Case Law Details

Kaushal Ferro (P) Ltd. Vs Commissioner of CGST (CESTAT Kolkata)

Material Facts

The appellant, a manufacturer of sponge iron falling under Chapter 72 of the Central Excise Tariff, availed CENVAT credit on iron and steel items such as angles, channels, beams, joists, plates and bars under Chapter 72, along with welding electrodes, which were used in the manufacture of capital goods within its factory. A show cause notice dated 27.10.2006 proposed denial of CENVAT credit availed during October 2005 to August 2006.

The appellant submitted a Chartered Engineer-certified utilisation statement and relied upon a physical verification conducted by the jurisdictional Range Superintendent on 31.07.2013. The verification found that, except for certain identified items, the fabricated goods were specified capital goods.

The adjudicating authority disallowed CENVAT credit of Rs.9,95,316 on iron and steel items and Rs.33,510 on welding electrodes, aggregating to Rs.10,28,826, treating the inputs as used for fabrication of support structures, imposed a penalty of Rs.2,50,000 under Rule 15(1) of the CENVAT Credit Rules, 2004, but allowed CENVAT credit of Rs.36,81,538 on other items used for manufacture of specified capital goods.

Both the appellant and the department filed appeals before the Commissioner (Appeals). The Commissioner (Appeals) rejected the appellant’s appeal as time-barred, reckoning limitation from the date of issue of the adjudication order, and allowed the department’s appeal, relying upon the Larger Bench decision in Vandana Global Ltd.

Procedural History

The appellant challenged the Commissioner (Appeals)’ order before CESTAT Kolkata. It contended that limitation should have been computed from the date of communication of the adjudication order and that the Commissioner (Appeals) had wrongly relied upon Vandana Global Ltd., which had subsequently been overturned.

Legal Issues

- Whether the appellant’s appeal before the Commissioner (Appeals) was barred by limitation.

- Whether CENVAT credit on iron and steel items used in fabrication of capital goods/supporting structures was admissible.

- Whether CENVAT credit on welding electrodes used in fabrication, repair and maintenance of capital goods was admissible.

Relevant Statutory Provisions

- Rule 2(a) of the CENVAT Credit Rules, 2004.

- Rule 15(1) of the CENVAT Credit Rules, 2004.

- Section 35(1) of the Central Excise Act.

Appellant’s Submissions

The appellant submitted that:

- The adjudication order was received on 28.04.2016 and limitation should be computed from the date of communication rather than the date of issue.

- Even assuming delay, it fell within the condonable period and no opportunity was given to seek condonation.

- The Commissioner (Appeals) failed to verify departmental records regarding service of the adjudication order.

- The findings of the adjudicating authority were supported by the Chartered Engineer’s certificate and the physical verification report.

- The Larger Bench decision in Vandana Global Ltd. was no longer good law in view of subsequent High Court decisions.

- Supporting structures and fabricated components qualified as capital goods or accessories under Rule 2(a) of the CENVAT Credit Rules.

- Welding electrodes used in manufacture of capital goods were eligible inputs.

Revenue’s Submissions

The Revenue argued that:

- The disputed inputs were used in supporting structures which were not eligible for CENVAT credit.

- The contravention came to light only after detailed verification and investigation.

- The confirmed demand was justified.

Tribunal’s Findings and Reasoning

Limitation

The Tribunal found that the Commissioner (Appeals) assumed that the adjudication order had been served on the date of its issue without any supporting evidence. The order appeared to have been dispatched by post and no verification was undertaken to establish the actual date of service.

The Tribunal also observed that if the Commissioner (Appeals) considered the appeal to be belated, a defect memo should have been issued to allow the appellant to explain the delay. Failure to do so violated the principles of natural justice.

The Tribunal further noted that although the Commissioner (Appeals) observed that the appeal deserved rejection on limitation, he nevertheless examined the merits and confirmed the entire demand. It therefore held that the appellate order had effectively been passed on merits.

CENVAT Credit on Iron and Steel Items

The Tribunal examined the annexures and the Chartered Engineer’s certification regarding use of angles, channels and other steel items in manufacture of capital goods within the factory.

It held that the Larger Bench decision in Vandana Global Ltd. had been overturned by the Chhattisgarh High Court. It also referred to subsequent High Court decisions recognising eligibility of CENVAT credit on goods used for fabrication of supporting structures and capital goods.

Applying those decisions to the facts before it, the Tribunal held that denial of CENVAT credit of Rs.45,50,485 on iron and steel items such as angles, channels and joists was not legally sustainable.

CENVAT Credit on Welding Electrodes

The Tribunal held that the issue regarding welding electrodes was no longer res integra. Referring to the Delhi Tribunal’s decision in Nuvoco Vistas Corporation Limited, which relied upon Supreme Court decisions, it observed that welding electrodes used in fabrication, repair and maintenance of capital goods are used in relation to manufacture and qualify for CENVAT credit.

Accordingly, it held that denial of CENVAT credit of Rs.1,59,879 on welding electrodes was unsustainable.

Final Ruling

The Tribunal:

- Set aside the impugned order.

- Held that denial of CENVAT credit on iron and steel items amounting to Rs.45,50,485 was not legally sustainable.

- Set aside the denial of CENVAT credit of Rs.1,59,879 on welding electrodes.

- Allowed the appeal.

- Held that the appellant would be entitled to consequential relief, if any, as per law.

Cases Discussed

- Nuvoco Vistas Corporation Limited Versus Commissioner of Central Excise (CESTAT Delhi), FINAL ORDER NO.56022/2024 dated 18.07.2024

- CGST & CE Rourkela Vs SPS Steels Ltd & Power Ltd. (Orissa High Court), 2022 (382) ELT 49 (Ori)

- CCE Vs. Singhal Enterprises Pvt. Ltd. (Chhattisgarh High Court), 2018 (359) ELT 313 (Chhattisgarh)

- Vandana Global Ltd. (Chhattisgarh High Court), 2018 (16) GSTL 462 (Chhattisgarh)

- CCE Vs. Madras Alluminium Co. Ltd. (Madras High Court), 2017 (349) ELT 133 (Mad.)

- Thiru Arooran Sugars and Ors Vs CCE (Madras High Court), [2017-TMI-524-MAD-HC]

- Thiru Aroonan Sugars Vs CESTAT (Madras High Court), [2017 (355) ELT 373 (Mad.)]

- Mundra Ports and Special Economic Zone Ltd Vs CCE (Gujarat High Court), (2015) 39 STR 726 (Guj.)

- CCE Vs. Jindal Steel & Power Ltd. (CESTAT Delhi), 2015 (330) ELT 708 (Tri.-Del.)

- Muthu Kumar Vs. CESTAT (Madras High Court), (2014) 35 STR 468 (Mad.)

- BSNL Vs. CCE (CESTAT Delhi), (2014) 33 STR 332 (Tri.-Del.)

- Surya Alloys Industries Ltd Vs UOI (Calcutta High Court), 2014 (305) E.L.T. 47 (Cal.)

- CCE VS Rajasthan Spinning & Weaving Mills Ltd. (Supreme Court of India), 2010 (235) E.L.T. 481 (S.C.)

- Commissioner of Central Excise, Jaipur v. M/s. Rajasthan Spinning & Weaving Mills Ltd. (Supreme Court of India), 2010 (255) E.L.T. 481 (S.C.)

- Commissioner of Central Excise, Coimbatore v. Jawahar Mills Ltd. (Supreme Court of India), 2001 (132) E.L.T. 3 (S.C.)

FULL TEXT OF THE CESTAT KOLKATA ORDER

The appellant is manufacturer of sponge iron falling under CET 72. In the course of their operations, they have taken the CENVAT Credit for Inputs like Angles, Channels, Beams, Joists, Plates, Bars falling under CH.72 and Welding Electrodes, which were used for manufacture of capital goods. A Show Cause Notice was issued on 27.10.2006 for the CENVAT Credit taken during the period October’2005 to August’2006. The lower authorities relied on the decision of the Larger Bench in the case of Vandana Global Ltd. Vs CCE reported in 2010(253) E.L.T. 440(LB) while denying the CENVAT Credit and confirming the demand. Being aggrieved, the appellant has filed the present appeal before the Tribunal.

2. The Ld. Counsel appearing on behalf of the appellant makes the following submissions:

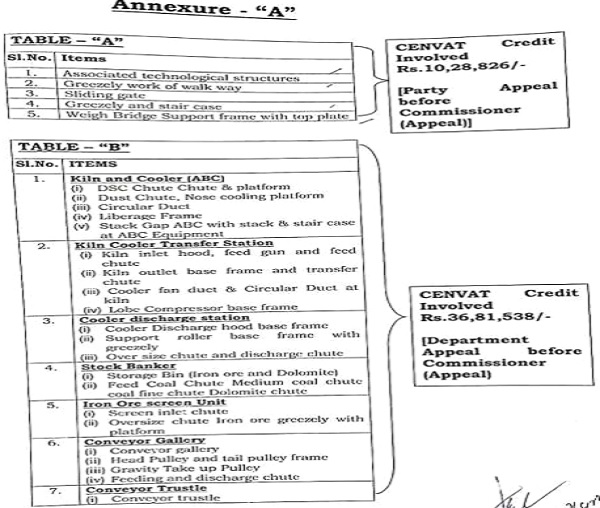

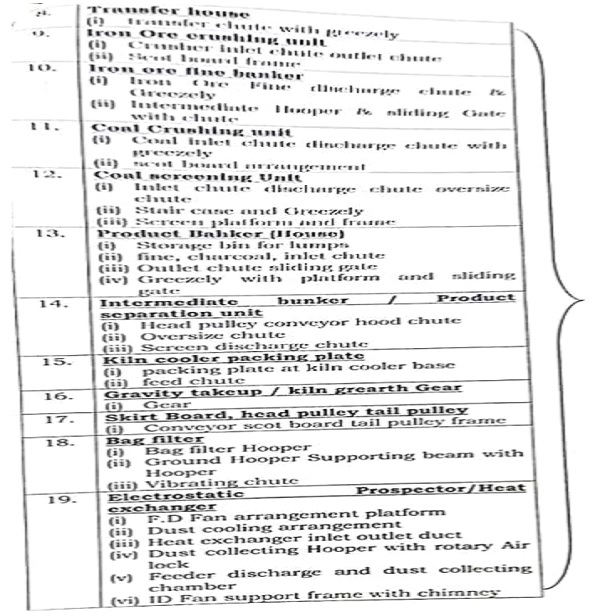

i. During the period 2005-06 and 2006-07 for setting up of Sponge Iron unit, the Appellant purchased various Iron and Steel materials (CH.72) and Welding Rods falling under Ch.38 on payment of excise duty of Rs.45,50,485/-and Rs.1,59,879/- respectively aggregating to Rs.47,10,364/-. The details of the manufacture capital goods are as per the the Annexure – “A” submitted along with Appeal.

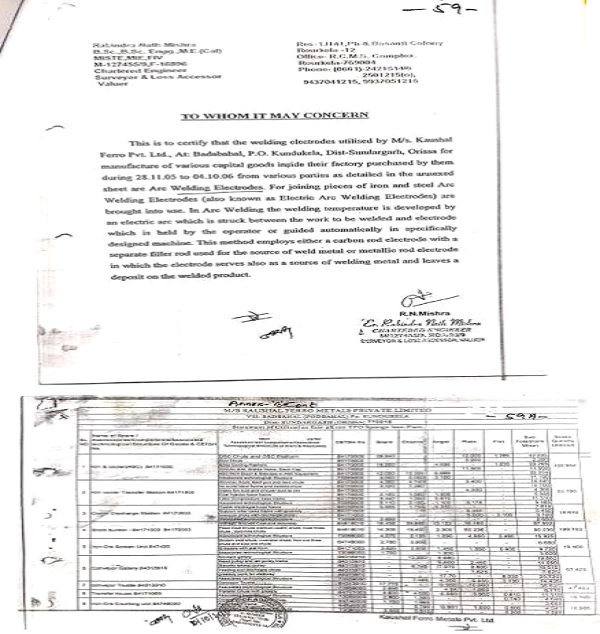

ii. The Appellant furnished Utilization Statement (Page 59 and also Para 4.14 at Page 128 of OIO) duly certified by qualified Chartered Engineer in support of their of claim.

iii. The ‘Capital Goods’ manufactured by them are separately fabricated and superficially attached to technological structures, foundations inside their factory by nuts and bolts.

iv. On the direction of Ld. Adjudicating Authority, a Physical Verification was conducted on 3107-2013 by the Jurisdictional Range Superintendent who submitted Physical Verification Report dated 31-07-2013.

v. In the said report, all other emergent goods, except Coal Injector base frame, Greezely work of Walk Ways, Sliding Gate, Greezely and Stair Case, Weigh Bridge support Frame with Top Plate and Associated Support Structures were found to be specified ‘Capital Goods’. (OIO, Page 128)

vi. Vide Order-in-Original dated 29-03-2016 (Para 4.14 Page 128), the Ld. Additional Commissioner disallowed CENVAT Credit of Rs.9,95,316/- on Iron and Steel materials and CENVAT Credit of Rs.33,510/- on Welding Electrodes aggregating to Rs.10,28,826/- on the ground that the impugned inputs are utilized for fabrication of ‘support structures’ on which CENVAT Credit cannot be allowed in view of decision in Vandana Global Ltd case. The Ld. Addl. Commissioner, further imposed penalty of Rs.2,50,000/-U/r 15(1) of the Rules of 2004 upon the Appellant.

vii. The Ld. Additional Commissioner, however, allowed CENVAT Credit of Rs.35,55,169/- on Iron and Steel materials and CENVAT Credit of Rs.1,26,369/- on Welding Electrodes aggregating to Rs.36,81,538/- (Para 4.18 of OIO Page 129) on the ground that impugned inputs are utilized for manufacture of specified Capital Goods in terms of various sub-clauses of Rule 2(a)(A).

2.1. Being aggrieved with confirmed demand, the present appellant filed their appeal before the Commissioner (Appeals). The Dept. being aggrieved by the dropping of the part of the demand, filed their appeal before the Commissioner (Appeals).

2.2. Both these appeals were taken up together by the Commissioner (Appeals) for disposal.

2.3. The Ld. Commissioner (Appeal) vide the impugned Order dated 22-03-2018, rejected the Appeal filed by the Appellant on the ground that the same is barred by period of limitation of 60 days. He has rejected the appeal filed by the Appellant reckoning limitation from the date of issue of the adjudication Order i.e. 29-03-2016 and held that the appeal is filed after a period of 60 days i.e. on 2706-2016 ignoring that the adjudication order was served on them on 28-04-2016 and also the delay if any was within condonable period and in any case the Appellant must have been provided with an opportunity to file application for condonation of delay which are arbitrarily not provided.

2.4. Vide the same Order, the Ld. Commissioner (Appeal) allowed the Appeal filed by the department and set aside the adjudication order dated 29-032016.

2.5. The Ld. Commissioner (Appeal) in the instant case instead of considering the date of ‘communication’ for the purpose of computing the statutory period of limitation of 60 days for filing the appeal and further period of 30 days as condonable period in terms of Sec 35(1) of the Act, considered date of ‘issue’ of impugned Order dated 29-03-2016 for the same on ground that the Appellant has failed to prove that the date of receipt of adjudication order is 28-04-2016. The date of issue of the adjudication Order was 29-03-2016, date of service was 28-04-2016 and the date of filing appeal was 27-06-2016. In the instant case, he did not verify the documents available with department to ascertain date of communication of the Order-in-Original on dated 28-04-2016.

3. The Appellant most humbly submits that: –

i. The Ld. Commissioner (Appeal) failed to appreciate that in the instant case there is nothing on record to suggest that the said adjudication order was served upon the Appellant prior to 28-04-2016. The Appellant relies on following judgments :-

(i) Muthu Kumar Vs. CESTAT reported in (2014) 35 STR 468 (Mad.);

(ii) BSNL Vs. CCE reported in (2014) 33 STR 332 (Tri.-Del.).

ii. The Appellant in the above background of the case most humbly submits that rejection of Appeal filed by the Appellant, more particularly, when the department appeal was also pending adjudication before the Ld. Commissioner (Appeal) against the same very adjudication Order and in any case the delay was within condonable period of 30 days.

iii. The Ld. Commissioner (Appeal) so far as department appeal is concerned treated the impugned goods as support structures on the basis Vandana Global Ltd. Vs CCE reported in 2010 (253) E.L.T. 440 (LB) which is no more good law and denied CENVAT Credit of Rs.36,81,538/- having been reversed by Hon’ble Chhattisgarh High Court in 2018 (16) GSTL 462 (CHH).

iv. The Ld. Commissioner (Appeal) seriously erred in holding that solely on the basis of Physical Verification Report and Chartered Engineer’s Certificate, the Ld. Adjudicating Authority could not have held that the emergent goods are not supporting structures, but are specified Capital Goods U/r 2(a)(A) of the CENVAT Credit Rules, 2004.

v. The Ld. Commissioner (Appeal) failed to appreciate that in the instant case the department not led any contra material to dislodge the findings of Ld. Additional Commissioner. Hence, findings of Ld. Commissioner (Appeal) is based on no evidence at all.

vi. The Appellant most humbly submits that the Physical Verification Report and Chartered Engineers certificate are experts opinion which cannot be rejected or brush aside without any contra material and/or counter expert opinion.

vii. The definition of ‘capital goods’ U/r 2(a) is wide and comprehensive. It covers in its fold components, spares or accessories made solely and principally for capital goods specified under clause (i) of Rule 2(a)(A). Clause (i) of Rule 2(a) covers “all goods” which includes parts, spares, accessories, components etc. of goods falling under the specified chapters. Clause (iii) of Rule 2(a) brings all components, spares and accessories under its fold which does not fall under the specified chapters

viii. The Hon’ble High Court of Gujarat in the case of Mundra Ports and Special Economic Zone Ltd Vs CCE reported in (2015) 39 STR 726 (Guj.), has held that Notification dated 07-07-2009 is prospective in nature and decision of Larger Bench of Hon’ble Tribunal in the case of Vandana Global Ltd. is not a correct law.

ix. The Appellant further submits that Hon’ble Madras High Court in the case of Thiru Arooran Sugars and Ors Vs CCE reported in [2017-TMI-524-MAD-HC], while impliedly overruling the decision of Hon’ble Larger Bench in Vandana Global Ltd. case held that Notification dated 07-07-2009 itself in no uncertain terms states that it shall come into force from the date of its publication in official gazette, hence, the said amendment will not apply to period prior 07-07-2009.

x. The Hon’ble Court while holding so relied upon amongst other its earlier judgments in the case of Thiru Aroonan Sugars Vs CESTAT reported in [2017 (355) ELT 373 (Mad.)] which due to non challenge has attained finality. The Hon’ble Court further held that even after 07-07-2009 explanation brought in by the said Notification dated 07-07-2009 CENVAT credit on Iron and Steel materials, Cement etc used for making of support structures, construction of foundation etc cannot be denied as ‘inputs’ in terms of main limb of Rule 2(k) so long as items fulfill criteria of ‘used in or in relation of manufacture of final products, whether directly or indirectly’.

xi. The Appellant further submits that the Hon’ble Calcutta High Court in the case of Surya Alloys Industries Ltd Vs UOI reported in 2014 (305) E.L.T. 47 (Cal.) considering the judgment of Hon’ble Apex Court in the case of CCE VS Rajasthan Spinning & Weaving Mills Ltd reported in 2010 (235) E.L.T. 481 (S.C.) and applying the ‘user test’ held that decision of Vandana Global Ltd. is no more a valid law.

xii. It is now well settled that by a series of judgment that support structures are ‘accessory’ of various production machineries and therefore are Capital Goods and credit is admissible. The Appellant relies on CCE Vs. Madras Alluminium Co. Ltd. reported in 2017 (349) ELT 133 (Mad.).

5. Cenvat Credit Rules, 2004 have defined the various expressions found therein in Rule 2 thereto. The expression “capital goods” has been defined as under :

“capital goods” means :-

(A) the following goods, namely :-

(i) all goods falling under Chapter 82, Chapter 84, Chapter 85, Chapter 90, heading No. 6805, grinding wheels and the like and parts thereof falling under heading 6804 of the First Schedule to the Excise Tariff Act;

(ii) Pollution control equipment;

(iii) Components, spares and accessories of the goods specified at (i) and (ii);

(iv) moulds and dies, jigs and fixtures;

(v) refractories and refractory materials;

(vi) tubes and pipes and fittings thereof; and

(vii) storage tank, used;

(1) in the factory of the manufacturer of the final products, but does not include any equipment or appliance used in an office;”

6. From a perusal of the above, it makes clear that such goods which fall under Chapters 82, 84, 85 and 90 and Headings No. 90, 68.05, etc., answer the description of capital goods. Similarly pollution control equipment also answers the description of capital goods. But However, the following which is found in the definition has some significance for the question that has engaged our attention. It reads as under;

“Components, spares and accessories of the goods specified at (1) above.”

While there is no difficulty for one to understand what constitutes components or spares of certain equipments, but the expression “accessories” is not free from any doubt. The expression “accessories” is normally understood as a thing which could be added to some thing else in order to make the former more useful, versatile or attractive. The show cause notice dated 4-42012 had enclosed thereto, an annexure listing out the equipments, for which the Cenvat credit has been initially taken by the respondent together with their usages. When we peruse the tabulated statement, in particular with regard to their usage, we have noticed that steel plates have been used by the respondent for supporting the other essential equipments such as HP/LP Heaters, Grider of cranes, cable trenching covering and also for covering the hot area of the boiler.

7. The claim of the respondent was that it has undertaken construction of the 4th unit of a captive power plant. In that process, it has utilized this material and “construed” them as “accessories”. We could also notice that the MS angles have been used as a support structure either for construction of a platform or for ladders. Going by the common understanding of the expression ‘accessories’, we are of the view that the notion entertained by the respondent that the MS plates and MS angles utilised by it at the first instance for Cenvat credit are only intended to enhance the effective utilisation of the other equipment which is needed to be put in place for their 4th unit of the captive power plant. Such an impression that MS plates and MS angles can be used as accessories is not a totally absurd view.

xiii. In the case of CCE Vs. Jindal Steel & Power Ltd., reported in 2015 (330) ELT 708 (Tri.-Del.) it is held by the Hon’ble Tribunal that Crane Girders, Crane Rail, Crane Column, Crane Surge Girders, Crane Auxiliary Girders being essential accessories for EOT Crane are covered under the definition of “Capital Goods”. It is further held that “Base Frames” for different machineries such as Air Preheated, Coal Feeder, Deachator Drum, etc. on which machineries are installed for rigidity and vibration free operation as no heavy machine/machinery can be installed without base frames, hence, there frames are essential “accessories” covered under Capital Goods. It is also held that “Chimney” and “Flue Duct” used for emission of fumes/gases and for holding/transferring gases for their emission through Chimney are essential “accessories” and are “Capital Goods”.

xiv. The Appellant most humbly submits that in the case of CCE Vs. Singhal Enterprises Pvt. Ltd. reported in 2018 (359) ELT 313 (Chhattisgarh), it is held by the Hon’ble Chhattisgarh High Court that ‘supporting structures’ manufactured out of structurals materials are eligible ‘Capital Goods’ in terms of Rule 2(a)(A).

4. In view of the above submissions, the Ld Counsel prays that the impugned Order may be set aside and the appeal may be allowed.

5. The Ld. Authorized Representative (A.R.), appearing for the Revenue, submits that the inputs in question have been used in the supporting structures, which are not eligible for CENVAT Credit. He further submits that only on account of detailed verification and investigation the contravention by the appellant has come to light. Hence, he justifies the confirmed demand.

6. Heard both the sides. Perused the Appeal papers and additional documents placed before us.

7. First of all we have to take up the issue as to whether, the appellant’s appeal before the Commissioner (Appeals) was time-barred or not. From the facts discussed above, it is seen that the OIO was dated 29.03.2016. The appellants have claimed that the same was received by them on 28.04.2016 and the appeal was filed on 27.06.2016. If the OIO date itself is taken as the date of serving of the same to the appellant, as has been taken by the Commissioner (Appeals), the appellant was required to file the Appeal by 28.05.2016, i.e. within 60 days. After this if the condonable period of 30 days is considered, then the appeal should have been filed by 27.06.2016. In this case, it is seen from the acknowledgement given by the Commissioner (Appeals) office that the appellant has filed their Appeal on 27.07.2016. If the Commissioner (Appeals) takes a view that the appeal was filed belatedly, proper Defect Memo should have been issued allowing the appellant to make their submissions. This has not been done this case, thus giving a go-by to the principles of natural justice. Further, nowhere any evidence has been brought in to the effect that the OIO was served on 29.03.2016 itself. From the copy marked to the appellant it is seen that the File Number along with suffix ‘2189A’ dated 29.03.2016 is appearing on the last page, which makes it clear that it was not served in person by taking any acknowledgement, but was sent by post only. The Commissioner (Appeals) has failed to get the matter verified with the Divisional officials as to how it was served on the appellant. He has gone on the assumption that it was served on the date of OIO itself, which rarely happens, unless it is proved by way of dated acknowledgement in the OIO by the receiver of the OIO.

8. Further from the first para of Page 11 of the OIA, it is observed that he has held “the claim of the appellant regarding date of receipt of the impugned OIO is not acceptable; in that view of the matter, the appeal filed by the appellant No.2, i.e., M/s Kaushal Ferro (P) Ltd deserves to be rejected on the above ground”

9. However, it is seen that after making the above observation, he has not dismissed the appeal on this ground as can be seen from the subsequent order portion of the OIA. He has gone on to discuss the merits of the case, eligibility of CENVAT Credit and has relied on the LB decision of the Vandana Global Ltd and has finally confirmed the entire demand of Rs.47,10,364 at Para 6 of the OIA.

10. In view of the factual details discussed above, we find that the OIA could not have been passed by dismissing on account of time bar, nor has it been done. Therefore, we have not hesitation to hold the view that the OIA has been passed only on merits, denying the CENVAT Credit by relying the Vandana Global case law.

11. Coming to the eligibility of the CENVAT Credit, we have gone through the Annexure A [Table A & Table B] give the details of the end capital goods / structures on which the CENVAT Credit was denied. The same is reproduced below:

–

12. We also find that the Chartered Engineer has certified usage of ‘Welding Electrodes’ and other items like Angles, Channels etc in respect of various capital goods manufactured within the factory premises. Sample data is reproduced below:

13. We find that the decision of LB in the case of Vandana Global was overturned by Chattisgarh High Court – 2018 (16) GSTL 462 (Chhattisgarh), holding as under:

“5. The impugned order of the Tribunal had come up for consideration before different High Courts either cited as precedent or as relied upon by the Tribunal in different other matters. The Gujarat High Court in Mundra Ports & Special Economic Zone Ltd. – 2015 (39) S.T.R. 726 (Guj.) referred to the contents of the amendment, to the extent it is relevant for the purpose of this case and held as follows:

“We do not find that amendment made in the Cenvat Credit Rules, 2004 which come into force on 7-7-2009 was clarificatory amendment as there is nothing to suggest in the Amending Act that amendment made in Explanation 2 was clarificatory in nature. Wherever the Legislature wants to clarify the provision, it clearly mentions intention in the notification itself and seeks to clarify existing provision. Even, if the new provision is added then it will be new amendment and cannot be treated to be clarification on particular thing or goods and/or input and as such, the amendment could operate only prospectively.”

6. That view has been quoted with approval by the Madras High Court in M/s. Thiruarooran Sugars v. Customs, Excise and Service Tax Appellate Tribunal (CMA 3814/2014 and connections) decided on 10-7-2017 [2017 (355) E.L.T. 373 (Mad.)] to conclude that the said amendment cannot be treated as clarificatory. M/s. Thiruarooran Sugars also considered the issue as to the effect and fundamental value of the evidentiary statement made by the Finance Minister dealing with an amendment in the budget speech.

7. Section 37 of the Central Excise Act, 1944; for short, ‘the Act’, is a rule making power. Section 37(2)(xvia) provide for the credit of duty paid or deemed to have been paid on the goods used in, or in relation to, the manufacture of excisable goods. Section 37(2A) of the Act – The power to make rules conferred by clause (xvi) of sub-section (2) shall include the power to give retrospective effect to rebate of duties on inputs used in the export goods from a date not earlier than the changes in the rates of duty on such inputs. Though the power to make rules include the power to give retrospective effect, while doing so the provision under consideration is neither made retrospective nor could it be treated as one.

8. We are in complete agreement with the ratio of Mundra Ports (supra) and M/s. Thiruarooran Sugars (supra) on all fours.

9. Resultantly, we answer the questions formulated in these appeals in favour of the assessees and against the Revenue.”

14. The Orissa High Court in the case of CGST & CE Rourkela Vs SPS Steels Ltd & Power Ltd. – 2022 (382) ELT 49 (Ori), has held as under :

“15. Reference could also be made to the decision in Commissioner of Central Excise, Jaipur v. M/s. Rajasthan Spinning & Weaving Mills Ltd. – 2010 (255) E.L.T. 481 (S.C.) where the Supreme court allowed Modvat credit on steel plates and M.S. channels used in the fabrication of chimney for the diesel generating set. In the said decision, the Supreme Court referred to the ‘use test’ evolved in Commissioner of Central Excise, Coimbatore v. Jawahar Mills Ltd. – 2001 (132) E.L.T. 3 (S.C.). The Madras High Court in CCE, Salem v. Madras Aluminium Co. Ltd. – 2017 (349) E.L.T. 133 (Mad.) also deployed a similar test. The decision of the said Madras High Court in India Cements Ltd. – 2012 (285) E.L.T. 341 (Mad.) which has discussed the decision of the Supreme Court in Saraswati Sugar Mills is also relevant in this context.

16. The view taken by the CESTAT is consistent with the decisions of the Madras High Court in CCE, Salem v. Madras Aluminium Co. Ltd. and India Cements Ltd. (supra).

17. For the aforementioned reasons, the questions framed by this Court are answered as under :

(a) Question (i) is answered in the affirmative by holding that the CESTAT was justified in dismissing the Department’s appeal since the credit was claimed in respect of the inputs used for fabrication items supporting structures of capital goods.

(b) Question (ii) is answered in the affirmative by holding the CESTAT was right in law by allowing Cenvat credit on the goods used for fabrication of supporting structure for capital goods.

(c) Question (iii) is answered in the affirmative by holding that the Tribunal was right in law in holding that the fabrication goods used for supporting structures were capital goods for which Cenvat credit was allowable.

18. These appeals are accordingly dismissed, but in the circumstances, with no order as to costs. An urgent certified copy of this order be issued as per Rules.”

15. We find that to the factual matrix of the present appeal, the cited case laws are squarely applicable. Hence, we hold that denial of CENVAT Credit of Rs.45,50,485/- on various items like angles, channels, joists etc is not legally not sustainable and we set aside the same.

16. Coming to the denial of CENVAT Credit of Rs.1,59,879/- on account of the CENVAT taken on electrodes, we find that the issue is no more res integra. It has been held time and again that welding electrodes used in fabrication of capital goods, repairs and maintenance of the capital goods are essential for the manufacturing activity. The Delhi Tribunal in the case of Nuvoco Vistas Corporation Limited Versus Commissioner of Central Excise, vide FINAL ORDER NO.56022/2024 dated 18.07.2024 has held as under :

3. The issue for consideration in the present appeal relates to the admissibility of CENVAT Credit on welding electrodes as inputs. The submission of the learned counsel for the appellant is that the issue has been settled by the Apex Court in the case of M/s.Lafarge India Limited Vs. Commissioner of Central Excise, Raipur 2 and also in the case of The Kisan Cooperative Sugar Factory Ltd. Vs. Commissioner of Central Excise, Meerut-I 3, wherein it has been categorically held that the cenvat credit is admissible on welding electrodes used in the repair and maintenance activities. The relevant para of the judgement is quoted below:-

“11. On consideration of sub-rule 4 of Rule 57-A of the Central Excise Rules, 1944, it is noted that the credit of specified duty is allowed in respect of two categories of inputs namely (i ) inputs used in the manufacture of final products; and (ii) inputs used in or in relation to the manufacture of final products whether directly or indirectly and whether contained in the final product or not. The latter category is quite wide enough to incorporate the use of welding electrodes and gases in the instant case for the purpose of maintenance and up-keep, which is in relation to the manufacture of final products and which is indirect and is not contained in the final product as such. Further, the expression “in relation to” is of a wider import. Hence, the appellant is entitled to the benefit of MODVAT/CENVAT Credit for the period in question.”

5. Considering the facts of the present case, in the light of decision of the Apex Court referred above, the appellant is entitle to CENVAT Credit on welding electrodes as inputs used in the manufacture of final products – cement and clinker. The impugned order, therefore, needs to be set aside and the appeal stands allowed.

17. Therefore, we set aside the confirmed demand of Rs.1,59,879 on account of CENVAT denial on welding electrodes and allow the appeal.

18. In the result, the impugned order gets set aside and the appeal stands allowed. The appellant would be eligible for consequential relief, if any, as per law.

(Order Pronounced in Open court on 19.09.2025)

Author Bio