Summary: Environmental, Social, and Governance (ESG) criteria have emerged as vital standards for companies, influencing investment decisions by socially conscious investors. The accountability of the Board of Directors is crucial for integrating ESG factors into business strategies, policies, and organizational culture. Boards must oversee ESG integration by identifying relevant goals, aligning corporate vision with these objectives, and ensuring compliance with regulatory requirements. The role of the Corporate Secretary is significant in this process, as they must monitor sustainability governance trends, advise on best practices, and ensure that sustainability discussions are embedded in Board agendas. The regulatory landscape for ESG compliance is fragmented across various laws, including the Companies Act, and has evolved to include frameworks for ESG Rating Providers. Effective ESG reporting and transparent practices not only fulfill compliance requirements but also enhance corporate reputation. A proactive, rather than reactive, approach to ESG is essential for fostering trust among stakeholders and ensuring long-term success in an interconnected business environment. By advocating for standardized reporting guidelines, companies can enhance transparency and contribute to a sustainable future.

INTRODUCTION

Environmental, social and governance (“ESG”) criteria are a set of standards for a company’s operations that socially conscious investors use to screen potential investments. ESG factors have become increasingly important in the last several years.

As ESG is emerging as important strategy resulting in long term value creation, the role/engagement and the accountability of Board of Directors (“Board”) is substantial in terms of strategies, policies, oversight and its integration into the business.

International Finance Corporation, World Bank Group defines ESG as under:

“ESG as a set of Environmental, Social, and Governance factors considered by companies when managing their operations, and investors when making investments, in respect of the risks, impacts, and opportunities relating to but not limited to:

Environmental issues: Potential or actual changes to the physical or natural environment

(E.g. pollution, biodiversity impacts, carbon emissions, climate change, natural resource use);

Social issues: Potential or actual changes on surrounding community and workers (e.g. health and safety, supply chain, diversity and inclusion); and

Governance: Corporate governance structures and processes by which companies are directed and controlled (e.g. board structure and diversity, ethical conduct, risk management, disclosure and transparency), including the governance of key environmental and social policies and procedures.

The Board and the management in many companies in India and abroad play significant role in ESG matters which is evident from their Annual Report. For example, Companies like Bharti Airtel, Vedanta, Infosys have Board level ESG committees. The terms of reference of these committees include Guiding on ESG Vision and Values, identifying ESG targets, industry specific material ESG issues, identification of ESG risks Mitigation measures, identifying ESG opportunities, Oversight on ESG strategies and goals, ensuring compliance requirements relating to ESG including reporting aspects.

The Board is necessitated to ensure that the organization’s culture is based on ESG commitments and the same is incorporated into the strategies, Risk Management process. There should be follow up mechanism also to measure the progress on various ESG strategies.

THE ACCOUNTABILITY OF THE BOARD ON ESG

The accountability of the Board on ESG may be discussed under the following heads:

1. Integration of ESG into strategy, Policy, Oversight, and the Organization Culture.

The Boards need to have a clear oversight of the notion of sustainability and long-term value creation. They should be able to ask questions around the organization’s ability to transition to lower carbon initiatives, the removal of waste from supply chains, the climate impact on and of the business, and its social and community impact across the value chain and supply systems, amongst others.

Integration of ESG involves:

a) Identification of ESG Goals.

b) Alignment of Vision, Mission and values of the corporates with ESG goals.

c) Alignment of ESG Goals into long-term and short-term strategies.

d) Establishment of ESG oversight mechanism.

e) Policy initiatives on ESG including environmental policy, anti-corruption policy, human rights policy etc.

2. Identification of ESG risks and opportunities

India being one of the most vulnerable countries to climate change, ESG is going to be one of the top risks of the company and the Board of directors are expected to consider the same in their business risk and strategy and into their enterprise risk management system and to monitor and ensure their effective implementation of the same.

ESG strategies also helps is exploring more business opportunities due to extensive stakeholder engagement that also brings corporate trust and reputation. Integrating ESG into enterprise risk management system helps in identifying emerging ESG Risks and mitigation. Investors are considering the sustainable, responsible, and ethical practices of corporations a large when they invest.

3. ESG Reporting

Disclosure under the Companies Act, 2013 and requirements under the Securities Exchange Board of India (“SEBI”) Business Responsibility & Sustainability Reporting (“BRSR”) Framework with respect to role and Accountability of the Board on ESG.

SUSTAINABLE COMPLIANCE:

The regulatory framework related to Environmental, Social and Governance (ESG) is not found in any one piece of legislation but comes under various pieces of legislation, Such as the Environment Protection Act, 1986; the Factories Act, 1948; Air (Prevention and Control of Pollution) Act, 1981; Water (Prevention and Control of Pollution) Act, 1974; Handling and Transboundary Movement) Rules, 2016; Hazardous Waste (Management, Companies Act, 2013 (Companies Act); Prevention of Money Laundering Act, 2002; Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“SEBI (LODR) Regulations, 2015”); Prevention of Corruption Act, 1988; and laws with respect to the payment of minimum wage, bonus, gratuity, welfare activities, health and safety, etc.

Various aspects of ESG are covered under these pieces of legislation in a fragmented manner such as:

Disclosures:

Adequate disclosure helps improve public understanding of the structure and activities of enterprises, corporate policies and performance with respect to environmental and ethical standards, and companies’ relationships with the communities in which they operate.

Corporates must disclose mandatorily under various legislations such as:

- Disclosures under the Companies Act, 2013 and Rules made thereunder;

- SEBI (LODR) Regulations, 2015, and other regulations applicable for Listed Companies;

- Secretarial Standard on Board’s Report-SS-4 (Recommendatory);

- Disclosure under the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 and rules made thereunder;

- Disclosures under other applicable Acts.

The various forms of disclosures required on the part of a corporate board are:

Annual Report:

An annual report is interactive in nature to its shareholders. It intends to brief the shareholders about the key performance angles of the current year. It also demonstrates the growth prospects relative to its industry landscape in order to get shareholders’ attention to the company’s potential for excellence.

Annual reports also give an account of corporate activities, legal highlights and corporate governance arena. In addition, the management discussion and analysis report emphasizes management commentary on risks and concerns of the business.

As per SEBI (LODR) Regulations, 2015, the annual report shall contain the following additional disclosures:

1. Related Party Disclosure

2. Management Discussion and Analysis

3. Corporate Governance Report

4. Declaration signed by the chief executive officer stating that the members of Board of Directors and senior management personnel have affirmed compliance with the code of conduct of board of directors and senior management.

5. Compliance certificate from either the auditors or practicing Company Secretaries regarding compliance of conditions of corporate governance shall be annexed with the Directors’ Report.

The Act requires the Board of Directors to disclose on various parameters about the performance and various other aspects of the company, its major policies, relevant changes in management, future programmers of expansion, modernization and diversification, risk management, board evaluation, implementation of Corporate Social Responsibility, a statement of declaration given by independent directors, Section 134(3)(m) of the Companies Act requires the board’s report to contain details on the conservation of energy.

CORPORATE SOCIAL RESPONSIBILITY:

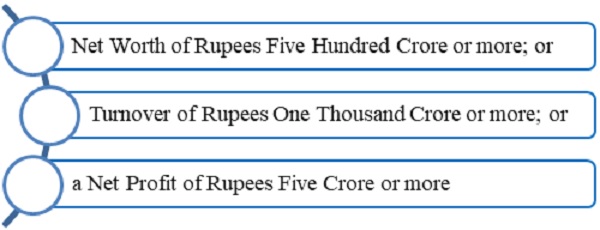

Provisions of section 135 of the Companies Act, 2013 read with Schedule VII of the Act and Companies (CSR Policy) Rules, 2014 provide the broad framework within which the eligible companies are required to formulate their CSR policies including activities to be undertaken and implementation of the same. CSR is a board-driven process, and the Board of the company is empowered to plan, approve, execute, and monitor the CSR activities of the company based on the recommendation of its CSR Committee. The Government has no direct role in the approval and implementation of the CSR programmes /projects of a company.

According to Section 135 of the Companies Act, 2013, every company having –

during the immediately preceding financial year shall constitute a Corporate Social Responsibility Committee of the Board consisting of three or more Directors, out of which at least one director shall be an independent director.

Where a company is not required to appoint an independent director under section 149(4), it shall have in its Corporate Social Responsibility Committee two or more Directors.

The responsibilities of the Board of a CSR-eligible company, inter-alia, include the following:

i. approve the CSR policy;

ii. disclose contents of such policy in its report and also place it on the company’s website, if any;

iii. ensure that the activities included in the CSR policy are undertaken by the company;

iv. ensure that the company spends, in every financial year, at least two per cent of the average net profits of the company made during the three immediately preceding financial years;

v. satisfy itself regarding the utilisation of the disbursed CSR funds; and

vi. if the company fails to spend at least two per cent of the average net profits of the company, the Board shall, in its report made under clause (o) of sub-section (3) of section 134, specify the reasons for not spending the amount and transfer the unspent CSR amount as per provisions of sections 135(5) and 135(6) of the Act.

SOCIAL STOCK EXCHANGE:

The Concept of Social Stock Exchange (“SSE”) was floated in the early part of this century with a view to provide a platform for channelizing investments focusing on social objectives.

In India, the proposal for setting up an electronic fund-raising platform in the form of SSE under the regulatory framework of SEBI was announced in the Union Budget presented in July 2019. The role of SSE as a platform that allows investors to buy shares. in a social enterprise. A SSE, could perform the following functions such as serving as a mediator between social enterprises that need funding and investors who are willing to invest their money, providing investors with procedures for simpler investment in social projects and providing investors with procedures for simpler investment in social projects etc.

Company Secretary (“CS”) is better equipped on structuring of enterprises, registration procedures with the SSE, listing procedures and compliances and will naturally be the preferred professional, as these new opportunities come up in the emerging scenario. Though areas such as impact analysis and social audit are new areas for the CS, the ability of the profession to network and co-ordinate / lead a multidisciplinary team should motivate the CS

SOCIAL AUDIT AND CS AS SOCIAL AUDITOR

The term social audit refers a formal review of a company’s endeavors, procedures, and code of conduct regarding the company’s social responsibility and the company’s impact on society. The objective of social audit is that of accurate identification of requirements, prioritization of developmental activities as per the requirements, proper utilization of funds coupled with conformity of the developmental activity with the stated goals along with quality of service. Since ICSI has come out with ‘Social Auditing Standards’, it has created new opportunities for Company Secretaries as Social Auditor.

SUSTAINABILITY REPORTING

The concept of sustainable development fostered reporting on sustainability as a response of organizations towards growing concerns about environmental degradation and social and ethical issues in business practices. In the late 1980s, the first voluntary environmental reports were published. Companies with environmentally sensitive operations, especially large polluters, started to publish sustainability reporting to showcase their efforts towards sustainable development and Companies with socially sensitive operations started to develop corporate social responsibility (CSR) reporting. The concept evolved over time through the efforts of various organizations, governments, and experts in the fields of sustainability and environmental management.

SUSTAINABILITY AUDIT

A sustainability audit is a comprehensive assessment of an organization’s environmental, social and economic impacts. The purpose of the audit is to identify areas where the organization can improve its sustainability performance and minimize its negative impacts on the environment, society and economy. The audit typically covers areas such as energy use, greenhouse gas emissions, waste management, water usage, product sourcing, supply chain management, employee relations, and community engagement. The outcome of a sustainability audit is used to develop a sustainability strategy and set goals for ongoing sustainability performance improvement.

ESG INVESTMENT

ESG Investing, also known as “socially responsible investing,” “impact investing,” and “sustainable investing” refers to investing that prioritizes optimal environmental, social, and governance (ESG) factors or outcomes. ESG investing is widely seen as a way of investing “sustainably”—where investments are made with consideration of the environment and human wellbeing, as well as the economy. It is based upon the growing assumption that the financial performance of organizations is increasingly affected by environmental and social factors.

It is a blanket term for investments made in firms that adopt ethical practices to make profits. ESG investors don’t invest in stocks of companies that do not meet some of the environmental, social, or corporate governance standards. For instance, chemical companies causing heavy pollution or companies that have poor labor practices. ESG investing has slowly started gaining popularity around the world, as many investment funds have started adopting this model in recent years.

RESPONSIBILITY OF BOARD

Section 166 of the Companies Act casts a duty on a director of a company to act in good faith in order to promote the objects of the company for the benefit of its members as a whole and in the best interests of the company, its employees, the shareholders, the community and for the protection of the environment.

COMPOSITION OF BOARD AND COMMITTEES AS PER COMPANY LAW AND SEBI

Section 149 of the Companies Act requires certain classes of companies to have a Woman Director.

Regulation 17(1)(b) of the Listing Regulations stipulates that one-third of the Board of a listed entity must be composed of Independent Directors if the chairperson is a non-executive director, and not a promoter or related to a promoter, or a person occupying a management position; otherwise, at least half of the board should be composed of Independent Directors.

Regulation 17(1)(a) of the Listing Regulations requires the top 1,000 listed entities (based on market capitalisation) to have an independent, Woman director on their boards.

Section 177 of the Companies Act requires the Board of every listed company and certain classes of public companies to constitute an audit committee consisting of a minimum of three directors, with independent directors forming a majority.

Regulation 18 of the Listing Regulations requires that at least two-thirds of a listed entity’s audit committee members are independent directors; however, in case of a listed entity having outstanding superior voting right equity shares, all members must be independent directors. It also requires that the chairperson of the audit committee be an independent director.

BUSINESS RESPONSIBILITY AND SUSTAINABILITY REPORTING

The Securities and Exchange Board of India (SEBI), i.e., the capital markets regulator, requires business responsibility and sustainability reporting by certain categories of listed entities. While SEBI made it mandatory for the top 100 listed companies by market capitalization to file a business responsibility report (BRR) capturing their non-financial performance across ESG factors back in 2012, in May 2021, it expanded the BRSR and replaced it with a new business responsibility and sustainability report (BRSR) with effect from the fiscal year of 2022–2023. SEBI also made it mandatory for the top 1,000 listed entities by market capitalization to include, in their annual report, a BRSR describing the initiatives taken by the listed entity from an ESG perspective. Recently, through an amendment dated 15 June 2023 to the Listing Regulations and a circular dated 12 July 2023 (BRSR Core Circular), SEBI has introduced a framework commonly referred to as ‘BRSR Core’ and ‘BRSR Core for company’s value chain’. The key aspects of this framework are:

i. BRSR Core, which is a sub-set of the BRSR, consisting of a set of key performance indicators (KPIs)/metrics under nine ESG attributes;

ii. updated format for BRSR after incorporating new KPIs of BRSR Core;

iii. BRSR Core for value chain; and

iv. Assurance requirement for BRSR Core (including value chain). Accordingly, the top 1000 listed entities (by market capitalization) are required to make disclosures as per the updated BRSR format from FY 2023–24, as part of their annual report. The requirement to undertake reasonable assurance of BRSR Core applies only to the top 150 listed entities (by market capitalization) for the current FY 2023–24, and will gradually extend to the top 1000 listed entities by FY 2026–27. The assurance provider should have necessary expertise for undertaking reasonable assurance in the area of sustainability and should not have any conflict of interest. While disclosures for value chain are required to be made by the listed company as per BRSR Core, as part of its annual report, ESG disclosures for value chain and its limited assurance shall become applicable to top 250 listed entities (by market capitalization) on a comply-or-explain basis from FY 2024–25 and FY 2025–26, respectively. The remaining listed entities may voluntarily disclose the BRSR or obtain the assurance of BRSR Core, for themselves or for their value chain.

RESERVE BANK OF INDIA (“RBI”) INITIATIVES

India’s central bank, i.e., the Reserve Bank of India (RBI) has released a ‘Framework for acceptance of Green Deposits’ (Green Deposit Framework) in April 2023 (effective from 1 June 2023), which allows certain RBI regulated entities (REs), i.e., scheduled commercial banks and deposit taking non-banking financial companies including housing finance companies to accept green deposits. Green deposits are interest-bearing fixed deposits denominated in Indian rupees, the proceeds from which are earmarked towards project/activities which yield environment benefits. The RBI has released a list of activities that qualify for the deployment of green deposits as well as a list of excluded activities. To address concerns related to depositor protection and greenwashing, the framework requires entities raising green deposits to have a board approved policy on ‘Green Deposit’ for issuance and allocation of green deposits and a board approved ‘Financing Framework’ for deploying the proceeds and establishing a process for evaluating project viability and assessing the impact of the funds deployed. REs are also required to, on an annual basis, obtain independent third-party verification/assurance for allocation of funds and with the assistance of external firms, undertake impact assessments.

DISCLOSURES RELATING TO ISSUANCE OF ‘GREEN DEBT SECURITIES’

In terms SEBI circular, an entity proposing to issue green debt securities is required to make certain initial disclosures in the offer document for public issues/private placement including: (i) statement on environmental sustainability objectives of the issue; (ii) details of decision-making process followed/proposed to determine the eligibility of projects and/or assets for which the funds are being raised including details of taxonomies, green standards or certifications both Indian and global, if any referenced; (iii) details of the projects/assets/areas towards which the issuer proposes to utilize the proceeds of the issue; (iv) systems in place for tracking the deployment of proceeds; (v) intended types of temporary placement of the unallocated and unutilized net proceeds; and (vi) perceived social and environmental risks and proposed mitigation plan. Further, an issuer who has listed green debt securities must make specified continuous disclosures in its annual report and financials including details of utilization of the proceeds of the issue, unutilized proceeds, qualitative and quantitative performance indicators and underlying assumptions, impact reporting, and major elements of BRSR in the specified format. There are incremental disclosure obligations for transition bonds (as specified by SEBI vide its circular dated 4 May 2023) to facilitate transparency and to ensure that the funds raised through transition bonds are not being misallocated.

ESG RATING PROVIDERS (“ERPs”)

SEBI has introduced a regulatory framework for ESG Rating Providers (“ERPs”) with effect from 4 July 2023 vide an amendment to the SEBI (Credit Rating Agencies) Regulations 1999 (“CRA Regulations”). ERPs, i.e., entities engaged in or proposed to be engaged in the business of issuing ESG ratings, will now need to be registered with SEBI. The CRA Regulations provide the eligibility criteria to qualify for certification, categories of ERPs, disclosure requirements targeted at ensuring transparency and prevention of conflict of interest, etc. SEBI also regulates cross-holdings among ERPs – specifically, ERPs are restricted from holding (directly or indirectly) more than 10% of shares or voting rights in, or having board representation in, another ERP. Similarly, a shareholder holding 10% or more shares or voting rights in an ERP is restricted from holding (directly or indirectly) more than 10% of shares or voting rights in another ERP (this restriction does not apply to holdings by pension funds, insurance schemes and mutual fund schemes). Disclosure norms and procedures for ERPs have also been further clarified by SEBI vide the Master Circular for ERPs dated 12 July 2023 (ERP Master Circular). As per this, ERPs must offer at least six specified rating products including ESG rating, core ESG rating basis third party assured/audited data, transition (parivartan) score for efforts made by the issuer in moving towards net-zero emission goals/ESG goals, and other ESG rating products. An ERP can follow either the ‘subscriber-pays’ or ‘issuer-pays’ business model.

What are the main ESG disclosure regulations?

1. Disclosures by ERPs

In order to ensure greater transparency, the CRA Regulations read with ERP Master Circular, inter alia, requires ERPs to maintain a website and disclose details of ESG ratings, rating rationales and reports, methodology and processes, periodic annual disclosures of average rating transition rates, ESG rating history and movement, general nature of compensation arrangement with clients, whether ratings were solicited or unsolicited, policies for dealing with conflict of interest, etc. Further, in case of listed entities/securities, ERPs are required to promptly disclose the ESG rating assigned and any changes in ESG ratings to the stock exchange(s) where the issuer or the security is listed. Moreover, ERPs are required to appoint a compliance officer who must immediately and independently report any non-compliance to SEBI.-

2. ESG schemes related disclosures

SEBI, vide letters dated 8 February 2022 and 21 June 2022 to the industry body for mutual funds, viz., the Association of Mutual Funds of India (AMFI) has prescribed disclosure norms for ESG labelled mutual fund schemes. These include mandatory disclosures to be made in the scheme information documents relating to objective, asset-allocation, etc., disclosure with respect to engagement and stewardship activities on material ESG issues, maintenance of information related to ESG policy and various aspects of ESG investing on the website, standardisation of ESG scoring process and publication of security-wise score. Further, the recent ESG Mutual Fund Schemes Circular has enhanced disclosure norms and requires mutual funds to disclose the specific strategy in the nomenclature of ESG schemes, reflect security-wise BRSR and BRSR Core score and details of ESG score of the ESG schemes along with name of ERPs in the monthly portfolio statements, disclose the votes cast in investee companies along with rationale for the same on a quarterly basis, disclose a fund manager commentary in the annual report, disclose details of independent reasonable assurance obtained for the ESG scheme in the annual report and disclose certification by board of directors after comprehensive internal audit on the ESG schemes. Separately, to promote consistency, comparability and reliability in disclosures concerning ESG schemes in the International Financial Services Centers (IFSC), the International Financial Services Centres Authority (IFSCA), on 18 January 2023 released a framework for disclosures by fund management entities set up in the IFSC which intend to launch ESG schemes

THE ROLE OF CORPORATE SECRETARY’S ROLE WITH CORPORATE SUSTAINABILITY

The role of Corporate Secretary’s role in Corporate Sustainability is as under:

- Monitor the external environment to remain fully informed of corporate sustainability governance trends, emerging issues and best practices especially those of relevance to the sector or key issues. Inform the Governance Committee on trends and changes in best practice corporate sustainability governance and regulator expectations. Determine and implement amendments to governing documents, processes and structures to incorporate sustainability oversight roles for the Board. Ensure executive and key employees understand the emerging trends in corporate sustainability governance. Along with other executives, ensure the Board regularly reviews, updates, and monitors compliance with corporate sustainability policies.

- The ‘sustainability oversight’ within the Board and Director roles and responsibilities.

- Inform the Chairperson or Committee Chairperson of trends and best practices in corporate sustainability governance.

- Inform the CEO of trends and best practices in corporate sustainability governance, as a shared responsibility with the sustainability prime.

- Include sufficient time for sustainability discussions on regular Board agendas, ideally embedded in all relevant discussions. Ensure meeting packages include sufficient information of sustainability impacts, risks and opportunities, including stakeholder considerations, for the Board to make informed decisions.

- Record Board discussions of sustainability and stakeholder considerations in meeting minutes.

- Support the Board to include diversity as a Board composition factor, increasing the number of women on the Board and greater diversity of skills, ethnicity, cultural background and age. Recommend that sustainability be included in the skills matrix and that at least one Director have skills / experience in corporate sustainability including executives from corporations with a successful track record on sustainability or topic experts.

- Secure time during Board and Committee meetings for education and in-depth review of sustainability risks, opportunities, impacts, trends and dependencies, including stakeholders and their key issues, to ensure the Board has the proper information and knowledge. Include sustainability education sessions in the Board calendar. Identify sustainability education opportunities for Directors.

- Include disclosure on corporate sustainability governance practices in annual and sustainability reports following internationally accepted reporting standards.

- Include sustainability in shareholder communications and ensure effective Board- stakeholder relations.

- Disclose sustainability results at annual general meetings.

CONCLUSION

In today’s interconnected world, it’s more important than ever to prioritize diligent ESG reporting. Taking a reactive approach, where companies only address issues as they arise, is not sustainable in the long run. It can have negative consequences for the company’s reputation and overall success.

Instead, fostering a culture of compliance is key. By proactively integrating ESG reporting into business practices, companies can ensure they are meeting their responsibilities and staying ahead of potential risks. This approach involves not only meeting the compliance requirements of different jurisdictions but also going beyond those requirements to demonstrate a commitment to sustainability and responsible business practices.

While compliance requirements may vary across jurisdictions, there is a global call for standardized reporting guidelines. Having consistent guidelines would not only make it easier for companies to navigate the reporting process but also enhance transparency and comparability across industries and regions. This would facilitate a better understanding of companies’ ESG performance and foster trust among stakeholders.

By embracing standardized reporting guidelines and promoting a culture of compliance, companies can demonstrate their commitment to sustainable practices, build trust with stakeholders, and contribute to a more sustainable and responsible global business environment.

*****

Disclaimer: This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement