Introduction

Immovable property refers to those assets that lack the ability to move from one location to another and are generally fixed at one place. The transfer of immovable property triggers complicated tax considerations. A thorough understanding of the tax laws comes in handy to make informed decisions, manage tax obligations, and ensure adherence to the applicable tax laws.

In the process of acquisition or sale of immovable property, multiple varied issues may arise with respect to TDS (Tax Deducted at Source), Stamp Duty and/or other statutory requirements.

For a detailed explanation, kindly refer to our previous article on “Legal Instruments for Transfer of Immovable Property” which is published on Taxguru.

1. Acquisition of property from a Non-Resident Individual (NRI)

The process of acquiring a property and deduction of TDS in the case of NRI seller is different from those when acquiring from a resident seller.

If the seller of the property is an Indian resident and the consideration exceeds Rs. 50 Lacs, then the buyer is required to deduct TDS and file form 26QB. However, there is no threshold limit for deduction of TDS at the time of acquisition of a property from NRI. Accordingly, TDS has to be withheld in all the transactions involving non-residents sellers.

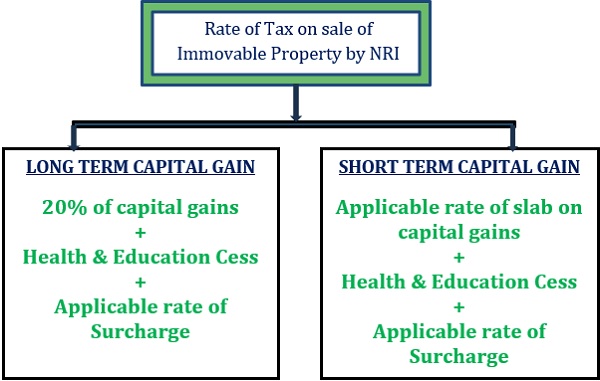

If the seller of a property is NRI, then the buyer is required to deduct TDS at the marginal/highest rate on the entire sale consideration and deposit the same with the income tax department, and file form 27Q within the specified due date.

The below chart represents TDS on Long Term Capital Gains & Short-Term Capital Gains in case of NRI Seller-

When acquiring a property from a Non-Resident, the buyer must possess a TAN (Tax Deduction and Collection Account Number).

The buyer is required to deduct the TDS amount and deposit it in the following month after completing Form 27Q and submitting the TDS return before the filing deadline for that quarter after the TDS is deposited.

2. TDS on sale of property in case of joint owners

When a property is sold, the buyer is required to deduct TDS from the total consideration paid to the seller. In the context of joint owners selling a property, the TDS liability is typically divided among the co-owners in proportion to their ownership share. Each co-owner is responsible for paying taxes on their respective share of the capital gains arising from the sale.

If more than One Buyer or Seller: Challan cum Form 26QB will be filled in by all the buyers for respective sellers for their respective shares.

For Example:

| No. of buyers and sellers | No of Challan and Form 26QB to be filed |

| One Buyer and Two Sellers | 2 |

| Two Buyers and Two Sellers | 4 |

Determining the share of co-owners in the property sold and bought is crucial, as it affects the distribution of TDS payments and tax liabilities.

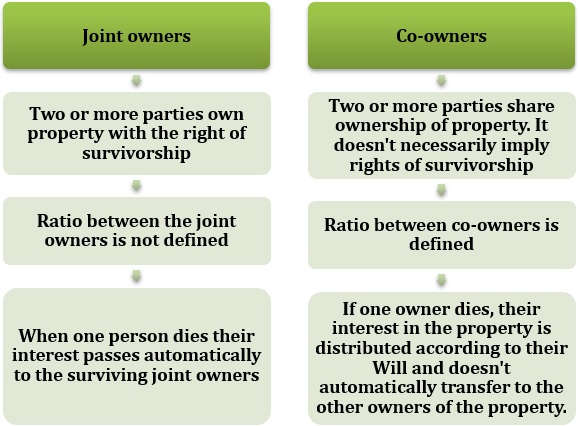

Difference between Joint owners and Co-owners:

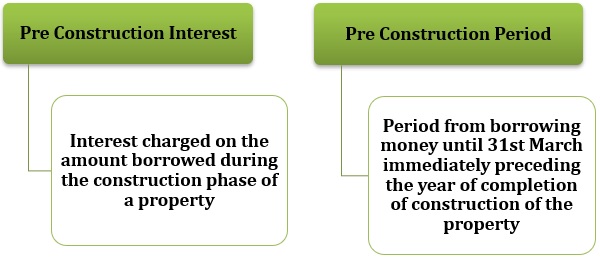

3. Under-construction property and Pre-Construction Interest

Under Construction Property refers to those Properties for which construction has commenced but the construction of such immovable property will be completed after a certain period.

Deduction Under Section 80C

Buyer of the residential immovable property is eligible to claim deductions on the repayment of principal component of construction loan maximum upto Rs. 1.5 lakhs under this Section.

Note: Previous Year(‘P.Y.’).

Deduction of Pre-construction Interest:

The interest allowable as deduction is maximum upto Rs. 2Lakhs per assessment year for a residential property.

Example:

| Particulars | Period |

| Loan Taken on | 1st April 2019 |

| Construction completed on | 1st April 2024 |

| Pre-Construction Interest Period | P.Y. 19-20 to P.Y. 23-24 |

| Post-Construction Interest Period | After P.Y. 24-25 |

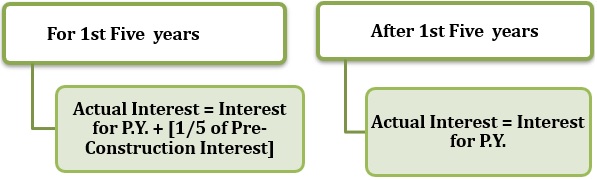

The deduction of pre-construction interest cannot be claimed from P.Y. 19-20 to P.Y. 23-24 in section 24(b) of the Act. However, it can be claimed in 5 equal instalments starting from P.Y. 24-25 in the abovementioned section.

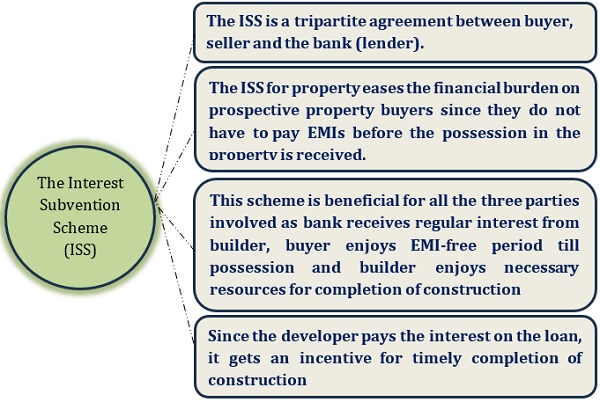

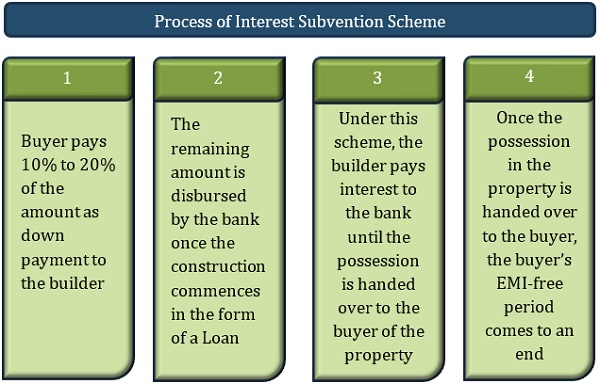

4. The Interest Subvention Scheme

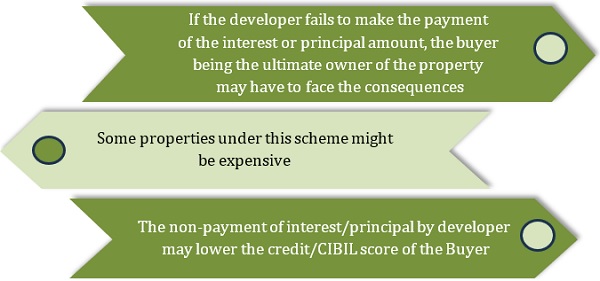

A subvention plan for a home loan also comes with its own set of drawbacks, such as:

5. Determining the date of acquisition

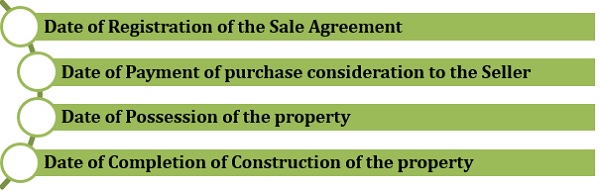

For calculating the period of holding for a house property which date should be taken as the date of acquisition:

There is considerable debate on the date that should be considered as the date of acquisition of a property, where the date of registration is different than the date of possession or the date of completion of payment. Determination of the date of acquisition is prerequisite for claiming of various income tax deductions and exemptions related to immovable properties. There are divergent judicial precedents, depending upon the facts of the case and the underlying documentation. The determination of the acquisition date for a property can be a complex issue with various dates coming into play.

6. Stamp duty on Immovable property

Stamp duty is a tax imposed that will be an additional cost a buyer incurs at the time of purchase of immovable property. The levy of stamp duty is a state subject and thus the rates of stamp duty may vary from state to state.

Stamp duty and Registration charges –

Tax Benefit on Stamp Duty and Registration Charges:

Under Section 80C of the Income Tax Act, 1961 (the Act); the stamp duty and registration charges paid for purchasing a property are eligible for tax deductions. This deduction forms part of the overall limit available under Section 80C of the Act, which includes deductions for other eligible investments like Provident Funds and Equity-Linked Saving Schemes.

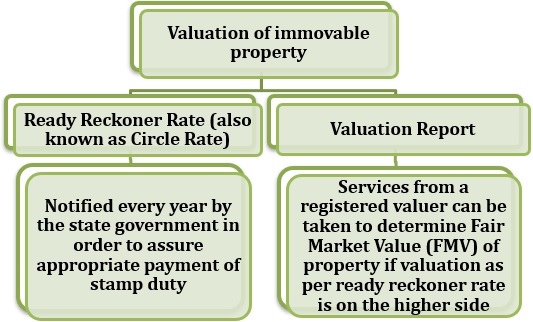

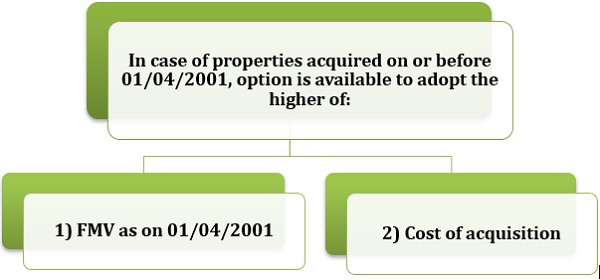

7. Valuation of property

Property acquired prior to 1st April, 2001

Property acquired prior to 1st April, 2001

It is advisable to obtain property valuation of Fair Market Value as on 1st April 2001 from Government Approved and Income Tax Approved Property Valuer at the time of the sale of such immovable property.

Further, it is always advisable to do either of the valuation at the time of sale of the property as well. Any sale of property below the Fair Market Value has very harsh consequences under the Income Tax Act which includes re-opening of assessments, additions of the under valued amount to the income of the buyer or seller and consequent interests and penalties.

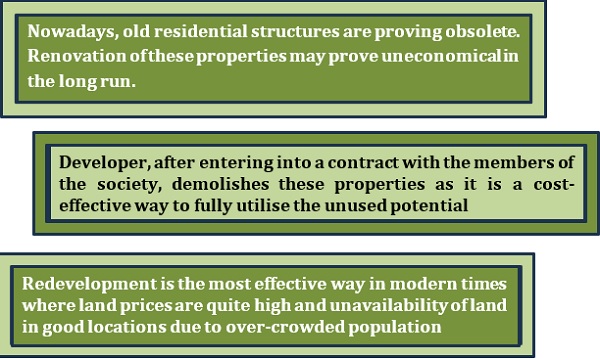

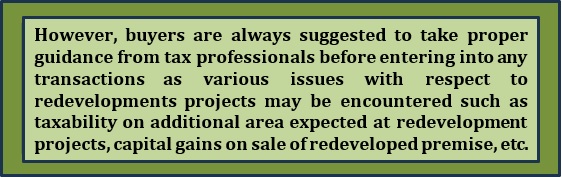

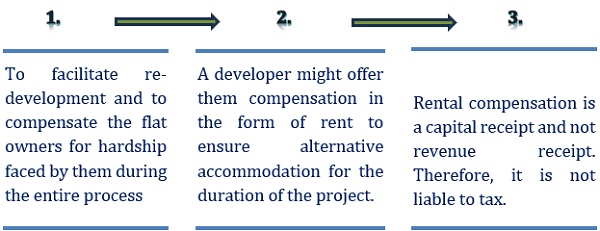

8. Re-development of Immovable Property

Redevelopment is the process where an existing building gets demolished entirely and a new residential premises is developed on the same land. Re-development of residential premises has become quite popular lately, as almost every part of the city/state in India is undergoing through re-development.

Rental Compensation for residential property received from Builder –

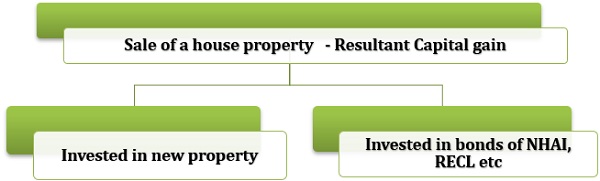

9. Sale of a capital asset and the resultant capital gain invested partially in two different capital assets to claim an exemption

Example:

| Particulars | Amount (In Rs.) |

| Sale consideration of one residential flat | 1 Crores |

| Net capital gain on sale of the above flat | 80 Lakhs |

| Investment made from the above capital gain: | |

| Investment in new property u/s 54 | 50 Lakhs |

| Investment in bonds u/s 54EC | 30 Lakhs |

Yes, it is possible to claim an exemption of capital gain arising from the sale of the same asset under two different sections simultaneously thereby claiming the entire capital gain of Rs. 80 lakhs as deduction. The above scenario might change in case the property in question is a non residential property.

10. Sale of two capital assets and the resultant capital gain invested in one capital asset to claim exemption

Example: Assessee sells one residential house property and any other long-term capital asset, suppose land.

| Particulars | Amount (In Rs) |

| Long-term capital gain from sale of residential house property | 30 Lakhs |

| Net sale consideration from the sale of land | 50 Lakhs |

| Capital gain on sale of Land | 20 Lakhs |

| Investment in new property costing | 70 Lakhs |

Exemption under which section:

Section 54: Entire CG from sale of house property invested in new House Property qualifying for full exemption under this section

Section 54F: Since net consideration from the sale of land is Rs. 50 lakhs and the assessee are investing only Rs. 40 lakhs and therefore proportionate exemption under this section.

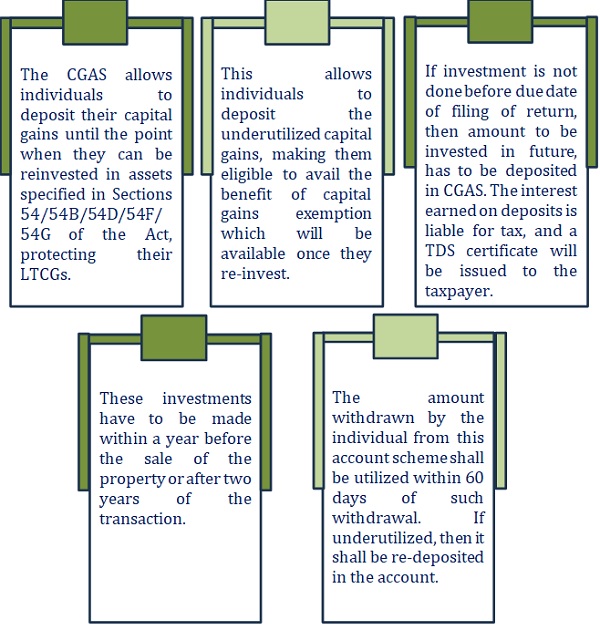

11. Capital Gain Account Scheme (CGAS)

Conclusion:

To ensure a smooth compliance with the income tax laws, it is mandatory for taxpayers to file their return of income before transacting in residential immovable properties.

The outlined points explain the various common issues that may arise at the time of transactions in immovable property. However, the explanations provided above may differ based on alterations in the specifics of each case. Buyers and sellers need to familiarize themselves with the legal framework governing property transactions and the challenges they may face while dealing with immovable property. Therefore, it is recommended to take proper advice from a tax advisor or a professional consultant before entering into such transactions.

****

Authors: Vishal Kothari (Partner), Nitesh Jha (Manager), Sakshi Jain and Anjali Devnath (Associate Consultants). For inquiries contact +91 7977370862.

Author Bio