Ministry of Corporate affairs is very strict nowadays about the money laundering concept and has decided to take all the details of outstanding money which still falls into the Companies Balance sheet as on 22.01.2019 from 01.04.2014 till 31.03.2019, accordingly Ministry of Corporate affairs has introduced a concept of revised DPT 3 form and ask for all Companies except Government Companies to file ONETIME return of all its outstanding money lying into the Company Balance sheet.

Now the common question which comes in every mind will be try to brief out by the author through this note.

1. Whether DPT 3 should be filed twice for the Financial Year 2018-19 or single DPT 3 is sufficient?

The brief note on the above question is as follows:

16 Return of Deposits to be Filed with the Registrar.

Every company to which these rules apply, shall on or before the 30th day of June, of every year, file with the Registrar, a return in Form DPT-3 along with the fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

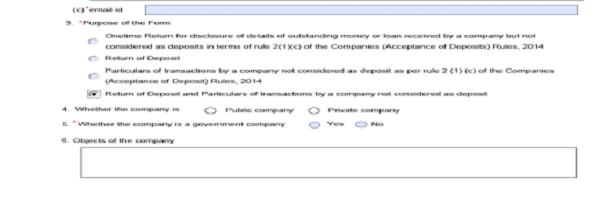

1[Explanation.- It is hereby clarified that Form DPT-3 shall be used for filing return of deposit OR particulars of transaction not considered as deposit OR both by every company other than Government company.]

(Inference: This clearly summarize that now every Company except Government Company required to report all its transaction whether it is deposit or not. So both the above details can be submit through only one DPT 3 by clicking on 4th option of 3rd column)

1 .Inserted by the Companies (Acceptance of Deposits) Amendment Rules, 2019 Dated 22nd January 2019

By virtue of Companies (Acceptance of Deposits) Amendment Rules, 2019 dated 22.01.2019, Sub Rule (3) of Rule 16(A) is inserted which is as follows:

“(3) Every company other than Government company shall file a ONETIME RETURN of outstanding receipt of money or loan by a company but not considered as deposits, in terms of clause (c) of sub-rule 1 of rule 2 from the 01.04.2014 to the date of publication of this notification in the Official Gazette (till 31.03.2019), as specified in Form DPT-3 within ninety days from the date of said publication of this notification (31.03.2019) along with fee as provided in the Companies (Registration Offices and Fees) Rules, 2014.”.

General Circular No. 05/2019: Filing of one time Return in DPT -3 Form – reg

As per Rule 16A(3) of the Companies (Acceptance of deposit) Rules, 2014 “every company other than Government company shall file a ONETIME RETURN of outstanding receipt of money or loan by a company but not considered as deposits, in terms of clause (c) of sub-rule 1 of rule 2 from the 01st April, 2014 to the date of publication of the notification in the Official Gazette, as specified in Form DPT-3 within ninety days from the date of said publication of this notification along with the fee as provided in the Companies (Registration Offices and Fees) Rules, 2014″.

It may also be noted that data on deposits should be filed upto 31st March, 2019 (as opposed to 22nd January, 2019 which was originally indicated in the said Rule). Rule change is being issued separately.

So by virtue of the above analysis it is hereby confirmed that for a Company who is required to report its transactions which are deposit shall file 2 returns. One is for ONE TIME RETURN and second is for Transactions considered as Deposit.

However for those Companies which does not having any Deposit Transaction shall file only ONETIME Return and required to file only one DPT 3.

The last date to report ONETIME RETURN DPT 3 shall be within 90 days from 31.03.2019 (i.e. 29.06.2019).

The last date to report ANNUAL RETURN DPT 3 shall be 30.06.2019.

Following are the details required for ONETIME RETURN

1. Net Worth as per the latest audited balance sheet preceding the date of the return and the calculation shall be as follows:

a)

(i) Paid up share capital

(ii) Free reserves

(iii) Securities Premium Account

(b)

(i) Accumulated Loss

(ii) Balance of deferred revenue expenditure

(iii) Accumulated un provided depreciation

(iv) Miscellaneous expense and preliminary expenses

(v) Other intangible assets

(c) Net worth (a) – (b)

2. Particulars of charge

(a) Date of entering into trust deed

(b) Name of the trustee

(c) Short particulars of the property on which change is created for securing depositors

(d) Value of the property

3. Total amounts of outstanding money or loan received by a company but not considered as deposits in terms of rule 2(1)(c) of the Companies (Acceptance of Deposits) Rules, 2014 as specified in rule 16(A)(3)

So please complete your filing requirement before 29th June 2019 and become a part of good corporate governance as the step was taken by the Ministry to wipe out the shell companies.

The author will be available at +91-9992693555 or mail us at sdeepak.cs@gmail.com.

Disclaimer – This article is for the purpose of information and shall not be treated as solicitation in any manner and for any other purpose whatsoever. It shall not be uses as legal opinion and not to be used for rendering any professional advice

Author Bio

Nice Artilcle