Insolvency and Bankruptcy Board of India

27th August, 2021

Discussion Paper

This discussion paper solicits comments on the following issues related to a corporate insolvency resolution process (CIRP).

A. Code of conduct for Committee of Creditors

B. Restrictions on request for resolution plans and use of swiss challenge in CIRP

C. Treatment of live bank guarantees and line of credit as claims in a CIRP

Part-A: Code of conduct for Committee of Creditors.

This part discusses concerns regarding the functioning of Committee of Creditors (CoC) under the Insolvency and Bankruptcy Code, 2016 (Code) and proposes a code of conduct for creditors and solicits comments on the same.

2. The Insolvency and Bankruptcy Code 2016 envisages market led solutions in the insolvency space driven by professionals and committee of creditors. For realization of optimum results, it is imperative that all the stakeholders driving the process shall be regulated and follow the rules of game threadbare. While other stakeholders i.e., insolvency professionals (IPs), Valuers and Information Utilities (IU) are regulated entities, the CoC functions in an unregulated environment. On several occasions questions have been raised in various fora about the action of CoC being detrimental to objectives of the Code; hence there is an urgent need to device an appropriate mechanism to effectively guide the CoC in its day-to-day functioning.

3. The Code puts in place a creditor-in-control process for insolvency resolution of corporate persons. The composition of the CoC is laid down under sub-section 2 of section 21 of the Code. The CoC comprise of all financial creditors (FCs), except related parties of the CD. The FCs are assigned voting share on the basis of debt owed to them. When the CD has no financial debt or where all FCs are related parties, CoC is constituted with operational creditors. Under the Code, the creditor pursues resolution; evaluates the best resolution plan and circumvents liquidation, to the extent feasible. Creditors of a corporate debtor (CD) act collectively to form a committee which acts in the best interest of all stakeholders. Hence, the CoC is the custodian of public trust during resolution process.

4. The CoC has a statutory role and it discharges a sort of public function. The pain and gain emanating from resolution of the CD are to be shared by all stakeholders with fairness and equity. It must, therefore, apply the highest standard, duty of care, follow due process, be fair to all stakeholders and also act in a transparent manner in discharge of its responsibilities. The IP who conducts the process also performs his duties under the guidance and supervision of the CoC. The role of CoC is vital for timely completion of activities and successful resolution.

5. During a CIRP, the CoC is vested with a duty of trust and care. CoC has to take important decisions on several matters impacting CD and associated stakeholders. The CoC has powers commensurate with its responsibilities. It can decide a haircut of any magnitude to any or all stakeholders required for rescuing the firm; and to seek and choose the best resolution plan from the market, unlike other avenues that allow creditors to find a resolution only from existing promoters. The resolution plan can entail a change of management, technology, or product portfolio or combination of all; acquisition or disposal of assets, businesses, or undertakings; restructuring of organisation, business model, ownership, or balance sheet; strategy of turnaround, buy-out, merger, amalgamation, acquisition, or takeover; and so on, as may be necessary to resolve the stress of the firm. Value maximisation with sustained resolution requires strategies much beyond restructuring of liabilities. This requires tremendous commercial dexterity and acumen on the part of members of the CoC.

6. Judicial pronouncements have clarified the role and responsibilities of the CoC and established the primacy of ‘commercial wisdom of CoC’ in deciding the fate of the CD undergoing corporate insolvency resolution process (CIRP).

6.1 The supremacy of the commercial wisdom of the CoC in financial decisions under the Code is well recognised by the Hon’ble Supreme Court in Re Swiss Ribbons. Commercial decisions of the CoC are left to its collective wisdom.

6.2 The Hon’ble Supreme Court in CoC of Essar Steel India Vs. Satish Kumar Gupta (CA No. 8766-67/2019 & others) has observed that the CoC has to take a business decision based on ground realities by a majority which then binds all stakeholders, including dissenting creditors. The Code envisages an exalted status for the CoC in commercial decision making strictly based on the ground realities and even the Adjudicating Authority (AA) has limited role in approving the resolution plans approved by CoC.

7. The CoC as a body is a new institution and is still evolving to understand its role in the context of value maximization and balancing the interest of all the creditors in market driven insolvency resolution process. In some cases, concerns have been raised by the AA regarding the capacity and conduct of the CoC. Some instances where the conduct of the CoC or some FCs have been under question are given below:

(i) In the matter of M/s. Andhra Bank Vs. Sterling Biotech Ltd. and Ors., absconding and section 29A ineligible promoters attempted to take over the company in the guise of One-Time Settlement with approval of 90.32% vote share of CoC. The NCLT observed: “This also raises doubt about the functionality of the CoC. Such an act of CoC can never be treated as an act of commercial wisdom.”

(ii) In the matter of Bank of Baroda, Vs. Mr. Sisir Kumar Appikatla, & Ors. the AA rejected the resolution plan approved by the CoC on the grounds that the Resolution Plan of resolution applicant was only used as a ploy to gain control of the CD by the very person who had pushed the CD into insolvency. While rejecting an appeal by an FC in the matter the NCLAT observed: “This in itself raises eyebrows. This is further compounded by approval of the Restructuring Plan camouflaged as Resolution Plan emanating from an ineligible person which renders the role of the Committee of Creditors questionable. Such circumstances justify raising of inference of complicity.”

(iii) In the CIRP of Bhushan Power & Steel Ltd., the Resolution Professional paid a fee of about Rs.12 crore for the services of lender’s legal counsel, rendered prior to CIRP and during CIRP. It was recorded in the minutes of the CoC that if the IBBI objects to inclusion of such expenses in insolvency resolution process cost, this amount would be reimbursed by the FCs on a pro-rata basis. Such an arrangement was clearly in contravention of the IBBI’s circular, dated 12.6.2018, which clearly states that IRPC shall not include any legal fee paid to legal counsel of the lenders/creditors. Clearly the RP and CoC deliberately planned for contravening a law.

(iv) In the CIRP of Varrsana Ispat Limited, the lead FC recovered debt during moratorium from the company’s account it was maintaining. In liquidation, even when the company was a going concern and a scheme under section 230 of the Companies Act, 2013 was under consideration, and despite instruction to contrary from the NCLT, the liquidator distributed Rs.26 crore to FCs under their pressure.

(v) Before commencement of CIRP of Gitanjali Gems Limited, an FC decided to engage an entity for services during CIRP. It proposed the name of an IP for appointment as IRP in the application, after having an understanding with him that on his appointment as the IRP, he shall appoint that entity. The IRP appointed the said entity on the date of commencement of CIRP. The fee of entity was 20 times of the fee of the IRP/RP.

(vi) In the case of Shashidhar, MD, Kamineni Steel & Power India Ltd. Vs Kamineni Steel & Power India Ltd. and others (Banks), the AA taking note of delaying tactics by the members of CoC in finalizing/approving resolution plans observed that “functioning of these three banks prima facie do not adhere to the preamble of IBC……………………., therefore functioning of these three Banks in resolving bad loans deserves to be scrutinised by the RBI which is the regulatory authority of the Banks.”

(vii) In this matter of Jindal Saxena Financial Services Pvt. Ltd. Vs. Mayfair Capital Private Limited, there were four financial creditors who attended the first meeting of the CoC. In the said meeting, the CoC did not approve appointment of IRP as RP since two of the four financial creditors, having aggregate voting rights of 77.97% required internal approvals from their competent authorities. The AA observed: “We deprecate this practice. The Financial Creditors/Banks must send only those representatives who are competent to take decisions on the spot. The wastage of time causes delay and allows depletion of value which is sought to be contained. The IRP/RP must in the communication addressed to the Banks/Financial Creditors require that only competent members are authorized to take decisions should be nominated to the CoC. Likewise, Insolvency and Bankruptcy Board of India shall take a call on this issue and frame appropriate Regulations.”

(viii) In the matter of SBJ Exports & Mfg. Pvt. Ltd. Vs. BCC Fuba India Ltd., AA observed that “… An unenviable situation has been created by the conduct of the Members of the CoC. Despite the fact that the Resolution Professional apprised the CoC that the period of 180 days is to expire on 12.02.2018 and sanction be granted for moving an application before the Adjudicating Authority for extension of the period. The CoC has behaved the way we have recorded in the preceding paras.”. It further observed: “A strange phenomenon has developed in so far as the functioning of the CoC is concerned. In a number of cases, it has now been seen that Members of the CoC are nominated by Financial Creditors like Banks without conferring upon them the authority to take decision on the spot which acts as a block in the time bound process contemplated by the Insolvency and Bankruptcy Code, 2016. Such like speed breakers and roadblocks obviously cause obstacles to achieve the targets of speedy disposal of the CIR process.”

(ix) In the matter of Rajnish Jain Vs. Anupam Tiwari RP & others, NCLAT observed that “…it appears that the Resolution Professional has failed to perform his obligation/duty to observe the Code, the Rules and Regulations as enumerated in the Code and CIRP Regulations while conducting CIRP for the reason of taking up such an Agenda of Meeting and leading to illegal Resolution of ousting the BVN Traders from the ‘Committee of Creditors’. Therefore, we are of the considered opinion that the Committee of Creditors was not empowered to adjudicate the issue that has cropped up in the present case, i.e., M/s BVN Traders’ is a ‘Financial’ or ‘Operational’ Creditor. Such adjudication is beyond the scope of consideration of the Committee of Creditors. Further, the Resolution Professional erred to reclassifying the status of a creditor from ‘Financial’ to ‘Operational Creditor’, based on the alleged expert opinion despite that the Adjudicating Authority took a contrary view.”

(x) The AA in the matter of STCI Finance Ltd. through Subash Chandra Modi Vs. Parinee Developers Private Limited, while dismissing the application of RP for withdrawal of CIRP, made observations against CoC for their conduct in postponing the issuance of EOI, Form-G continuously 10 times without obtaining approval for the same from the AA. Further observed that CoC had taken law in to its hands and not complied with applicable provisions of the Code and CIRP Regulations.

(xi) In the matter of INCAB Industries, NCLAT observed that “85… Constitution of the Committee of Creditors violates the proviso to Section 21 (2) of the I & B code 2016 read with 12(3) of CIRP Regulations. Therefore, the Constitution of the creditors’ committee is a nullity in the eye of law that vitiates the entire CIRP. Liquidation is like a death knell for the corporate entity/corporate person. Liquidation based on the resolution of the CoC, which consists of related party Financial Creditors having 77.20 % vote share, is a matter of grave concern. Hon’ble Supreme Court in the case of Phoenix ARC (supra) has described the entering of such related party Financial Creditors in the Committee of Creditors as an act of commercial contrivances through which these entities sought to enter the COC which could affect the other independent Financial Creditors. An order for liquidation of corporate debtor based on the sole decision of related parties Financial Creditors could be fatal for the existence of the corporate debtor, cannot be sustained. It is also pertinent to mention that when the Constitution of the Committee of Creditors itself is found to be tainted, then the decision of that COC cannot be validated on the pretext of exercise of commercial wisdom.”

8. Presently, the conduct and decision making of the CoC is not subject to any regulations, instructions, guidelines etc. Many stakeholders have expressed the need of a code of conduct for the CoC. The thirty second report of the Parliamentary Standing Committee on finance has also recommended the same stating that, “there is an urgent need to have a professional code of conduct for the CoC, which will define and circumscribe their decisions, as these have larger implications for the efficacy of the Code”.

9. The institution of CoC is key to successful conduct and resolution of companies through the Code. It decides the fate of the CD and its commercial wisdom is supreme. The Code has empowered the CoC to choose the best possible resolution from the market and provide for any measure as part of such plan to ensure sustained life of the company. The responsibility comes with accountability. Since the decisions of the CoC impact the life of the firm and consequently its stakeholders, it needs to be fair and transparent in its decisions. However, as discussed above, there have been several issues and apprehensions regarding the conduct of members of the CoC observed. A key step in taking these efforts forward would be to put in place a code of conduct as guidelines for the benefit of participating members in a CoC.

10. International experience

It is observed that internationally there are precedents, whereby, the CoC with the CD are subject to certain rules and regulations for their conduct in the process. In UK, there exist elaborate guidance issued by the Association of Business Recovery Professionals, in conjunction with the Recognized Professional Bodies, on what might be expected of CoC. Similarly, in USA, creditors and other stakeholders play an important role in acting as a watchdog over a debtor’s conduct, and the section 1102 of the US Code places responsibility of interest of those represented by the committee, but not appointed on it, on the members of the committee.

11. Economic Analysis

Since the decisions of the CoC impact the life of the firm and consequently its stakeholders, it needs to be fair and transparent in its decisions. Such power should come with accountability. Specifying a code of conduct will promote transparent working of the CoC and make participating members accountable for their actions during the process. Any attempt by members of CoC to make favourable decision in the interest of any particular (group of) stakeholder(s) would be avoided, thereby ensuring that the principle of fairness is met. It shall also promote higher responsibility to make decisions in the interest of all stakeholders instead of their own self-interests. It will strengthen collective action, which is a fundamental principle underlying the Code.

12. The Board proposes to put in place a code of conduct for CoC that shall elevate accountability and responsibility of CoC to ensure transparency in the functioning of a CoC. A draft is presented in the Annexure. The practice of insolvency and restructuring is complex and varied. It may be difficult to conceptualise and codify every possible situation or scenario. Accordingly, the proposed code of conduct establishes broad principles that can be applied to every situation. It also draws from the ethical norms on which a CoC is expected to function and shall act as the guiding light for the CoC while conducting itself.

13. Public Comments

The Board accordingly solicits comments on the following:

a. Whether a code of conduct should be specified by the Board?

b. Any item of the draft code of conduct placed at Annexure, that should be omitted or modified.

c. Any item that is not part of the draft code of conduct placed at Annexure but should be

Part-B: Request for resolution plans and use of Swiss challenge in CIRP

14. This part deals with the issue related to request for revision of resolution plan (RFRP) multiple times, and submission of unsolicited plans causing delay and uncertainty and the idea of using challenge mechanisms such as the swiss challenge in the CIRP for value maximisation.

15. The Preamble to the Code states that objective relates to reorganisation and insolvency resolution of corporate person for maximisation of value of assets of corporate persons. There are several features in the Code which drive value maximisation. The likelihood of resolution is much higher, if sufficient freedom is provided to the stakeholders in formulation of resolution plans. The explanation inserted to the definition of ‘resolution plan’ under clause (26) of section 5 of the Code clarified that a resolution plan may include provisions for the restructuring of the corporate debtor (CD), including by way of merger, amalgamation and demerger. The Code thus provides sufficient freedom regarding formulation of resolution plans. With the maturity of the insolvency ecosystem, there is need for removal of ambiguities and scope for process innovation.

16. The ‘time boundness’ feature of the Code distinguishes it from the erstwhile insolvency regimes. Section 12 of the Code provides that the CIRP shall be completed within a period of 180 days from the date of admission, with a one-time extension of 90 days permitted by the AA in certain cases. The significance of timeline under the Code cannot be stressed enough. The CD was not in pink of its health when it defaulted and hence required resolution. A very long CIRP period is likely to push the corporate towards liquidation, while reducing its liquidation value. The CIRP, therefore, needs to be completed as quickly as possible.

17. It is also known that there are large costs associated with delay in insolvency process that may have to be borne by all the stakeholders. Further, increased delay in process causes erosion of stakeholder confidence in process.

18. Since the coming into force of the provisions of CIRP, 4541 CIRPs have been initiated till June 30, 2021. Of these, 653 have been closed on appeal or review or settled or others; 461 have been withdrawn under Section 12A; 1349 have ended in liquidation and 396 have ended in approval of resolution plans. As on June 30, 2021, the data pertaining to ongoing CIRPs is as per Table:

Status of CIRPs

| Status of CIRPs | No. of CIRPs | |

| Admitted | 4541 | |

| Closed on Appeal / Review / Settled | 653 | |

| Closed by Withdrawal under section 12A | 461 | |

| Closed by Resolution | 396 | |

| Closed by Liquidation | 1349 | |

| Ongoing CIRP | 1682 | |

| >270 days | 1264 | |

| > 180 days ≤ 270 days | 82 | |

| > 90 days ≤ 180 days | 218 | |

| ≤ 90 days | 120 | |

19. As can be seen, from the Table above, about 1264 CIRPs have breached the Code mandated timeline of 270 days. Further, the average time taken in resolution of 396 CIRPs is 482 days while the average time taken for passing orders for commencement of liquidation in 1349 CIRPs is 362 days. It is evident that there are challenges to adhering to the prescribed timeline. There are several reasons for delays in the CIRP including the repeated requests for expression of interest, continued extension of time for submission of resolution plans, unsolicited revision of submitted plans, repeated negotiations with the resolution applicants, receipt of unsolicited plans etc.

20. Regulation 36B of the CIRP Regulations contain provision regarding request for resolution plans. It provides for a minimum of 30 days for prospective resolution applicants to submit the plans and allows for revision/ modification of the request for resolution plan (RFRP) subject to the 30-day timeline but there is no cap on the number of revisions that may be allowed in a resolution plan. These have the effect of delaying resolution. There are also cases where the resolution applicants revise the resolution plans multiple times, with or without the consent of the CoC, leading to delays in completing the process.

21. The CoC, at many times keeps on entertaining these plans for value maximization. It, however, creates uncertainty about the process and rather places an incentive on the PRAs to offer lesser at the initial stages. If sufficient competition is not achieved in the process, such practice may even lead to less than optimum value for the corporate debtor. Invariably, the delay in the process adds to the costs leads to further destruction of the value of the CD.

Swiss Challenge Method

22. Swiss Challenge is a bidding process, wherein a bidder (original bidder) makes an unsolicited bid to the auctioneer. Once approved, the auctioneer then seeks counter proposals against the original bidder’s proposal and chooses the best amongst all options (including the original bid). The original bidder in most cases is granted the “right to first refusal”. If the original bidder agrees to match its offer to the challenging proposal, the bid is awarded to him, else it is awarded to the challenging bidder. The process is generally used in public procurement.

23. Regulation 39 of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) provides the mechanism for approval of resolution plan by the CoC. Sub-regulation 3(a) provides that the CoC shall evaluate the resolution plans received as per evaluation matrix and thus the said regulation is silent on the exact method to be used for selection of the best resolution plan. Therefore, it is observed that there is no express prohibition on the adoption of Swiss challenge method during a CIRP. The Swiss challenge method has been used by the CoC in the CIRP of M/s. Ruchi Soya Limited, wherein the CoC decided to conduct a Swiss challenge to maximise the asset(s) value.

24. In the Report of the Sub-Committee of the Insolvency Law Committee on Pre-packaged Insolvency Resolution Process1, the sub-committee noted that swiss challenge is a time-tested mechanism and has proven to be highly effective in value maximisation and ensuring transparency of the process. The provisions of the Code and Rules and Regulations thereunder with respect to the Pre-packaged Insolvency Resolution Process (PPIRP) provides for a hybrid method for value maximisation during the resolution process. The hybrid method is inspired from the Swiss challenge with certain modification(s)/improvement(s) necessary for successful implementation under the PPIRP. The hybrid method provides for a resolution plan from CD as base resolution plan and challenging plans are sought from the third-party resolution applicants disclosing the score of the base plan and basis for evaluation. Post receipt of plans, if the bast plan is significantly better than the base resolution plan, the submitter of the base resolution plan losses the right for first refusal. Whereas, if the best alternate plan is not significantly better, the submitters of the best alternate plan and base plan are given multiple chances to outbid each other on an electronic platform. They get multiple chances for improvement until one of the submitters opts out. The said process of improvement is to be closed within a definite time period not exceeding the window provided under law.

Swiss Challenge Method in Banking

25. RBI has on 1st September 2016 issued Guidelines on Sale of Stressed Assets by Banks2. The essence of the Guidelines is urging banks to create mechanism for timely identification of stressed accounts and take appropriate actions to ensure there is low vintage and better price realisation for banks. Under the Guidelines, Swiss challenge method is envisaged to be introduced for sale of stressed assets as well. The banks have also resorted to the Swiss challenge3 to offload their stressed assets under the SARFAESI Act, 2002. Thereafter, RBI has issued Draft Comprehensive Framework for Sale of loan exposures on 8th June 2020 and invited public comments on the same.

Jurisprudence

26. Hon’ble NCLT, Mumbai Bench, in the matter of Bank of Baroda v. Mandhana Industries Ltd., issued directions which are as following:

“…….. they shall proceed in accordance with the directions given in the order, directing the Applicant and R18 to outbid each other in the presence of the Resolution Professional and the CoC at 3 p.m. on 4th July, 2018 and to complete bidding within two hours thereof, then highest value emerged in outbidding in between the Applicant and R18 shall be taken into consideration in addition to the marks already scored on considerations other than bid offers through evaluation matrix already arrived at. Soon after completion of the bidding, the plan through in the bidding process in the light of evaluation matrix earlier prepared, shall be examined by the CoC and put to voting as deferred to 6.7.2018 to be concluded by 7.7.2018 afternoon. It is further clarified that on each round of bid, the difference of bid offer shall not be less than Rs. 10 crores.”

27. The AA thus on an application by one of the resolution applicants expressly ordered the RP to conduct Swiss Challenge under CIRP. It may be mentioned that the applicant emerged as the successful resolution applicant and the resolution plan was approved vide order dated 30th November, 2018.

28. On another instance, Hon’ble NCLT, Mumbai Bench, in the matter of Saket Tex Dye Private Limited v. Kailash T. Shah, held that:

“12. Further, we are of the view that the Swiss Challenge method (usually adopted for Govt tendering process to facilitate the awarding of contract in the second round of bidding to the highest bidder) as suggested by the applicant does not find any place in the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (“CIRP Regulations”), as the CIRP Regulations provide the manner in which the Resolution Plan has to be approved. The applicant herein framed the rule on his own and contended that rule has to be followed by the CoC for approving the resolution plan, disregarding the CIRP Regulations. The method suggested by the applicant, on the guise of maximization of value of Corporate Debtor, is nothing but an auction sale of the Corporate Debtor, where the commercial wisdom of the CoC has to take a back seat.”

29. Hon’ble NCLT rejected the use of Swiss challenge method during the CIRP due to absence of it being expressly provided under CIRP Regulations and the same being proposed by the applicant post approval of resolution plan by CoC.

Proposed Amendment

30. Considering the issues in RFRP and to provide for option for Swiss challenge to the CoC, it is proposed to amend the regulations to provide for:

(i) The RP and CoC to place the RFRP with due consideration of the market conditions.

(ii) The CoC shall decide on allowing for revision of the RFRP, number of such revisions and timelines for the same on ex-ante basis. The number of revisions shall not exceed 2.

(iii) CoC shall decide the timelines within which it will allow for negotiation and changes to the submitted resolution plans

(iv) CoC and RP shall not entertain unsolicited revision to resolution plans.

(v) The CoC shall decide whether it considers appropriate to opt for a swiss challenge method and if the same is decided by the CoC, then it should be provided in RFRP on ex-ante basis.

(vi) The CoC to decide basis for evaluation, timelimit within which the challenge process shall be concluded and the minimum threshold for improvement over the resolution plan on ex-ante basis.

Economic Analysis

31. The proposed amendment would help by allowing additional options to the CoC for resolution of a firm while under CIRP. The cap on number of extensions in RFRP would ensure that the sacrosanct timelines envisaged under the Code is practicable. Further, such an amendment would help instilling faith amongst stakeholders in the corporate insolvency resolution process and prevent potential misuse in absence of any specifications. This would also ensure that the CIRP remains timebound and value obtained is a competitive one and the maximum achievable given the market condition.

Public Comments

32. The Board accordingly solicits comments on the following:

(i) Should there be any restrictions on the number of revisions in the RFRP?

(ii) If, yes, do you suggest any changes in the proposal at Para 30 (ii).

(iii) Should swiss challenge mechanism be available in the CIRP regulations?

(iv) If yes, do you suggest any changes in the proposal at Para 30 (vi).

Part-C: Treatment of live bank guarantees and line of credit as claims

33. This paper discusses the issue of treatment of live bank guarantees and line of credit as claims in a corporate insolvency resolution process (CIRP) and solicits comments on the same.

Legal Provisions

34. Clause (6) of Section 3 of the Insolvency and Bankruptcy Code, 2016 (Code) defines the term “claim” to mean the following:

(a) a right to payment, whether or not such right is reduced to judgment, fixed, disputed, undisputed, legal, equitable, secured, or unsecured;

(b) right to remedy for breach of contract under any law for the time being in force, if such breach gives rise to a right to payment, whether or not such right is reduced to judgment, fixed, matured, unmatured, disputed, undisputed, secured or unsecured;

(1) Clause (11) of Section 3 of the Code defines the term “debt” to mean the following:

debt means a liability or obligation in respect of a claim which is due from any person and includes a financial debt and operational debt;

(2) From a plain reading of the aforementioned definition, it can be said either there must be a direct right to payment available with the claimant or in case there is a breach of contract, the remedy for the said breach should provide a right of payment to the aggrieved. It is pertinent to note that in case there is no direct right, there must arise a breach of contract for a right to remedy to arise.

35. Clause (b) of Section 18 of the Code states that it is the duty of the interim resolution professional to receive and collate all the claims submitted by creditors to him, pursuant to the public announcement made under sections 13 and 15. Further, clause (2) of Section 23 of the Code states that the resolution professional shall exercise powers and perform duties as are vested or conferred on the interim resolution professional under this Chapter. Thus, the IRP and the RP are both vested with the duty of receipt and collation of claims as submitted by creditors to them.

36. Clause (1) of Regulation 13 of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) states that “the interim resolution professional or the resolution professional, as the case may be, shall verify every claim, as on the insolvency commencement date, within seven days from the last date of the receipt of the claims…”.

Clarity required

37. The list of creditors in a CIRP must be as accurate as possible. The Hon’ble Supreme Court in the matter of Committee of Creditors of Essar Steel India Limited Vs. Satish Kumar Gupta & Ors. [Civil Appeal No. 8766-67/2019 and other petitions] has held that: ‘All claims must be submitted to and decided by the resolution professional so that a prospective resolution applicant knows exactly what has to be paid in order that it may then take over and run the business of the ’ Thus, it is important that an IP understands and is able to differentiate whether a particular claim is to be admitted or not. Some concerns have come to notice regarding the treatment of live bank guarantees and letter of credit as claims. Keeping these as the perimeter, it requires clarity whether a letter of credit or a live bank guarantee can be included as a claim under CIRP?

38. Black’s Law Dictionary defines letter of credit (LC) in the following words: An instrument under which the issuer (usually a bank), at a customer’s request, agrees to honour a draft or other demand for payment made by a third party (the beneficiary), as long as the draft or demand complies with specified conditions, and regardless of whether any underlying agreement between the customer and the beneficiary is satisfied. LC is a written undertaking by an issuer given to the beneficiary at the request and in accordance with the instructions of applicant to effect payment of a stated amount within a prescribed time limit and against stipulated documents, provided all the terms and conditions of the credit are complied with. The documentary credit of LC may be communicated to the beneficiary by the issuer directly or indirectly it may be done by another bank. The issuer or the bank acting on its behalf makes the payments after satisfying itself that conditions laid down for payment have been met. The applicant in turn reimburses the issuing bank for the payment made to the beneficiary. It is used for one or more transactions usually carried out within a smaller period of time.

39. Section 126 of Indian contract Act, 1872 defines a contract of guarantee as a contract to perform promise or discharge the liability of the third person if he makes any default. The person who promises to perform or discharge the liability of the third person is called the “Surety”. The person for whom guarantee is given is called “Principal debtor” and the person to whom guarantee is given is called the “Creditor”. Bank guarantee (BG) is a tripartite agreement between banker, the beneficiary and the person or the creditor4 in which “Bank” becomes the surety for the transactions between the Debtor and Creditor. A bank guarantee is a written contract given by a bank on the behalf of a customer which undertakes to pay or discharge the liability of the debtor in case of any default. The concept of bank guarantee is basically, introduced for the free flow of the trade as guarantee given by bank secures the creditor from loss and also enables the creditor to claim the debt in case of any default without opting for the cumbersome process of litigation5. These are used to cover contracts that are applicable over a longer time period.

40. From the above, it can be seen that both BGs and LCs are similar kinds of instruments which require the issuers to make certain payments to beneficiaries in case the applicant fails to adhere to the contract agreed upon. The issuers then proceed to recover the payment from applicant through means available to them. In cases where LC/BG is issued in lien of a fixed deposit or collateral security of the applicant, the same is used to recovery dues from the applicant.

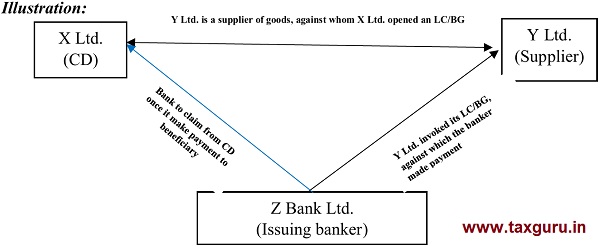

41. It can be said that mere issuing of BGs/LCs does not confer a right to payment to the banks. Such a right arises on the bank as an indemnity only and only when the debtor defaults on his contract with the beneficiary and the banks had to honour their commitment. As can be seen from the below illustration, since the supplier invoked the LC/BG issued in its favour, the CD’s banker is bound to honour the payment and has accordingly made the payment. As the payment was made on behalf of the CD, the CD must indemnify the banker for such payment made.

42. Since there is no direct right to payment for banks arising out of BGs/LCs given and the indirect right to payment arises only when the debtor defaults. Thus, live BGs/LCs cannot be said to fall under the definition of “claims”.

Illustration:

43. In the context of the Code, the treatment of the LC/BG, for which the CD undergoing CIRP is the applicant and their treatment as claims requires clarity. The following scenarios are possible

Scenario – 1: Where the LC/BG was invoked by the beneficiary before the insolvency commencement date (ICD) of the CD.

Since the creditor invoked its LC/BG and the bank has made the payment against such invocation, the banker has a right to be indemnified by the CD. Since the LC/BG has been invoked, it ceases to remain live and the right to payment being established even before the commencement of insolvency proceedings against the CD, by virtue of Sec. 6(3) it becomes a “claim” against the CD as on the date of insolvency commencement.

Scenario – 2: Where the LC/BG remains live and remains uninvoked during CIRP.

Since the beneficiary has not invoked the LC/BG, it remains live and uninvoked for its natural life. Since, the bank has not made any payment to the supplier, there is no question of the CD indemnifying the banker, as there is no right created for the banker. However, any live LC/BG has the possibility of being invoked at anytime and are hence reflected as a liability in the CDs balance sheet and the same may be considered as a contingent liability and acted upon accordingly.

Scenario – 3: Where the LC/BG is invoked by the beneficiary during the corporate insolvency resolution process.

Since the creditor invoked its LC/BG and the bank has made the payment against such invocation, the banker has a right to be indemnified by the CD and the right to payment is established and it qualifies as a claim. Market practice is that RPs have admitted such claims even when submitted after the 90-day period for claim submission has lapsed and in some cases claims have been admitted with approval of the Adjudicating Authority.

44. Any LC/BG which are live are part of information memorandum prepared by the RP and therefore, admission of claim under Scenario 2 and 3, may not be taken as burdening the resolution applicant with unexpected liabilities.

45. Proposed Amendment

It is proposed to provide in the regulations that in case, the LC/BG is invoked by the beneficiary during the CIRP, the issuer shall be eligible to submit its claim to the resolution professional.

46. Economic Analysis

The proposed amendment would help by removing ambiguity regarding rejection of claims pertaining to bank guarantee and letter of credit. This would help enhance faith amongst stakeholders in CIRP.

47. Public Comments

The Board accordingly solicits comments on the following:

(i) Do you agree to the treatment of LC/BG in scenario 1?

(ii) If No, provide reasons/issues and alternative available?

(iii) Do you agree to the treatment of LC/BG in scenario 2?

(iv) If No, provide reasons/issues and alternative available?

(v) Do you agree to the treatment of LC/BG in scenario 3?

(vi) If No, provide reasons/issues and alternative available?

48. After considering the comments, the Board proposes to make regulations under clauses (aa) and (t) of subsection (1) of section 196 of the Code.

49. Submission of comments

Comments may be submitted electronically by 17th September 2021. For providing comments, please follow the process as under:

(i) Visit IBBI website, www.ibbi.gov.in;

(ii) Select ‘Public Comments’;

(iii) Select ‘Discussion paper – CIRP Aug 21’

(iv) Provide your Name, and Email ID;

(v) Select the stakeholder category, namely, –

(a) Corporate Debtor;

(b) Personal Guarantor to a Corporate Debtor;

(c) Proprietorship firms;

(d) Partnership firms;

(e) Creditor to a Corporate Debtor;

(f) Insolvency Professional;

(g) Insolvency Professional Agency;

(h) Insolvency Professional Entity;

(i) Academics;

(j) Investor; or

(k) Other

(vi) Select the kind of comments you wish to make, namely,

a) General Comments; or

b) Specific Comments.

(vii) If you have selected ‘General Comments’, please select one of the following options:

a) Inconsistency, if any, between the provisions within the regulations (intra regulations);

b) Inconsistency, if any, between the provisions in different regulations (inter regulations);

c) Inconsistency, if any, between the provisions in the regulations with those in the rules;

d) Inconsistency, if any, between the provisions in the regulations with those in the Code;

e) Inconsistency, if any, between the provisions in the regulations with those in any other law;

f) Any difficulty in implementation of any of the provisions in the regulations;

g) Any provision that should have been provided in the regulations, but has not been provided; or

h) Any provision that has been provided in the regulations but should not have been provided.

(viii) And then write comments under the selected option.

50. If you have selected ‘Specific Comments’, please select para number and then sub-para number and write comments under the selected para/sub-para number.

51. You can make comments on more than one para/sub-para, by clicking on more comments and repeating the process outlined above from point 47(vi) onwards.

52. Click ‘Submit’ if you have no more comments to make.

Annexure

CODE OF CONDUCT FOR COMMITTEE OF CREDITORS

1. A member of the committee of creditors, while discharging its duties shall abide by the following code of conduct, as individual and jointly with other members of the committee.

2. A member of the committee shall:

a. maintain integrity in performing its roles and functions under the Code.

b. must not misrepresent any facts or situations and should refrain from being involved in any action that is detrimental to the objectives of the Code.

c. must maintain objectivity in exercising decisions on the subject matter bestowed to the committee under the Code.

d. must disclose the details of any conflict of interests to the stakeholders, whenever it comes across such conflict of interest during a process.

e. not acquire, directly or indirectly, any of the assets of the debtor, nor knowingly permit any relative of the committee member to do so, without making a disclosure to the stakeholders.

f. not adopt any illegal or improper means to achieve any objective.

g. co-operate with the insolvency professional in discharging his duties under the Code.

h. not influence the decision or the work of committee so as to make undue gain or advantage for itself or its related parties.

i. disclose the existence of any pecuniary or personal relationship with any stakeholders entitled to distribution, as soon as it becomes aware of it.

j. ensure that decisions are made without any bias, favour, fear, coercion, undue influence or conflict of interest.

k. maintain transparency in all activities and decision making.

l. respect the moratorium and creditors who maintain the accounts of the CD shall not adjust the receipts of the CD during CIRP for past due in violation of moratorium.

m. become fully aware of the provisions of the Code and rules/regulations. It must have complete knowledge of the role and responsibilities assigned to it by the Code.

n. nominate representative with sufficient authorization to participate in meetings and make decisions during the process.

o. participate actively, constructively and effectively in deliberations and decision making.

p. not conceal any material information or knowingly make a misleading statement to the Board, the Adjudicating Authority or any stakeholder, as applicable.

q. ensure that timelines provided in the Code and Regulations are not breached.

r. facilitate the appointment of various professionals within timelines prescribed under the Code and the Regulations.

s. cooperate with the insolvency professionals in seeking various approvals from Adjudicating Authority within model timeline prescribed under the Code and Regulations.

t. ensure complete confidentiality of information that they receive or come across as part of the process at all times. It shall not share any information with any person who is not authorised to receive such information and without the consent of the relevant parties or as required by law.

u. at all times respect the privacy of any information.

v. take necessary measures to ensure that the insolvency resolution process cost is reasonable, keeping in balance the need to conduct a smooth and timely resolution process.

w. ensure that their cost associated with the process is not booked as insolvency resolution process cost.

x. not withhold release of insolvency resolution process cost, including fee of professionals.

y. adhere to the Code and regulations in performing their roles and functions under the Code at all times.

z. bear the collective interest of all stakeholders in mind in all activities and decision making.

aa) respect the demarcation of roles and responsibilities assigned by the Code to different stakeholders and shall not, either directly or indirectly interfere with the functions of the insolvency professional.

bb) at all times endeavor to ensure that timelines prescribed in the Code and Regulations are adhered to.

cc) not contravene any provisions, of the Code, regulations, instructions, guidelines and circulars issued by the Board from time to time.

dd) endeavor to protect the CD as a running business and its assets and take necessary steps to protect the value of the assets of the CD.

ee) extend interim finance to the extent required for completion of the process.

1 https://ibbi.gov.in/webfront/notice_alongwith_subcommittee_report_for_public_comments.pdf

2 https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10588&Mode=0

3 https://www.bankofindia.co.in/UploadData/TenderFiles/Publication%20for%20Sale%20of%20NPA%20 Tranche%20-%2032019-12-02%20044845024.pdf https://www.sbi.co.in/documents/39129/55789/15032021 WEB+NOTICE.pdf/d18759fc-c3ce-5f47-a2ad-8860b77c2999?t=1615788977176

4 B.B. Patel v. Nexim Exports Pvt. Ltd., BC II (2000) 559

5http://docs.manupatra.in/newsline/articles/Upload/1A60C2E6-874F-4655-8821-CA4915F9D4F6.-%20banking.pdf