CA Anuj Agrawal

India being an agriculture based economy, many activities are being carried out in way to raise live animals, crop harvesting & selling etc and apart from its dealing within an unorganized sector, there are many corporate sector (either listed or not) which directly or indirectly operate into such agricultural activities in India.

India being an agriculture based economy, many activities are being carried out in way to raise live animals, crop harvesting & selling etc and apart from its dealing within an unorganized sector, there are many corporate sector (either listed or not) which directly or indirectly operate into such agricultural activities in India.

Under the current accounting systems there is nothing specific in terms of guidance which can talk about how to account/ deal with these agricultural activities in the books of account based on their very different nature comparing to other normal goods/ services. New accounting requirement basically leading towards fair value accounting comparing to the cost basis accounting for such agricultural products/ assets.

Ind-As -41 “Agriculture” which is mainly in line with IAS-41 “Agriculture” (as issued by IASB) has now been brought into which will mandatorily be applicable on the entities/ businesses which are required to follow such accounting standards. First of all, let’s understand the scope of this standard in brief.

As per para 1 of Ind-As 41 states that: – It applies to the following when they relate to Agriculture activities –

a) Biological assets,

b) Agriculture produce at the point of harvest,

c) grant related to biological asset

Let’s get some practical expedient on these words as mentioned in the standard. The agriculture activities is the management by an entity of the biological transformation and harvest of biological assets for sale or for conversion into agricultural produce or into additional biological assets which essentially means that there should be some managed services then only it will be qualified as agricultural activities. For example there are some fishes which are in the sea water and apparently the sea cannot be managed by any entity (it is rather managed by government) hence these activity will not fall into agriculture activities for such entity. Standard wanted majorly to focus on LIVING plants and /or animals which are being used either to produce some harvested products or used to grow any biological assets further.

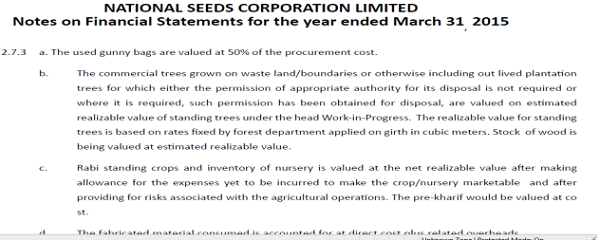

Now, currently there is nothing specific in our Indian accounting system which can talk about Agriculture industry and hence companies are making their own policies in line with the basic principles to recognize assets/ liabilities. Below example is one of the company engaged in agricultural related activities and has mentioned its accounting policies under current accounting system-

Readers can download full report by using this publically available link http://www.indiaseeds.com/doc-file/NSC1415.pdf

Now, let’s understand what exactly this standard tries to cover and its measurement methodology in a more simple and practical manner-

1. Standard clearly defines what is to be included, hence one needs to focus what is specifically excluded by the standard to avoid any confusion while interpreting this standard. There are some plants, organic substances etc. which are mainly being used by drug companies duly patented will not be covered in the standard because either it is used for development activity (to be expensed off) or as Intangible assets which will be covered by some other standards,

2. As per this standard, all biological assets at the initial recognition and subsequently will be measured at its fair value less cost to selland all harvested produce (products which usually come out from biological assets) at the point of harvest (Only at the harvest point) whereas in the current accounting system these type of products are being measured at cost or at its NRV,

3. Standard says that afterthe point of harvest (i.e. a product which is to be sold by the entity) it will then be treated as inventories (if not sell) and hence Ind-As -2 “Inventories” will be applicable,

4. Standard says that there should be some transformationof biological assets (defined above) and should be managed (as discussed above) by the entity for its sale or producing harvested product,

5. Land which is normally being used for the purpose of such agriculture activities are not in the scope of this standards and will continue to be governed with either Ind-As 16 “Property, plant & equipment” or Ind-As 40 “Investment Property” as the case may be,

6. Any Intangible assets that meets recognition criteria will be governed by Ind-As 38 “Intangible Assets” and will not be covered within this standard,

7. Now, one has to carefully note that while transiting from current accounting practice to Ind-As regime there would be deemed cost exemption available for all assets that are being carried over and hence entity will have gain/ loss by valuing such biological assets at fair value soon after the date of such transition,

8. There are some practices available where an entity makes a policy to capitalize some of the directly attributable expense incurred on such biological assets however it will not make any difference by capitalizing such expenses in such assets as all such assets will be fair valued at each reporting date with corresponding effects in P&L (diff between previous carrying value and reporting date fair value),

9. As we are aware that under the Ind-As regime, it is much easier to recognize an asset than the present accounting system as if an entity can demonstrate that an expense incurred has expected use for more than one period(considering other criteria has been fulfilled to recognize as an asset) then it can be capitalized accordingly,

10.There could be some contracts to sell such assets/ harvested products which can either be executory (for actual usage or physical delivery purposes) in nature or net settlement in cash , then these contracts will be accounted either by Ind-As 109 as “Derivatives” or simple sale/ purchase contracts,

11. There are some situation where fair value of such biological assets can not be reliably measured because of non-availability of active market then standard gives alternative to account at cost till the time its fair market value is available,

12. Now, There are many situation where government provide grants to such activities, then standard states as per its para 34 “An unconditional government grant related to a biological asset measured at its fair value less costs to sell shall be recognised in profit or loss when, and only when, the government grant becomes receivable”, which means that when there is no pending condition (where some grants requires an entity to fulfill certain conditions) which is to be fulfilled by the entity then only it will recognized in profit & loss account, However para 37 of the standard specifically excludes its applicability in case the grants are being given to the assets measured at cost, and in those cases it will be governed by Ind-As 20 “Government Grants”,

These are based on some practical experiences encountered during professional assignments and hence these should not be treated any kind of advise in any manner. The facts/ circumstances might be different in each case and can change its recognition/ measurement accordingly.

(You may reach to me for any further discussion on anujagarwalsin@gmail.com or whatsapp +91 9634706933)

Author Bio

what if the company has not recognised agricultural income as per ind as 41 but now wants to subsequently recognise it??

Dear sir, thanks for your comments..

Worthful article. Thanks for sharing .