Objective

The Author in this article discusses a decision of tribunal (ITAT) regarding taxation of amount paid by companies for broadcasting Cricket World cup matches during FY 2001-02 and 2002-03 held outside India in the hands of a non-resident. The bench has decided that the amount is taxable as royalty in India.

The author is not very sure about the correctness or otherwise of the conclusions reached by the learned bench.

Citation of the case

ADIT v Global Cricket Corporation Pte Ltd., [2022] 145 taxmann.com 570 (Mumbai – Trib.) [14-12-2022]

(The bench has disposed off a batch of related IT appeals and Cross Objections thereof)

Entering the subject

A critical portion of this judgement is based on section 9(1)(vi)(c ) and section 5 of the Indian Income Tax Act, 1961 (the ITA)

Scope of total income.

5. (1) Subject to the provisions of this Act, the total income of any previous year of a person who is a resident includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such year by or on behalf of such person ; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year ; or

(c) accrues or arises to him outside India during such year :

Provided that, in the case of a person not ordinarily resident in India within the meaning of sub-section (6) of section 6, the income which accrues or arises to him outside India shall not be so included unless it is derived from a business controlled in or a profession set up in India.

(2) Subject to the provisions of this Act, the total income of any previous year of a person who is a non-resident includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such year by or on behalf of such person ; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year.

Explanation 1.—Income accruing or arising outside India shall not be deemed to be received in India within the meaning of this section by reason only of the fact that it is taken into account in a balance sheet prepared in India.

Explanation 2.—For the removal of doubts, it is hereby declared that income which has been included in the total income of a person on the basis that it has accrued or arisen or is deemed to have accrued or arisen to him shall not again be so included on the basis that it is received or deemed to be received by him in India.

Income deemed to accrue or arise in India.

9. (1) The following incomes shall be deemed to accrue or arise in India :—

(i)…..

….

(vi) income by way of royalty payable by—

(a) ….; or

(b) ….; or

(c) a person who is a non-resident, where the royalty is payable in respect of any right, property or information used or services utilised for the purposes of a business or profession carried on by such person in India or for the purposes of making or earning any income from any source in India :

Example

1. Consider an example that M/s X of Country X, an architecture firm with ancient structures as domain expertise engages a firm M/s Y of Country Y to advise it whether it is a proper time to enter Indian market.

2. As of the point neither M/s X nor M/s Y has any connection with India whatsoever whether directly or indirectly. Neither Country X nor Country Y has any treaty with India.

3. M/s Y conducts a survey of Indian market based on information available on internet and gives a report that it is not an opportune movement to enter Indian market. M/s X accepts the advice and pays the consultancy charges.

What are the obligations of M/s X and M/s Y under the ITA? Please treat this as question of law and not the practical view as to how the Indian Revenue Services will come to know this transaction etc.

Observations about the Example

Decision taken by M/s X of not entering Indian market may qualify “for the purposes of making or earning any income from any source in India”.

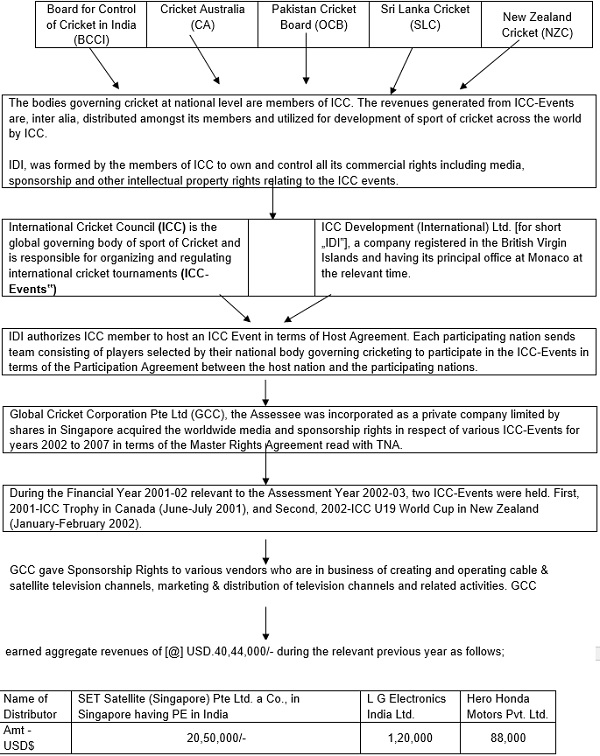

Facts of the case

Cricket regulating body(ies) of respective countries

@ -The figures for other AY are enormously huge as compared to above.

Questions framed and Answers

Main question

| Whether the sum of USD$ 40,44,000/- is chargeable to tax in India under the Income Tax Act, 1961 (the ITA), If yes, the manner of taxation thereof.(the quantum is much more for other AY) | Yes. |

Ancillary Questions

|

a) Whether GCC is eligible for India-Singapore Treaty benefit (the treaty) b) Whether the article 24(1) of the treaty will come into play to deny the benefit c) Whether GCC has any Permanent Establishment in India d) If yes, whether the income is chargeable to tax in India as Business Income e) Whether article 12(7) of the treaty is exhaustive in nature f) Whether the above mentioned income will be chargeable under article 12 as royalty? g) Whether the meaning of the word “arise” in the article 12 of DTAA is to be given an expansive meaning as per domestic law including the deeming provisions thereof? |

Yes

No No N.A. No Yes Yes |

Adjudication by AO and CIT(A) in brief

The Assessing Officer had denied GCC the benefit of the provisions of DTAA. The CIT(A) overturned the decision of Assessing Officer by holding that the benefit of provisions of DTAA would be available to GCC since the provisions of Article 24 of DTAA would not be attracted.

The CIT(A), thereafter, proceeded to conclude that the income received by GCC from SET did not “arise” in India since the provisions of Article 12(7) of DTAA were not attracted.

The CIT(A) did not hold that income arose in India in terms of Section 5 of the Act as the CIT(A) only referred to Section 9(1)(vi)(c) of the Act. Section 9 of the Act only deals with income which is „deemed to accrue or arise‟ in India and, therefore, even as per CIT(A) royalty income did not arise in India in terms of Section 5 of the Act.

Arguments of both the parties

|

Revenue’s view |

Assessee’s View |

| The royalty income from SET arose in India as per Article 12(2) of DTAA read with Article 3(2) and Section 5 & 9 of the Act.

SET had obtained the rights in respect of the India territory and the matches were telecasted in India from which advertisement and distribution income was earned by SET from India. There existed an intricate web of complex agreements forming part of the same activity which must be read together to construe and determine the effect of such agreements. All the agreements (including the two sponsorship agreements with LGEIL and HH) when read together conjunctively help in appreciating the ‘real’ effect of the agreements. Examined thus, the agreements show that the royalty income arose in India in view of the following: (a) Agreements contained reference to India, Indian territory and Indian Prime Time. Then there were clauses which provide the territory covered by transmission of the ‘Feed’ would include India. As per Schedule 1 of the Heads Agreement, the „„License Fee‟‟ was spread over for the periods from the year 2002 to 2007 with other stipulations like, authorized number of exhibitions, minimum commitment and rights provided therein. (b) As per the production agreement between GCC and the producer (i.e. Octagon CSI Limited), Feed was to be created at the place where match is played. The access to the production team is procured by GCC from the Thought production agreement was not placed on record, but the same was relied upon by both the sides to the extent it was reproduced by the CIT(A) in paragraph 16 of his order disposing appeal for the Assessment Year 2003-04. organizers of the matches (i.e. the various cricket associations who owned/controlled the venues). From the Schedule itself it was evident that at least one match was played in India. Further, as the information available, ICC Championship Trophy was held in India in the year 2006 and as per Schedule 2 to the Heads Agreement, 11% of the total consideration was apportioned to this event. (c) The Heads Agreement makes provision to define, Pay-per-view, terrestrial rights, terrestrial restrictions, telephony rights, video rights and theatrical rights to define how these rights can be exercised. Clearly these rights had nexus with the „Licensed Territory‟ which included India. (d) There was coverage of viewership in the India where SET had a PE which telecasted the matches in India. |

(a) the agreement with SET and GCC granting rights to SET was entered outside India

(b) GCC carried out all its business operations outside India (c) payment and receipt of consideration was outside India (d) the broadcast of matches, which were held outside India, happened from SET‟s broadcasting facility in Singapore (e) mere fact that the signals were downlinked and viewed in India cannot be considered to constitute source of income in India According to Article 12(7) of DTAA payments made from one non-resident to another non-resident would arise in India only when all the following three conditions are satisfied. First, non-resident payer (i.e. SET) should have a Permanent Establishment in India. Second, the liability to pay royalty is incurred in connection with such Permanent Establishment. Third, the royalty is borne by such Permanent Establishment. None of the aforesaid conditions are satisfied in case of payments made by SET to GCC during the Assessment Year 2002-03. The CIT(A) had accepted the aforesaid contention of GCC as the CIT(A) had concluded that the payments received from SET did not have any nexus or connection with the Permanent Establishment of the payer (i.e. SET) in India. Therefore, CIT(A) rightly held that the payments from SET did not arise in India in terms of Article 12(7) of DTAA. Learned Senior Counsel for GCC further submitted that Section 12(7) of the DTAA exhaustively defines the place where royalty arises. Therefore, once the royalty cannot be said to have arisen in India in terms of Article 12(7) of DTAA, royalty income cannot be brought to tax in India. In this regard, the Learned Senior Counsel for GCC relied upon the decision of the Tribunal in the case of Decca Survey Overseas Limited, UK Vs ITO, Ward 12(2), Mumbai 30.01.2006 and the decision of AAR in the case of Jay Shree Tea and Industries Limited: 274 ITR 97.

|

Analysis of issues on hand

The main question is whether the income of GCC is chargeable to tax in India and the main bone of contention was the interpretation of article 12(7) read with article 12(1) and 12(3).

Following are the relevant observations

5.12. In the Section 90(1) of the Act enables the Union of India to enter into the above agreements, conventions or tax treaties with the foreign Governments [hereinafter referred to as „Tax Treaties‟], inter alia, for the purpose of granting relief against double taxation to the residents of such foreign countries having income taxable in India. The Tax Treaties allocate right of taxation between the two Contracting States – the Residence State (i.e. the State of residence of the taxpayer in receipt of income) and the Source State (i.e. the Other Contracting State where income arises). Tax Treaties, generally, do not create a charge on income but merely allocate taxing rights by, inter alia, providing for restricted scope of income and/or beneficial rate of taxation in respect of income chargeable to tax in, both, Residence State and Source State. India has entered into DTAA with Singapore and taxing rights in respect of income in the nature of „royalties‟ have been allocated by Article 12 of DTAA. In Article 12(2) of DTAA the term „arise‟ has been in the context of the „contracting state‟ having right to tax income and not in the context of income or scope thereof. When viewed from this perspective, the expression „Contracting State in which they arise‟ used in Article 12(2) refers to the contracting state having the right to tax (i.e. Source State).

5.13. The meaning as well as purport of term „arise‟ has to be adopted and understood keeping in view the provisions of the Act only. We note that the OECD Model Convention provided the Residence State exclusive right the tax royalty income and therefore, there was no occasion to define the terms „arise‟. However, UN Model Convention departed from this position and provided for sharing of taxing rights in respect of income in the nature of „royalties‟ between the Residence State and the Source State. It provided that the „royalties‟ may also be taxed in Source State and according to the law of the Source State at a rate not exceed the rate agreed upon by the contracting states through bilateral negotiation. Since the benefit was limited to reduce rate of tax in respect of defined royalty income, there was again no occasion to define the meaning of term „arise‟. However, Article 12(3) of DTAA provided a narrower definition of „royalties‟ as compared to the one contained in Explanation 2 to Section 9(1)(vi) of the Act. Therefore, the meaning and purport of „arise‟ as used in Article 12(2) or „arising in a contracting state‟ as used in Article 12(1) of the DTAA would, in our view, flow from the domestic tax law of the contract states only.

5.14. We are not inclined to accept the contention advanced on behalf of GCC that use of term „arise‟ in Article 12(2) of DTAA, when interpreted keeping in view the meaning of term „arise‟ as per the provisions of the Act in view of Article 3(2) of the DTAA, leads to the conclusion that income which is “deemed to arise” in India in terms of Section 9 read with Section 5 of the Act would fall outside the ambit of Article 12(2) of the DTAA. The aforesaid interpretation would, in our view, lead to anomalous situation as explained hereafter. Expression “deemed to arise‟ is absent in, both, Article 12(1) and 12(2) of the DTAA. Article 12(1) and 12(2) of DTAA read as under:

“Article 12 Royalties and Fees for Technical Services”

1. Royalties and fees for technical services arising in a Contracting State and paid to a resident of the other Contracting State may be taxed in that other State.

2. However, such royalties and fees for technical services may also be taxed in the Contracting State in which they arise and according to the laws of that Contracting State, but if the recipient is the beneficial owner of the royalties or fees for technical services, the tax so charged shall not exceed ….”

Para 5.15 para-phrased

5.15. In case proposed meaning of the term “arise” or ‟arising” is accepted, the ambit of the right of State of Residence of the recipient of royalty income to tax such royalty income would get also restricted to income arising in India in terms of Section 5 of the Act as Article 12(1) also does not use the expression “deemed to arise” whereas Section 5 uses the expression “deemed to accrue/arise‟ in addition to „accrues/arises‟.

Thus, depriving the beneficial treatment available in terms of Article 12(1) of the DTAA in respect of income “deemed to accrue/arise” in India in terms of Section 9 read with Section 5 of the Act.

Such income, which is deemed to accrue or arise in India as per the provisions of the Act, would also not be covered by Article 12(2) of DTAA, and therefore, be liable to tax at normal rates as per the provisions of the Act in India.

This would clearly be an anomalous situation.

[Emphasis supplied]

Author’s opinion

The author is in respectful dis-agreement with the underlined portion in para 5.14 supra.

What is expressed by the bench as” an anomalous situation” is perhaps the intention of DTAA in terms of restricting the taxing rights.

It is difficult to read the terms and / or expression “deemed to accrue/arise‟ in addition to “accrues/arises” into the treaty which is not there.