Case Law Details

Dinesh Prasad Vs Commissioner of Customs (CESTAT Kolkata)

Conclusion: Where the Revenue failed to establish the foreign origin or smuggled nature of seized gold through independent, scientific, or legally admissible evidence, the statutory presumption under Section 123 could not be invoked solely on suspicion. Untested statements recorded during investigation could not override contemporaneous documentary evidence in the absence of compliance with Section 138B of the Customs Act. Accordingly, confiscation of the gold and consequential penalties under Sections 112 and 114AA were set aside.

Held: Appellants challenged an order directing the absolute confiscation of two gold bars weighing 1,758.390 grams under Sections 111(b) and 111(d) of the Customs Act, 1962, along with penalties under Sections 112 and 114AA. Revenue alleged that the gold was of smuggled origin and relied primarily on statements recorded during investigation under Section 108 of the Customs Act, contending that the supporting purchase and melting invoices produced by appellants were fabricated. Appellants, however, produced contemporaneous purchase invoices, melting invoices, stock registers, and stock summaries evidencing lawful procurement and subsequent melting of the gold. They further contended that the seized gold bore no foreign markings, was intercepted during local transportation, and that the Department had failed to conduct any scientific, forensic, or metallurgical examination linking the seized gold to foreign origin or establishing forgery of the documents. Appellants submitted that the statutory presumption under Section 123 of the Customs Act could not be invoked merely on suspicion when the seizure was unsupported by evidence indicating foreign origin. They argued that their documentary evidence established a complete chain of lawful acquisition and that the Department had neither disproved the authenticity of the records through forensic investigation nor complied with the mandatory safeguards under Section 138B before relying upon third-party statements. They also contended that the alleged confessional statement of the carrier was disputed and lacked independent corroboration. Revenue contended that the seized gold was smuggled and that the statements recorded during investigation established fabrication of the purchase and melting invoices. It argued that the documentary evidence produced by the appellants was unreliable due to discrepancies in purity and that the statutory presumption under Section 123 shifted the burden upon the appellants to prove lawful possession. Tribunal held that the absence of foreign markings, the local nature of the interception, contemporaneous commercial records evidencing lawful procurement, and the absence of any scientific or forensic material linking the gold to foreign origin collectively created substantial doubt regarding the very foundation for invoking Section 123 of the Customs Act. Revenue failed to establish that the statutory presumption could be validly invoked merely on suspicion. Tribunal further held that the Department’s reliance on statements recorded during investigation was legally unsustainable as the mandatory safeguards under Section 138B had not been followed. Allegations of forgery were unsupported by handwriting examination, forensic analysis, expert opinion, or any other independent evidence. Mere untested statements could not displace contemporaneous documentary records. Since Revenue failed to establish the smuggled character of the gold through legally admissible and cogent evidence, the order of confiscation was unsustainable. Consequently, the penalties under Sections 112 and 114AA, being consequential in nature, also could not survive.

FULL TEXT OF THE CESTAT KOLKATA ORDER

The present appeals have been filed by Shri Dinesh Prasad (hereinafter referred to as the “appellant no. 1”) and Shri Raj Kumar Soni (hereinafter referred to as the “appellant no. 2”) against the Order-in-Appeal No. KOL/CUS(CCP)/DC/221 & 222/2026 dated 30.03.2026 passed by the Ld. Commissioner of Customs (Appeals), Kolkata, whereby the order of absolute confiscation of the gold in question has been upheld and penalties have been imposed upon the appellants under the provisions of the Customs Act, 1962.

2. Briefly stated, specific intelligence was received by the officers of the Directorate of Revenue Intelligence (DRI), Kolkata Zonal Unit, that one person, by name, Shri Dinesh Prasad of Ballia, Uttar Pradesh (appellant no. 1 herein) would be carrying a substantial quantity of foreign-origin gold while travelling from Kolkata to Ballia by Train No. 13121 (KOAA–GCT Express) on 17.07.2022. Acting thereupon, the officers of the DRI proceeded to Kolkata Railway Station along with two independent witnesses. The intelligence further indicated that Shri Dinesh Prasad would be travelling in Coach No. S-3, Seat No. 51 of the said train. At about 7:40 p.m. on 17.07.2022, the officers boarded Coach No. S-3 of the train stationed at Platform No. 1 of Kolkata Railway Station and located Shri Dinesh Prasad occupying Seat No. 51. Upon being questioned regarding possession of any contraband articles, he was informed of his legal right to be searched before a Gazetted Officer. At his request, considering that the train was shortly to depart and that the railway platform was not conducive for conducting detailed search proceedings, he was served with summons under Section 108 of the Customs Act, 1962 requiring his presence at the office of the DRI, Kolkata Zonal Unit for completion of the search proceedings.

3. Upon reaching the office of the DRI, Kolkata Zonal Unit, the officers conducted the personal search of Shri Dinesh Prasad in the presence of independent witnesses and a Gazetted Officer. During such search, two rectangular yellow metal bars wrapped in carbon paper, newspaper and adhesive tape were recovered from the person of Shri Dinesh Prasad / appellant no. The appellant no. 1 was unable to produce any documents evidencing the licit acquisition or lawful possession of the recovered gold during the time of query by the said officers.

4. The recovered metal bars were weighed and found to weigh 937.220 grams and 821.170 grams respectively, aggregating to 1758.390 grams. The bars were thereafter examined by a Government Approved Valuer, who opined that they were gold of 24 carat purity, believed to have been obtained by melting gold bars/biscuits, collectively valued at Rs. 89,67,789/-. Representative samples were drawn in the presence of witnesses and, thereafter, the recovered gold bars, the concealment materials, the specially tailored waist belt, the mobile phone recovered from Shri Dinesh Prasad and certain railway tickets were seized under the provisions of the Customs Act, 1962 under the belief that the goods were liable to confiscation.

5. Samples drawn from the seized gold were subsequently forwarded to the Chemical Laboratory, Kolkata for examination. Vide Test Report dated 05.09.2022, the Chemical Laboratory confirmed the samples to be gold of 99.8% purity.

6. During the course of investigation, statements of Shri Dinesh Prasad were recorded under Section 108 of the Customs Act, 1962 on 17.07.2022 and 18.07.2022. Thereafter, considering the circumstances emerging during investigation, Shri Dinesh Prasad was arrested under Section 104 of the Customs Act, 1962 and produced before the jurisdictional Magistrate.

7. Subsequently, one Shri Raj Kumar Soni, Proprietor of M/s. R.S. Jewellers, Ballia, (the appellant no. 2 herein) addressed a communication dated 26.07.2022 to the Customs authorities claiming ownership of the seized gold. According to him, the seized gold had been lawfully procured by his establishment in the ordinary course of business and had been entrusted to Shri Dinesh Prasad, his employee, for business purposes. In support of such claim, copies of registration documents, stock registers and certain invoices relating to melting of gold were produced and a request was also made for provisional release of the seized gold. In the said letter Shri Soni inter alia stated that, the goods seized in the instant case belonged to M/s. R. S. Jewellers and he was the proprietor of M/s. R. S. Jewellers and was actively involved in purchase and sale of gold ornaments/bullion; that they purchase gold in primary form from various authorized parties and send them to different Karigars for crafting the same into ornaments, that Shri Dinesh Prasad was their employee to whom gold was given for the purpose of delivering it to Kolkata for crafting into jewelleries, that the goods so seized had been legally procured by them. To corroborate his claim, he submitted the following documents.

i. Stock Summary (1st April 2022 – 23rd July 2022)

ii. Stock Item Register (1st April 2022 – 23rd July 2022)

iii. Melting Invoice No. 53 dated 14.07.2022

iv. Melting Invoice No. 54 dated 14.07.2022

7.1. Shri Raj Kumar Soni inter alia further stated that, they were in possession of 1932.570 grams of gold in primary form, that in due course of trade the gold was melted and out of the said 1932.570 grams of gold, 1758.390 grams of gold was handed over to Shri Dinesh Prasad; that Shri Prasad had gone to Kolkata for the assigned task, however due to high exchange rate he was instructed to return to Uttar Pradesh with the said gold, that while returning from Kolkata to Uttar Pradesh, he got intercepted by the DRI officials, for which Shri Prasad had failed to produce relevant documents of the said gold. Shri Raj Kumar Soni thus prayed for provisional release of the seized gold in terms of Section 110A of the Customs Act, 1962.

8. In order to verify the aforesaid claim, summons were issued to Shri Raj Kumar Soni and further investigation was undertaken. The investigation included examination of the documents relied upon by the claimant, follow-up enquiries conducted through the jurisdictional officers at Ballia, verification of mobile phone records, examination of the premises of M/s. R.S. Jewellers, verification from the proprietors of M/s. Priyansh Hallmarking & Gold Tunch Centre and M/s. Brij Jewellery, as well as recording of statements of the persons concerned. Enquiries were also undertaken regarding the mobile numbers allegedly connected with the persons referred to during investigation.

9. Upon completion of investigation, the Revenue formed the view that the seized gold was of smuggled origin and that the documents subsequently relied upon by the claimant/appellant no. 2 did not satisfactorily establish lawful acquisition of the seized gold and that the appellant no. 2, in connivance with the appellant no. 1, had attempted to smuggle gold of foreign origin through unauthorized routes and were involved in carrying, transporting and dealing illegally in the same in contravention of the provisions of the Customs Act, 1962. Accordingly, a Show Cause Notice dated 09.01.2023 came to be issued proposing confiscation of the seized gold and allied articles under Sections 111(b), 111(d) and 119 of the Customs Act, 1962, besides proposing penalties upon Shri Dinesh Prasad and Shri Raj Kumar Soni under Sections 112(a)(i) / 112(b)(i) and 114AA of the Customs Act, 1962.

9.1. The said proceedings culminated in the passing of Order-in-Original No. 173/ADC/CC(P)/WB/2024-25 dated 21.03.2025, whereby the ld. adjudicating authority ordered absolute confiscation of the seized gold totally weighing 1758.390 grams, under Section 111(b) and Section 111(d) of the Customs Act, 1962 together with confiscation of the concealment materials under Section 119 of the said Act. Penalties of Rs. 9,00,000/- each were imposed upon Shri Dinesh Prasad and Shri Raj Kumar Soni under Section 112(a)/(b), besides a further penalty of Rs. 9,00,000/- upon Shri Raj Kumar Soni under Section 114AA ibid.

9.2. Aggrieved thereby, both the noticees preferred appeals before the Ld. Commissioner of Customs (Appeals), Custom House, Kolkata, who, vide common Order-in-Appeal No. KOL/CUS(CCP)/DC/221 & 222/2026 dated 30.03.2026, upheld the findings regarding absolute confiscation of the seized gold under the Customs Act, while reducing the penalties imposed under Section 112 of the Act upon Shri Dinesh Prasad and Shri Raj Kumar Soni to Rs.2,00,000/- and Rs.6,00,000/- respectively and also reducing the penalty imposed under Section 114AA on Shri Raj Kumar Soni to Rs.3,00,000/-.

9.3. Against the said order, the appellants have preferred the instant appeals. Customs Appeal No. 75468 of 2026 has been filed by Shri Dinesh Prasad against the imposition of penalty on him under Section 112 of the Customs Act. Customs Appeal No. 75509 of 2026 has been filed by Shri Raj Kumar Soni, challenging the order of absolute confiscation of the gold in question as well as the imposition of penalties on him under Sections 112 and 114AA of the Act.

10. The Ld. Counsel appearing on behalf of the appellants assailed the impugned order and submitted that the findings recorded by the lower authorities are contrary to the materials available on record and suffer from serious factual as well as legal infirmities. It was argued that the authorities below had failed to appreciate that the appellants had, during the course of investigation, produced documentary evidence establishing the lawful acquisition and ownership of the seized gold. In this regard, reliance was placed upon the GST Registration Certificate, PAN particulars, statutory GST returns including GSTR-1 and GSTR-3B and other business records maintained by M/s. R.S. Jewellers. It is argued that these documents sufficiently established that the claimant was engaged in a legitimate jewellery business and regularly dealt with gold in the ordinary course of trade.

10.1. It was further contended that undue emphasis had been placed by the Department on the fact that the relevant invoices and business records were not produced immediately at the time of interception of Shri Dinesh Prasad. It is his contention that mere delayed production of documents cannot, by itself, render otherwise genuine documents fabricated or unreliable, particularly when the same were subsequently furnished before the investigating authorities and formed part of the adjudication record. It was also argued that the genuineness of the documents ought to have been appreciated on their own evidentiary worth rather than on the basis of the stage at which they were produced.

10.2. Furthermore, the Ld. Counsel for the appellants submitted that the statutory burden cast under Section 123 of the Customs Act, 1962 stood duly discharged once the appellants disclosed the source of procurement of the seized gold and produced supporting documentary records identifying the seller and the transactions. It was argued that upon such disclosure, the burden shifted upon the Revenue to affirmatively establish, through cogent evidence, that the seized gold was in fact of smuggled origin. It is pointed out that despite conducting detailed enquiries with the persons from whom the appellants claimed to have procured the gold and despite undertaking extensive investigation, the Revenue has failed to discover any material conclusively demonstrating illicit importation or smuggled origin of the seized gold. In such circumstances, it was submitted that the burden under Section 123 could not be said to have remained undischarged by the appellants.

10.3. He further argued that the very foundation of the seizure under Section 110 of the Customs Act, 1962 was legally unsustainable inasmuch as the requisite “reasonable belief” regarding the smuggled nature of the goods was absent at the time of seizure. Elaborating the submission, it was contended that the seized gold bars did not bear any foreign markings, inscriptions, refinery stamps or other distinguishing features ordinarily associated with imported gold. The subsequent laboratory report merely confirmed the purity of the seized gold as 99.8%, which, according to the learned Counsel, could not by itself justify an inference of foreign origin. It was argued that internationally traded foreign-marked bullion generally possesses a purity of 99.9% and, therefore, the purity report itself militated against the allegation that the seized gold was necessarily of foreign origin. It was also emphasized that the existence of “reasonable belief” under Section 110 must be judged at the precise moment of seizure and cannot be retrospectively supplemented on the basis of subsequent investigation.

10.4. On the evidentiary basis of the proceedings, it was submitted that the Revenue had substantially relied upon the statements recorded under Section 108 of the Customs Act, 1962, particularly those of Shri Dinesh Prasad / appellant no. 1. It was argued that the said statements ceased to possess any independent evidentiary value unless corroborated by reliable and independent evidence. According to the Ld. Counsel for the appellants, the documentary materials subsequently produced by the appellants materially contradicted several portions of the alleged confessional statements, thereby lending credence to the appellants’ assertion that such statements had been recorded under coercion, pressure and duress. It was submitted that a retracted confession, unsupported by independent corroboration, cannot legally constitute the sole foundation for ordering confiscation or imposing penal consequences.

10.5. Moreover, it is contended that the imposition of penalties under Section 112 of the Customs Act, 1962 was wholly unwarranted in the facts of the present case, inasmuch as the Department had failed to establish conscious knowledge or deliberate involvement of the appellants in any act of smuggling. It was argued that the materials placed on record did not satisfy the statutory ingredients necessary for invoking the penal provisions of the Act.

10.6. Without prejudice to the above submissions, the Ld. Counsel specifically challenged the imposition of penalty upon Shri Raj Kumar Soni under Section 114AA of the Customs Act, 1962. It was submitted that the said provision is intended to deal with situations involving the intentional use of false declarations, statements or documents in connection with customs transactions, particularly where such documents are employed for obtaining benefits or facilitating import or export under the Customs Act. According to the learned Counsel, the present case did not involve any such paper or fictitious transactions and the allegation of the Revenue to this extent was false as not backed by any evidence. Consequently, it is contended the essential ingredients for invocation of Section 114AA were wholly absent and the penalty imposed thereunder was liable to be set aside.

10.7. In support of the aforesaid submissions, learned Counsel placed reliance upon the following judicial pronouncements: –

i. Om Sai Trading Company v. Union of India [2020 (372) E.L.T. 542 (Pat.)];

ii. Madhukar Sonaba Bhagat v. Commissioner of Customs (Prev.), West Bengal [2019 (368) E.L.T. 990 (Tri. – )]

iii. Jain & Sons v. Commissioner of Customs [2003 (160) E.L.T 910 (T.)];

iv. Samir Kumar Roy & ors. v. Commissioner of Customs (Prev.), West Bengal [2001 (135) E.L.T. 1036 (T.)];

v. Geetanshu Aggarwala, M/s. Dharmender Kumar Jha & anr. v. Commissioner of Customs (Preventive) [2025 (2) TMI 1291 – CESTAT, Kolkata];

vi. Vikram Kumar Kabra v. Pr. Commissioner of Customs, Hyderabad [2025 (5) TMI 587 – CESTAT, Hyderabad];

vii. Om Prakash Shah. Director of M/s. Quilon Trade Commerce Pvt. Ltd. & ors. v. Commissioner of Customs (Prev.), Kolkata [2025 (5) TMI 1623 – CESTAT, Kolkata]

10.8. In view of the foregoing submissions, the Ld. Counsel for the appellants prayed for setting aside the impugned order in its entirety, with consequential reliefs in favour of the appellants.

11. On the other hand, the Ld. Authorized Representative of the Revenue appearing before us reiterated the findings recorded in the impugned order and submitted that the investigation has conclusively established the illicit nature of the seized gold and the appellants’ conscious involvement in its possession, transportation and attempted concealment. It was contended that the appellants had failed to discharge the statutory burden cast upon them under Section 123 of the Customs Act, 1962 by producing credible and legally admissible evidence establishing the licit acquisition of the impugned gold. The Ld. Authorized Representative further submitted that the documents subsequently relied upon by Shri Raj Kumar Soni, including the invoices purportedly evidencing lawful procurement of the gold, were found to be false during investigation. In this regard, reliance was placed upon the statements recorded under Section 108 of the Customs Act, 1962 from the proprietor of M/s. Priyansh Hallmarking & Gold Tunch Centre and the owner of M/s. Brij Jewellery, which, according to the Revenue, demonstrated that the invoices and supporting records produced by the appellants were fabricated or forged or not in connection with the seized gold.

11.1. In support of the aforesaid submissions, reliance was placed upon the following decisions:

i. Commissioner of Customs (Preventive), Kolkata v. Anil Kumar Soni & Anr. [Judgment dated 31.03.2026 in CUSTA 30 of 2025 with IA No. GA 2 of 2025 (High Court at Calcutta)];

ii. Commissioner of Customs (Preventive), Kolkata v. Rajendra Kumar Damani @ Raju Damani [2024 (389) E.L.T. 444 (Cal.)];

iii. State of Gujarat v. Mohanlal Jitamalji Porwal & Anr. [1987 (29) E.L.T. 483 (S.C.)]

11.2. In view thereof, the Ld. Authorized Representative of the Revenue prayed for dismissal of the appeals by contending that the order directing absolute confiscation of the seized gold, as well as the penalties imposed upon the appellants under the respective provisions of the Customs Act, 1962, are legal, proper and warrant no interference.

12. Heard both sides and perused the documentary evidence placed on record before us.

13. We have carefully considered the rival submissions advanced by both sides, perused the records of the case, the impugned order and the materials placed before us. Upon such consideration, in our considered view, the following issues arise for determination:

(I) Whether, in the facts and circumstances of the present case, the Revenue had entertained a valid and reasonable belief that the seized gold was of smuggled origin so as to justify the seizure and consequent invocation of the statutory presumption under Section 123 of the Customs Act, 1962, or not.

(II) Whether the statements recorded during investigation, forming the principal basis of the Revenue’s case, are legally admissible and sufficiently corroborated so as to sustain the findings of confiscation and penal liability against the appellants, or not.

Issue No. (I): Reasonable belief and burden of proof under Section 123 of the Customs Act, 1962

14. The principal plank of the Revenue’s case rests upon the applicability of Section 123 of the Customs Act, 1962, whereby the burden of proving that the seized gold was not smuggled is sought to be shifted upon the appellants. Before such statutory burden can operate, however, the jurisdictional requirement contained in the provision itself must first stand satisfied, namely, that the goods were seized under the Act on a “reasonable belief” that they constituted smuggled goods. The existence of such reasonable belief is, therefore, not a matter of formality but a foundational fact, the absence whereof would render the statutory presumption incapable of being invoked.

14.1. In the present case, it is an admitted position that the seizure is a town seizure and not one effected at or near an international border, customs station or port of import. Equally significant is the fact that the two gold bars recovered from the possession of appellant Shri Dinesh Prasad were admittedly bereft of any foreign markings, inscriptions, serial numbers or embossments indicative of foreign manufacture or origin. The Panchnama, the Inventory-cum-Seizure Memo and the materials brought on record are conspicuously silent as to the existence of any foreign inscriptions upon the seized gold. Yet, the seizure records proceed to describe the country of origin as “Bangladesh”. Save and except such recital, no independent material has been brought on record explaining the basis upon which the investigating authority could, at the very inception, attribute such an origin to the seized gold. Such a conclusion, unsupported by any contemporaneous objective material, appears to rest more on assumption than demonstrable evidence.

14.2. Before the statutory presumption embodied under Section 123 of the Customs Act, 1962 can be pressed into service, the Revenue is first required to establish the foundational fact, namely, that the goods were seized under a reasonable belief that they were smuggled goods. Such reasonable belief cannot be founded upon conjectures, assumptions or mere suspicion, but must be supported by objective circumstances existing at the time of seizure itself. It is only upon the existence of such foundational facts that the reverse burden contemplated under Section 123 becomes operative. Conversely, where the very foundation of such belief is found wanting, the statutory presumption itself becomes unavailable and the ordinary rule of evidence would govern the matter, thereby requiring the Department to independently establish that the goods were in fact smuggled into India. Applying the aforesaid principle to the facts of the present case, we find that the seizure was effected from a town area and not from any notified border or customs area. More importantly, the impugned gold bars admittedly bore no foreign inscriptions, refinery marks, serial numbers or any other identifying feature suggestive of foreign origin. The Chemical Examiner’s report merely certifies the purity of the seized gold as 99.8%, which, by itself, cannot constitute conclusive evidence of foreign origin, particularly when no material has been brought on record to establish that such purity is exclusively attributable to imported or smuggled gold. In absence of any intrinsic characteristic connecting the seized gold with a foreign source, the mere quantity of gold recovered or the circumstances of possession cannot, by themselves, furnish the reasonable belief contemplated under Section 123 of the Act.

14.2.1. Even assuming for the sake of argument that the initial burden under Section 123 had validly shifted upon the appellants, we find that the said burden stood sufficiently discharged by the claimant/appellant no. 2, namely, Shri Raj Kumar Soni, by placing on record the Registration Certificate, GST documents, stock registers, stock summaries and the melting invoices, thereby furnishing a prima facie explanation regarding the licit acquisition and movement of the impugned gold. Once such documentary evidence was produced, the burden necessarily shifted back upon the Revenue to affirmatively establish that the said documents were fabricated, forged or otherwise unrelated to the seized goods. In the present case, the Revenue has merely relied upon uncorroborated statements recorded during the course of investigation instead of leading independent and legally admissible evidence. Though reliance has been placed upon the statements of certain proprietors to question the genuineness of the documents produced by the appellants, the investigation has not culminated in any forensic examination, expert opinion, prosecution for forgery, or any contemporaneous documentary material conclusively demonstrating that the GST records, stock registers, invoices or business records were fabricated or manipulated. Likewise, despite enquiries conducted with M/s. Brij Jewellery, M/s. Mahalaxmi Dharamkanta and other entities connected with the documentary trail, no substantive material has emerged establishing that the transactions reflected therein were fictitious or that the seized gold could not have emanated therefrom. The Revenue has also not been able to trace any other person linking the impugned gold with any act of illegal importation.

14.3. We also take note of the fact that searches conducted at the residential premises of Shri Dinesh Prasad and at the business premises of Shri Raj Kumar Soni/M/s. R.S. Jewellers did not yield any incriminating material indicative of an organised smuggling syndicate or clandestine dealings in foreign-origin gold. The sweeping allegation contained in paragraph 20 of the Show Cause Notice, describing the present case as part of a “systematic and organised smuggling network”, remains unsupported by any independent evidence whatsoever. Such serious allegations, carrying grave civil consequences, cannot rest upon assumptions or generalized inferences in the absence of cogent material establishing the alleged illegal importation or the participation of the appellants therein.

14.3. We also find substance in the contention advanced on behalf of the appellants that the purity report does not materially advance the Revenue’s case. The Chemical Examiner has certified the seized gold to possess a purity of 99.8%, as already observed hereinbefore, whereas the Revenue has not placed any technical or scientific material demonstrating that such purity, by itself, is indicative of foreign origin or that it constitutes a distinguishing characteristic of smuggled gold. In the absence of any foreign markings or corroborative scientific evidence connecting the seized gold with any foreign source, mere purity of the gold cannot by itself furnish the reasonable belief contemplated under Section 123 of the Act.

14.4. The allegation that the present seizure formed part of a larger organised syndicate engaged in smuggling gold from Bangladesh undoubtedly constitutes a serious charge. However, the gravity of an allegation cannot substitute the legal requirement of proof. Except for the statements recorded during investigation, no contemporaneous material, call data analysis, financial trail, or any other independent evidence has been brought on record to substantiate such allegation. Serious allegations necessarily require equally cogent proof; they cannot be sustained merely on conjecture or investigative suspicion.

14.4.1. In this connection, we find it relevant to refer to the decision of the Hon’ble Patna High Court in the case of Om Sai Trading Company v. Union of India [2020 (372) E.L.T. 542 (Pat.)], wherein it was observed as follows: –

“18. The consignor and the consignee are recorded and are identified. The goods are not seized at any notified custom zone or area. Save and except for what is recorded in the seizure memo, there is no other material available on record. The Learned Additional Solicitor General has tried to supplement the reasons for formation of ‘reason to believe’, which also are on mere suspicion, through the affidavit of the authority. In the light of what is laid down by the Apex Court in Mohinder Singh Gill and Another v. The Chief Election Commissioner, New Delhi and Others, AIR 1978 SC 851, it would be impermissible for the authority to do so. When a statutory functionary makes an order based on certain grounds, its validity must be judged by the reasons so mentioned and cannot be supplemented by fresh reasons in the shape of an affidavit or otherwise, for a bad order, with the passage of time, and supplementing the reasons would become good, which is not how the authorities are required to function, more so, in a case of confiscatory legislation. But assuming hypothetically, accepting the reasons furnished by the officer, even then it is nothing more than a mere suspicion. A general practice in trade cannot be, ipso facto, applied and adopted to the instant case, for unless it is shown that the act and the conduct of the petitioner makes him to be a part and parcel of the trading community, based in the area or dealing with the illegal activities of such like nature. There is no track record of past history of the instant petitioners.”

14.4.2. In Madhukar Sonaba Bhagat v. Commissioner of Customs (Prev.), West Bengal [2019 (368) E.L.T. 990 (Tri. – Kol.)], this Tribunal has held that: –

“11. The allegation is that the appellant has smuggled gold, which is liable for confiscation under Section 111 of the Customs Act, 1962. The gold was not seized while it was being smuggled either at the Port or at the Airport. It was seized from his shop in the City. In such cases, Section 123 of the Customs Act, 1962, provides in respect of the gold and some other notified goods, if the seizure was under reasonable belief, that they are smuggled, the onus of proving that they are not rests upon the person from whom the goods were seized. The first question is whether there was reasonable belief. In this case, we find that the seizure was based on the information that they had received and that the documents pertaining to the gold, were not found in shop at the time of seizure. There is nothing on record to suggest that the pieces which were seized had any foreign markings. Under these circumstances, we find that there was no reasonable belief for the seizure. Further, we find that the appellant had produced various documents to show how he came in the possession of gold and these documents, on investigation, were found to be genuine. It is for this reason that the Ld. Commissioner has refrained from imposing any penalty upon the appellant under Section 114AA of the Customs Act, 1962. Under the circumstances, we find that not only was there no reasonable belief for seizure of the gold and the Currency in the first place, but also that the appellant has satisfactorily explained that the gold and currency which were in his possession. The confiscation of gold and the currency and imposition of penalty upon the appellant under Section 112 of the Customs Act, 1962, are, therefore, not sustainable and the impugned order needs to be set aside and we do so.”

14.4.3. Similarly, an identical issue has been examined in the case of Samir Kumar Roy & ors. v. Commissioner of Customs (Prev.), West Bengal [2001 (135) E.L.T. 1036 (T.)]. The relevant portion of the said order reads as under: –

“Onus as placed under Section 123 was discharged when the appellant produced the sale/purchase vouchers showing the sale of the goods from the gold dealers who admitted having sold the same.”

14.4.3. We have also gone through the case-law relied upon by the Revenue in support of its contentions. However, the factual matrix of the said cases being different from those involved herein, we are of the view that the same are distinguishable on facts and not applicable to the instant case before us.

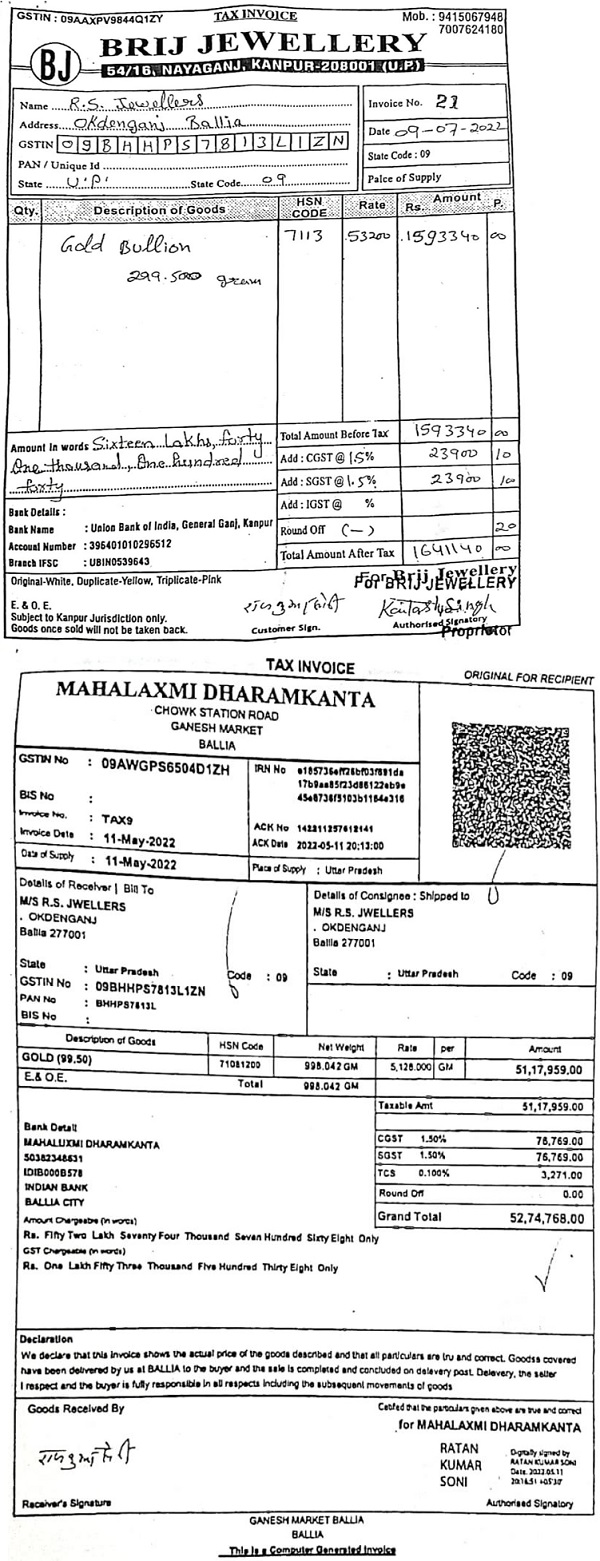

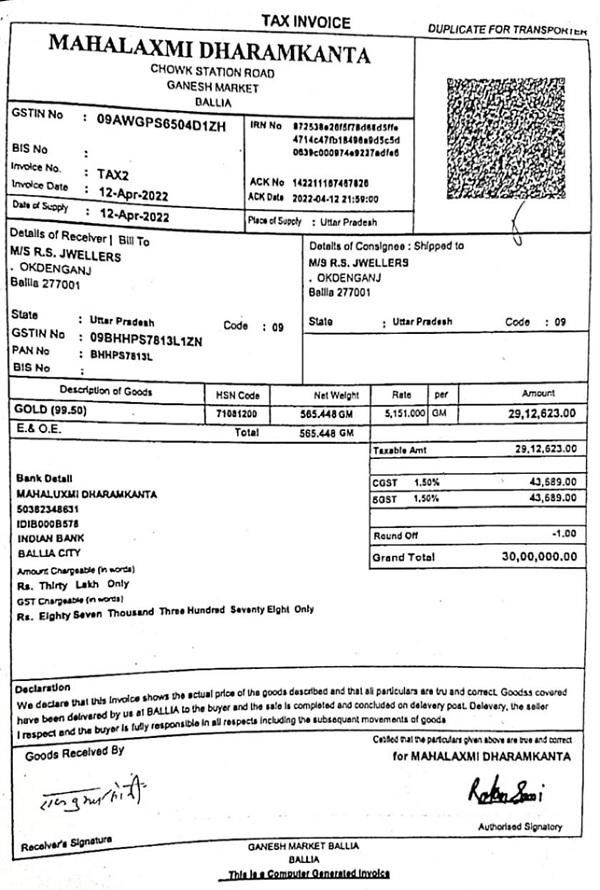

14.5. Another aspect which requires to be examined pertains to the documentary chain sought to be established by appellant No. 2 regarding procurement and subsequent processing of the seized gold. The record reveals that appellant No. 2 had produced purchase invoices evidencing procurement of 299.500 grams of gold from M/s. Brij Jewellery and 565.448 grams and 998.042 grams of gold respectively from M/s. Mahalaxmi Dharamkanta. Significantly, though the proprietors of the aforesaid establishments have expressed reservations regarding the identity of the seized gold, they have not disputed the factum of the underlying transactions reflected in the said invoices. The sales themselves, therefore, stand substantially acknowledged. The appellants have consistently explained that the said gold, after its procurement, was entrusted for melting, which ultimately resulted in the form in which the impugned gold came to be seized. Prima facie, therefore, the documentary evidence demonstrating procurement of the raw gold cannot be brushed aside merely because the Revenue entertains a different inference regarding its subsequent identity. For better appreciation of the said facts, the invoices issued by M/s. Brij Jewellery and M/s. Mahalaxmi Dharamkanta, as placed on record, are reproduced below: –

–

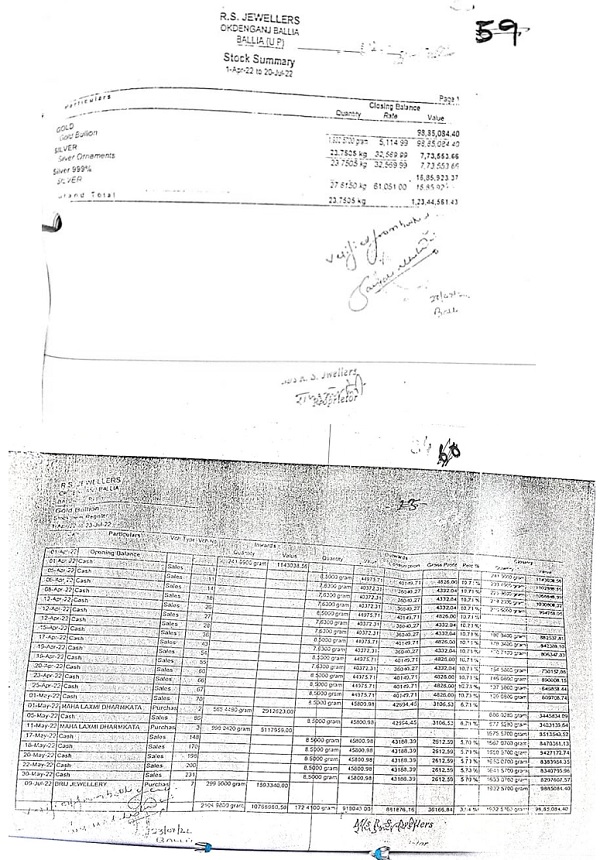

14.5.1. We further find the above documentary evidence produced by the appellants to be consistent with the Stock Summary and Stock Register relied upon by appellant No. 2 duly reflect the aforesaid purchases, which indicate the availability of the corresponding quantity of gold during the relevant accounting period. The same is extracted below: –

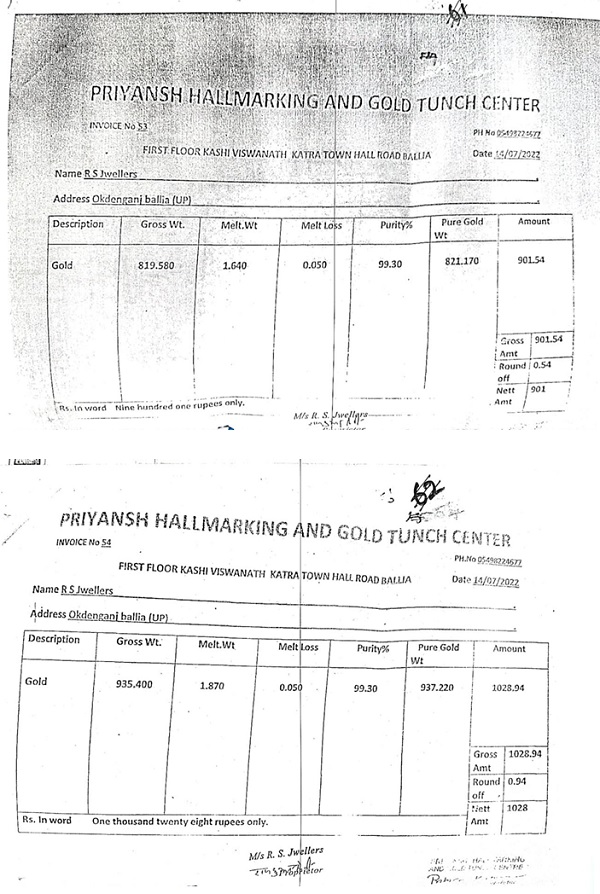

14.5.2. More importantly, the melting process is stated to have culminated in two gold bars weighing 937.220 grams and 821.170 grams respectively, which precisely correspond to the individual weights of the two gold bars recovered and seized by the officers. The aggregate weight reflected in the melting invoices, namely 1758.390 grams, exactly matches the collective weight of the seized gold. Such mathematical correspondence between the contemporaneous commercial records and the seized goods constitutes a relevant circumstance lending prima facie support to the appellants’ explanation, which, in our considered view, cannot be ignored. The said invoices are reproduced below for ease of reference: –

14.6. The Revenue has sought to question the authenticity of the documents furnished by the appellants on the ground that the purity reflected in the purchase invoices allegedly differs from the purity of the seized gold. We are, however, unable to accept such contention as conclusive. The explanation consistently advanced by the appellants is that the gold procured from M/s. Brij Jewellery and M/s. Mahalaxmi Dharamkanta was subsequently subjected to melting before being entrusted to Shri Dinesh Prasad for transportation. Except for the statements recorded during investigation, no independent technical examination, metallurgical opinion or forensic analysis has been undertaken by the Department to demonstrate that the seized gold could not have originated from the gold covered under the aforesaid invoices. In these circumstances, the appellants’ explanation cannot be discarded solely on the basis of suspicion, and the attendant circumstances, viewed cumulatively, persuade us to extend the benefit of doubt in their favour.

14.7. Viewed cumulatively, the absence of foreign markings on the seized gold, the fact that the seizure was effected in the course of a town interception, the absence of any scientific or technical material connecting the seized gold with a foreign source, the production of contemporaneous commercial records by the claimant, and the absence of any independent evidence dislodging the authenticity of those documents, collectively create a substantial doubt as to whether the foundational requirement of a reasonable belief stood satisfied at the time of seizure. Consequently, we are of the considered opinion that, in the peculiar facts obtaining in the present case, the invocation of the statutory presumption under Section 123 of the Customs Act cannot be sustained solely on the basis of suspicion. The burden, therefore, cannot be said to have irrevocably shifted upon the appellants merely by virtue of the seizure itself, and the Revenue was required to establish, through legally admissible and independent evidence, the smuggled character of the impugned gold.

Issue No. (II): Revenue’s reliance on the statements recorded during the course of investigation

15. Having held that the statutory presumption under Section 123 of the Customs Act, 1962 cannot, in the peculiar facts of the present case, be mechanically invoked, we now proceed to examine whether the independent evidence relied upon by the Revenue—principally the statements recorded during the course of investigation— would, by itself, be sufficient to sustain the allegations contained in the impugned order. Upon a careful examination of the record, we find that the Revenue’s case substantially rests upon (i) the statement of appellant No.1, Shri Dinesh Prasad, recorded under Section 108 of the Customs Act, 1962, and (ii) the statements of the proprietors/owners of M/s. Priyansh Hallmarking & Gold Tunch Centre, M/s. Brij Jewellery and M/s. Mahalaxmi Dharamkanta, recorded during investigation, which have been relied upon to contend that the documents submitted by appellant No.2 are forged/fake. The evidentiary worth of these statements, therefore, assumes considerable significance.

15.1. We find considerable substance in the grievance of the appellants that the statements of the proprietors of the aforesaid firms have been relied upon without adherence to the mandatory statutory safeguards prescribed under Section 138B of the Customs Act, 1962, which is in pari materia with Section 9D of the Central Excise Act, 1944. The legislative scheme does not contemplate automatic admission of statements recorded during investigation as substantive evidence against a noticee. The adjudicating authority is first required to examine the maker of such statement as a witness, record its satisfaction regarding admissibility and thereafter afford the affected noticee an effective opportunity to test such evidence through cross-examination. These safeguards are not empty formalities but constitute substantive facets of the principles of natural justice. The record before us does not disclose compliance with the aforesaid mandatory requirements before placing reliance upon the statements in question.

15.2. The Revenue seeks to reject the documentary evidence produced by appellant No.2 almost exclusively on the basis of the statements of Shri Prince Kumar, Proprietor of M/s. Priyansh Hallmarking & Gold Tunch Centre, Shri Kailash Singh, owner of M/s. Brij Jewellery and Shri Ratan Kumar Soni, Proprietor/Authorized Signatory of M/s. Mahalaxmi Dharamkanta. However, these statements have not been subjected to the statutory safeguards embodied under Section 138B of the Customs Act, 1962 and thus such statements cannot, by themselves, be equated with conclusive evidence for discarding the documentary evidence furnished by the appellants in support of their case.

15.3. This aspect assumes greater significance in relation to the allegation that Melting Invoice Nos. 53 and 54 were forged or fabricated. We find that the principal, if not the sole, basis for arriving at such conclusion is the statement attributed to Shri Prince Kumar, proprietor of M/s. Priyansh Hallmarking & Gold Tunch Centre. Except for the said statement, no handwriting examination, forensic analysis of signatures, expert opinion, seizure of original records, comparison of contemporaneous invoice books or any other independent evidence has been brought on record to establish that the said invoices were in fact forged. Suspicion, however grave, cannot substitute legal proof.

In proceedings carrying serious civil consequences, a finding of forgery cannot rest merely upon an untested statement recorded during investigation, without any supporting material capable of independent verification.

15.4. Similarly, we find that the Revenue’s observation regarding the Stock Item Register is founded more upon inference than evidence. Paragraph 20(xi) of the Show Cause Notice merely observes that the Stock Item Register “appeared to have been prepared afterwards.” Such observation, however, is not supported by any expert examination/cogent evidence.

15.5. It is also pertinent to take note of the submissions advanced on behalf of appellant No.1 regarding the circumstances under which his statement under Section 108 of the Customs Act came to be recorded. It has been specifically contended that the statement was electronically typed by the investigating officers and appellant No.1 was merely directed to append his signature without being afforded an opportunity to meaningfully verify its contents, which submission has been recorded at page 28 of the Order-in-Original dated 21.03.2025. Although the said statement could be relied upon in the instant proceedings, the fact remains that once its voluntariness stood seriously disputed, prudence demanded that the Department substantiate the same by leading independent corroborative evidence before placing exclusive reliance thereon. No such corroboration is forthcoming from the record. Therefore, in the peculiar facts and circumstances of the case, we are of the opinion that the said statement of Shri Dinesh Prasad cannot be relied upon so as to conclude as to the foreign character or smuggled nature of the gold in question.

15.6. It is therefore observed that the Revenue’s case rests predominantly upon untested statements recorded during investigation, which are not supported by independent documentary or scientific evidence capable of withstanding judicial scrutiny. The documentary evidence relied upon by the appellants has not been displaced by any cogent material except such statements, while the allegation of forgery itself remains unsupported by any objective investigation.

15.7. For all the aforesaid reasons, we are of the considered opinion that the evidence relied upon by the Revenue does not attain the standard of legal admissibility and probative value necessary to sustain the findings recorded in the impugned orders. The reliance placed upon uncorroborated and procedurally untested statements, creates sufficient doubt regarding the allegations levelled against the appellants. The cumulative effect of the evidentiary deficiencies noticed hereinabove creates sufficient doubt as to the correctness of the Revenue’s case, and such doubt must, in law, be resolved in favour of the appellants.

16. In view of the foregoing discussion and for the reasons recorded hereinabove, we are of the considered opinion that the Revenue has failed to establish the allegations of smuggling by legally admissible and cogent evidence. Consequently, the order directing absolute confiscation of the impugned gold under Sections 111(b) and 111(d) of the Customs Act, 1962 cannot be sustained and is accordingly liable to be set aside.

17. As regards the aspect of imposition of penalty under Section 112 of the Customs Act, 1962, having held that the Revenue has failed to establish, by legally admissible and cogent evidence, that the impugned gold was of smuggled origin and having consequently found the order of confiscation to be unsustainable, the foundation upon which the penalties imposed under Section 112 of the Customs Act, 1962 rest, itself ceases to exist. Penalty under Section 112 is consequential in nature and necessarily presupposes the existence of goods liable to confiscation under the Act. Once the very basis for confiscation fails, the consequential penal liabilities cannot survive independently.

17.1. We are also of the view that the penalty imposed upon appellant No.2, Shri Raj Kumar Soni, under Section 114AA of the Customs Act, 1962 is equally unsustainable. Section 114AA contemplates a deliberate act of knowingly or intentionally making, signing or using a declaration, statement or document which is false or incorrect in any material particular for the purposes of the Customs Act. Such penal provision, being quasi-criminal in nature, necessarily requires the Revenue to establish the requisite element of conscious knowledge and deliberate falsity by cogent and convincing evidence. In the present case, however, the allegation that the documents relied upon by appellant No.2, including the melting invoices and other supporting records, were forged or fabricated, has itself not been established by any independent evidence. As discussed hereinbefore, the Revenue has principally relied upon uncorroborated statements recorded during investigation, nor has any forensic, expert or other objective evidence been brought on record to conclusively establish fabrication of the documents in question. In such circumstances, the essential ingredients necessary for invoking Section 114AA remain unproved.

17.2. Viewed thus, we are of the considered opinion that the Revenue has failed to establish the necessary jurisdictional facts for sustaining the penalties imposed under Sections 112 and 114AA of the Customs Act, 1962. The impugned penalties, therefore, cannot be sustained and are liable to be set aside.

18. In the result, we hold that the order of confiscation of the seized 02 (two) pieces of gold bars collectively weighing 1758.390 grams and the imposition of penalties on the appellants, Shri Dinesh Prasad and Shri Raj Kumar Soni, under Sections 112 and 114AA of the Customs Act, 1962 cannot be sustained and are hereby set aside. Consequently, the impugned order stands set aside.

19. The appeals are allowed, with consequential relief, if any, as per law.

(Order pronounced in the open court on 02.07.2026)