Introduction

There are majorly two types of trust based on the nature of objects for their establishment and the activities undertaken by them:

- Charitable Trusts are set up for the purpose of undertaking activities such as helping the poor, providing education or healthcare, or preservation of environment etc. People or organizations donate money, property, or assets to the trust.

- Religious Trusts are set up for promoting and advancing the religious activities. These trusts aim to develop and uphold religious belief associated with a particular religion and their main objective is to teach and promote the traditions of a particular religion.

Trusts are treated differently compared to a regular taxpayer in the eyes of income tax laws. The trusts are required to get registered under Section (‘u/s’) 12A of Income Tax Act, 1961 (‘the Act’). The income earned by these trusts are usually exempt from income tax, provided they have an active registration u/s 12A and the exemption is also subject to the fulfilment of certain conditions specified under relevant provisions of the Act.

The due date of filing form 10B/10BB is on or before 30th September after the end of the previous year, pertaining to which the form is being filed i.e. one month prior to the due date of filing the return of income for the respective previous year. All Trusts are required to file audit report in Form 10B/10BB within the time limits prescribed in the Act. If the trust does not file its audit report in the applicable form, the donations received by the trusts during the previous year shall not be eligible for the exemption u/s 11 of the Act.

Trusts are required to get their accounts audited by a certified Chartered Accountant in the prescribed form 10B/10BB. Proper filing and submission of Form 10B/10BB is essential for trusts to comply with the tax regulations for claiming tax exemption.

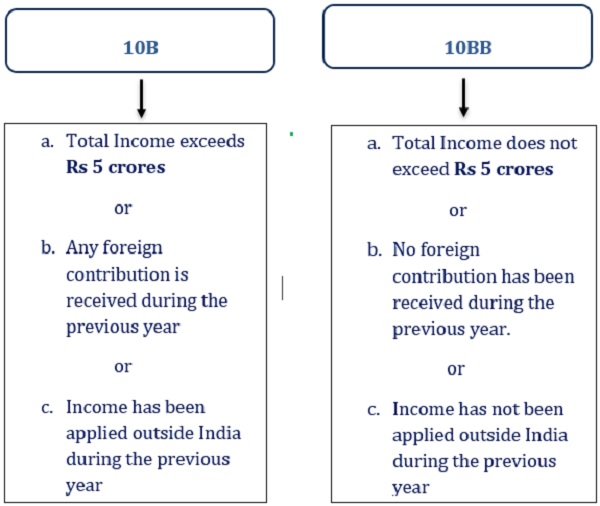

Applicability for form 10B/ 10BB

Clauses in Form 10BB

a. Basic Details (clause 1 to 6) – These clauses require PAN, Name, assessment year, previous year, Registered address & Other Addresses of the trust.

b. Legal (clause 7 & 8) – This clause requires the information about Type of the trust (whether trust is trust/society/company/others) and whether the trust is established under an instrument or not such as a trust deed, will, or similar document.

c. Management (clause 9)– This clause requires the trust to mention the details about the Author/ Society Members/Trustees / Shareholding exceeding 5%/Directors.

d. Registration (clause 10) – This clause requires the details of where the trust has been granted provisional registration or provisional approval, whether activities have commenced during the previous year if yes than date of commencement of activities to be provided.

e. Details of Place where books of account and other documents have been maintained (clause 11) – This clause requires the details of the books of account and other documents have been kept and maintained in the form and manner and at such place as prescribed by the trust.

f. Voluntary contribution (clause 12 to 20) – This clause requires information about whether the trust has filed Form No. 10BD for the previous year. Further, it requires total Sum of donations reported in Form No. 10BD furnished by the trust for the previous year, Donations which could not be reported in Form No 10BD due to non-availability of identification of donor as required under Form No. 10BD, donations received in kind, anonymous donations referred to in section 115BBC (any income of a wholly charitable trust or institution by way of anonymous donation shall be included in its total income and taxed at the rate of 30 %), Any other voluntary contribution not part of Form No. 10BD and total donation not reported in Form No. 10BD.

g. Application of Income (clause 23) – This clause is required to mention the amount of application of income along with amount disallowed from the application.

h. Taxable income (clause 24)- This clause requires to mention the taxable income of the trust on which tax is required to be paid by the trust.

i. Income taxable U/S 115BBI (clause 25)– This clause requires to mention the income taxable U/S 115BBI. Section 115 BBI deals with the taxation of specified Income of the Trust.

j. Anonymous (not specific) donation which is chargeable to tax @ 30 % U/S 115BBC– This clause requires to mention the anonymous donation which is chargeable to tax @ 30 % U/S 115BBC. The trusts are allowed to receive anonymous donation received up to a specified limit. The limit specified in the section is as follows

Higher of the following two amounts:-

- The aggregate anonymous donations in excess of Rs 1 lakh

- 5% of the total donations received

k. Application of income out of different sources (clause 27) – Trust needs to provide information about where income has been applied during the previous year out of the sources like 15% accumulated amount or corpus or borrowed funds

l. Person referred to in 13(3) i.e. deals with the taxation of income received or accrued outside India (clause 28 to 31)

It requires specifying the name of the related person and details whether this asset or property given to the trust is benefiting that specified person or not. If that asset or property is benefitting the specified person in any way then the above income won’t get any exemption. Here the clause also specifies whether the trust has taken any actions for the same.

m. Tax deduction or collection details (Clause 32) Trust needs to mention the amount deducted as TDS or collected as TCS, the section in which TDS is deducted or TCS collected, and the rate at which TDS/TCS is taken.

Difference in Form 10BB and 10B

The following points are included in Form 10B but are not included in Form 10BB:

a) Registration details:

In this clause, the trust needs to provide information about where the trust is registered, date of registration, unique registration No, authority who has granted registration.

b) Object of the trust:

In this clause, the trust needs to mention if there has been any modification in the object which do not match with the condition of registration, date of modification, whether proper application for registration is made within 30 days of modification, date of the above registration, status of such registration and URN of such registration.

c) Advancement of General Public Utility:

In this clause, the trust needs to mention whether any activity/service is being carried on by the trust which is in the nature of trade, commerce, or business, if yes then the percentage of receipt from such activity/service, whether such activity/service in the nature of trade, commerce or business is undertaken in the course of actual carrying out of such advancement of any other object of general public utility.

d) Business Undertaking:

In this clause, the trust needs to mention whether the trust has any business undertaking, If yes then mention the nature of the business undertaking, whether separate books of account have been maintained for the business undertaking, Income from the business undertaking for the previous year which is not to be included in the total income of the trust and income which is to be included now.

e) Business is carried on according to the objects :

In this clause, the trust needs to mention whether the trust has any income being profits and gains from any business.

f) TDS on receipts :

In this clause, the trust needs to mention details of the receipts of the trust on which tax has been deducted at source referred to in section 194C/H/Q/J.

It requires the name/TAN of Deductor, amount on which tax is deducted, amount of TDS.

i) Section 115BBI i.e. how the tax should be treated on income earned by the trust :

Tax should be charged at 30% of the income. Whether income is applied and accumulated for charitable or religious purposes, whether such income accumulated ceases to remain invested or deposited in any of the forms, whether such income accumulated is not utilised for the purpose for which it is so accumulated, whether the trust has any income which is to be included in total income which is chargeable to tax @ 30 % U/S 115BBI

j) Expenditure Incurred for Religious Purposes:

In this clause the trust needs to needs to specify the total income earned and the amount of expenditure done for religious purposes out of total income.

k) Specified Violation:

In this clause, the trust needs to specify the amount of violation. Violations like income not applied for the object of trust, profits and gains of business which is not incidental to the attainment of its objectives, or separate books of account are not maintained by trust in respect of the business which is incidental to the attainment of its objectives, any income applied which is not for the benefit of people, any income applied for a particular religion, trust has not complied with the law.

Conclusion

It is of utmost importance for eligible trusts to file the required audit report accurately and within the stipulated time frame. Failure to do so can have severe repercussions, including the loss of exemption claimed in the Income Tax Return.

Failure to file the form 10B/10BB can result in the loss of tax benefits and exemption for the relevant year. Therefore, trusts seeking tax exemptions must ensure timely and accurate submission of Form 10B/10BB along with the necessary audit report to meet their legal obligations.

*****

Authors:

Vishal Kothari | Partner | Email id: vishal.kothari@bmccorporate.in|Contact Number: 9320614111

Nitesh Jha | Manager | Email id: nitesh.jha@bilimoriamehta.com| Contact Number: 7057907959

Deveshh Gupta | Article Trainee | Email id: deveshh.gupta@bilimriamehta.com | Contact Number: 8657208449

Author Bio