Dividend is defined under Section 2(35) of the Companies Act, 2013 as “Dividend includes any Interim Dividend”

Cambridge Dictionary defines “Dividend as a payment by a company of a part of its profit to the people who own shares (= units of ownership) in the company”

In this article we will discuss the provisions of the Dividend as explained in the Chapter VIII- “Declaration and Payment of Dividend” of the Companies Act, 2013 ranging from Section 123 to 127 of the act (excluding section 126 pertaining to Investor Education and Protection Fund, which we will discuss in next article)

Section 123- Declaration of Dividend

- Dividend shall be paid out of

- The current year’s profit or earlier year’s profit or both as calculated below:

| Profit Before Depreciation | XXX |

| Less: Depreciation as per Schedule II | XXX |

| Less: Unrealised Profit | XXX |

| Less: Notional gain or revaluation of assets | XXX |

| Less: Change in carrying amount of assets and Liability | XXX |

| Less: Set-off of previous loss and depreciation not provided for | XXX |

| Profit available for Distribution | XXX |

-

- Money provided by Central or state Government for declaration of dividend in pursuance of the guarantee given by that government.

- The accumulated profit and transferred to the free reserves, subject to the following guidelines and checks:

> The rate of dividend declared shall not exceed the average of the rate of dividend declared in the immediately preceding 3 years

| Particulars | Scenario I | Scenario II | Scenario III |

| Preceding 1 year | 5% | Not declared | 0% |

| Preceding 2 year | 6% | Not declared | 6% |

| Preceding 3 year | 7% | Not declared | 7% |

| Average | 6% | NA | 4.33% |

| Maximum Rate of Dividend | 6% | Any rate may be declared | 4.33% |

> Other Conditions

| Maximum amount to be withdrawn from accumulated profits | – 1/10th of Paid up Capital and free reserve as per latest Audited Balance Sheet

– Balance Reserve should be atleast 15% of Paid up Capital as per latest ABS. |

| Order of adjustment | Set off of the losses of the FY in which dividend is declared |

- Interim Dividend

Between Close of FY and AGM or Any period during the FY

Dividend can be declared by Board of Directors out of the Surplus in the Profit and Loss account or Out of profit of the Financial Year for which interim dividend is sought to be declared or out of profits generated in the financial year till the quarter preceding the date of declaration of the interim dividend

Provided that in case the company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim dividend shall not be declared at a rate higher than the average dividends declared by the company during the immediately preceding three financial years.

The same has been explained above in the table

- Other Conditions for Declaration of Dividend

-

- Dividend can be paid only from its free reserves and not from other reserves

- Amount of Dividend, including, interim dividend shall be deposited in a separate Bank account within Five days of declaration.

- Dividend shall be payable only to the registered shareholder or to his order or to his Banker and shall not be payable except in cash.

Provided that nothing in this sub-section shall be deemed to prohibit the capitalisation of profits or reserves of a company for the purpose of issuing fully paid-up bonus shares or paying up any amount for the time being unpaid on any shares held by the members of the company

-

- Company should not be defaulter on account of Section 73 (Prohibition on Acceptance of Deposits from Public) and Section 74 (Repayment of Deposits, etc., Accepted before commencement of the Act).

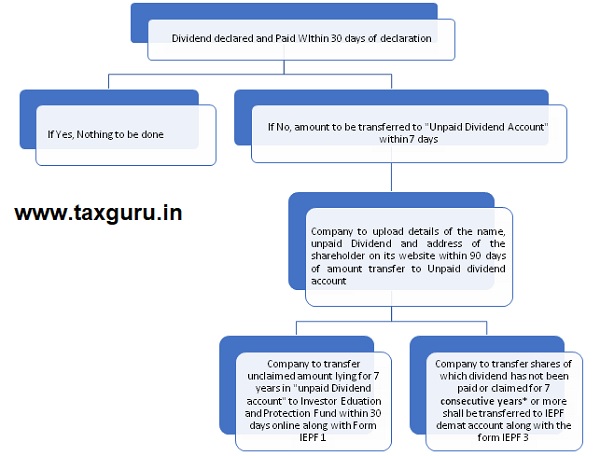

Section 124: Unpaid Dividend Account

* For the removal of doubts, it is hereby clarified that in case any dividend is paid or claimed for any year during the said period of seven consecutive years, the share shall not be transferred to Investor Education and Protection Fund.

If a company fails to comply with any of the requirements of this section, the company shall be punishable with fine which shall not be less than five lakh rupees but which may extend to twenty-five lakh rupees and every officer of the company who is in default shall be punishable with fine which shall not be less than one lakh rupees but which may extend to five lakh rupees.

Section 126 Right to Dividend, Rights Shares and Bonus Shares to be Held in Abeyance Pending Registration of Transfer of Shares

Where any instrument of transfer of shares has been delivered to any company for registration and the transfer of such shares has not been registered by the company, it shall, notwithstanding anything contained in any other provision of this Act,—

(a) transfer the dividend in relation to such shares to the Unpaid Dividend Account referred to in section 124 unless the company is authorised by the registered holder of such shares in writing to pay such dividend to the transferee specified in such instrument of transfer; and

(b) keep in abeyance in relation to such shares, any offer of rights shares under clause (a) of sub-section (1) of section 62 (Further Issue of Share Capital) and any issue of fully paid-up bonus shares in pursuance of first proviso to sub-section (5) of section 123.

Section 127 Punishment for Failure to Distribute Dividends

Where a dividend has been declared by a company but has not been paid or the warrant in respect thereof has not been posted within thirty days from the date of declaration to any shareholder entitled to the payment of the dividend, every director of the company shall, if he is knowingly a party to the default, be punishable with imprisonment which may extend to two years and with fine which shall not be less than one thousand rupees for every day during which such default continues and the company shall be liable to pay simple interest at the rate of eighteen per cent per annum during the period for which such default continues:

Provided that no offence under this section shall be deemed to have been committed:—

(a) where the dividend could not be paid by reason of the operation of any law;

(b) where a shareholder has given directions to the company regarding the payment of the dividend and those directions cannot be complied with and the same has been communicated to him;

(c) where there is a dispute regarding the right to receive the dividend;

(d) where the dividend has been lawfully adjusted by the company against any sum due to it from the shareholder; or

(e) where, for any other reason, the failure to pay the dividend or to post the warrant within the period under this section was not due to any default on the part of the company.]