council of Applied and Economic Research (NCAER), Tourism Direct Gross Value Added (TDGVA) witnessed a decline of 42.8 per cent in Q1, 15.5 per cent in Q2, and 1.1 per cent in Q3 of FY21 due to the overall economic slowdown in FY21. Tourism being a contact-intensive sector, employment in the sector was impacted due to the lockdown, and it was a global phenomenon. 14.5 million direct jobs in Q1, 5.2 million in Q2, and 1.8 million in Q3 are expected to have been lost compared to an estimated 34.8 million direct jobs in the tourism sector in the pre-pandemic period of FY20.

10.14 However, with the waning of the pandemic, India’s tourism sector is also showing signs of revival. Foreign tourist arrivals in India in FY23 have been growing month-on-month with the resumption of scheduled international flights and the easing of Covid-19 regulations. Yet, the arrivals are below the pre-pandemic level. Profitability ratios of the tourism industry further point towards a strong rebound in the June 2022 quarter. In addition, with the resumption of corporate travel and flexible work arrangements, the rebound in MICE tourism and bleisure7 travel is re-gaining popularity in India. With infrastructure amenities constantly improving, India is increasingly the preferred destination for MICE events.

10.15 India is ranked 10th out of the top 46 countries in the World in the Medical Tourism Index FY21 released by Medical Tourism Association. The way India has handled the Covid situation and also prepared itself for future shocks, trust in India’s medical infrastructure has improved. This will give a big push to Medical Value Tourism (MVT) which is expected to grow to US$ 13 billion by 20228. Several factors, such as the presence of world-class hospitals and skilled medical professionals, superior quality healthcare, low treatment costs compared with other countries, credibility in alternative systems of medicine, and increased global demand for wellness services like Yoga and meditation, make India a popular medical tourism destination.

10.16 India has also attempted to improve its attractiveness as a destination for specialised tourism. Recent initiatives like the Ayush visa for tourists who desire to visit India for medical treatment, the launch of the National Strategy for Sustainable Tourism & Responsible Traveller Campaign, the introduction of the Swadesh Darshan 2.0 scheme, and Heal in India can assist in capturing a larger share of the global medical tourism market. Going forward, the G20 presidency presents a unique opportunity for the Indian travel and tourism industry to take advantage of this chance to promote India as a “major tourism destination”, which is likely to positively impact passenger travel and hotel occupancy rate.

Box X.2: Making India an attractive tourist destination

The Ministry of Tourism has undertaken various measures to boost the Tourism sector, which include: –

NIDHI: The Ministry of Tourism, with the help of State Governments and Union Territory Administrations, is making efforts to register accommodation units in the country in the Ministry’s portal National Integrated Database of Hospitality Industry (NIDHI). The comprehensive national database will help in creating policies and strategies for the promotion and development of tourism at

various destinations.

SAATHI: System for Assessment, Awareness, and Training for Hospitality Industry (SAATHI) was launched in association with the Quality Council of India to restrict any further transmission of the virus while providing accommodation and other services post-lockdown. The objective of the scheme is to sensitise the industry on the Covid-19 regulations of the government and instil confidence amongst the staff and guests that the hospitality unit has exhibited intent towards ensuring safety and hygiene

at the workplace.

RCS UDAN3: Better connectivity is the critical component for flourishing tourism in any region. With this objective, the Regional Connectivity Scheme (RCS- UDAN) was launched by the Ministry of Civil Aviation to facilitate/stimulate regional air connectivity by making it affordable. The total number of Tourism RCS air routes has increased to 59, out of which 51 are presently operational. An

amount of ₹104.19 core has already been reimbursed to the Airport Authority of India in the form of Viability Gap Funding (VGF) during FY21 and FY22.

LGSCATSS: Under the Loan Guarantee Scheme for Covid Affected Tourism Service Sector (LGSCATSS) administered through the National Credit Guarantee Trustee Company (NCGTC), working capital/personal loans are provided to households that were impacted due to the Covid-19 pandemic to discharge liabilities and restart businesses. The scheme was launched to cover 10,700 Regional Level Tourist Guides (recognised by the Ministry of Tourism), Tourist Guides (recognised by the State Governments/ UT Administration), and about 1,000 Travel and Tourism Stakeholders (TTS) (recognised by the Ministry of Tourism).

To boost the tourism sector, the first 5 lakh Tourists Visa were announced by the Government for tourists of foreign nationals visiting India. The scheme was applicable until 31st March 2022 or until 5 lakh free visas were issued, whichever is earlier. The benefit was available only once per tourist.

Real Estate

10.17 The onset of the Covid-19 pandemic accentuated a slowdown in every economic space, and the real estate sector was no different. Project delays, deferment of big-ticket purchases, stagnation of property prices, and scarce funding for developers induced slackening of demand. The situation was further aggravated by the associated lockdown and migration of workforces involved in the sector to their natives. The work-from-home model had an impact on the demand for office space requirements by the corporates.

10.18 The Pandemic, however, brought about a change in individual home buyers’ sentiment in favour of owning a house. With the easing of curbs, there was an increase in interest in the residential housing sector and more so in the readily available and affordable segment. The hybrid work mode with the privileges of working from anywhere encouraged first-time home buyers to move away from the conventional metros, and this brought about a pent-up demand in the residential real estate markets of Tier II and III cities. Improvement in affordability in response to measures taken by the government during the pandemic, such as lower interest rates, reduction in circle rates, and cut in stamp duties on transaction of sale/purchase of immovable property, the extension of the Real Estate Regulation Act (RERA) also played a significant role in post-pandemic rebound of Real Estate sector.

Box X.3: Measures taken by the Government to boost the Housing sector

The various policy intervention by the government, including ‘Housing for All’, Aatmanirbhar Bharat, etc., provided an impetus to the Housing Finance sector. The permission by RBI to lending institutions to grant a total moratorium of 6 (3+3) months in case of payment failure due between 1st March 2020 to 31st August 2020, infusion of ₹75,000 crore for Non-Banking Financial Corporations (NBFCs), Housing Finance Companies (HFCs) and Micro Finance Institutions (MFIs), among others, have also contributed to the revival of the real estate sector.

The interest subvention under Pradhan Mantri Awas Yojana-Credit Linked Subsidy Scheme Urban) (PMAY-CLSS (U)) has been the demand-side driver in the residential housing space. This, along with streamlined policies to increase the credit flow, has helped in the creation of a consumer-friendly ecosystem for housing finance. Since its inception, the government has released a subsidy amounting to ₹ 53,548 crore benefitting approximately 22.87 lakh households. Further, the Affordable Housing Fund (AHF) created sufficient liquidity in the sector for viable growth. Under the Affordable Housing Fund, National Housing Bank has disbursed ₹ 34,588 crore for 3.9 lakh dwelling units since its inception. Under the Special Liquidity Facility of RBI, National Housing Bank (NHB) disbursed ₹13,917 crore and ₹8,112 crore during the 1st and 2nd waves of the pandemic, respectively, to ensure seamless business as usual in the sector. Including the above, National Housing bank has provided Liquidity support of ₹ 88,400 crore through various refinance schemes since the onset of the Pandemic.

The concessional liquidity provided the sector with the much-needed liquidity influx for keeping the sector resilient. The Co-lending model has been put forward with the aim to leverage the liquidity base of the banks and reach of HFCs to deliver formal housing credit to the bottom of the pyramid. The Smart City Project, with a plan to build 100 smart cities across India, was aimed at improving the overall opportunity for the real estate sector and encouraging investments. The overall affordability in the residential real estate sector was high during the post-pandemic period, as reflected by a decline in the weighted average annual interest rate on home loans from 8.6 per cent during January-March 2020 to 7.3 per cent during January-March 2022 for Scheduled Commercial Banks. Also, with a consistent thrust on affordable housing and a series of measures taken by the Government and the Regulators, the sector bounced back, registering a more robust growth with consistent improvement in sales as well as new launches.

10.19 The geopolitical tensions between Russia and Ukraine have again raised concerns regarding disruption in the global supply chain and its consequent impact on the real estate sector. With a volatile international market, the surge in prices of construction materials has pushed developers to halt ongoing construction. The Wholesale Price Index for Cement, Lime & Plaster has increased from 127.1 in December 2021 to 137.6 during December 2022, indicating an uptick in the input cost for construction. The Russia-Ukraine conflict has further affected the supply chain resulting in price escalations of steel, cement, finishing materials, imported chemicals, and fuel, thereby increasing the overall construction cost and resulting in a rise in housing prices.

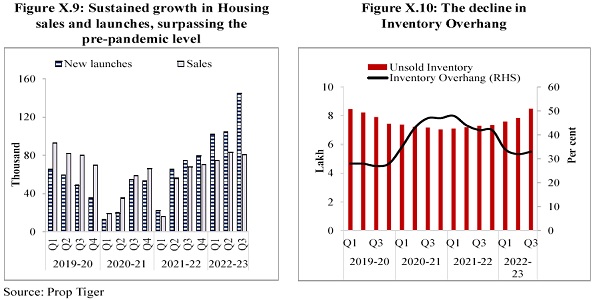

10.20 Notwithstanding the current impediments, such as rising interest rates on home loans and an increase in property prices, the sector has witnessed resilient growth in the current year, with housing sales and the launch of new houses in Q2 of FY23 surpassing the pre-pandemic level of Q2 of FY20. There is evidence of a significant decline in the inventory overhang9 dipping to 33 months during Q3 of FY23 from 42 months last year. The unsold inventory stood at 8.5 lakh at the end of 2022 with 80 per cent of the stocks under various stages of construction. This comes on the back of sustained sales momentum as the sector steadily recovers from the impact of the pandemic. Going forward, the recent government measures, such as the reduction in import duties on steel products, iron ore, and steel intermediaries, will cool off the construction cost and help to check the rise in housing prices.

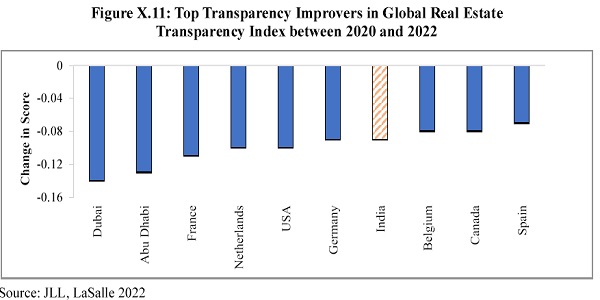

10.21 According to JLL’s 2022 Global Real Estate Transparency Index10 11, India’s real estate market transparency is among the top ten most improved markets globally, with its composite transparency score improving from 2.82 in 2020 to 2.73 in 2022, driven by increased institutional investment and the growing number of Real Estate Investment Trusts (REITs). Regulatory initiatives such as the Model Tenancy Act and digitisation of land registries & market data through the Dharani and Maha RERA platforms have helped to broaden the market and bring more formalisation to the sector.

IT-BPM Industry

10.22 Covid-19 has accelerated the pace of digital transformation across most of India’s end-user industries, with companies witnessing a rise in investment, more complex technology convergence use-cases, and the prioritisation of enterprise-scale data and cloud strategy. With rapid digitisation across the value chain, end-user industries are primed to adopt holistic and high-end enterprise performance solutions in an evolutionary journey over the near to long term.

10.23 According to NASSCOM’s report12, India’s IT-BPM industry has been exceptionally resilient during the pandemic, driven by increased technology spending, accelerated technology adoption, and digital transformation. This is evident in the swift and wide-scale remote working adoption of one of the world’s largest IT workforces. Capitalising on the learnings from the first wave, the industry’s response to the second wave has moved beyond addressing the immediate challenges to significantly enhancing capabilities to become a future-ready organisation. An obsession with customer-centricity, domain-specific solutions, a digital-first talent pool, and a laser-sharp focus on creating future-ready solutions have been the key pillars that enabled technology firms to respond proactively to emerging customer demand throughout the pandemic.

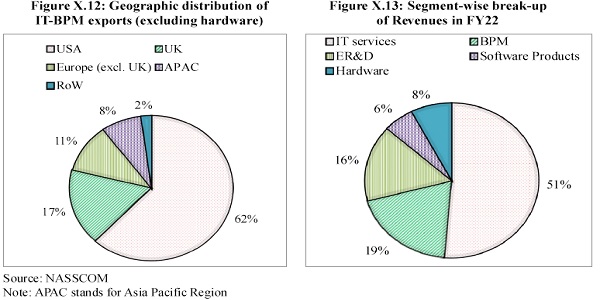

10.24 IT-BPM revenues registered YoY growth of 15.5 per cent during FY22 compared to 2.1 per cent growth in FY21, with all sub-sectors showing double-digit revenue growth. Within the IT-BPM sector, IT services constitute the majority share (greater than 51 per cent). Exports (including hardware) witnessed a growth of 17.2 per cent in FY22 compared to 1.9 per cent growth in FY21, owing to the increased reliance of businesses on technology, the roll-out of cost-reducing deals13 and the use of core operations. Growth in exports was seen across all the major markets, with the USA, Europe (excl. UK), and the UK continues to be the major markets. Many firms are now focusing on new markets, more prominently the Middle East and Latin America leading to market diversification which will increase the IT-BPM sector’s resilience in the coming years. The industry recorded nearly 10 per cent estimated growth in direct employee pool in FY22 with a highest-ever net addition to its employee base. The domestic technology industry is estimated to grow at 10 per cent on account of enterprise digital acceleration and transformation.

10.25 The industry undertook over 290 Mergers and Acquisitions in FY22, primarily focusing on digital services. India’s massive digital infrastructure played a crucial role in driving technology adoption, with public digital platforms becoming the bedrock of India’s digital advantage. However, NASSCOM’s quarterly review in August 2022 indicates that technology spending during FY23 is likely to see a relatively muted growth dampened by an expected global slowdown.

Box X.4: Major growth drivers in the IT-BPM Industry

Increasing penetration of digital tech and “Made in India digital-first solutions for the world.”

In India, the proportion of digital revenue as a percentage of total revenue has increased from around 26-28 per cent in FY20 to 30-32 per cent in FY22. In recent years, India has emerged as a global powerhouse for Engineering R&D (ER&D) and innovation and is steadfastly committed to ushering future growth and innovation for global enterprises. Many Global Competency Centres (GCCs) have been incorporated in India in the last six years. GCCs in India are increasingly performing complex R&D functions and are leveraging futuristic technologies and developing digitally innovative products as well building either the largest or the second-largest ER&D hubs in India. Patent filing has increased drastically, with over 138,000 patents filed between 2015- 21, with over 85,000 filed in emerging technologies.

Margin defence through operational excellence

Margin defence has been the critical focus amidst supply challenges as growing demand for tech talent puts pressure on margins with a limited opportunity to pass on the cost increase. Key margin levers include increased capacity utilisation, a higher share of offshore revenue, a declining share of travel and facility costs, and operating leverage.

India is a digital talent nation

India has emerged as a digital talent nation with a high share of the working population and growing undergraduate enrolments. Employment across technology companies witnessed an increase, with an uptrend in the digital talent base. New talent hiring from tier-2 cities, with a focus on reskilling non-tech talent, has led India to evolve as a significant subcontractor base, with more women getting back into the workforce.

Leading in hybrid work models

Indian tech industry led the adoption of hybrid work models

The technology used for augmenting employee experience and integrating tech solutions in aspects such as employee onboarding, communication, collaboration, and employee well-being & enablement has been the major driver. The HR functions at organisations are undergoing a transformation journey; the organisations are moving forward with an objective to deliver cost savings while expanding services and improving experiences by using a combination of labour arbitrage, optimised workforce models, elimination of low-value vendor spends, increasing talent liquidity and reducing people space cost.

E-Commerce

10.26 On the same lines as the IT-BPM sector, the E-Commerce sector also witnessed a renewed push and a sharp increase in penetration in the aftermath of the pandemic. Lockdowns and mobility restrictions disrupted consumer behaviour and gave an impetus to online shopping. The Government’s push to boost the digital economy, growing internet penetration, rise in smartphone adoption, innovation in mobile technologies, and increased adoption of digital payments further accelerated the adoption and growth of e-commerce. According to the Global Payments Report by Worldpay FIS, India’s e-commerce market is projected to post impressive gains and grow at 18 per cent annually through 2025.

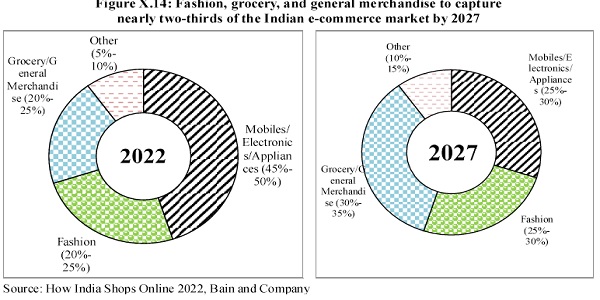

10.27 The expansion of e-commerce to newer segments like grocery, fresh-to-home fruits and vegetables, and general merchandise has contributed to the expansion of the customer base beyond traditional buyers. And as per the latest report ‘How India Shops Online 2022’ by Bain & Company, emerging categories – fashion, grocery, general merchandise – would shore up e-commerce growth in India and would capture nearly two-thirds of the Indian e-commerce market by 2027.

10.28 There has also been an increase in the adoption of digital solutions by Micro, Small and Medium Enterprises (MSMEs) like e-commerce and e-procurement, realising the prospects of increased revenues and margins, improved market reach, access to new markets, and customer acquisition. A recent study by IIFT analysing the impact of the interaction between MSMEs and e-commerce found that in recent years, MSMEs that adopted digital solutions fared far better than offline MSMEs, assisting them in accessing a large marketplace without incurring huge costs. The E-commerce platform has not only empowered small businesses by removing geographical barriers and providing a large customer base but also allowed them to deal directly with manufacturers and suppliers, thus reducing the cost of procurement. This increased access to suppliers significantly helps small business owners scale up their businesses at a much lower investment level, thus boosting their cost structure.

10.29 Further, there has been a phenomenal geographical expansion with the growth of e-commerce business in rural India driven by increased smartphone penetration, internet adoption, and increased purchasing power of rural customers. In addition, fiscal support during the pandemic helped boost e-commerce penetration in rural areas, likely by increasing consumption, which could mostly be done online in the presence of pandemic restrictions. A vast untapped rural market holds the potential for strengthening consumption growth; new E-commerce companies like Trell, Meesho, and shop 101, are expanding and gaining popularity in Tier 3 and 4 cities. The E-commerce industry is focusing on local solutions to penetrate rural areas by strengthening the network of rural distributors and retailers and using local distribution centres as Pick Up Drop Off points, enabling logistics companies to serve rural consumers.

10.30 In terms of order volume and valuation, post-Covid-19 years have been the most successful years for Indian E-commerce start-ups. As per the Retail and E-commerce Trends report released by Unicommerce and Wazir Advisors14, overall e-commerce order volume witnessed a growth of 69.4 per cent YoY in FY22, driven mainly by consumers from tier-II and tier-III cities in the last two years. The shoppers from tier-II and tier-III cities accounted for over 61.3 per cent of the overall market share in FY22, increasing from 53.8 per cent in FY21. The order volume from tier-II and tier-III cities grew at almost double the pace of tier-I cities, with 92.2 per cent and 85.2 per cent YoY growth, respectively, in FY22. In contrast, tier-I cities indicated a comparatively slower order volume growth rate of 47.2 per cent.

10.31 The Government E-Marketplace (GeM) has also witnessed tremendous growth in Gross Merchandise Value (GMV) and is catching up with E-commerce giants like Amazon and Flipkart. GeM attained an annual procurement of ₹1 lakh crore within FY22, representing a 160 per cent growth compared to last FY. GeM has taken a host of steps to onboard products of Self-Help Groups (SHGs), tribal communities, artisans, weavers, and MSMEs. 57 per cent of the total business on GeM has come through the MSME units, and female entrepreneurs have contributed over 6 percent.

10.32 Initiatives taken by the Government for the promotion of e-Commerce, including the Digital India program, Unified Payment Interface (UPI), GeM, etc., have been major contributory factors to the growth of E-commerce in recent years. Various initiatives have also been taken to provide an opportunity to small retailers, manufacturers, and Self-Help Groups for greater outreach. One District – One Product (ODOP) initiative has been facilitating the onboarding of sellers of identified products on e-Commerce platforms to provide greater visibility for small businesses from the rural sector. E-marketplace www.tribesindia.com portal through Tribal Cooperative Marketing Development Federation of India Limited (TRIFED) has been onboarding tribal artisans with their products for online sales, ensuring tribal products find a larger audience in the international market as well.

10.33 The recent initiative of the launch of Open Network for Digital Commerce (ONDC) is also playing a significant role in democratising digital payments, enabling interoperability, and bringing down transaction costs. ONDC provides better market access to sellers and helps bring the country’s remotest corners into the e-Commerce framework by empowering them with digitisation. Details on the applicability and advantages of ONDC are further discussed in Ch-12 on Physical and Digital Infrastructure: Lifting Potential Growth.

Digital Financial Services

10.34 Digital financial services enabled by emerging technologies and innovative solutions are accelerating financial inclusion, democratising access, and spurring the personalisation of products. With a strong foundation provided by the Jan Dhan-Aadhaar-Mobile (JAM) trinity, UPI, and other regulatory frameworks, the pandemic has aided acceleration in digital adoption and provided a fillip to digital financial services solutions by banks, NBFCs, insurers as well as fintech. The pandemic provided the opportunity for fintech companies to reach the underserved and provide cost-effective financial services to those at the bottom of the pyramid. While globally, the technological solutions cushioned the reverberations of the pandemic, India took the lead with the fintech adoption rate of 87 per cent, substantially higher than the world average of 64 per cent as per the latest Global FinTech Adoption Index15.

10.35 Over the last few years, the number of neobanking platforms and global investments in the neo-banking segment has also risen consistently. Neobanks operate under mainstream finance’s umbrella but empower specific services long associated with traditional institutions such as banks, payment providers, etc. Neobanks operate entirely online, with no physical presence apart from office space in the offline world. The growth of these institutions is spurred by the need for on-demand and easier-to-access financial solutions by a young and increasingly digitally savvy demographic. Neobanks have eased availability and provided access to financial services to MSMEs and underbanked customers and areas. The government also, through various initiatives, has given a push to digital banking solutions. 75 Digital Banking Units (DBU) across 75 districts announced in Union Budget 2022-23 to take banking solutions to every nook and corner of the country have been launched.

10.36 The introduction of CBDC will also significantly boost digital financial services. Issuance of CBDC in India offers several benefits, which inter alia, include reduction in operational costs involved in physical cash management, fostering financial inclusion, bringing resilience, efficiency, and innovation in the payments system, boosting innovation in cross-border payments space, and providing public with uses that any private virtual currencies can provide, without the associated risks. As of July 2022, there are 105 countries in the process of exploring CBDC, a number that covers 95 per cent of the global GDP. Many countries have already launched the CBDC, while others are in the pilot stage.

10.37 RBI has also recently launched pilots of CBDC in both the Wholesale and Retail segments. Digital Rupee –Wholesale- the pilot in the wholesale segment was launched on 1st November 2022, with the use case being limited to the settlement of secondary market transactions in government securities. Use of Digital Rupee- Wholesale is expected to make the inter-bank market more efficient. The pilot in the retail segment, known as Digital Rupee-Retail kicked off on 1st December 2022, within a closed user group comprising participating customers and merchants. For full operationalisation of CBDC, RBI is gradually expanding the pilots’ scope to include more banks, users, and locations based on feedback received during the pilots.

10.38 Digitalising documents has also played a pivotal role in giving further impetus to digital financial services. The digitisation of documents ensures safety, online verification, improved accessibility, and fraud reduction, enhancing use for end customers and the service provider.

Box X.5: Account Aggregator Framework: Transforming India’s Financial Services

Account Aggregator (AA) is a Non-Banking Financial Company (NBFC) engaged in the business of providing the service of retrieving or collecting financial information pertaining to the customer. No financial information of the customer is retrieved, shared or transferred by AA without the explicit consent of the customer. AA transfers data from one financial institution to another based on an individual’s instruction and consent. Registering with an AA is fully voluntary for consumers. Entities may enrol themselves on AA framework as Financial Information Provider (FIP) viz. banking company, non-banking financial company, asset management company, depository, depository participant, insurance company, insurance repository, pension fund etc. and as Financial Information User (FIU)

which is an entity registered with and regulated by any financial sector regulator. In this direction, RBI has issued the Master Direction viz Non-Banking Financial Company – Account Aggregator (Reserve Bank) Directions, dated September 02, 2016. At present, RBI has granted a Certificate of Registration to six companies as AA.

Achievements so far

- As on 31st December 2022, 27 Financial Institutions have gone live as FIPs, including all 12 PSBs, 10 Private Sector Banks, 1 Small Finance Bank, and 4 Life Insurance Companies.

- 119 Financial Institutions have gone live as FIUs viz; 93 RBI Regulated, 12 SEBI Regulated, 12 IRDAI-regulated entities, and 2 PFRDA-regulated entities.

- With 23 Banks onboarded to the Account Aggregator framework, more than 1.1 billion bank accounts are eligible to share data on AA. 3.3 million users have linked their accounts on the AA framework out of which 3.28 million users successfully shared data via AA. RBI has also notified Goods and Services Tax Network as FIP on 23rd November 2022 which will enable digital invoice financing and provide much-needed credit to the MSME sector.

Box X.6: Dematerialisation of documents: The next wave of digitisation

In line with the objective of the Digital India mission, which seeks to transform India into a digitally empowered nation, National e-Governance Services Limited (NeSL), an Information Utility registered with and regulated by the Insolvency and Bankruptcy Board of India under the aegis of the IBC 2016, introduced the Digital Document Execution (DDE) platform in 2020. This was done at the behest of the Insolvency and Bankruptcy Board of India and with the support of the Department of Financial Services (DFS), Ministry of Finance.

The core principle of the NeSL-DDE platform is to digitise all the steps of the document/ agreement execution journey. These include: –

- Submission of information and document/agreement to be executed on the platform

- Flexibility to accommodate any agreement/document format

- Consent-based process

- Digital payment of stamp duty and affixing of digital e-stamp certificate

- Verification of the identity of the executants and digital execution using an electronic signature

- Secure storage transmission and retrieval of the digitally executed document generated using the platform

The NeSL-DDE platform eliminates the need for the physical presence of the executants and the manual process to be carried out for executing documents/agreements. By doing so, the platform generates several benefits, such as lower execution time and cost, a secure system, authorised access, bulk processing, fraud prevention, legal robustness, and evidentiary value. A significant enabler in the journey of digitisation of documents/agreements in the financial sector is the use of the Aadhaar e-Sign, which has made electronic signatures widely available to citizens at a nominal cost.

The NeSL-DDE platform has garnered the support of state governments, ministries, and financial institutions. DFS has been encouraging banks to consider adopting DDE for their agreements. Currently, 23 States and Union Territories are available for digital e-stamping on the NeSL DDE platform. 27 banks and NBFCs are using the platform for executing their agreements, and so far, more than 9 lakh transactions have been undertaken. This includes small-ticket consumer lending transactions to large-value corporate lending transactions.

One use case of the NeSL-DDE platform is the electronic bank guarantee (e-BG), which takes away all the issues and challenges associated with the issuance, transfer, and management of physical bank guarantees and brings inefficiencies of time and cost savings. As the adoption of e-BG picks up, the NeSL platform can also function as a central repository of bank guarantees. Recently, the Department of Expenditure has amended the General Financial Rules, 2017, to permit the acceptance of e-BG in the government procurement process.

While the initial use case of NeSL-DDE is financial documents/agreements, the platform shall also enable the digital execution of other documents/agreements. This secure, paperless, hassle-free contracting offered by NeSL-DDE will have significant implications on the ease of doing business in the nation.

Outlook

10.39 India’s services sector growth which was highly volatile and fragile during the last 2 fiscal years, has shown resilience in FY23 driven by the release of pent-up demand, ease of mobility restriction, near-universal vaccination coverage and pre-emptive government interventions. Broad-based recovery has been observed in recent months, with pick up in almost all sub-sectors especially contact intensive services sector, which bore the maximum brunt of the pandemic. This is reflective of an uptick in the performance of various HFIs, reflecting a solid upswing in recent months, hinting at an enhanced presentation of the services sector in the next fiscal. The prospects look bright with improved performance of various sub-sectors like Tourism, Hotel, Real estate, IT-BPM, E-commerce etc. The downside risk, however, lies in the external exogenous factors and bleak economic outlook in Advanced Economies impacting growth prospects of the services sector through trade and other linkages.

Note:

1Until October 2022

2Sigma Report (No 4/2022) by Swiss Re (Page no 15)

3https://api.anarock.com/uploads/research/HVS%20ANAROCK%20Indian%20Hospitality%20Overview%202020.pdf

4https://api.anarock.com/uploads/research/HVS%20ANAROCK%20India%20Hotel%20Industry%20Overview%202021%20E-book.pdf

5https://api.anarock.com/uploads/research/HVS%20ANAROCK_H2O_DEC%2022.pdf

6https://tourism.gov.in/sites/default/files/2021-11/Tourism-Corona%20Report_Print%20version.pdf

7Bleisure is a term used to describe travel that combines both business and leisure

8https://www.niti.gov.in/sites/default/files/2022-02/AIM-NITI-IPE-whitepaper-on-Blended-Financing.pdf

9Inventory overhang refers to the estimated time period developers are likely to take to sell off the unsold inventory, based on the current sales velocity.

10The Global Real Estate Transparency Index is based on a combination of quantitative market data and survey results across 94 countries and 156 city markets. The Index scores markets on a scale of 1 to 5 based on their performance in the following indicators-Performance measurement, Market fundamentals, Governance of Listed Vehicles, Regulatory and Legal, Transaction Process and Sustainability

11https://www.us.jll.com/content/dam/jll-com/documents/pdf/research/global/jll-global-real-estate-transparency-index-2022.pdf. A lower value represents a more transparent market, and a higher value represents that the market is opaque

12 https://nasscom.in/knowledge-center/publications/technology-sector-india-2022-strategic-review

13 Cost-reducing deals refer to business deals which result in a decline in the company’s expenses to maximise profits. It involves identifying and removing expenditures that do not provide added value while also optimizing processes to improve efficiency.

14https://retail.economictimes.indiatimes.com/files/cp/1294/cdoc-1661333692-ECOM_july_7_5in%20x%208in_Correction.pdf

15 https://assets.ey.com/content/dam/ey-sites/ey-com/en_gl/topics/banking-and-capital-markets/ey-global-fintech-adoption-index.pdf