Why this article-:

In general, for a CA, the nature of work is Ascertainment of facts and Apply principles Principles = provisions of various laws, auditing standards, accounting standards, rules regulations etc. (principles).

It is of paramount importance that one should be able to understand the meaning of fact.

Definition of Fact

The word “fact” has been defined the Indian Evidence Act, 1872 has defined following words like:-

-Fact

-Facts in issue

-document

-evidence

-proved

-dis-proved

-Not proved

-Conclusive Proof

The said portion of Act is re-produced below in appendix 1.

“Fact” means and includes–

(1) any thing, state of things, or relation of things, capable of being perceived by the senses;

(2) any mental condition of which any person is conscious.

“Relevant.”

One fact is said to be relevant to another when the one is connected with the other in any of the ways referred to in the provisions of this Act relating to the relevancy of facts.

“Facts in issue.”

The expression “facts in issue” means and includes–

any fact from which, either by itself or in connection with other facts, the existence, non-existence, nature or extent of any right, liability, or disability, asserted or denied in any suit or proceeding, necessarily follows.

Explanation.–Whenever, under the provisions of the law for the time being in force relating to Civil Procedure, 1* any Court records an issue of fact, the fact to be asserted or denied in the answer to such issue is a fact in issue.

Simply going by the definition, we do not end up getting much out of it. Let it be illustrated by way of an example.

Example:

Remuneration paid to wife. One has to prove that her services are worth the amount of remuneration.

1. An Individual is working as immigration consultant.

2. As per the nature of business, he has to attend calls with Indian embassy in foreign countries as per their timing.

3. Obviously, as per Indian Standard Time, many a times, he has to attend calls at late hours in night.

4. He has engaged services of his better half.

5. Being an individual, he cannot get any other person to do the job at 2 am in the night.

Explanation:

1. The portion upto point no 4 are facts. Point no 5 is an argument.

2. Point no 5 cannot be a fact.

3. It is not a law that a proprietor must engage his wife for the job.

4. There are other call centers or other immigration consultants who have to attend the calls at odd hours. They employ other people in shifts.

5. Thus the sentence that “Being an individual, he cannot get any other person to do the job at 2 am in the night” is not a fact but an argument.

6. But many times, the client perceives it as a fact.

7. I can assure you that the process of fact finding is mysterious, fascinating, thrilling and sometimes terrifying.

8. I completely believe in the proverb that “Reality is stranger than fiction”.

9. Highest level of wisdom, imagination suspicion cannot replace a fact as the fact is under no obligation to be linked to logic

Process of Fact Finding

1. It is necessary to explain the importance because, in real life, it really takes pains to identify correct, clear, complete, crispy and precise facts.

One needs to objectively carve out the facts from the facts from the humongous data.

Many a times, there is a challenge to distinguish between a fact and an argument.

It is so because the information available is humongous.

2. That does not mean it is complete. Without fail, it includes irrelevant data.

3. It is clouded by the emotions of the persons involved.

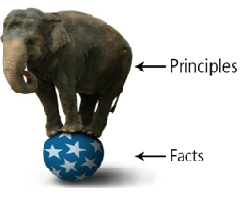

4. It would be apt to demonstrate our perception about importance of facts. We begin with a picture.

Perception of Fact Finding:-

Data/Information given- Expected Outcome-

Importance of Fact:-

1. Though the quantum of facts is small (like the ball), the humongous mammoth of principles (like elephant) can stand only on solid foundation of facts.

2. If the facts are not correct, clear, complete, crispy and precise, the humongous mammoth of principles will not be able to stand.

(i) Mastery of facts is as important as or rather more important than mastery over the law.

(ii) Facts do not cease to exist because they are ignored.

(iii) Every man has a right to his opinion. But no man has a right to be wrong on facts.

(iv) In deed, the presentation and arrangement of facts constitute half the art of exposition.

(v) Further, the truth of a fact has to borne out from irrefutable evidence, in possession of the person.

(vi) In our profession, quoting an incorrect fact is a crime.

(vii) Anyone who knows a strange fact shares in its singularity.

(viii) Blessed is the man who, having nothing to say, abstains from giving us wordy evidence of the fact.

(ix) Comment is free but facts are sacred.

(x) Every fact is related on one side to sensation, and, on the other, to morals.

(xi) Facts are facts and will not disappear on account of your likes.

(xii) Facts are stubborn things; and whatever may be our wishes, our inclinations, or the dictates of our passions, they cannot alter the state of facts and evidence.

(xiii) Facts don’t cease to exist because they are ignored.

(xiv) “Facts are stubborn things, but statistics are pliable.”

(xv) “For every fact there is an infinity of hypotheses. ”

Appendix

The definition of “fact” is given by the Indian Evidence Act, 1872

Relevant extracts of The Indian Evidence Act, 1872

“Fact.”

“Fact” means and includes–

(1) any thing, state of things, or relation of things, capable of being perceived by the senses;

(2) any mental condition of which any person is conscious.

“Relevant.”

One fact is said to be relevant to another when the one is connected with the other in any of the ways referred to in the provisions of this Act relating to the relevancy of facts.

“Facts in issue.”

The expression “facts in issue” means and includes–

any fact from which, either by itself or in connection with other facts, the existence, non-existence, nature or extent of any right, liability, or disability, asserted or denied in any suit or proceeding, necessarily follows.

Explanation.–Whenever, under the provisions of the law for the time being in force relating to Civil Procedure, 1* any Court records an issue of fact, the fact to be asserted or denied in the answer to such issue is a fact in issue.

“Document”.

“Document” 1* means any matter expressed or described upon any substance by means of letters, figures or marks, or by more than one of those means, intended to be used, or which may be used, for the purpose of recording that matter.

“Evidence.”

“Evidence” means and includes–

(1) all statements which the Court permits or requires to be made before it by witnesses, in relation to matters of fact under inquiry; such statements are called oral evidence;

(2) all documents produced for the inspection of the Court; such documents are called documentary evidence.

“Proved.”

A fact is said to be proved when, after considering the matters before it, the Court either believes it to exist, or considers its existence so probable that a prudent man ought, under the circumstances of the particular case, to act upon the supposition that it exists.

“Disproved.”

A fact is said to be disproved when, after considering the matters before it, the Court either believes that it does not exist, or considers its non-existence so probable that a prudent man ought, under the circumstances of the particular case, to act upon the supposition that it does not exist.

“Not proved.”

A fact is said not to be proved when it is neither proved nor disproved.

“May presume.”

Whenever it is provided by this Act that the Court may presume a fact, it may either regard such fact as proved, unless and until it is disproved, or may call for proof of it:

“Shall presume.”

Whenever it is directed by this Act that the Court shall presume a fact, it shall regard such fact as proved, unless and until it is disproved:

“Conclusive proof.”

When one fact is declared by this Act to be conclusive proof of another, the Court shall, on proof of the one fact, regard the other as proved, and shall not allow evidence to be given for the purpose of disproving it.

“Existence of course of business when relevant.”

When there is a question whether a particular act was done, the existence of any course of business, according to which it naturally would have been done, is a relevant fact.

Illustrations:-

(a) The question is, whether a particular letter was dispatched. The facts that it was the ordinary course of business for all letters put in a certain place to be carried to the post, and that particular letter was put in that place are relevant.

(b) The question is, whether a particular letter reached A. The facts that it was posted in due course, and was not returned through the Dead Letter Office, are relevant.

(Author CA. Yogesh S. Limaye can be reached at yogesh@salcoca.com)