Introduction

In the realm of investments, real estate stands out as a notably secure option when compared to the unpredictable nature of the stock market, the constant fluctuations of cryptocurrencies, and the concerns associated with gold storage and theft. Real estate emerges as a comparatively secure avenue for parking surplus funds. The recent upswing in the real estate sector from 2019 to 2023, attributed to regulatory implementations like RERA (Real Estate Regulation Act), reduced home loan interest rates and demonstrated remarkable resilience. In the intricate landscape of property transactions, understanding the transactions relating to transfer, selling, purchasing or creating an interest in any property, including the change of property title, are governed by several, rules and regulations made by the Central and State Governments. These methods outlined in the Transfer of Property Act, 1882, serve as legally recognized and binding methods for transferring ownership or interest in a property. A transfer, in this context, involves the exchange of ownership or possession from one party to another. Whether tangible or intangible, any property can be transferred by relinquishing rights, interests, ownership, or possession, provided all necessary requirements are met.

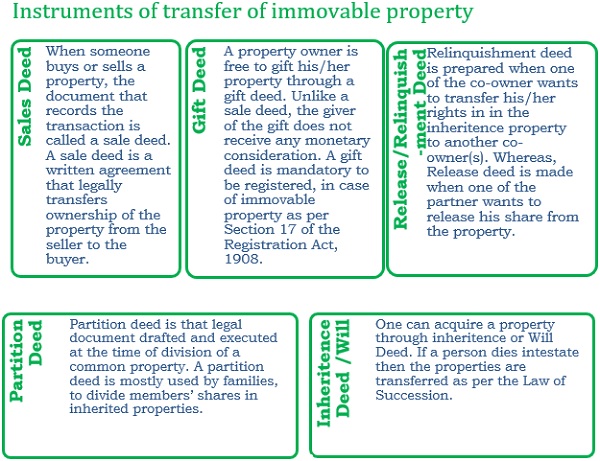

Different instruments for acquiring or transferring Immovable Property

Immovable property can be acquired or transferred from one person to another with the help of following legal instruments:

1. Sale Deed

i. This is the most common way of transferring the property. The registration of sale deed or transfer deed is compulsorily required to be stamped (stamp duty) and once the sale deed is registered in Sub-Registrar office, the ownership gets transferred to the new owner.

ii. Cost:Stamp duty, registration fees, lawyer fees and property taxes may apply. Stamp duty and registration fees can vary depending on the property value and location. For Ex: in Mumbai one has to pay 6% of Property’s market value.

iii. Tax Implications:

a. If you are a seller of the property then you have to pay applicable taxes on Capital Gains.

b. The Registrar of properties will report purchase & sale of all immovable property exceeding Rs 30 Lakh to the Income Tax authorities.

c. If the property worth Rs 50 Lakh or more then purchaser is required to withhold 1% tax deposit at source (TDS).

d. A buyer of property can claim Income Tax exemption on interest payments of up to Rs 2 lakh under section 24(b) and another Rs 1.5 lakh under Section 80C towards the principal repayment.

2. Gift Deed

i. A gift is money or house, shares, jewellery etc. that is received without consideration, or simply an asset received without making a payment against it and is a capital asset for the ‘Recipient’. It can be in the form of cash / movable property / immovable property.

ii. If a person wishes to gift the property to any of his/her blood relative, Gift deed can be used. Once the property is gifted, it belongs to the beneficiary (receiver of gift) and the donor cannot reverse the transfer or even ask for monetary compensation.

iii. Cost: The stamp duty is payable for registering a Gift Deed. The stamp duty on gift deed is generally less than the stamp duty that is applicable for selling the property through a Sale Deed. It can be a cost-effective way of transferring the ownership in a property.

iv. Tax Implications:

a. If a gift, whether movable or immovable, is received by an individual from a relative, no tax will be levied.

b. In the case of a gift received from a non-relative, tax exemption is applicable up to Rs 50,000, however if the gift exceeds this threshold, tax is levied on the entire gift amount considering the stamp duty value of immovable property.

c. As per the provision of taxation of gifts, any Gift received from any person on the occasion of the marriage is not liable to income tax.

d. Gifts received under a WILL or inheritance is tax-exempted.

3. Relinquishment/ Release Deed

i. Legal documents which allow a person to give up, on his or her legal rights over a property to somebody else are known as relinquishment deeds. The person gives up the property with their consent.

ii. In case of a relinquishment deed, it can only be produced for the inheritance of property by the family members and the release of any services. For Ex: when a person dies without any will, and his property is given to his legal heir (suppose two brothers). In case one of the two brothers decide to transfer his rights over the property to his brother due to any reason. In this case, the right to transfer will be known as the relinquishment deed.

iii. A deed which can be enforced towards anyone who has a pure interest in the property, regardless of the fact, whether they are a family member or not. This transfer of deed is known as Release deed. A release deed is used to terminate the existing rights of a person over the certain property.

iv. Cost:The Relinquishment deed and Release deed has to be registered and applicable stamp duty has to be paid. The stamp duty has to be paid only on the portion of the property that is being relinquished and not on the total value of the property.

v. Tax Implications:The tax on capital gains, as applicable in the case of a Sale Deed, is levied solely on the portion of the property that is relinquished by the individual. In case of Release deed, if money is involved, capital gains can arise, which will be taxable.

4. Partition Deed

i. Partition Deed is generally executed by the co-owners of the property (jointly held property) when a court order or order by local revenue authority has to be implemented.

ii. After the division through the partition deed, each member becomes the independent owner of his share in the property and is legally free to sell, rent or gift his asset, according to his wishes.

iii. Cost: The parties involved in the partition, will have to pay stamp duty charges. For Ex: in Maharashtra, 2% of the value of the separated share of the property has to be paid as the stamp duty on a partition deed along with a 1% registration charge.

iv. Tax Implication:After dividing a property by a partition deed, the recipients are not required by the Income Tax Act to pay any capital gains tax.

5. Inheritance Deed/Will

i. An absolute owner of a property is free to give his/her property through a will. It is ideal to register a will to give it legal sanction. Unlike a gift deed, ownership will only pass to the beneficiaries after the passing of the testator or the property’s owner. A will-maker is free to change the will as many times as they like during their lifetime.

ii. After the death of owner of a property his heirs, such as wife, children i.e. male and female, married or unmarried may, as per respective personal law, get the Patta/Khata transferred on production of death certificate of the owner with details of property held by him.

iii. For Ex: if property is house or vacant land in a city/village other than agricultural land — Offices of Corporation, Municipality, Panchayat can be contacted.

iv. Cost: Registration of WILL is not compulsory. Stamp duty charges are not applicable and minimal amount is charged as registration fee as per different state.

v. Tax Implication:

a. When beneficiary receive a property through inheritance deed or WILL, there will be no tax implications.

b. However, if beneficiary re-sells the property, then normal capital gain taxation rules are applicable. The property which is acquired do not cost anything to the beneficiary, but for calculation of capital gain the cost to the previous owner is considered as the cost of acquisition of the Property. Also, the year of acquisition of the previous owner is considered for the purpose of indexation of the cost of acquisition.

In conclusion, the legal instrument depends on the unique circumstances and preferences of the individuals involved. While these instruments facilitate property transactions, it is crucial to recognize the associated legal and tax implications. Transferring property through different agreements provides individual with strategic and controlled method to pass on their immovable property. However, cost of stamp While the process of preparing these agreements involves adherence to legal formalities, the appointment of executors, and consideration of various contingencies, it is an essential tool for transferring immovable property.

Maharashtra Stamp Duty Amnesty Scheme 2023-24

While understanding the different agreements of property transfer deeds is crucial, navigating the nuances of the process can still feel daunting. Fortunately, for homeowners and investors in Maharashtra, the Maharashtra Stamp Duty Amnesty Scheme 2023-24, popularly known as Abhay Yojna, acts as a guiding star, casting its beneficent light on the complex terrain of stamp duty and registration fees. The amnesty scheme was implemented in two phases: the First phase was from 1st December 2023 to 31st January 2024 and the second phase was from 1st February 2024 to 31st March 2024.

The Abhay Yojana provided opportunities for individuals and entities to rectify past lapses in stamp duty payments and penalties on insufficiently paid documents. Whether you’ve inherited a property with pending dues, purchased one without paying the full stamp duty, or simply missed registering a transfer within the stipulated timeframe, the Amnesty Scheme had given a window of opportunity to set things right without facing hefty consequences.

*****

(This article represents the views of authors only and does not intend to give any kind of legal opinion on any matter.)

Authors:

Vishal Kothari | Partner

Jash Shah | Associate Consultant

(Authors can be reached at blogs@bilimoriamehta.com or at +91 98709 25375, +91 99305 98581)

Author Bio