A. PROVISION FOR TRANSFER OF DIVIDEND

As per Provisions of companies act 2013 where

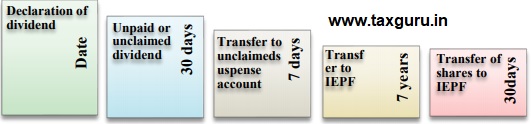

-dividend has been declared by a company according to section 124 of Companies Act

-but is unclaimed by shareholder within 30 days of date of declaration company shall

-transfer such unclaimed dividend within 07 days of expiry of such 30 days

-to a special bank account named under the style “unpaid Dividend Account”

Company after transferring dividend to unclaimed suspense account shall file details of the amount transferred along with list of shareholders in form IEPF-1 within 30 days of such transfer

B. Appointment of Nodal Officer

- At first company shall appoint a Nodal officer who shall be a Company secretary or Director or CFO of the company,

- The nodal officer shall be appointed through form IEPF-2 and if the company has already appointed a nodal officer

- then any change in the status of nodal officer shall be communicated through the form IEPF-2 within 7 days of such change along with board resolution.

- However any company can also appoint one or more Deputy nodal officers who can assist nodal officer in processing the transfer of amount and shares or claiming of shares from IEPF.

C. Transferring the amount of unclaimed from continuous 7 years

Company shall within a period of sixty days after the holding of Annual General Meeting or the date on which it should have been held

⇓

and every year thereafter till completion of the seven years period, identify the unclaimed amounts on the date of holding of Annual General Meeting

⇓

furnish a statement or information of unclaimed dividend along with list of shareholders through Form No. IEPF -2.

Please note that company shall separately furnish and upload on its own website list of the shareholders whose dividend is being transferred to IEPF.

| Current Scenario for filing of the forms related to IEPF.

According to the latest circular due dates of filing the forms has been extended till 30th September,2020 without payment of additional fees |

D. Shares and dividend which are not liable to be transferred to IEPF

♦ Where there is a specific order of Court or Tribunal or statutory Authority restraining any transfer of such shares and payment of dividend, the company shall not transfer such shares to the Fund (even if they are unclaimed for more than 7 years or more.

♦ The company shall furnish details of such shares and unpaid dividend to the authority in Form No. IEPF 3 within thirty days from the end of financial year.

E. Manner for transfer of shares to IEPF

where shares are in physical form

Company shall inform at the latest available address, the three months before the due date of transfer of shares along with ewspaper avertisement

The share shall be credited to an IEPF suspense account (on the name of the company) with one of the depository participants (NSDL/CDSL) as may be identified by the IEPF Authority within a period of thirty days of such shares becoming due to be transferred to the Fund:

Please note that if shareholder has encashed any dividend warrant during the last seven years, such shares shall not be required to be transferred to the Fund even though some dividend warrants may not have been encashed.

where shares are held in demat form

The Company shall inform the depository by way of corporate action, where the shareholders have their accounts for transfer in favour of the Authourity

on receipt of such intimation, the depository shall effect the transfer of shares in favour of DEMAT account of the Authority.

The details of the shares (physical/demat) transferred to IEPF shall be communicated in the form IEPF-4 within 30 days of the corporate action by the Depositary.

F. Dividend due for transfer in next financial year

The company shall furnish a statement to the Authority in Form No. IEPF 6 within thirty days of end of financial year stating therein the amounts due to be transferred to the Fund in next financial year

G. Introduction of form IEPF-7

In case the shares have already been transferred to the IEPF Suspense Account, in case of further dividends which will be credited to the Fund, IEPF 7 need to be filed within 30 days of such transfer Other cases for filing of the form are:-

If the company is getting delisted

If the company is being would up

Any further dividend received on such shares shall be credited to the Fund and a separate ledger account shall be maintained for such proceeds.

H. Introduction of form IEPF-1A

♦ The companies which have transferred any amount referred to in clauses (a) to (d) of subsection (2) of section 205C of the Companies Act, 1956

♦ but have not filed the statement or have filed the statement in any format other than in excel template

♦ shall submit details in Form No. IEPF – 1A along with excel template within sixty days of notification of these amended rule i.e 20th August, 2019 .”

IEPF Authority has provided extension in filing of this form as per latest circular last date of filing was upto 31.12.2019

Author – Shaifali Chawla Contact – E-mail- shaifali.chawala@gmail.com

For any Query feel free to contact. Reviews will be highly helpful

The company was public limited while declaring the dividend 2013-14 and later converted to private limited after two years in 2015-16. Now unclaimed dividend lying in the account and its completed 7 years. How to transfer the amount?. Is IEPF applicable to private limited? How can i generate the challan to transfer the money to the IEPF account? SRN is not generating on offline payment method of MCA. Please advise.

what to do in case IEPF-1 is rejected and amount is already transferred w.r.t. the said form. We cannot file for re-submission or fresh IEPF-1.

Now this what I called capsule easy to intake.

Very well explained ! Really helpful 🍻

Good explanation..done well👍🏻

Nice explanation..

Quoted elaborately, easy to understand.

Very useful and clear understanding. Thanks.