India’s external sector gained further stability in the first half of 2019-20, witnessing improvement in Balance of Payments (BoP) position. India’s foreign reserves are comfortably placed at US$ 461.2 billion as on 10th January, 2020. The improvement in BoP was anchored by narrowing of current account deficit (CAD) from 2.1 per cent in 2018-19 to 1.5 per cent of GDP in H1 of 2019-20. The contraction of CAD has emanated from easing of crude prices. Export growth remains subdued with external demand weakened by slowdown in global investment, output and heightened trade tensions, notwithstanding resilient service exports. Increase in service imports is inevitable with increasing foreign direct investment (FDI) and ‘Make in India’. Petroleum products, precious stones, drug formulations & biologicals, gold and other precious metals continue to be top exported commodities, with fastest growth seen in drug formulations & biologicals in 2019-20 (April to November). Crude petroleum, gold, petroleum products, coal, coke & briquittes constitute top import items, with fastest growth seen in electronics in 2019-20 (April to November). India’s top five trading partners continue to be USA, China, UAE, Saudi Arabia and Hong Kong. Further improvement in BoP was contributed by easing of external financial conditions, impressive FDI, rebounding of portfolio flows and receipt of robust remittances. Net FDI inflows have continued to be buoyant in 2019-20 attracting US$ 24.4 billion in the first eight months, higher than the corresponding period of 2018-19. This reflects a global sentiment that increasingly believes in India’s growth story and reform measures being undertaken by the government. External debt as at end September, 2019 remains low at 20.1 per cent of GDP. India’s Net International Investment Position (NIIP) to GDP ratio has also improved compared to 2018-19. After witnessing significant decline since 2014-15, India’s external liabilities (debt and equity) to GDP has increased at the end of June, 2019 primarily driven by increase in FDI, portfolio flows and external commercial borrowings (ECBs).

OVERVIEW: INDIA’s BALANCE OF PAYMENTS

3.1 Almost synchronous with the acceleration in GDP growth to 7.5 per cent in 2014-19, the Balance of Payments (BoP) position of India improved from accumulated foreign reserves of US$ 304.2 billion at end of 2013-14 to US$ 412.9 billion at end of 2018-19. For an open emerging market economy like India, improvement in BoP position is critical. It ensures financing of essential imports like crude oil and other such inputs that drive the manufacturing sector which provides livelihood to crores of people in the country. For a country that has mostly remained in current account deficit, injecting into its income stream not as much earnings from abroad as permitting leakage from it through payments overseas, a continuous improvement in its BoP position is a reflection of a global sentiment that increasingly believes in India’s growth story. This belief will hold the country in good stead when it looks to access foreign savings to meet the investment requirement for a US$ 5 trillion-economy.

3.2 Despite GDP growth decelerating in 2019-20 the global sentiment has remained positive. The BoP has improved from US$ 412.9 billion of forex reserves in end March, 2019 to US$ 433.7 billion in end September, 2019 and further to US$ 461.2 billion as on 10th January, 2020. Yet the improvement has an undercurrent of vulnerability. Unlike in 2014-19 when a sharp decline in crude price combined with high FDI inflows to engineer an improvement in BoP position, the improvement in the first half of 2019-20 has emanated from a lower growth of imports following a sharp deceleration in GDP growth and some easing of crude prices besides continued acceleration in FDI inflows. The weakening of the GDP growth poses a challenge to both net FDI and net FPI inflows in improving the BoP position of the country. Should such inflows become smaller on the back of growing pessimism on India’s prospective growth, the BoP position may worsen making access to foreign savings much more difficult in times to come.

3.3 Some of the components of BoP have contributed to improving the BoP position and some have not, both in the period 2014- 19 and in 2019-20. The components that have contributed favorably will need to be further enhanced and those that have not will need to be re-energized, through an effective mix of policies. The data pertaining to 2019- 20 is provisional. The balance of payments table from 2014-19 to 2019-20 (April to September) is placed at Annexure I.

A. Current Account Deficit (CAD)

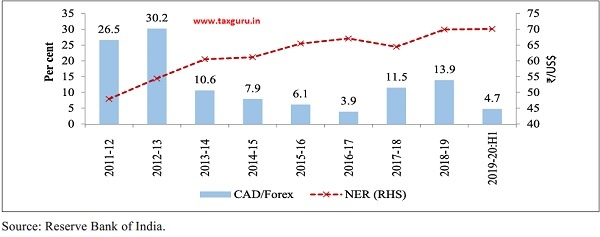

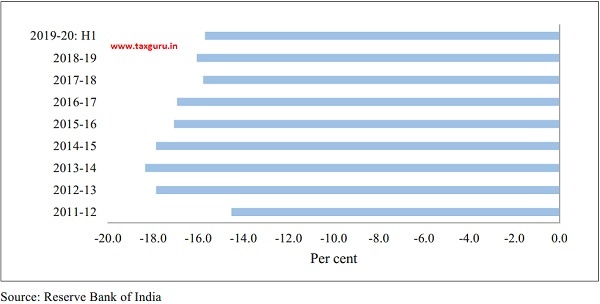

3.4 An increase in CAD as a ratio to GDP worsens the BoP by drawing down on forex reserves or building the potential to worsen it by increasing the external debt burden. Yet that has not been the case with CAD to GDP ratio significantly improving from 2009-14 to 2014-19 (Table 1). The improvement has continued going forward with the CAD to GDP ratio lower in the first half of 2019-20 as compared to 2018-19 (Figure 1).

Figure 1: Current Account Deficit (CAD) as per cent of GDP

Table 1: Current account deficit (CAD) as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| -3.3 | -1.4 | -2.1 | -1.5 |

Source: Reserve Bank of India.

3.5 The backup to CAD is the forex reserves with increase in CAD/forex ratio reflecting the decreasing strength of the backup. The decreasing strength spills into depreciating the currency. The ratio increased from 10.6 per cent in 2013-14 to 13.9 per cent in 2018-19 and depreciated the rupee from ` 60.50:1 US$ to ` 69.92:1 US$ between the two points in time (Figure 2). As the Nominal Exchange Rate (NER) has more or less stayed stable in 2019-20 it appears that the strength of the backup has not changed. Ceteris paribus, depreciation in NER makes imports costlier besides disincentivising foreign portfolio investors, which increases the pressure on BoP to worsen.

A.1 Merchandise Trade Deficit

3.6 Merchandise trade deficit is the largest component of India’s current account deficit

Figure 2: Movements in CAD/Forex and NER

significantly impacting the BoP position. Over the recent years, the escalation of global trade tensions leading to slowdown in world trade has increased the fragility of India’s trade deficit with the potential of worsening the BoP. In sync with an estimated 2.9 per cent growth in global output in 2019, growth in global trade is estimated to grow at 1.0 per cent after having peaked in 2017 at 5.7 per cent. The slowdown of world trade reflects a confluence of factors, including a slowdown in investment, reduced spending on heavily traded capital goods and a sizable decline in trade in cars and car parts. Global trade growth is however projected to recover to 2.9 per cent in 2020 with recovery in global economic activity. However, there is heightened uncertainty regarding the future structure of global value chains and the repercussions of trade tensions on technology, which may continue to weigh down the growth in world trade.1

3.7 On average, India’s merchandise trade balance has improved from 2009-14 to 2014-19 (Table 2), although most ofthe improvement in the latter period was on account of more than fifty per cent decline in crude prices in 2016-17. Lately the improvement in trade balance has positively contributed to the improvement in BoP position (Figure 3).

Figure 3: Merchandise Trade Balance as per cent of GDP

Figure 4: Terms of Trade (Base Year 1999-2000)

Table 2: Merchandise Trade Balance as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| -8.6 | -6.0 | -6.8 | -6.3 |

Source: Department of Commerce & Central Statistics Office (CSO).

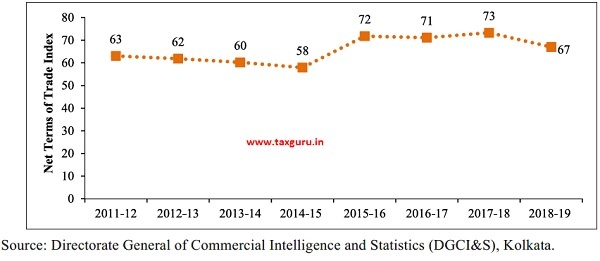

3.8 The adverse movement in Net terms of trade2 (NTT) between export and import prices may immiserize exporters but can lead to improvement in merchandise trade deficit as costlier imports lead to smaller purchase of quantity imports. Since 2017-18 the adverse movement has started which has contributed to the improvement in trade balance in the BoP (Figure 4).

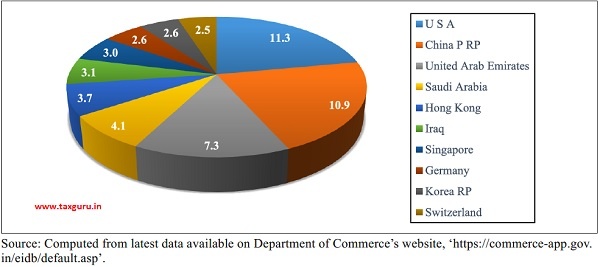

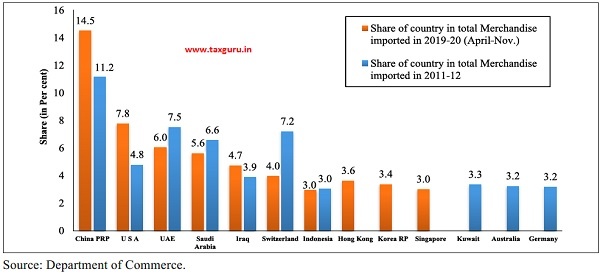

3.9 India’s top 10 trading partners during 2019-20 (April-November) jointly account for more than 50 per cent3 of India’s total merchandise trade (Figure 5).

3.10 The bilateral trade position with respect to top trading partners over a period of time

Figure 5: Top 10 Trading Partners of India in 2019-20 (April-November)(in Per cent)

is shown in Table 3. With two top trading countries i.e. USA and United Arab Emirates, India has consistently run trade surplus since 2014-15. On the other hand, India has trade deficit continuously since 2014-15 with respect to other major trading partners i.e. China PRP, Saudi Arabia, Iraq, Germany, Korea RP, Indonesia and Switzerland. India had trade surplus with Hong Kong and Singapore till 2017-18, before it changed to trade deficit in 2018-19. The bilateral imbalances have remained stable in most cases.

Table 3: Bilateral Trade Surplus/Deficit (Sorted on Year: 2018-19)

(Values in US$ Billion)

| Country | 2014-15 | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 (April- November) | |

| Trade Surplus Countries | U S A | 20.63 | 18.55 | 19.90 | 21.27 | 16.86 | 10.91 |

| United Arab Emirates | 6.89 | 10.87 | 9.67 | 6.41 | 0.34 | 0.25 | |

| Trade Deficit Countries | China PRP | -48.48 | -52.70 | -51.11 | -63.05 | -53.57 | -35.32

|

| Saudi Arabia | -16.95 | -13.94 | -14.86 | -16.66 | -22.92 | -14.32 | |

| Iraq | -13.42 | -9.83 | -10.60 | -16.15 | -20.58 | -13.98 | |

| Germany | -5.25 | -5.00 | -4.40 | -4.61 | -6.26 | -3.09 | |

| Korea RP | -8.93 | -9.52 | -8.34 | -11.90 | -12.05 | -7.80 | |

| Indonesia | -10.96 | -10.31 | -9.94 | -12.48 | -10.57 | -6.99 | |

| Switzerland | -21.06 | -18.32 | -16.27 | -17.84 | -16.90 | -11.97 | |

| Hong Kong | 8.03 | 6.04 | 5.84 | 4.01 | -4.99 | -3.88 | |

| Singapore | 2.68 | 0.41 | 2.48 | 2.74 | -4.71 | -3.15 |

Source: Computed from latest data available on Department of Commerce’s website, ‘https://commerce-app.gov. in/eidb/default.asp’.

A.1.1 Merchandise Exports

3.11 An increase in merchandise exports to GDP ratio has a net positive impact on BOP position. Over the years the merchandise exports to GDP ratio has been declining, entailing a negative impact on the BoP position (Table 4 and Figure 6).

Table 4: Merchandise Exports as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 15.7 | 12.7 | 12.1 | 11.3 |

Source: Department of Commerce & Central Statistics Office (CSO).

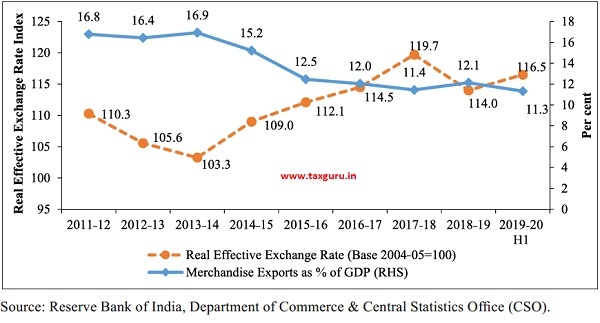

3.12 The slowdown of world output has definitely had an impact on reducing the export to GDP ratio, particularly from 2018-19 to H1 of 2019-20. The appreciation in the real exchange rate (Table 5 and Figure 6) has also contributed to the declining exports to GDP ratio.

Table 5: Real Effective Exchange Rate (Base 2004-05=100)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 107.1 | 113.9 | 114.0 | 116.5 |

Source: Reserve Bank of India

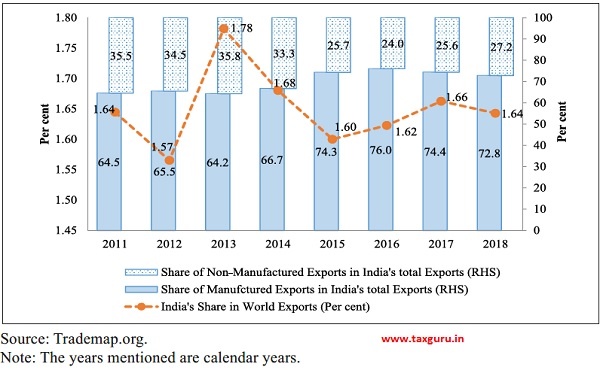

3.13 The impact on India’s exports of a slowdown in world output and appreciation of India’s real exchange rate has been an outcome of increasing integration of India’s exports with global value chain. The integration with the global value chain has increased following a relatively higher growth in manufacturing exports. In view of government’s growing emphasis on “Make in India” programme, increase in the share of manufacturing exports in total exports is inevitable (Table 6 and Figure 7).

Table 6: India’s Manufactured exports share in Total merchandise exports

| 2009-13 | 2014-18 | 2017 | 2018 |

| 66.5 | 72.8 | 74.4 | 72.8 |

Source: Trademap.org.

Note: The years mentioned are calendar years.

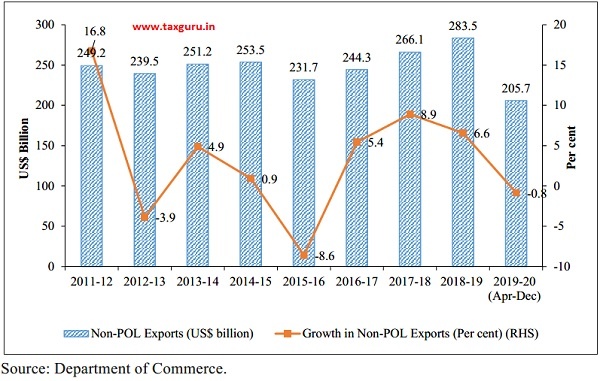

3.14 Petroleum, Oil and Lubricants (POL) exports have a dominant share in India’s export basket. However, since petroleum exports are a value-added pass through of petroleum imports, exports net of POL

Figure 6: Movement in 36 Currency REER (Base 2004-05) & Merchandise Exports as per cent of GDP

Figure 7: India’s share in World Exports, Share of Manufactured &Non-Manufactured Items in India’s Total Merchandise Exports

exports reflects how broad-based India’s exports are in generating value addition in the country. Growth in Non-POL exports dropped significantly from 2009-14 to 2014-19 (Table 7 and Figure 8). This is a challenge that needs to be addressed in times to come.

Table 7: Growth of Non-POL Exports

| 2009-14 | 2014-19 | 2018-19 | 2019-20 (Apr-Dec) |

| 11.0 | 2.6 | 6.6 | -0.8 |

Source: Department of Commerce.

Figure 8: Non-POL Exports and its Growth rate

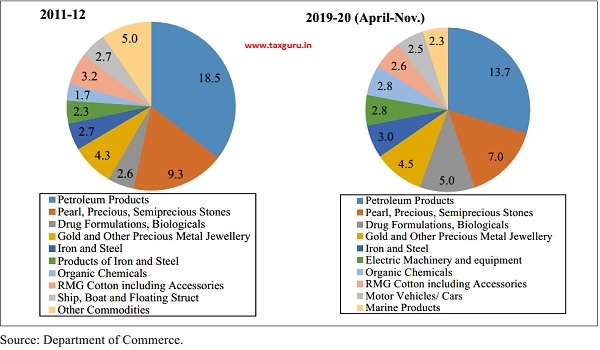

Figure 9: Commodity-wise Composition of Exports (By Share in Per cent)

3.15 In 2019-20 (April-November), petroleum products continued to be the largest exported commodity, in value terms. In terms of growth, it was drug formulations, biologicals which grew the highest between 2011-12 and 2019-20 (April-November) (Figure 9).

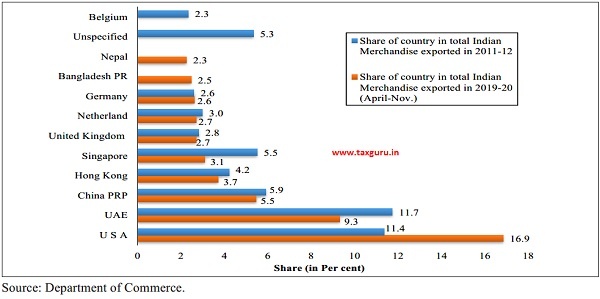

3.16 India’s largest export destination country continues to be the United States of America (USA) in 2019-20 (April-November), followed by United Arab Emirates (UAE), China and Hong Kong. Between 2011-12 and 2019-20, India’s exports to USA grew the highest (Figure 10).

Figure 10: Top 10 Export Destinations in 2011-12 and 2019-20 (April-November)

Figure 11: India’s Merchandise Imports as percent of GDP

A.1.2 Merchandise Imports

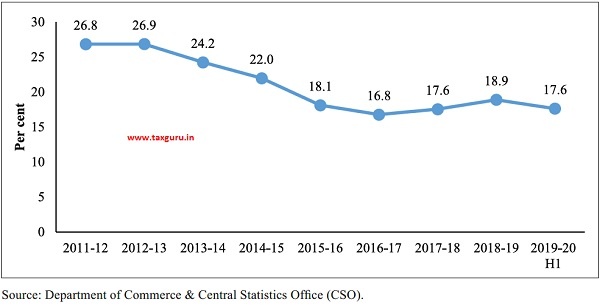

3.17 An increase in the merchandise imports to GDP ratio has a net negative impact on the BoP position. Over the years the ratio has been declining for India entailing a net positive impact on the BoP position (Table 8 and Figure 11).

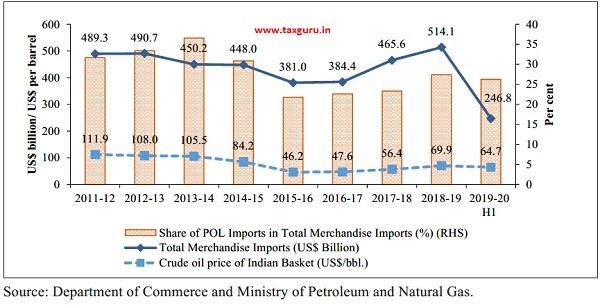

3.18 Crude oil imports have a large presence in the import basket that correlates India’s total imports with crude prices. Evidence also bears this out. As crude price rises so does the share of crude in total imports that increases imports to GDP ratio (Table 9 and Figure 12).

Table 8: India’s Merchandise Imports as percent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20-H1 |

| 24.3 | 18.7 | 18.9 | 17.6 |

Source: Department of Commerce & Central Statistics Office (CSO).

Table 9: Share of POL Import in Total Imports and Crude Oil Price (Indian Basket)

| Item | 2009-14 | 2014-19 | 2018-19 | 2019-20-H1 |

| Share of POL imports in total imports (per cent) | 32.1 | 25.2 | 27.4 | 26.3 |

| Crude oil price of Indian Basket (US$/bbl.) | 96.0 | 60.8 | 69.9 | 64.7 |

| Merchandise Imports as percent of GDP | 24.3 | 18.7 | 18.9 | 17.6 |

Source: Department of Commerce and Ministry of Petroleum and Natural Gas.

Figure 12: India’s Imports, Share of POL import in Total Imports and Crude Oil Price

Figure 13: India’s Gold Import Value and share vis-à-vis Gold Price

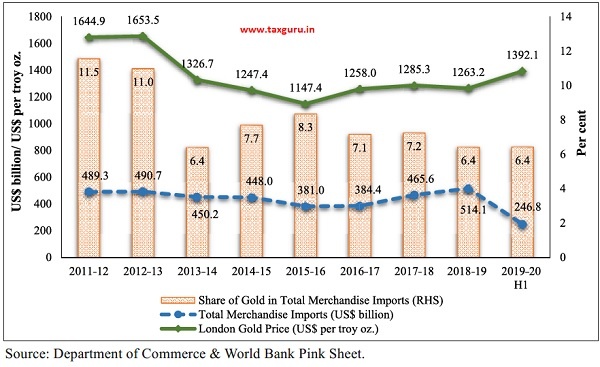

3.19 Gold imports also have a significant presence in the import basket that correlates India’s total imports with gold prices. While broadly that has been true for the two five-year periods, 2009-14 and 2014-19, the share remained the same between 2018-19 and the first half of 2019-20, despite an increase in gold prices, possibly due to increase in import duty that reduced the import of gold (Table 10 and Figure 13).

3.20 Although a fall in merchandise imports to GDP ratio entails a net positive impact on the BoP position, it may be a reflection of a deceleration in GDP growth. Non-pol-non-gold imports are understood to be positively correlated with GDP growth. However, non-pol-non-oil imports fell as a proportion to GDP from 2009-14 to 2014-19 when GDP growth accelerated between the two periods

Table 10: Share of Gold Imports in Total Imports and London Gold Price

| Item | 2009-14 | 2014-19 | 2018-19 | 2019-20-H1 |

| Share of gold imports in total imports ( per cent) | 10.0 | 7.4 | 6.4 | 6.4 |

| London Gold Price (US$ per troy oz.) | 1388.3 | 1240.3 | 1263.2 | 1392.1 |

| Merchandise Imports as percent of GDP ( per cent) | 24.3 | 18.7

|

18.9 | 17.6 |

Source: Department of Commerce & World Bank Pink Sheet.

Table 11: Non-POL, Non- Gold Imports and Growth in Real GDP

| Item | 2009-14 | 2014-19 | 2018-19 | 2019-20-H1 |

| Non-POL, Non- gold imports as percent of GDP (per cent) | 14.0 | 12.5 | 12.5 | 10.3 |

| Growth in Real GDP ( per cent) | 6.7 | 7.5 | 6.8 | 4.8 |

Source: Department of Commerce & Central Statistics Office (CSO).

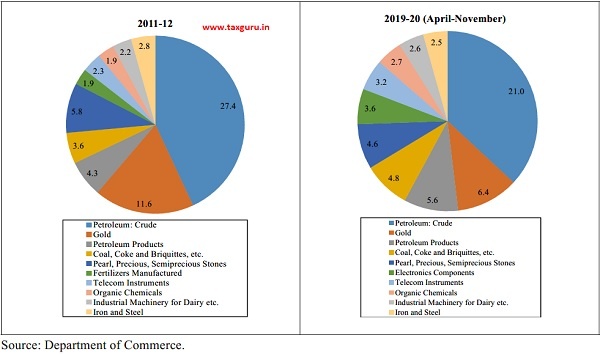

(Table 11). This may have happened because of consumption driven growth while the investment rate declined lowering non-pol-non-gold imports. Continuous decline in investment rate decelerated GDP growth, weakened consumption, dampened the investment outlook, which further reduced GDP growth and along with it non-pol-non-gold imports as a proportion of GDP from 2018-19 to H1 of 2019-20 (Figure 14). 3.21 In the import basket of 2019-20 (April- November), crude petroleum had the largest share followed by gold and petroleum products. However, between 2011-12 and 2019-20, imports of Electronics grew the fastest from a negligible share to 3.6 per cent (Figure 15).

Figure 14: Non-POL, Non-Gold Imports as per cent of GDP and Growth in Real GDP

Figure 15: Commodity-wise Composition of Imports in (By Share in Per cent)

Figure 16: Top 10 Import Origins of India in 2011-12 and 2019-20 (April-November) (By Share in Per cent)

3.22 China continues to be the largest exporter to India followed by USA, UAE and Saudi Arabia. In recent times, Hong Kong, Korea and Singapore have also emerged as significant exporters to India (Figure 16).

3.23 In the presence of high custom duties, the impact of acceleration in the growth of GDP on increasing non-pol-non-gold imports is somewhat muted, which limits the worsening impact on BoP. On the other hand, when GDP growth decelerates, high tariffs amplify the impact on lowering non-pol-non-gold imports thereby making a more than proportionate improvement in BoP. In this regard, India has also benefitted with tariff levels steeper than that in other countries (Figure 17).

Figure 17: Trade Weighted Average Import Tariff (Total) during 2017

A.2 Net Services

3.24 Net services as a proportion of GDP reflects the net impact of service exports and imports on BoP. India’s net services surplus has been steadily declining in relation to GDP (Table 12 and Figure 18).

Table 12: Net services as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 3.3 | 3.2 | 3.1 | 2.9 |

Source: Reserve Bank of India.

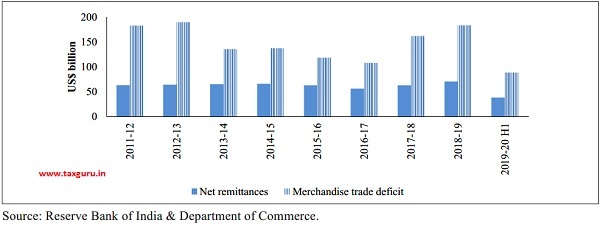

3.25 The surplus on net services has been significantly financing the merchandise trade deficit. The financing reached its peak to about two-thirds of merchandise deficit in 2016-17 before declining to less than half in the last couple of years (Figure 19). Given a steady decline in net services to GDP ratio, the extent of financing will steadily fall unless merchandise trade deficit improves in relation to GDP.

A.2.1 Service Exports

3.26 An increase in service exports to GDP ratio has a net positive impact on the

Figure 18: Net services as per cent of GDP

Figure 19: Net services and trade deficit

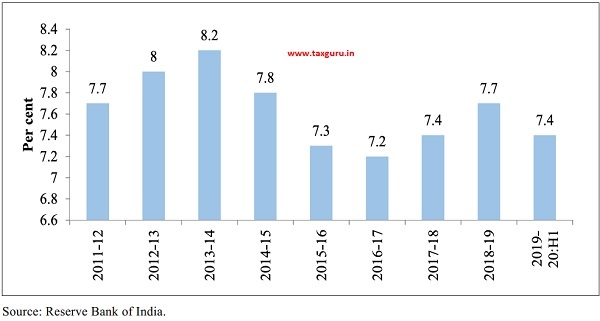

BoP position. India’s service exports have however consistently hovered between 7.4 to 7.7 per cent of GDP reflecting the steadiness of this source in contributing to the stability of BoP (Table 13 and Figure 20).

Table 13: Service Exports as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 7.7 | 7.5 | 7.7 | 7.4 |

Source: Reserve Bank of India.

Figure 20: Service exports as per cent of GDP

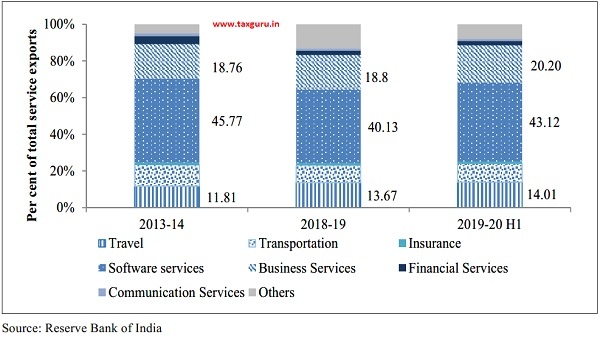

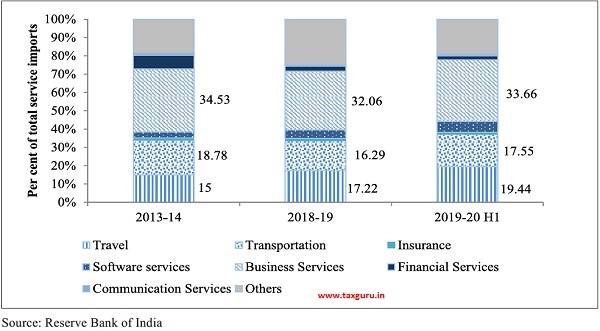

3.27 The composition of service exports has remained largely unchanged over the years. Software services constitute the bulk of it at around 40-45 per cent, followed by business services at about 18-20 per cent, travel at 11-14 per cent and transportation at 9-11 per cent (Figure 21).

Figure 21: Composition of service exports

A.2.2 Service Imports

3.28 An increase in service imports to GDP ratio has a net negative impact on the BoP position. Over the years, service imports in relation to GDP has been steadily rising putting pressure on BoP to worsen (Table 14 and Figure 22). However, increase in service imports to GDP ratio is inevitable given a rising level of FDI and a gradual upscaling of the Make in India program.

Table 14: Service Imports as per cent of GDP

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 4.4 | 4.3 | 4.6 | 4.6 |

Source: Reserve Bank of India.

Figure 22: Service imports as per cent of GDP

Figure 23: Composition of service imports

3.29 The relative shares of the various constituents of service imports have also not varied much with business services constituting about a third of service imports, which is in consonance with the rising level of economic activity in the country. The component of travel services has however been steadily increasing reflecting the growing attractiveness of global destinations to the domestic tourists in the country (Figure 23).

A.3 Policy Environment

A.3.1 India and WTO

3.30 India hosted a WTO Ministerial Meeting of Trade Ministers on 13-14 May 2019 in New Delhi wherein sixteen developing and six least developed countries along with the DG, WTO participated to deliberate on matters of concern to the member countries. The meeting culminated in an outcome document, which lays out priorities for developing countries in various areas and envisages addressing the challenges being faced by the Dispute Settlement system of the WTO.

3.31 India has also been working collectively with other developing countries and has submitted a paper in the General Council meeting of the WTO spelling out the priorities that are required to be taken into consideration while undertaking reforms in the WTO. The submission calls for preservation of core principles of the Multilateral Trading System, safeguarding special and differential treatment provisions, resolution of the Appellate Body crisis, addressing unilateral actions and continuation of negotiations in mandated areas, among others. In particular, India has emphasized that special and differential treatment provisions are essential for better integration of the developing countries in the global trading system. These provisions are at the core of the WTO and must be preserved.

3.32 In addition, a submission on transparency and notification requirements at the WTO has also been made by India along with other WTO members including Cuba, African group. The submission outlines

that transparency should be a common thread running in all the operations of the WTO. Developing countries including the least developed countries, who are already resource/capacity constrained should not be penalized in the name of improving transparency.

3.33 The twelfth Ministerial Conference of the WTO (MC12) is scheduled to be held in June 2020 in Nur-Sultan, Kazakhstan. Discussions for an outcome at MC12 are underway at various informal Ministerial meetings and regular meetings at the WTO. Despite wide divergences among members in the positions taken by them in different areas of negotiation, India is regularly engaging with members with a view to find solutions which addresses the issues of concern to the larger membership of the WTO.

3.34 India has, time and again, underscored the need of a permanent solution in public stockholding for food security programmes. There has, however not been constructive engagement in this area of negotiation. Besides, India is also fully engaged in the fisheries subsidies negotiations in the WTO and considers safeguarding the interests of poor, small and artisanal farmers as a priority in the negotiations.

3.35 India has bilateral trade arrangements with many major regional groupings/ countries. The list of Free Trade Agreements (FTAs) and Preferential Trade agreements (PTAs) already in force and the list of on-going trade negotiations are placed at Annexure II.

A.3.2 Trade Facilitation

3.36 India ratified the WTO Agreement on Trade Facilitation (TFA) in April 2016 and subsequently constituted a National Committee on Trade Facilitation (NCTF) to commence the implementation. In order to optimize the gains of trade facilitation, National Trade Facilitation Action Plan (NTFAP 2017-20) containing specific activities to further ease out the bottlenecks to trade was released on 20th July, 2017 with an overall vision of the Government to see India as an active facilitator of trade. Since then, the NCTF has played an important role in reducing the high cost of imports and exports so as to integrate the country’s cross-border trade with the global value chain. As a result of consistent trade facilitation efforts, India has improved its ranking from 143 in 2016 to 68 in 2019 under the indicator, “Trading across Borders”, which is monitored by World Bank in determining the overall ranking of around 190 countries in its Ease of Doing Business Report.

3.37 Sub-parameters of indicator “Trading Across Borders” namely time and cost required to comply with documentary requirement and border requirement for export and import have shown significant improvement since India ratified the WTO’s trade facilitation agreement in 2016. Further, in order to achieve cargo release time targets, India is undertaking a national level Time Release Study (TRS) for the first time in 2019 across multiple locations covering seaports, Inland Container Depots (ICDs), air cargo complex and integrated check posts. The intended objectives of national TRS are to assess impact of extant measures to reduce release time, examine extant procedures, technologies and infrastructure and administrative concerns and thereby identify manual processes and physical touchpoints, bottlenecks and inefficiencies (by stakeholders) to bring down the overall release time.

3.38 The key initiatives contributing to reduction in overall cargo release time and

Box 1: Major Schemes for Export Promotion

Merchandise Exports from India Scheme (MEIS): Introduced w.e.f. 01.04.2015, the objective of MEIS is to offset infrastructural inefficiencies and associated costs involved in exporting goods/ products which are produced/ manufactured in India. The scheme incentivizes exporters in terms of Duty Credit Scrips at the rate 2, 3, 4, 5, 7 per cent of Free On Board (FOB) value of exports realized. These scrips are transferable and can be used to pay certain Central Duties/ taxes including customs duties. The scheme covers exports of more than 8000 tariff lines. The process from application till final issuance of the MEIS scrip is digitized end to end, without any manual interface for more than 99 per cent of HS Codes on which MEIS is eligible.

Services Exports from India Scheme (SEIS): Under this scheme, rewards on Net foreign exchange earnings, to service providers of notified services who are providing service from India to the rest of the World, in the form of Duty Credit scrips are available. The scrips, just like MEIS are transferable and can be used to pay certain Central Duties/ taxes including customs duties. The service exporters are eligible for SEIS at the rate of 5 per cent and 7 per cent of the Net Foreign Exchange Earnings (NFEE) for exports made in a Financial Year.

Export Promotion Capital Goods (EPCG) Scheme: This Scheme allows exporters to import capital goods (except certain specified items under the Scheme) for pre-production, production and post-production at zero customs duty. In return, the exporters are required to fulfill the export obligation to the tune of six times the import duties, taxes and cess saved amount on capital goods, to be fulfilled in six years from date of issue of the Authorization. Capital goods imported under EPCG authorizations for physical exports are also exempt from Integrated Goods and Services Tax (IGST) and Compensation Cess, at present up to 31.03.2020.

Advance Authorization Scheme: Advance Authorization (AA) is issued to allow duty free import of inputs, which are physically incorporated in export products (making normal allowance for wastage). In addition, fuel, oil, catalyst which are consumed/ utilized in the process of production of export products are also be allowed.

Duty Free Import Authorization (DFIA): Duty Free Import Authorization (DFIA) is issued on post export basis for products for which Standard Input Output Norms (SION) have been notified. One of the objectives of the scheme is to facilitate transfer of the authorization or the inputs imported as per SION, once export is completed. Provisions of DFIA Scheme are similar to Advance Authorization Scheme.

Interest Equalization Scheme (IES): The scheme came into effect from 01.04.2015 for a period of 5 years. This scheme is being implemented by the DGFT through Reserve Bank of India (RBI) for pre and post Shipment Rupee Export Credit. Under the Scheme, interest equalization @ 3 per cent per annum has been made available to eligible exporters. W.e.f. 02.11.2018, the interest equalization rate has been increased from 3 per cent to 5 per cent for exports made by MSME sector under the ongoing Interest Equalization Scheme (IES) on Pre and post Shipment Rupee Export Credit. The merchant exporters have also been included at the interest equalization rate of 3 per cent under this scheme w.e.f. 02.01.2019.

Export Oriented Units (EOU)/Electronic Hardware Technology Park(EHTP)/Software Technology Parks (STP)/Bio-Technology Parks (BTP) Scheme: The objectives of these four schemes, i.e.; Export Oriented Units (EOU), Electronic Hardware Technology Park (EHTP), Software Technology Parks (STP) and Bio-Technology Parks (BTP) Scheme; are to promote exports, enhance foreign exchange earnings, attract investment for export production and employment generation. The units undertaking to export their entire production of goods and services (except permissible sales in DTA) may be set up under the schemes. Trading units are not covered under these schemes. Under this scheme, the EOUs etc. are permitted to import and/ or procure from DTA or bonded warehouse in DTA or from international exhibition held in India till 31.03.2020 (as provided by GST Council and notifications issued there under) without payment of customs duty as provided under First Schedule to the Customs Tariff Act, 1975 and additional duty, if any, of Customs leviable under Section 3(1), 3(3) and 3(5) and without payment of Integrated Tax and GST Compensation Cess leviable under section 3(7) and 3(9) of the said Act as per notification issued by the Department of Revenue from time to time.

Deemed Exports Scheme: Deemed Exports refers to those transactions in which the goods supplied do not leave the country and the payment for such supplies is received either in Indian rupees or in free foreign exchange. Under the scheme of deemed exports, exemption/ refund of duties on the goods manufactured and supplied to specified categories of deemed exports as given under the Foreign Trade Policy (FTP) is provided to ensure a level playing field to domestic manufacturers. The benefits under the Scheme are duty exemption, refund of terminal excise duty, refund of duties suffered by the inputs utilized in manufacture and supply of the goods to the specified categories of deemed exports. Under the GST regime, the Duty Drawback is limited to exemption/ refund of basic custom duties.

Transport and Marketing Assistance (TMA) for Specified Agriculture Products Scheme: To mitigate disadvantage of higher cost of transportation of export of specified agriculture products due to trans-shipment and to promote brand recognition for Indian agricultural products in specified overseas markets, the “Transport and Marketing Assistance” (TMA) scheme for specified agriculture products was launched in February, 2019 and is available for exports occurring from 01.03.2019 to 31.03.2020.

Trade Infrastructure for Export Scheme (TIES): The Government of India has launched a scheme namely, Trade Infrastructure for Export Scheme (TIES), from FY 2017-18 with the objective to assist Central and State Government Agencies for creation of appropriate infrastructure for growth of exports from the States. The Scheme provides financial assistance in the form of grant-in-aid to Central/State Government owned agencies for setting up or for up-gradation of export infrastructure as per the guidelines of the Scheme. Establishment of facility for the identification of origin and authenticity at Export Inspection Agency, Mumbai and Construction of office-cum-lab complex of EIA Chennai SO Visakhapatnam are two projects, approved under TIES.

Source: Department of Commerce.

consequent improvement in ranking of India under the indicator “Trading across Borders” include the following:

- Enablement of Single Window Interface for Facilitating Trade (SWIFT) on Customs Portal,

- Enablement of post clearance audit,

- Self e-sealing through RFID tag by trusted exporters,

- Requirement of only 3 mandatory documents for import/export,

- Introduction of ‘E-Sanchit’ for lodging supporting documents online,

- Tracking of imported cargo clearance time through Indian Customs Ease of Doing Business Dashboard (ICEDASH),

- 24X7 online customs clearance facility,

- Elimination of merchant overtime fees,

- Launch of Atithi mobile App for international passengers and

- Elimination of merchant overtime fees and installation of drive through scanners.

3.39 New schemes like Direct Port Delivery (DPD) for imports and Direct Port Entry (DPE) for exports are facilitating faster clearances at the ports. Up-gradation of port infrastructure, putting up new scanners at ports, development of robust risk based measures and introduction of new Port Community System at all major ports, have led to improvement in average dwell time at sea ports. New initiatives like ‘Turant’4 customs will make customs clearance faster and faceless.

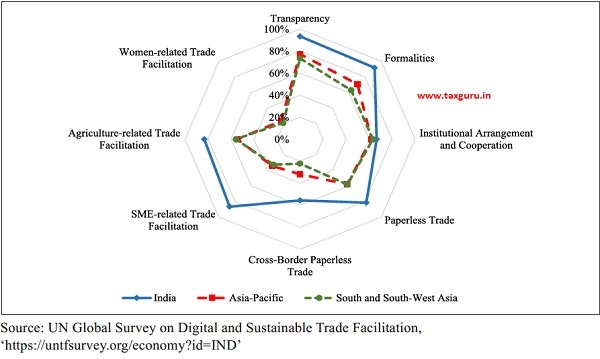

3.40 In a recently released UN global survey on digital and sustainable trade facilitation 2019, India has not only improved its overall trade facilitation score from 69 per cent to 80 per cent but also outperformed other countries in the Asia-pacific and South and South-west Asia region (Figure 24).

Figure 24: India’s performance in Digital and Sustainable Trade Facilitation, in comparison to Asia-Pacific and South and South-West Asia (2019)

Table 15: World Bank Logistics Performance Index in 2018

| Country | LPI Rank |

Customs | Infra-structure | Inter-national shipments | Logistics compe-tence | Trac king & tracing | Time liness |

| Germany | 1 | 1 | 1 | 4 | 1 | 2 | 3 |

| Sweden | 2 | 2 | 3 | 2 | 10 | 17 | 7 |

| Belgium | 3 | 14 | 14 | 1 | 2 | 9 | 1 |

| Austria | 4 | 12 | 5 | 3 | 6 | 7 | 12 |

| Japan | 5 | 3 | 2 | 14 | 4 | 10 | 10 |

| India | 44 | 40 | 52 | 44 | 42 | 38 | 52 |

Source: World Bank.

A.3.3 Trade related Logistics

3.41 Indian logistics sector is riding a growth wave and is a sunshine industry. According to estimates, Indian logistics sector is expected to grow at 8-10 per cent over the medium term. The logistics industry of India is currently estimated to be around US$ 160 billion and is expected to touch US$ 215 billion by 20205.

3.42 The Indian warehousing and logistic market received around US$ 3.4 billion of institutional capital over the last few years (January 2014 – January 2018). Investments into the warehousing sector account for around 26 per cent of the total private equity investments into real estate during this period. Many new startups are coming up in logistics eco-system with already 350 startups registered in Logistics. Agri-logistcs is also attracting attention. Solar powered micro cold stores are being developed and app based grading facilities are being created. Startups are also working on providing solution to making vehicles more fuel-efficient and environment friendly. In terms of job creation, experts predict that logistics sector can be the largest job creator by 2022. The sector currently provides employment to more than 22 million people in the country.

3.43 According to World Bank’s Logistics Performance Index, India ranks 44th in 2018 globally, up from 54th rank in 2014. The top 5 countries in the world in Logistics Performance Index (LPI) are shown in Table 15, along with India, with their rankings in LPI and each separate indicator.

3.44 To improve trade logistics, Government is building infrastructure through ambitious projects like the Bharatmala, Sagarmala and the Dedicated Freight Corridors. Inland waterways are being developed as a cost effective means of transportation. Multimodal logistic parks are being created to promote multimodal transportation. These are part of the infrastructure project pipeline worth `102 lakh crore whose details have been released by government in December, 2019. The infrastructure projects will be created over the next five years.

3.45 The Government of India is working on a National Logistics Policy and a National Logistics Action Plan. Major commodities have been identified and will be encouraged to be transported by the cheapest mode. Movement by other modes like railways, coastal, waterways and slurry pipelines are being promoted through infrastructure and policy interventions. Fast-tags have been made mandatory to cut delays at toll plazas. Qualification packs have been created to improve skilling in the sector. Apprentice programmes are being promoted through industry participation. Standards are being developed to bring in efficiency.

3.46 The government’s focus going forward is to bring down the cost of logistics which will boost the competitiveness of our manufacturing sector. Driving logistics cost down from estimated current levels of 13-14 per cent of GDP to 10 per cent in line with best-in class global standards is essential for India to become globally competitive.

A.3.4 Anti-dumping and Safeguard Measures

3.47 India conducts anti-dumping investigations on the basis of applications filed by the domestic industry with prima facie evidence of dumping of goods in the country, injury to the domestic industry and causal link between dumping and injury to the domestic industry. The countries involved in these investigations are China PR, Hong Kong, Korea, Germany, EU, USA, Malaysia, South Africa, Thailand, Brazil, among others.

3.48 During the period from 01.04.2019 to 30.11.2019, Directorate General of Trade Remedies (DGTR) initiated 25 antidumping investigations, 5 countervailing duty investigations and 6 safeguard investigations. Final findings in 14 antidumping investigations, 4 countervailing duty investigations and preliminary findings in 5 investigations were issued during this period.

3.49 In its efforts to promote transparency, efficiency and expedited relief to the domestic producers, DGTR has introduced online portal to submit online petitions for different trade remedies like anti-dumping duty, safeguard duty and countervailing duty. The portal is named ARTIS (Application for Remedies in Trade for Indian industry and other Stakeholders). Applicants can monitor the current status of their applications through online portal.

3.50 Outreach programmes to sensitize various stakeholders about the available Trade Remedy Measures are being conducted by officers of DGTR from time to time. In addition, seminar and interactive sessions on Trade Remedy Mechanism for delegations from GCC and Zimbabwe have been held. A Help Desk & Facilitation Centre has been established to facilitate optimal utilization by different stakeholders of available trade remedial measures aimed at curbing ‘unfair trade’.

A.4 Net Remittances

3.51 An increase in net remittances improves the BoP position. Net remittances from Indians employed overseas has been constantly increasing year after year and has continued doing so with the amount received in the first half of 2019-20 being more than 50 per cent of the total receivables in 2018-19 (Table 16). The pro-cyclicality of India’s remittances with respect to crude oil price movements has been established empirically by various studies including the Economic Survey 2016-17. Apparently because of this link, remittances had fallen in 2016-17 when crude prices had significantly declined (Figure 25).

Table 16: Net Remittances (US$ billion)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 298.21 | 319.53 | 70.60 | 38.4 |

Source: Reserve Bank of India

3.52 The Migration Report 2019 released by the United Nations has placed India as the leading country of origin of international migrants in 2019 with a diaspora strength

Figure 25: Remittances and Merchandise trade deficit

Figure 26: Net FDI and CAD

of 17.5 million. Further, as per the October 2019 report of World Bank, India remained the top remittance recipient country in 2018, followed by China, Mexico, the Philippines and Egypt.

B. Foreign Direct Investment (FDI)

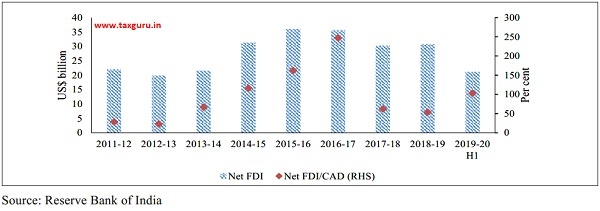

3.53 Net FDI in the first eight months of 2019-20 stood at US$ 24.4 billion. An increase in net FDI improves the BoP position. The impressive improvement in BoP position from March, 2014 to March, 2019 is mainly attributed to almost doubling of net FDI into the country from 2009-14 to 2014-19. Net FDI inflows have continued to be buoyant in 2019-20 attracting in the first half itself an amount more than 50 per cent of the previous year level (Table 17). Continuous liberalization of FDI guidelines has been responsible for rising inflows of foreign investment into the country.

Table 17: Net FDI (US$ billion)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 92.51 | 163.87 | 30.7 | 21.3 |

Source: Reserve Bank of India

3.54 An increase in net FDI also provides a more stable source of funding the CAD and in that sense provides greater stability to the improvement in BoP position as compared to other capital inflows. Net FDI’s financing of CAD in the first half of 2019-20 has been higher than the same period of 2018-19 (Figure 26).

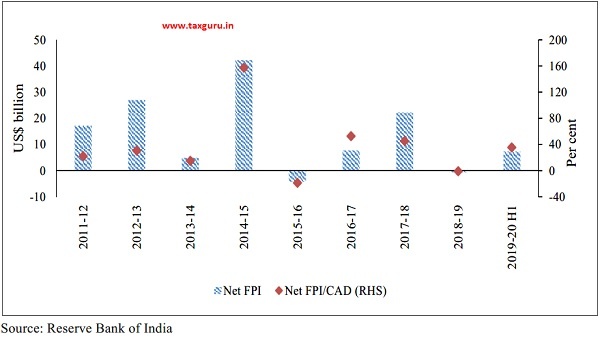

C. Foreign Portfolio Investment (FPI)

3.55 Net FPI in the first eight months of 2019-20 stood at US$ 12.6 billion. An increase in net FPI flows improves the BoP position and arises on account of cross-border transactions involving debt or equity securities, other than those included in direct investment or reserve assets. However, FPI is often referred to as “hot money” because of its tendency to flee at the first signs of trouble in an economy or improvement in investment attractiveness elsewhere in the world, particularly in the US at the hands of the Federal Reserve. In relation to net FDI, dependence on net FPI to finance the CAD was less in 2014-19 at 17.1 per cent as compared to 45.6 per cent in 200914 (Figure 27). In 2018-19, there was a net portfolio outflow from the country that was seen as weakening of confidence of investors in India’s economy. However, portfolio flows in H1 of 2019-20 have turned positive which could be attributed to the dovish monetary policy stance of the US, enhanced liquidity in global markets and reinforced growth prospects for India post budget announcements and reform measures (Table 18).

Table 18: Net FPI (US$ billion)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 59.1 | 67.18 | -0.62 | 7.3 |

Source: Reserve Bank of India

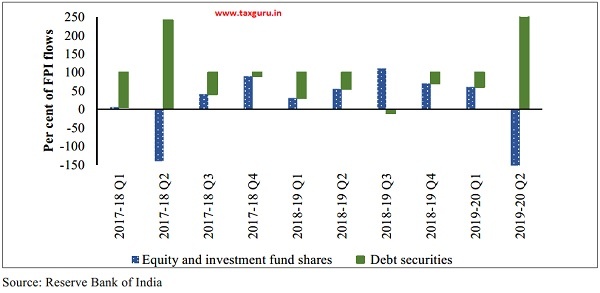

3.56 The debt-equity composition of net FPI matters in terms of impacting servicing of external debt. A lower debt component reduces the debt servicing burden and improves the BoP position. In recent quarters until Q1 of 2019-20, a change in the composition of FPI flows towards more non debt creating equity and investment funds is discernible (Figure 28). However, on the flip side increase in investment in debt instruments is important to deepen the debt market in the country.

Figure 27: Net FPI and CAD

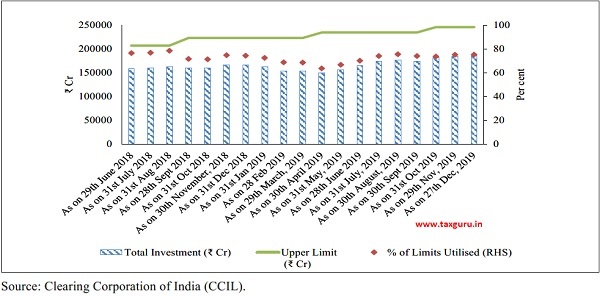

3.57 A report on assessment of India’s BoP in 2018-19 published by RBI in November, 2019 stated that the highest FPI outflow in the debt segment took place from the sovereign sector (i.e., G-Secs). In this regard the recent policy initiatives of enhancing investment limits of FPIs in government securities and easing of minimum residual maturity are

Figure 28: Composition of FPI flows

Figure 29: FPI in government securities.

likely to boost FPI flows. In April, 2018, RBI revised the limit for FPI investment in central government securities (G-secs) wherein the limit would be increased by 0.5 per cent each year to 5.5 per cent of outstanding stock of securities in 2018-19 and 6 per cent of outstanding stock of securities in 2019-20. Based on latest data available, the utilization rate of FPI limits in G-secs increased from 68.6 per cent in March 2019 to 75.6 per cent in December, 2019 (Figure 29).

D. External Commercial Borrowings (ECBs)

3.58 An increase in net ECBs improves the BoP position but it worsened the BoP by turning negative during 2014-19, from a healthy positive level in 2009-14 (Table 19). In 2018-19 however there was a surge in net ECB inflows and almost a matching amount has already flowed into the country in the first half of 2019-20.

Table 19: Net ECB (US$ billion)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 42.80 | -4.24 | 9.77 | 9.76 |

Source: Reserve Bank of India

3.59 While domestic bank credit growth has remained subdued in recent years, credit through the ECB route has witnessed significant growth since 2017-18 (Figure 30). The increasing preference of corporates for the ECB route may be attributed to low global interest rates and improved liquidity overseas. In addition, a host of measures introduced recently by the government towards liberalization of ECBs, rationalisation of all-in-cost of ECBs, expansion of list of eligible borrowers, removal of sector-wise borrowing limits for all eligibleborrowers up to US$750 million and approval of oil marketing companies to raise up to US$ 10 billion for working capital, has increased the attractiveness of ECBs.

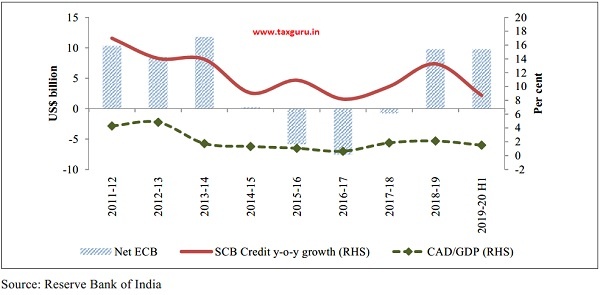

3.60 The availability of ECB avenue and an increasingly easier one at that raises a question mark on the assertion that increase in fiscal deficit crowds out private investment for want of funds. In an open economy foreign savings are always available and India has benefited from that by attracting FDI and ECBs. In this regard if fixed corporate investment rate during 2014-19 did not rise it was not because government was crowding out the corporate sector by pre-empting commercial bank credit. For had that been the reason, the corporate sector could have easily accessed ECBs as it did post 2017-18.

3.61 In an open economy framework a rising fiscal deficit gives rise to two problems. First, it increases the domestic cost of capital tempting corporates to invest their surplus in the domestic market while seeking to finance their investment through ECBs. Low interest rate abroad plus the cost of hedging turns out to be lower than the domestic cost of capital. Second, as higher fiscal deficit pushes corporates into seeking

Figure 30: ECBs, Scheduled Commercial Bank (SCB) credit (y-o-y) and CAD

larger amounts of foreign savings, the CAD widens, bringing the country closer to the twin-deficit challenge, wherein even a small loss of investor confidence can result in capital flight and sharp depreciation of the rupee. In this situation a default on the BoP becomes highly probable.

E. External Debt

3.62 An increase in external debt to GDP ratio increases debt servicing and draws down on forex reserves worsening BoP position. After a significant reduction in 2014-19 relative to 2009-14, India’s external debt to GDP ratio slightly increased by 0.3 per cent at the end of first half of 2020 over its level at end-March 2019, primarily on account of an increase in commercial borrowings, non-resident deposits and short-term trade credit (Table 20 and Figure 31). However, the increase was partially offset by valuation gains resulting from appreciation of the US dollar against Indian rupee and other major currencies in Q2 of 2019-20. India’s external debt remains low as compared to the average external debt to GDP ratio of all developing countries (25.6 per cent) according to World Bank’s International Debt Statistics, 2020.

Table 20: External Debt (Per cent of GDP)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| 23.9 | 19.7 | 19.8 | 20.1 |

Source: Reserve Bank of India, Quarterly external debt report, DEA, M/o Finance.

3.63 A rising share of short-term debt makes the BoP position more vulnerable because of relatively higher rates of interest on such borrowings. However, a contraction of short term debt is visible in the falling share of short term debt (with original maturity of up to one year) in total external debt since 2012-13 (Figure 32). At a time when exports are not growing rapidly, loans at high interest rates can create pressure on BoP in the future.

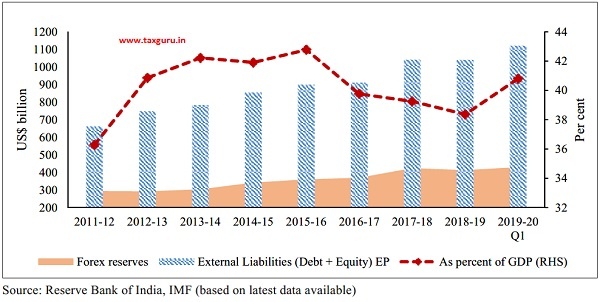

F. External liabilities (Debt + Equity)

3.64 External liabilities (Debt + Equity)/ GDP ratio is a more comprehensive measure of external liabilities as it adds dividend payout to debt servicing. A rise in this ratio draws down to a greater extent the forex reserves and worsens the BoP position. A recall of equity investment, both under FPI and FDI can increase the vulnerability of BoP position. India’s external liabilities to GDP

Figure 31: External debt/GDP and Foreign exchange reserves

Figure 32: Short term debt

ratio has witnessed significant decline during 2014-19 as against 2009-14 (Table 21 and Figure 33). The recent surge in this ratio in Q1 of 2019-20 despite modest external debt level indicates that total external liabilities are relatively skewed towards equities. This may be attributed to the rise in FDI and FPI inflows, a larger part of which is accounted for by equity. An increase in non-debt liabilities in the form of dividend pay outs on foreign investment in equity will exert strain on BoP. However, on the flip side such investment holds potential for future wealth creation and the pressure on BoP may be lifted to some extent if the dividend payouts are deployed back in the country.

Table 21: External Liabilities

(Debt + Equity)/GDP (End Period)

| 2009-14 | 2014-19 | 2018-19 | 2019-20 Q1 |

| 42.2 | 38.2 | 38.4 | 40.8 |

Source: IMF (based on latest data available)

Figure 33: External Liabilities (Debt + Equity)-End Period (EP)

G. Net International Investment Position (NIIP)

3.65 NIIP measures the gap between a nation’s stock of foreign assets and foreigner’s stock of that nation’s assets at a specific point in time. Changes in NIIP/GDP ratio nets out the impact of investment made by the country abroad from the external liabilities borne by the country thereby measuring the net changes in the debt and equity servicing burden in relation to GDP. The surge in net FDI inflows has worsened the absolute NIIP level from 2009-14 to 2014-19 (Table 22). However, in relation to GDP the burden has reduced and so has the debt and equity servicing obligations. At the end of 2019-20:H1, NIIP/GDP ratio has remained the same as at end of 2018-19 (Figur 34).

Table 22: Net IIP (End Period)

| Item | 2009-14 | 2014-19 | 2018-19 | 2019-20 H1 |

| NIIP ($US billion) | -340.8 | -436.8 | -436.8 | -436.7 |

| NIIP/GDP | -18.4 | -16.1 | -16.1 | -15.7 |

Figure 34: Net IIP/GDP

OUTLOOK

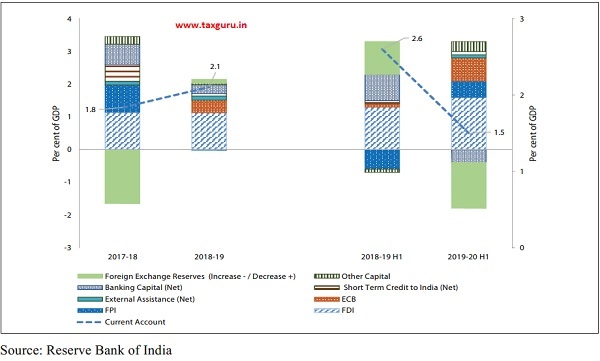

3.66 After witnessing a rise in vulnerabilities in 2018-19 leading to a modest depletion of foreign exchange reserves, India’s external sector has gained further stability in the first half of 2019-20 with improvement in BoP position anchored by capital flows bouncing back through FDI, FPI and ECBs, receipt of robust remittances and contraction of CAD to GDP ratio. External debt remains low at 20 per cent of GDP. As on 10th January, 2020, India’s foreign exchange reserves stood at US$ 461.2 billion, recording an accretion of US$ 27.5 billion from H1 of 2019-20. Summary of changes in foreign exchange reserves over the years is placed at Annexure-III. Financing of CAD in recent years is depicted in Figure 35.

Figure 35: Financing of CAD

3.67 In recent times India’s tariff regime have come under pressure from trade partners who seek a cut in the country’s basic custom duties. India has defended its tariff regime stating that it is necessary for protecting the vulnerable businesses in India. However, independent of trade partners, Government is aware that some reduction in tariff rates may have to be done in respect of intermediate inputs and raw material to correct the presently inverted duty structure. A corrected duty structure will reduce the cost of intermediate inputs imported for manufacturing of exports thereby making the country’s exports more competitive. The resulting increase in exports will strengthen India’s BoP position. Box 2 discusses that every time India’s imports of intermediate inputs have risen so have the exports of associated consumption goods with an elasticity of greater than 1. Accordingly, a reduction in basic custom duty on intermediate inputs will not only correct the inverted duty structure creating the right incentives for boosting manufacturing but will also increase the growth of exports of consumption goods that significantly use imported intermediate goods.

Box 2: IMPORT ELASTICITY OF EXPORTS

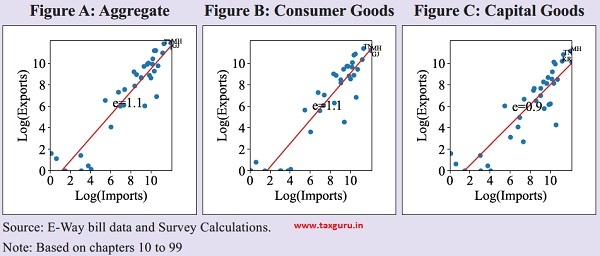

An analysis of the relation between exports of finished goods and imports of raw materials and intermediate goods for India is being undertaken. The raw/ intermediate goods are being imported for production of goods that can be consumed domestically or exported. For instance, trans-axles and its parts are imported for production of trucks; gold is imported for making jewellery; etc. This analysis is done by using data available from e-way bills during the period October, 2018 to September, 2019. The product level classification of World Integrated Trade Solution (WITS) viz., raw materials, intermediate goods, consumer goods and capital goods is used to further disaggregate this data at the 4-digit level. For illustration, in the leather sector, WITS product-level classification has been used only for chapters 41, 42 and 43 of harmonized system codes to identify raw materials/ intermediate goods and consumer/ capital goods at the 4-digit level. The E-Way bill product level data is also available at 4-digit. For sectors like automobiles and pharmaceuticals, research papers and reports have been used that have classified raw materials and final goods at 4-digit level.

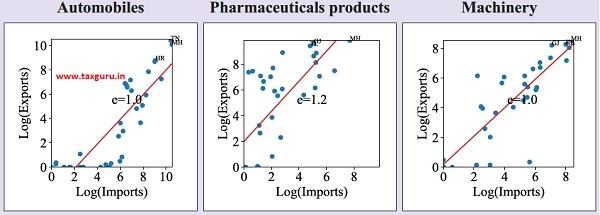

At an aggregate level, the import elasticity of exports is 1.1 (as shown in Figure A), i.e., 1 per cent increase in imports of raw materials and intermediate goods leads to 1.1 per cent increase in exports of finished goods from India. Figures B and C show the import elasticities of export of consumer goods and capital goods as 1.1 and 0.9 respectively. This implies that exports of consumer goods are more sensitive to imports of raw materials and intermediate goods, as compared to capital goods.

Import elasticity of export

Sector-wise Analysis

Sector wise analysis shows that sectors like automobiles, motorcycles, organic and inorganic chemicals, pharmaceutical products, machinery, articles of apparel, articles of leather, footwear, miscellaneous manufactured articles like toys and cushions, glassware and ceramic products, optical instruments, boilers, stainless steel and switches have import elasticity of export greater than 1. Figure D shows the import elasticities for some of the sectors.

Figure D: Sectors with import elasticity of exports greater than 1

The following table shows the raw materials/ intermediate goods used in the production of the finished good in the aforementioned sectors.

| Sector | Raw Materials/ Intermediate Goods | Final Goods |

| Automobiles | Chassis, bodies, auto parts and accessories, tubes and pipes of vulcanized rubber, safety glass | Tractors, motor vehicles, dumpers, special purpose motor vehicles, motorcycles |

| Pharmaceuticals | Antisera, vaccines, immunological products, drugs of animal origin not for retail sale | Medicines and drugs for retail sale |

| Machinery | Parts of shavers, electric transformers, primary cells, | Fans, dish-washing machines, washing machines, vacuum cleaners, ovens, filament lamps, DC motors, generators, transformers |

| Articles of apparel | Cotton, silk, yarn, wool, woven fabrics, synthetic staple fibres, jute | Sanitary towels, carpets, cloths, wall coverings, blankets, shawls, mattresses |

| Articles of leather | Skin and fur-skins of animals, animal leather | Trunks, handbags, gloves, jackets, belts |

| Footwear | Leather soles, sheep lining, umbrella frames, felt hat forms and bodies | Footwear, hats, umbrellas |

Source: World Integrated Trade Solution (WITS)

This shows that through value addition, India is exporting a processed final product after importing raw materials in these sectors. This moves India up in the value chain in these sectors. To support this further, it is necessary to facilitate ease of import of raw materials and intermediate goods in these sectors, by reducing basic custom duty on intermediate inputs. This will not only correct the inverted duty structure but would also create right incentives for boosting manufacturing, employment and growth of exports of consumer goods.

CHAPTER AT A GLANCE

> India’s Balance of Payments (BoP) position witnessed improvement from US$ 412.9 billion of forex reserves in end March, 2019 to US$ 433.7 billion in end September, 2019, anchored by narrowing of current account deficit (CAD) from 2.1 per cent in 2018-19 to 1.5 per cent of GDP in H1 of 2019-20. India’s foreign reserves stood at US$ 461.2 billion as on 10th January, 2020.

> In sync with an estimated 2.9 per cent growth in global output in 2019, global trade is estimated to grow at 1.0 per cent after having peaked in 2017 at 5.7 per cent. However, it is projected to recover to 2.9 per cent in 2020 with recovery in global economic activity.

> India’s merchandise trade balance has improved from 2009-14 to 2014-19 although most of the improvement in the latter period was on account of more than fifty per cent decline in crude prices in 2016-17.

> Petroleum products, precious stones, drug formulations & biologicals, gold and other precious metals continue to be top exported commodities. Crude petroleum, gold, petroleum products, coal, coke & briquittes constitute top import items. India’s top five trading partners continue to be USA, China, UAE, Saudi Arabia and Hong Kong.

> India’s net services surplus has been steadily declining in relation to GDP. It financed two-thirds of merchandise deficit in 2016-17 before declining to less than half in the last couple of years.

> Under trade facilitation, India has improved its ranking from 143 in 2016 to 68 in 2019 under the indicator, “Trading across Borders”, monitored by World Bank in determining the overall ranking of around 190 countries in its Ease of Doing Business Report.

> The logistics industry of India is currently estimated to be around US$ 160 billion and is expected to touch US$ 215 billion by 2020.

> Net remittances from Indians employed overseas has been constantly increasing year after year and has continued doing so with the amount received in H1 of 2019-20 being more than fifty per cent of the previous year level.

> Net FDI inflows have continued to be buoyant in 2019-20 attracting US$ 24.4 billion in the first eight months, higher than the corresponding period of 2018-19. Net FPI in the first eight months of 2019-20 stood at US$ 12.6 billion.

> External debt as at end September, 2019 remains low at 20.1 per cent of GDP. After witnessing significant decline since 2014-15, India’s external liabilities (debt and equity) to GDP has increased at the end of June, 2019 primarily driven by increase in FDI, portfolio flows and external commercial borrowings (ECBs).

Annexure I

Balance of Payments

(US$ Million)

| SI. No. | Item | 2014-15 | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2018-19 Apr- Sep | 2019-20 Apr -Sep |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| I | Current Account | |||||||

| 1 | Exports | 3,16,545 | 2,66,365 | 2,80,138 | 3,08,970 | 3,37,237 | 1,66,788 | 1,62,743 |

| 2 | Imports | 4,61,484 | 3,96,444 | 3,92,580 | 4,69,006 | 5,17,519 | 2,62,575 | 2,47,037 |

| 3 | Trade Balance (1-2) | -1,44,940 | -1,30,079 | -1,12,442 | -1,60,036 | -1,80,283 | -95,788 | -84,294 |

| 4 | Invisibles (net) | 1,18,081 | 1,07,928 | 98,026 | 1,11,319 | 1,23,026 | 60,931 | 63,673 |

| A. Services | 76,529 | 69,676 | 68,345 | 77,562 | 81,941 | 38,932 | 40,474 | |

| B. Income | -24,140 | -24,375 | -26,302 | -28,681 | -28,861 | -14,363 | -14,739 | |

| C. Transfers | 65,692 | 62,627 | 55,983 | 62,438 | 69,946 | 36,362 | 37,938 | |

| 5 | Goods and Services Balance | -68,411 | -60,402 | -44,098 | -82,474 | -98,342 | -51,240 | -43,820 |

| 6 | Current Account Balance (3+4) | -26,859 | -22,151 | -14,417 | -48,717 | -57,256 | -34,857 | -20,621 |

| II | Capital Account | |||||||

| Capital Account Balance | 89,286 | 41,128 | 36,447 | 91,390 | 54,403 | 21,391 | 39,935 | |

| i. External Assistance (net) | 1,725 | 1,505 | 2,013 | 2,944 | 3,413 | 478 | 1,913 | |

| ii. External Commer-cial Bor- rowings (net) | 1,570 | -4,529 | -6,102 | -183 | 10,416 | 877 | 9,767 | |

| iii. Short-term credit | -111 | -1,610 | 6,467 | 13,900 | 2,021 | 1,298 | 1344 | |

| iv. Banking Capital (net) of which: | 11,618 | 10,630 | -16,616 | 16,190 | 7,433 | 10,583 | -5,702 | |

| Non-Resident Deposits (net) | 14,057 | 16,052 | -12,367 | 9,676 | 10,387 | 6,838 | 5,034 | |

| v. Foreign Investment (net) of which | 73,456 | 31,891 | 43,224 | 52,401 | 30,094 | 9,040 | 28,646 | |

| A. FDI (net) | 31,251 | 36,021 | 35,612 | 30,286 | 30,712 | 16,983 | 21,327 | |

| B.Portfolio (net) | 42,205 | -4,130 | 7,612 | 22,115 | -618 | -7,943 | 7,319 | |

| vi. Other Flows (net) | 1,028 | 3,242 | 7,460 | 6,138 | 1,026 | -885 | 3967 | |

| III | Errors and Omission | -1,021 | -1,073 | -480 | 902 | -486 | 259 | -211 |

| IV | Overall Balance | 61,406 | 17,905 | 21,550 | 43,574 | -3,339 | -13,206 | 19102 |

| V | Reserves change [increase (-) / Decrease (+)] | -61,406 | -17,905 | -21,550 | -43,574 | 3,339 | 13,206 | -19,102 |

Source: Reserve Bank of India.

Note: P: Preliminary

Annexure II

Free Trade Agreements (FTAs) already in force

| S.No.. | Name of the Agreement | Date of Signing of the Agreement Date of Signing of the Agreement | Date of Implementation of the Agreement & Recent Developments |

| 1 | India – Sri Lanka FTA | 28th December. 1998 | Date of implementation of treaty was 1st March, 2000, The negotiations for the proposed Economic and Technology Cooperation Agreement (ETCA) between India and Sri Lanka, covering trade in goods, trade in services, invest- ment and economic and technology cooperation are in progress. Eleven Round of Negotiations have been completed. |

| 2 | Agreement on SAFTA (India, Pakistan, Nepal, Sri Lanka, Bangladesh, Bhutan, the Maldives and Afghanistan) | 4th January, 2004 | Date of implementation of treaty was 1st January, 2006 (Tariff concessions implemented from 1st July, 2006) |

| 3 | India Nepal Treaty of Trade | 27th October, 2009 | The Treaty has been extended for a further period of seven years and is currently in force till 26th October 2023. A Comprehensive Review of the India-Nepal Treaty of Trade, initiated in 2018, is in progress. |

| 4 | India – Bhutan Agreement on Trade Commerce and Transit | 17th January, 1972 | Renewed periodically, with mutually agreed modifica- tions. Agreement dated 29th July 2006 was valid for ten years. With mutual consent, the validity was extended for a period of one year or the period till the proposed new Agreement comes into force. The renewed Agree- ment has been signed on 12th November, 2016 and came into force with effect from 29th July, 2017. |

| 5 | India – Thailand FTA – Early Harvest Scheme (EHS) | 9th October, 2003 | Date of implementation of treaty was 1st September, 2004 |

| 6 | India – Singapore CECA | 29th June, 2005 | Date of implementation of treaty was 1st August, 2005.

The second review of India Singapore CECA was joint- ly concluded and announced on 1st June, 2018 during the state visit of Prime Minister of India to Singapore. |

| 7 | India – ASEAN- CECA – Trade in Goods, Services and Investment Agreement (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myan-mar, Philippines, Singapore, Thailand and Vietnam) | 13th August, 2009 for goods and November, 2014 for Services and Investment | Date of implementation of treaty for Goods

Services and Investment For Services and Investment, date of implementation of treaty was 1stJuly, 2015. |

| India – South Korea CEPA | 7th August, 2009 | Date of implementation of treaty was 1st January, 2010.

The two sides have commenced negotiations for up- gradation of CEPA in 2016 to explore the possibility of providing further tariff concessions/ simplification of Rules of Origin to Indian exporters. 8th round of negotiations for upgrading India-Korea CEPA was held in June, 2019 in India. |

|

| 9 | India – Japan CEPA | 16th February, 2011 | Date of implementation of treaty was 1st August, 2011 |

| 10 | India – Malaysia CECA | 18th February, 2011 | Date of implementation of treaty was 1st July, 2011 |

Annexure II (contd.)

Preferential Trade Agreements (PTAs) already in force

| S.No. | Name Of The Agreement | Date Of Signing Of The Agreement | Date Of Implementation Of The Agreement & Recent Developments |

| 1 | Asia Pacific Trade Agreement (APTA) (Bangladesh, China, India, Republic of Korea, Lao People’s Democratic Republic and Sri Lanka) | July, 1975 (revised on 2nd November, 2005) | Date of implementation of treaty was 1st November, 1976. |

| 2 | Global System of Trade Preferences (GSTP) (Algeria, Argentina, Bangladesh, Benin, Bolivia, Brazil, Cameroon, Chile, Colombia, Cuba, Democratic People’s Republic of Korea, Ecuador, Egypt, Ghana, Guinea, Guyana, India, Indonesia, Iran, Iraq, Libya, Malaysia, Mexico, Morocco, Mozambique, Myanmar, Nicaragua, Nigeria, Pakistan, Peru, Philippines, Republic of Korea, Romania, Singapore, Sri Lanka, Sudan, Thailand, Trinidad and Tobago, Tunisia, Tanzania, Venezuela, Viet Nam, Yugoslavia, Zimbabwe) | 13th April, 1988 | Date of implementation of treaty was 19th April, 1989. |

| 3 | SAARC Preferential Trading Agreement (SAPTA) (Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan and Sri Lanka) | 11th April, 1993 | Date of implementation of treaty was 7th December, 1995 |

| 4 | India – Afghanistan | 6th March, 2003 | Date of implementation of treaty was 13th May, 2003 |

| 5 | India – MERCOSUR (Argentina, Brazil, Paraguay and Uruguay) | 25th January, 2004 | Date of implementation of treaty was 1st June, 2009. |

| 6 | India – Chile | 8th March, 2006 | Date of implementation of treaty was 11th September, 2007. The agreement has been expanded on 6th September, 2016 and came into force w.e.f. 16th May, 2017. |

Source: Department of Commerce.

Annexure II (contd.)

On-going Trade Negotiations

| S. No. | Name of the Agreement | Status |

| 1 | India – EU BTIA | Negotiations launched on 28th June, 2007 in the areas of Goods, Services, Investment, Sanitary and Phyto-sanitary Measures, Technical Barriers to Trade, Trade Facilitation and Customs Cooperation, Competition, IPR & GIs. Etc. Sixteen rounds of have been held till date. |

| 2 | India – Sri Lanka Economic and Technical Cooperation Agreements (ETCA) | Eleven rounds of negotiations have been held so far. |

| 3 | India – Thailand CECA | Early Harvest Scheme on 83 items implemented. So far, thirty rounds of India-Thailand Trade Negotiation committee (ITTNC) meetings have been held. |

| 4 | India – Mauritius Comprehensive Economic Cooperation and Partnership Agreement (CECPA) | The negotiations under CECPA include Trade in Goods, Trade in Services, Trade Remedies, SPS/TBT issues and Dispute Settlements. The negotiations for CECPA has been finalized. |

| 5 | India – EFTA TEPA (Iceland, Norway, Liechtenstein and Switzerland) | The India- EFTA TEPA (Trade and Economic Partnership Agreement) was launched in January, 2008. So far, seventeen rounds of negotiations have been held. |

| 6 | India – New Zealand FTA/CECA | Ten Rounds of negotiation of CECA have been held so far. The 10th Round was held in New Delhi on 17-18 February, 2015. |

| 7 | India – Israel Trade Agreement | Nine rounds of negotiations on India-Israel FTA have been held so far. |

| 8 | India – Singapore CECA (3rd review) | Third review of India Singapore CECA was launched on 1st September, 2018. |

| 9 | India – SACU PTA (South Africa, Botswana, Lesotho, Swaziland and Namibia) | Five rounds of negotiations have been held so far. |

| 10 | India – Mercosur PTA expansion (Argentina, Brazil, Paraguay and Uruguay) | The existing India-MERCOSUR PTA is being expanded. The third meeting of Joint Administrative Committee (JAC) was held in Brasilia on 29th September, 2016. Both sides have exchanged their initial offers on 14th September, 2017. |

| 11 | BIMSTEC CECA (Bangladesh, India, Myanmar, Sri Lanka, Thailand, Bhutan and Nepal) | Twenty one meetings of the Trade Negotiation Committee (TNC) have taken place. The 21st Meeting of BIMSTEC Trade Negotiating Committee (TNC) was held during 18-19 November, 2018 in Dhaka, Bangladesh. |

| 12 | India – Gulf Cooperation Council (GCC) Framework Agreement | Two rounds of negotiations have been held so far in 2006 and 2008. In 2011, GCC Secretariat stated to have deferred negotiations with all countries until GCC States completely review the issue of negotiations. Recently GCC Secretariat vide its Note Verbale dated 6th November, 2019 has informed that GCC welcomes resumption of India-GCC FTA negotiations. |

| 13 | India – Canada FTA | Ten rounds of negotiation on India-Canada CEPA have been held so far. The 10th round was held in August, 2017 in New Delhi. An Inter-Sessional round was held in February, 2018 at Ottawa. |

| 14 | India – Australia | Nine rounds of negotiations have been held. The 9th round of negotiations was held on 21-23 September, 2015 in New Delhi, India. |

| 15 | India-Malaysia CECA (1st Review) | The first meeting of the India-Malaysia Joint Committee meeting to review implementation of India-Malaysia CECA was held on 8th December, 2014. |

| 16 | India-ASEAN Trade in Goods Agreement (1st Review) | India has requested for the review of India ASEAN Trade in Goods Agreement (AITIGA). |

| 17 | India-Korea CEPA review | Eight rounds of negotiations for upgrading India-Korea CEPA have been held so far. The 8th round was held on 17-18 June, 2019 in New Delhi. |

| 18 | India-Iran PTA | Four meetings have taken place so far |

| 19 | India-Peru Trade Agreement | The four rounds of negotiations have taken place so far. |

| 20 | India-EAEU Technical Consultations | The first round of technical consultations were held on 30-31 January, 2018 in New Delhi. |

| 21 | India-Bangladesh CEPA | A Joint Study for examining the feasibility of CEPA is to be carried out. India has identified Centre for Regional Trade for conducting the study and Bangladesh has been requested to identify a suitable organisation for this purpose. |

| 22 | India-Chile PTA (2nd Expansion) | First meeting of the 2nd Expansion of India Chile PTA was held in New Delhi on 10-11 December, 2019. |

Source: Department of Commerce.

Annexure III

Summary of Changes in Foreign Exchange Reserves

| Sl. No. | Year | Foreign Exchange reserves at the end of financial year (end March) | Total Increase (+)/ Decrease (-) in reserves | Increase (+) / decrease (-) in reserves on a BoP basis | Gain (+)/Loss (-) in reserves due to valuation effect |

| 1 | 2007-08 | 309.7 | 110.5 | 92.2 | 18.4 |

| 2 | 2008-09 | 252.0 | -57.7 | -20.1 | -37.7 |

| 3 | 2009-10 | 279.1 | 27.1 | 13.4 | 13.6 |

| 4 | 2010-11 | 304.8 | 25.8 | 13.1 | 12.7 |

| 5 | 2011-12 | 294.4 | -10.4 | -12.8 | 2.4 |

| 6 | 2012-13 | 292.0 | -2.4 | 3.8 | -6.2 |

| 7 | 2013-14 | 304.2 | 12.2 | 15.5 | -3.3 |

| 8 | 2014-15 | 341.6 | 37.4 | 61.4 | -24.0 |

| 9 | 2015-16 | 360.2 | 18.5 | 17.9 | 0.6 |

| 10 | 2016-17 | 370.0 | 9.8 | 21.6 | -11.8 |

| 11 | 2017-18 | 424.5 | 54.6 | 43.6 | 11.0 |

| 12 | 2018-19 | 412.9 | -11.7 | -3.3 | -8.3 |

| 13 | H1: 2018-19 | 400.5 | -24.0 | -13.2 | -10.8 |

| 14 | H1: 2019-20 | 433.7 | 20.8 | 19.1 | 1.7 |

Source: Reserve Bank of India (RBI).

Notes:

1. Arguments guided by World Economic Outlook of IMF.

2. Net terms of trade (NTT) of a country is the ratio of unit value index of export to that of import.

3. Exports plus imports from a trade partner as a share of total imports plus exports of India determines the share of the trade partner in India’s merchandize trade.

4. It is a set of next generation of reforms, under which a new functionality in software systems of Indian customs is enabled, that obviates the need of producing import related documents physically to custom officials for approval, thereby reducing release time.

5. As per inputs received from Department of Commerce.