Charge Under Companies Act, 2013

Charge specially gives security and empower the charge holder that in case the Company makes a default for the repayment of the loan than chargeholder can get the claim amount from the security which was charged by the Company in favour of the charge holder.

Filing of Charge is necessary to secure the lender as well as to secure the third party that as and when any third party dealing with the same property it must be aware that the property is already under charged with some lender and before executing the transaction all the charge details must be agreed with all the parties.

In other words a charge is a right created by any person including a company referred to as “the borrower” on its assets and properties, present and future, in favour of a financial institution or a bank, referred to as “the lender”, which has agreed to extend financial assistance.

As per Section 2(16) of Companies Act, 2013, “Charge” means an interest or lien created on the property or assets of a company or any of its undertakings or both as security and includes a mortgage.

Section 77 reads with Rule 3 of Registration of charges Rules 2014

Section 77 talks about on 2 aspects

1. Charge in case of debenture – filed in the form CHG 9

2. Charge other than debenture – filed in the form CHG 1

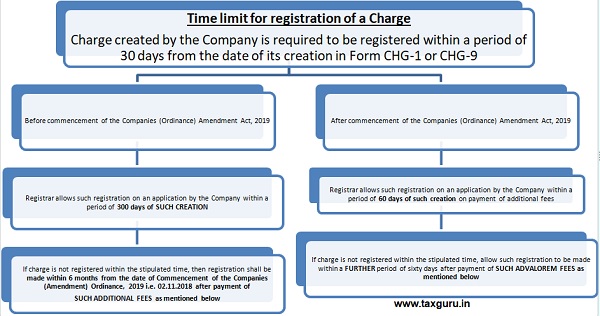

But in both the cases the charge must be filed within 30 days from the date of creation of charge or within 30 days from the date of modification in existing charge

Page Contents

Timeline of filing of Registration of Charge

Imp Note:

1. we want to highlight here one important note in the case of charges created before the commencement of Ordinance and here the law maker intention is to restrict for filing of CHG 1 by latest of 02.05.2019 because the initial days of 300 days was started from creation whereas the second proviso allow six months from the date of commencement of Ordinance and that six months shall elapse on 02.05.2019, So on those days the last date to file CHG 1 was 02.05.2019 and the advalorem fees was not levied on those charges as the law maker imposes the advalorem fees on or after 01.08.2019.

2. As on the current situation i.e. in the year 2020 the CHG 1 can be filed maximum within a period of 120 days and after the expiry of 120 days Company shall unable to file CHG 1.

Fees for filing charge documents

The important point here to be described is that as on current date i.e. in year 2020 the situation 1 is not relevant as the time period has already expired but the same shall be mentioned below for knowledge sharing purpose.

A. charges created or modified before the 2nd November, 2018, and allowed to be filed within a period of three hundred days of such creation or six months from the 2nd November, 2018, as the case may be, the following ADDITIONAL FEES shall be payable:-

| Sl. No. | Period of delay | Additional Fee applicable |

| 1. | Up to 30 days | 2 times of normal fees |

| 2. | More than 30 days and up to 60 days | 4 times of normal fees |

| 3. | More than 60 days and up to 90 days | 6 times of normal fees |

| 4. | More than 90 days and up to 180 days | 10 times of normal fees |

| 5. | More than 180 days | 12 times of normal fees |

B. Charges created or modified on or after the 2nd November, 2018:-

i. The following ADDITIONAL FEES shall be payable up to 31st July, 2019, by all companies:-

| Sl.

No. |

Period of delay | Additional/Advalorem Fees applicable |

| 1. | Up to 30 days | 2 times of normal fees |

| 2. | More than 30 days and up to 60 days | 4 times of normal fees |

| 3. | More than 60 days and up to 90 days | 6 times of normal fees |

ii. the following ADVALOREM FEES shall be payable with effect from 1st August, 2019:-

| Sl.

No. |

Period of delay | Small Companies and One Person Company | Other than Small Companies and One Person Company |

| 1. | Up to 30 days | 3 times of normal fees | 6 times of normal fees |

| 2. | More than 30 days and up to 90 days | 3 times of normal fees plus an ad valorem fee of 0.025 per cent. of the amount secured by the charge, subject to the maximum of one lakh rupees. | 6 times of normal fees, plus an ad valorem fee of 0.05 per cent. of the amount secured by the charge, subject to the maximum of five lakh rupees”.] |

As per the Rule 6 the Registrar shall issue a certificate of registration of charge in 2 cases –

- Where a charge is registered with the Registrar under sub-section (1) of section 77 or section 78, he shall issue a certificate of registration of such charge in Form No.CHG-2

- Where the particulars of modification of charge is registered under section 79, the Registrar shall issue a certificate of modification of charge in Form No. CHG-3

Now lets suppose Company is not filing the Charge or fails to file the charge within 30 days before the Registrar, now section 78 gives remedy to the chargeholder and according to section 78 the person in whose favor the charge is created may apply to the Registrar for registration of the charge along with the instrument created for the charge, within such time and in such form and on payment of additional/advalorem fees as discussed above and the Registrar may, on such application, within a period of fourteen days after giving notice to the company, unless the company itself registers the charge or shows sufficient cause why such charge should not be registered, allow such registration on payment of such fees.

Register of Charges

Liability on the Registrar – Section 81 mandate the Registrar that the registrar shall in respect of every company, keep a register containing particulars of the charges registered and that particulars is being maintained on the Ministry of Corporate Affairs portal i.e. www.mca.gov.in

Liability on the Company – Every Company shall have to maintain register of charge in form CHG-7 along with copy of the instrument creating the charge at its registered office of the Company which shall include all types of charges.

The entries in the register of charges maintained by the company shall be made forthwith after the creation, modification or satisfaction of charge, as the case may be.

Entries in the register shall be authenticated by a director or the secretary of the company or any other person authorised by the Board for the purpose.

The register of charges shall be preserved permanently and the instrument creating a charge or modification thereon shall be preserved for a period of eight years from the date of satisfaction of charge by the company.

Now above we have read in detail about the creation of charge, now let us understood about the satisfaction/close of a particular charge registered before the Registrar.

Satisfaction of Charges

Satisfaction of charge means when the tenure of financial assistance has been expired or the instrument of charge has been revoked by both the parties before the expiry of tenure with mutual consent, in that case the satisfaction or payment of charge shall be reported to the Registrar of Companies.

Every Company shall give intimation to the Registrar in form CHG-4 of the PAYMENT or SATISFACTION IN FULL of any charge registered before the Registrar within a period of 30 days from the date of such PAYMENT or SATISFACTION IN FULL.

Now here a important point to be noted is that if charge is partially satisfied than in that case CHG 4 shall not be filed and CHG 1 shall be filed for modification in existing charge.

However the registrar may on an application by the Company or the Charge holder may allow a further time period of 270 days after the expiry of 30 days on payment of additional fees.

Penalties and Punishment for Contravention

Section 86 talks about the same and If any company contravenes any provision than following will be the penal consequences:

- company shall be punishable with fine which shall not be less than one lakh rupees but which may extend to ten lakh rupees; and

- every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to six months or with fine which shall not be less than twenty-five thousand rupees but which may extend to one lakh rupees, or with both.

However if a practicing professional wilfully furnishes any false or incorrect information or knowingly suppresses any material information, required to be registered in accordance with the provisions of section 77, he shall be liable for action under section 447.

Rectification by Central Government in Register of Charges

While drafting any law the law maker also need to add the points that in case if Company has expired all the timeline as mentioned in the law than after expiry of all such extended time how the application for registration shall be moved, and in case of charge, Section 87 gives some power to the central government (the powers are delegated to the respective Regional Director).

Section 87 gives power to rectify the mistake made by the Company, but Section 87 can rectify only 2 kinds of mistake:

1. the omission to give intimation to the Registrar of the payment or satisfaction of a charge within a extended period of 300 days i.e. Company fails to file CHG 4 within a period of 300 days;

2. the omission or misstatement of any particulars, in any filing previously made to the Registrar with respect to any such charge or modification i.e. Company has already filed the CHG 1 but made some omission or miss some statement in the filed CHG 1 and the timeline to file the CHG 1 for modification of charge has been expired.

Now in both the above cases Company can file the CHG 8 before the Central government along with the relevant petition and annexures requesting to rectify the mistake made by the Company and the Central government may rectify the mistake on case to case basis.

Now after reading of section 87 we draw a conclusion that CHG 8 shall not be allowed to filed in case if Company fails to file CHG 1 for creation of fresh charge which was earlier allowed. Hence the maximum timeline to create a charge shall be 120 days only.

Essence of each Forms

CHG 1 – filing before the Registrar for creation of new charge or modification in existing charge for other than Debenture.

CHG 2 – certificate of registration of charge issued by the Registrar of Companies.

CHG 3 – certificate of modification in existing charge issued by the Registrar of Companies.

CHG 4 – payment or satisfaction in full of any charge registered before the Registrar of Companies.

CHG 5 – certificate of registration of satisfaction of charge issued by the Registrar of Companies.

CHG 6 – Notice of appointment or cessation of receiver or manager.

CHG 7 – Register of charges made by the Company.

CHG 8 – Application to Central Government for extension of time for filing particulars of modification / satisfaction of charge OR for rectification of omission or misstatement of any particular in respect of creation/ modification/ satisfaction of charge.

CHG 9 – filing before the Registrar for creation of new charge or modification in existing charge for Debenture.

The author is available at +91-9992693555, 0124-4007548 or mail us at sdeepak.cs@gmail.com.

Disclaimer – This article is for the purpose of information and shall not be treated as solicitation in any manner and for any other purpose whatsoever. The entire contents of this document has been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore users of this information are expected to refer to the relevant existing provisions of applicable Laws. The users of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event i shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

Author Bio

In case, existing loan is taken over by another bank, then which charge form will be filed?

what are the consequences in case of late filing of CHG-4 by pvt limited company?

Can Company file Form CHG-4 after 30 days?