As we know India is facing Covid 19 pandemic since March, 2020 and cases are increasing day by day. Central Government have also taken and launched various scheme on time to time basis.

Ministry of Corporate Affairs (MCA) have also relaxed the stakeholders in filling various forms, and in line to the relaxation, MCA have vide its General Circular No. 23/2020 dated 17th June, 2020 have launched the ‘Scheme for relaxation of time for filing forms related to creation or modification of charges under the Companies Act, 2013′ (‘Scheme’) by which relaxation has been granted in filling Form CHG – 1 and Form CHG – 9.

It is to be noted that as per the provisions of Section 77 of the Companies Act, 2013 (“Act”) it is the duty of Company to register for creation/ modification the charge with the Registrar within 30 Days of its creation.

If company fails to register/ modify the charge within the above said time period, the Registrar may allow registering creation/ modification such charge on payment of additional fee within period of 60 days of its creation/ modification.

Even after additional 30 days as in above para, the company fails to register charge; Registrar may allow application for registering for creation/ modification the charge within further extension of 60 days on payment of advalorem fees.

In case, the company fails to register the charge within the period of 30 referred to in sub-section ( 1) of section 77 , the charge holder may file the form related to creation or modification of charge under section 78 of the Act, within the overall timelines for filing of such form under section 77. We can say that registration of creation/ modification of charge is possible only till 120 days of its creation/ modification on payment of additional fee or advalorem fee as the case may be.

Many stakeholders have faced the problems for registering the charge due to Covid 19 Pandemic and Lockdown. Now, as per the Scheme MCA allow to exclude the time period starting from 01st March, 2020 to 30 September, 2020 for the purpose of filling and calculation of fee.

We can analyze this Scheme in various scenarios as under:-

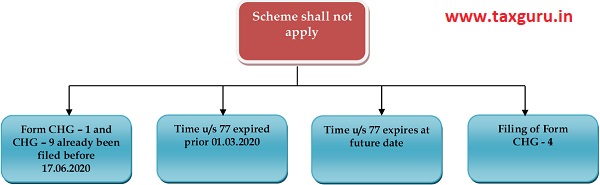

Non Applicability: The Scheme shall not be applicable as under:-

Author Bio